Backyard Keys ADU Loan Program: 2026 Salt Lake City Eligibility, Costs & Application Checklist

By the Dwelling Index editorial team · Last updated: May 27, 2026 · Last verified: May 27, 2026

Published May 27, 2026 · Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not affiliated with Salt Lake City, the Community Reinvestment Agency, or CDCU, and we are not a lender. This page is educational information, not financial, legal, tax, or construction advice.

The bottom line on the Backyard Keys ADU loan program

The Backyard Keys ADU loan program is a Salt Lake City construction loan for owner-occupants building an accessory dwelling unit (ADU) on the city's west side — generally west of I-15 — administered by the nonprofit Community Development Corporation of Utah (CDCU). Official sources describe loans of up to $200,000 at a 3% fixed rate on a 30-year amortization, with a 5-year term plus a possible 5-year extension. To qualify you must own and live on the property, complete the city's Good Landlord training and CDCU financial counseling, and follow one income rule: if your household earns 80% of Area Median Income (AMI) or less, there are no rent restrictions; if you earn more, you must rent either the ADU or your main home at a rate affordable to a household at 80% AMI or below.

This is not a national loan, and it is not a grant — it is money you repay. Funding is limited; the city allocated roughly $2.9 million to the program, enough for only about a dozen-plus full-size loans. Your single most important next step hinges on one thing: is your property west of I-15 inside Salt Lake City limits? If yes, you may be a strong fit. If no, this program can't help you, and you'll want a fallback financing path instead.

Backyard Keys at a glance

| Question | Fast answer |

|---|---|

| Who it's best for | Salt Lake City owner-occupants, west of I-15, building one legal ADU |

| Who it's not for | Anyone east of I-15 or outside SLC limits; non-owner-occupants; investors; short-term-rental plans |

| Maximum loan | Up to $200,000 |

| Interest rate | 3% fixed |

| Amortization | 30 years |

| Term length | 5 years + possible 5-year extension (confirm maturity mechanics with CDCU) |

| Income rule | ≤80% AMI: no rent restriction · >80% AMI: rent ADU or main home affordably to a household at ≤80% AMI |

| Up-front cost | $2,000 origination fee ($200 due as application; rest may be rolled in) + $1,000 minimum personal funds |

| Administrator | Community Development Corporation of Utah (CDCU) / Utah Community Investment Fund |

| Biggest catches | Tiny geographic footprint, limited pilot funding, rent rules above 80% AMI, unresolved forgiveness language |

| First action | Confirm your address is west of I-15 in SLC, then submit CDCU's ADU inquiry form |

Source: Salt Lake City Community Reinvestment Agency (cra.slc.gov) and Community Development Corporation of Utah (cdcutah.org), both verified May 27, 2026.

🗺 Check Your Backyard Keys Fit — Free Eligibility + Funding-Gap Checker

Our Backyard Keys Eligibility + Funding-Gap Checker walks you through the five questions that actually decide this in about three minutes, then tells you exactly what to ask CDCU before you spend a dollar on design. It works on any Salt Lake City address — find out if you're west of I-15 and which income lane you're in.

What is the Backyard Keys ADU loan program?

The short answer: The Backyard Keys ADU loan program is a Salt Lake City Community Reinvestment Agency initiative, administered by the nonprofit Community Development Corporation of Utah (CDCU), that lends qualifying west-side homeowners up to $200,000 at a 3% fixed rate on a 30-year amortization to build an accessory dwelling unit. It is a loan, not a grant, restricted to owner-occupied properties west of I-15 within Salt Lake City boundaries.

“Backyard Keys” is the branding the Salt Lake City Community Reinvestment Agency (CRA) gives to what its own materials also call, more plainly, the ADU Loan Program. The CRA is the city's redevelopment arm; it partnered with CDCU — a long-running local housing nonprofit and certified community development financial institution — and CDCU's affiliate, the Utah Community Investment Fund, to originate and service the loans. In short: the city designed and funds the program, and CDCU is who you apply through and repay.

An accessory dwelling unit (ADU) is a second, smaller, self-contained home on the same lot as a primary house — a basement apartment, a converted garage, an attached addition with its own entrance, or a detached backyard cottage. The program's stated purpose is twofold: add affordable housing on the city's west side, and help west-side homeowners build wealth through the equity and rental income an ADU can generate.

Backyard Keys is not a loan product you shop for like a mortgage. It behaves more like a city housing program with a waitlist: geographic rules, income rules, finite funding, and strings attached in exchange for a below-market rate. You don't get a Backyard Keys loan by having great credit and a big down payment — you get it by fitting a narrow eligibility profile during a window when money is available.

Don't confuse it with the other “backyard” programs

Several U.S. cities run similarly named ADU loan programs that are entirely separate. If you've read “$250,000” or “payments deferred for 30 years” somewhere, you were almost certainly reading about a different city's program.

| Backyard Keys (SLC) | Backyard Builders (Long Beach) | MassHousing ADULP (MA) | |

|---|---|---|---|

| Where | Salt Lake City, west of I-15 | Long Beach, CA (designated areas) | Massachusetts |

| Max loan | $200,000 | Up to $250,000 | Up to $250,000 |

| Rate | 3% fixed | Subsidized (often ~2%) | Conventional + deferred component |

| Administrator | CDCU | LBCIC | MassHousing lenders |

Sources: SLC CRA / CDCU; City of Long Beach; MassHousing. Verified May 27, 2026. The two non-SLC programs are shown for disambiguation only — you cannot apply for them in Utah.

Also important — what Backyard Keys is not:

- Not a general Utah ADU loan — it's specific to Salt Lake City's west side

- Not available nationwide

- Not a guarantee of approval

- Not a building permit — you still go through SLC's full ADU permitting process

- Not permission to run an Airbnb — SLC prohibits short-term-renting an ADU

- Not a grant or guaranteed-forgivable loan (see the forgiveness section)

Who qualifies for the Backyard Keys ADU loan?

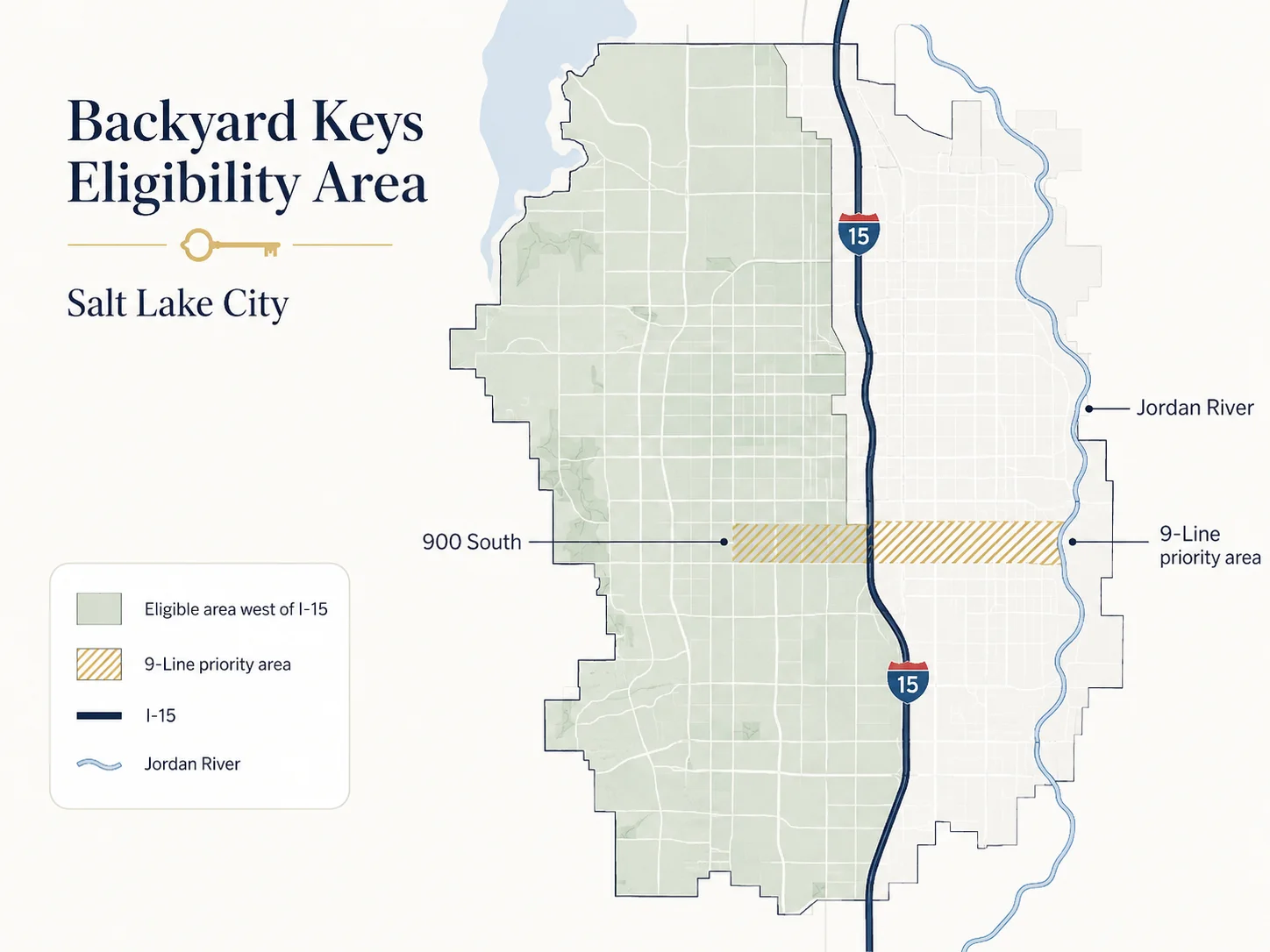

The short answer: You likely qualify if you own and live in a home west of I-15 within Salt Lake City, will keep it as your primary residence, and will complete the city's Good Landlord training and CDCU financial counseling. Properties in the 9-Line Community Reinvestment Area — roughly 900 South between I-15 and the Jordan River — receive priority funding. Households above 80% AMI can still qualify but must rent one unit at an affordable rate.

There are four hard gates, and you must clear all of them. Then there's an income test that changes the terms, not your eligibility.

Gate 1 — Location: west of I-15, inside Salt Lake City

This is the first and most decisive filter. The property must sit west of Interstate 15 and within Salt Lake City's municipal boundaries. Both matter. A home west of the freeway but in West Valley City, South Salt Lake, or unincorporated Salt Lake County is not eligible. Within the eligible area, the 9-Line Community Reinvestment Area gets priority — running roughly along 900 South between I-15 and the Jordan River, covering neighborhoods like Poplar Grove and Glendale.

Gate 2 — Owner-occupancy and primary residence

You must own the property and live on it as your primary residence. You can live in the main house and rent the ADU, or live in the ADU and rent the main house — but you cannot hold the property purely as an investment and rent out both units. This comes from two directions: Salt Lake City's ADU zoning code (§21A.40.200) requires owner-occupancy for single-family ADUs, and Backyard Keys layers its own primary-residence requirement on top.

Owner-occupancy means the legal owner of record lives on the property; the city generally records an affidavit as a condition of the ADU permit.

Gate 3 — Good Landlord training and a rental business license

If you'll rent the ADU (or the main home), Salt Lake City requires participation in its Good Landlord Program and a business license for the rental. The adopted 2026 program terms fold the business-license step into the Good Landlord requirement. Start this early; it's easy to leave until the end and then scramble.

Gate 4 — Financial counseling

CDCU requires participation in financial counseling as part of the program. Treat it as a feature, not a hoop — it's also where you'll get straight answers on the open questions we flag later.

The income test: which lane are you in?

Your household income relative to Area Median Income (AMI) determines your rental obligations, not your basic eligibility.

- At or below 80% AMI: No rent restrictions. Live in the ADU, leave it for family, or rent it to anyone at any price.

- Above 80% AMI: You still qualify, but you must rent either the ADU or the main home at a rate affordable to a household earning 80% AMI or below. CDCU screens tenants before the lease starts and verifies affordability each year.

We translate “80% AMI” into actual 2026 dollars in the next section — because the official program page never does.

Eligibility decision table

| If this is true about you | Likely result | What to do |

|---|---|---|

| Property east of I-15 | Not eligible | Use a fallback financing path |

| West of I-15 but outside SLC limits | Likely not eligible | Confirm your municipal boundary first |

| West of I-15, inside SLC | Potentially eligible | Continue to owner/income/project checks |

| In the 9-Line area | Potential priority | Ask CDCU how priority is applied |

| You won't live on the property | Not eligible | Consider investor/rental financing instead |

| Household ≤80% AMI | Eligible, no rent restriction | Confirm AMI with CDCU |

| Household >80% AMI | Eligible, with rent restriction | Decide whether the rent rule fits your plan |

| You want a short-term/Airbnb rental | Not a fit | SLC prohibits short-term-renting ADUs |

Decision framework assembled by Dwelling Index from CRA and CDCU program rules and SLC Code §21A.40.200. Verified May 27, 2026.

Before financing matters, find out what your lot can actually hold.

See What You Can Build → Get Your Free ADU Report

See What You Can Build → Get Your Free ADU ReportFree, no email required. Setbacks, parking, and ADU type decide your real options long before a loan does.

What is 80% AMI in Salt Lake City? (2026 dollar figures)

The short answer: For the Salt Lake City metro area, 80% of Area Median Income under the 2026 HUD limits ranges from $70,650 for a one-person household to $100,900 for a household of four, up to $133,200 for eight. If your household earns at or below the limit for your size, Backyard Keys imposes no rent restriction.

The official program page states the “80% AMI” rule but never tells you what that means in dollars — so here it is, the single number that decides which income lane you're in. These figures come from Salt Lake City's published 2026 HUD AMI table (HUD FY2026, effective May 1, 2026).

Salt Lake City metro 80% AMI by household size (2026)

| Household size | 80% AMI income limit | 50% AMI (for reference) |

|---|---|---|

| 1 person | $70,650 | $44,150 |

| 2 people | $80,750 | $50,450 |

| 3 people | $90,850 | $56,750 |

| 4 people | $100,900 | $63,050 |

| 5 people | $109,000 | $68,100 |

| 6 people | $117,050 | $73,150 |

| 7 people | $125,150 | $78,200 |

| 8 people | $133,200 | $83,250 |

Source: Salt Lake City Housing Stability Division, 2026 HUD Area Median Income levels (HUD FY2026, effective May 1, 2026). The SLC metro AMI area covers Salt Lake and Tooele counties. Verified May 27, 2026.

How to read it: Find your household size, then compare your gross household income to the 80% AMI figure. Earn at or under it, and you're in the no-rent-restriction lane. Earn over it, and you're still eligible but must rent one unit affordably. For your exact standing, run the numbers on CDCU's official AMI calculator — it's the figure CDCU actually uses to place you.

Is Backyard Keys a grant, a forgivable loan, or a standard loan?

The short answer: Backyard Keys is a repayable loan, not a grant. The public sources currently conflict on whether any partial loan forgiveness exists: the Salt Lake City CRA page references up to 10% forgiveness for rent-restricted ADUs, while the adopted 2026 program changes and CDCU's lender page do not include forgiveness. Confirm forgiveness directly with CDCU in writing before you count on it.

This is the single most important verification point on this page. We read all three documents side by side and tell you plainly that they don't match.

The conflict, stated directly

- The Salt Lake City CRA program page still lists: “Loan Forgiveness — Up to 10% for rent-restricted ADUs.”

- The adopted 2026 CRA program modifications describe changes that omit the partial loan-forgiveness option.

- The CDCU “Finance ADU construction” page — the administering lender's own current page — lists the program terms and does not mention loan forgiveness at all.

| Source | What it says on forgiveness | How to treat it |

|---|---|---|

| SLC CRA public program page | “Up to 10% for rent-restricted ADUs” | Don't rely on this alone — may be outdated |

| Adopted 2026 CRA program changes | Omits the partial-forgiveness option | Suggests forgiveness was removed |

| CDCU lender page (current) | No forgiveness listed | Reinforces caution |

| Your actual loan documents | The only thing that governs your loan | The deciding source — get it in writing |

Conflict identified by Dwelling Index by comparing cra.slc.gov, the adopted 2026 CRA program documentation, and cdcutah.org on May 27, 2026.

When you talk to CDCU, ask directly: “Does my loan include any forgiveness provision, and if so, what triggers it and how much?” Get the answer in writing before it touches a single budget decision. Be skeptical of any contractor or third-party page that advertises “forgivable” Backyard Keys money.

What would the Backyard Keys loan payment be?

The short answer: Using the published 3% fixed rate on a 30-year amortization, a full $200,000 Backyard Keys loan works out to roughly $843 per month in principal and interest. The adopted program terms also describe an interest-only period for the first 12 months during construction, with a construction-period interest reserve funded from loan proceeds. These are illustrative calculations, not a quote from CDCU.

Illustrative monthly payment math

| Loan amount | Approx. monthly P&I at 3%, 30-yr amortization |

|---|---|

| $100,000 | ~$422 |

| $125,000 | ~$527 |

| $150,000 | ~$632 |

| $175,000 | ~$738 |

| $200,000 | ~$843 |

Dwelling Index calculation using a 3% fixed rate amortized over 30 years. Excludes property taxes, insurance, fees, reserves, and construction-period/maturity effects. Verified May 27, 2026.

Up-front costs and the maturity question

Per CDCU's lender page, expect a $2,000 origination fee (of which $200 is payable as the application fee; the remaining $1,800 may be rolled into the loan), plus a requirement that the borrower contribute a minimum of $1,000 in personal liquid funds. The CRA materials also reference a $200/year compliance fee for affordability verification on rent-restricted loans.

The structure to nail down is the term. Both the CRA page and the adopted 2026 program terms describe a 5-year term with a possible 5-year extension layered on top of the 30-year amortization — meaning a balance remains at the end of the term that has to be refinanced, paid off, or resolved. Confirm exactly how this works before you sign:

- What happens at the 5-year maturity if the extension isn't granted, and what qualifies you for the extension?

- Does the $200,000 maximum include the financed portion of the origination fee?

- How is the construction-period interest reserve calculated, and how long is the interest-only period?

- Can the loan be combined with other financing if your project runs past $200,000?

Will $200,000 cover a Salt Lake City ADU?

The short answer: Often, for smaller builds — and not always, for larger ones. Builder-published examples for compact detached models land between roughly $162,000 and $199,000 all-in. But those figures are package-and-install estimates, not independent bids, and a larger custom detached ADU can exceed $200,000 once site work, utility upgrades, permits, design, and contingency are added.

The $200,000 coverage test

One Utah ADU vendor publishes example pricing for models marketed to fit Backyard Keys. We reproduce them here as a reality check — clearly labeled as the builder's own package/install estimates, not independent all-in bids:

| Example model (builder-published) | Size | Published total estimate | Cushion under $200K |

|---|---|---|---|

| Skylight 400 | 400 sq ft | ~$162,000 | ~$38,000 |

| Rondavel 480 | 480 sq ft | ~$178,000 | ~$22,000 |

| Skylight 500 | 500 sq ft | ~$181,000 | ~$19,000 |

| Rondavel 580 | 576 sq ft | ~$199,000 | ~$1,000 |

Source: builder-published examples from a Utah ADU vendor (aduutah.com), captured May 27, 2026. Package-plus-installation estimates from a single vendor, not independent bids. May exclude items below. Use to gauge feasibility, not as a guaranteed all-in cost.

Where the $200,000 tends to land by ADU type

- Internal ADU (e.g., a basement apartment) or garage conversion: Usually the most affordable per square foot because you're reusing existing structure — often the best fit for the cap.

- Attached ADU (an addition with its own entrance): Frequently workable, depending on size and site work.

- Detached new-build cottage: Where the cap gets tight. A modest standardized or prefab unit can fit; a larger custom detached ADU can exceed $200,000.

What advertised ADU prices usually leave out

A builder's “from $XXX,XXX” headline is rarely your all-in number. Before you assume Backyard Keys covers everything, make sure your scope includes:

- Site work (clearing, grading, foundation, drainage)

- Utility laterals and upgrades — water, sewer, gas, power; an electrical panel upgrade is common

- Permit and impact fees

- Design and engineering (even pre-approved plans need a site-specific layout)

- Contingency (10–20% is prudent on any construction project)

- Appliances and furnishings, if not in a quoted package

- Temporary disruption costs if you live on-site during the build

If your project runs past $200,000 — or you're outside the west-side footprint — you still have paths. Compare mortgage-backed ADU financing lanes (cash-out refinance, home-equity, and renovation loans) so you can set a realistic budget before you fall in love with a floor plan.

Approval and terms are never guaranteed. This link is to an affiliate financing partner.

How many Backyard Keys loans are actually available?

The short answer: The city allocated about $2.9 million to the program — roughly $1.9 million from 9-Line project-area funds and $1 million for other west-side properties. At the full $200,000 maximum, that's only about 14 full-size loans before fees, reserves, and varying project sizes are accounted for. This is a small pilot, and funding moves on a first-ready, first-funded basis.

This is the math the official pages don't show you, and it's the reason “join the list early” is real advice rather than a sales line.

| If the average loan is… | Approx. projects the ~$2.9M funds |

|---|---|

| $200,000 (the max) | ~14 |

| $175,000 | ~16 |

| $150,000 | ~19 |

| $125,000 | ~23 |

Dwelling Index calculation using the $2,913,215 allocation described in the adopted 2026 CRA program documentation ($1,913,215 from 9-Line funds + $1,000,000 from west-side funds). Actual loan counts depend on project sizes, repayments, fees, reserves, and administration. Verified May 27, 2026.

The takeaway isn't panic — it's timing. A program this size fills quietly. If you're eligible and serious, getting your inquiry in and your training started early is the difference between catching a funding window and missing it.

What rent restrictions apply if you earn above 80% AMI?

The short answer: If your household earns at or below 80% AMI, Backyard Keys imposes no rent restriction. If you earn above 80% AMI, you must rent either the ADU or your primary home at a rate affordable to a household earning 80% AMI or below for the term of the loan. CDCU screens tenants before the lease begins and verifies their income annually.

This is the trade the program asks of higher earners: a below-market 3% loan in exchange for keeping one unit affordable. Whether that's a fair deal depends entirely on your goals. Planning to house a parent or adult child? The rent rule may be irrelevant. Planning to maximize income from a market-rate tenant? The restriction directly affects your returns, and you should price it out before you commit.

What “affordable to 80% AMI” actually means

A unit is generally considered affordable when a household spends no more than about 30% of its income on housing. So the affordable rent ties back to the 80% AMI figures above, adjusted for the unit's size. CDCU sets and verifies the exact figure for your loan. Ask directly: “What rent schedule applies to my rent-restricted unit, and how is tenant income verified?”

What Salt Lake City ADU zoning rules can block your project?

The short answer: Backyard Keys financing doesn't override Salt Lake City's ADU rules. Under SLC Code §21A.40.200 you still need a building permit, owner-occupancy, and compliance with size, setback, height, and parking standards, and you cannot rent the ADU short-term. A detached ADU may not exceed 1,000 square feet of gross floor area.

A loan approval and a zoning approval are two different things. You can have the money lined up and still be stopped by a setback, a utility issue, or a height limit.

Size, setbacks, height, and parking

- One ADU per single-family property, owner-occupancy required.

- Detached ADU cap: 1,000 sq ft gross floor area (ceiling, not a guarantee).

- 3-foot side and rear setbacks for detached ADUs (typical).

- 17-foot height limit (base); up to ~24 ft pitched / 20 ft flat with additional setback conditions.

- One off-street parking stall required; waived/reduced within ¼ mile of a transit stop or ½ mile of a city-designated bicycle lane.

- No minimum lot size — but setbacks, height, parking, utilities, easements, and building code can still block or shrink a project.

- Short-term rentals prohibited — no Airbnb-style use; long-term rentals (30+ days) are permitted where owner-occupancy is met.

- Building permit required before construction; public-utilities review applies.

| SLC ADU rule (§21A.40.200) | What to check |

|---|---|

| Number of ADUs | One per single-family property |

| Owner-occupancy | Required (limited exceptions) |

| Detached ADU size | May not exceed 1,000 sq ft gross floor area |

| Setbacks (detached) | 3 ft side/rear (typical) |

| Height (detached) | 17 ft base; up to ~24 ft pitched / 20 ft flat with added setbacks |

| Minimum lot size | None — but other standards still apply |

| Parking | 1 stall; waived/reduced near transit or bike routes |

| Short-term rental | Prohibited |

| Permit | Building permit required; public-utilities review applies |

Source: Salt Lake City Code §21A.40.200 and SLC Building Services ADU resources. Verified May 27, 2026.

Pre-approved plans help — they don't approve your site. Salt Lake City publishes a list of pre-approved ADU standard plans (which includes a 775-square-foot two-bedroom plan from Nest Tiny Homes) that can speed permitting. But the city is explicit that using a listed plan does not eliminate site review, fees, or code compliance, and is not a city endorsement of any designer.

Loan approval and zoning approval are not the same thing.

Check your property → get your free ADU report.

See What You Can Build → Get Your Free ADU ReportHow do you apply for the Backyard Keys ADU loan?

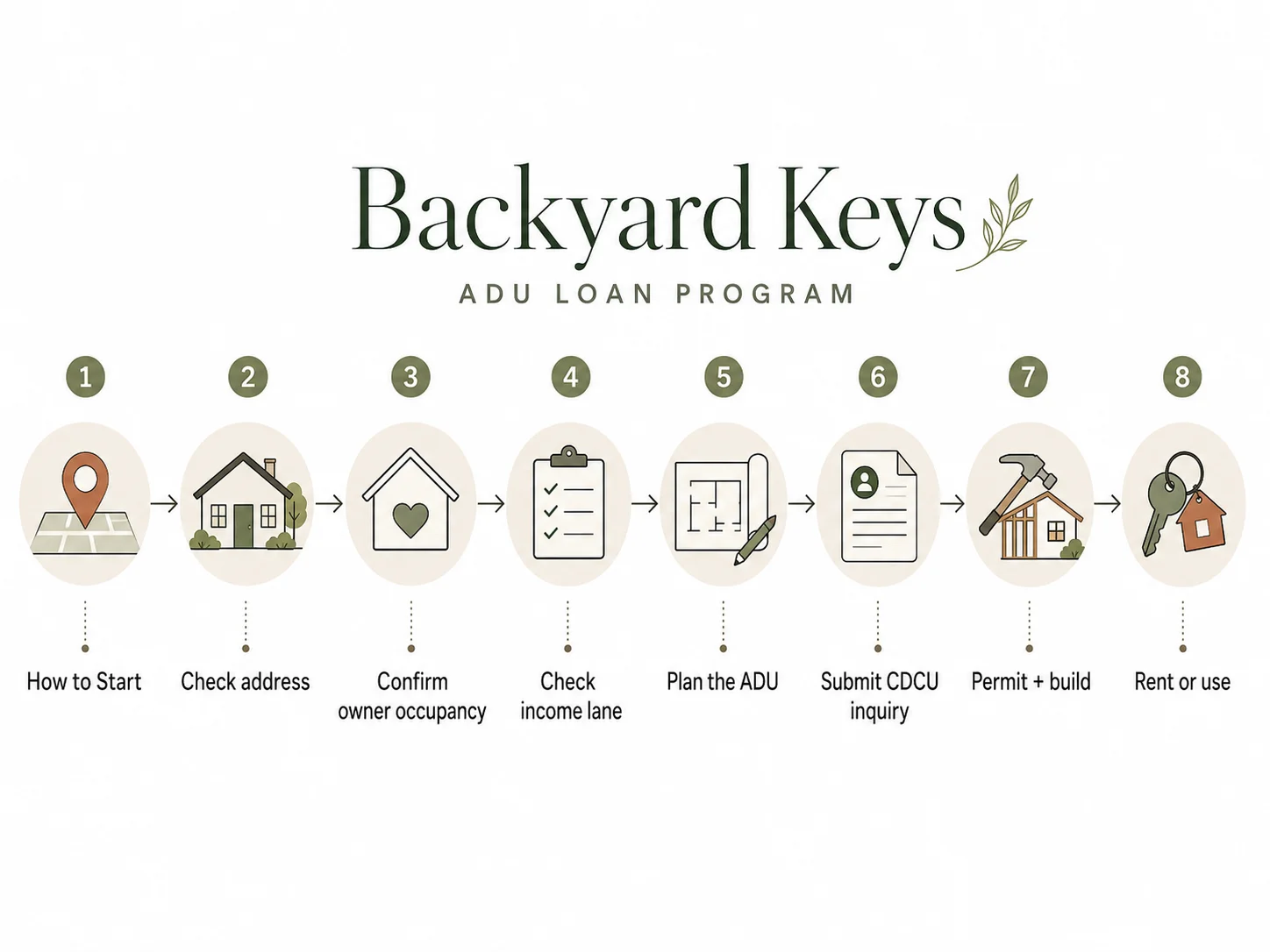

The short answer: You apply through CDCU, not a bank. Confirm your property is west of I-15 inside Salt Lake City, estimate your ADU scope and cost, check your income against 80% AMI, review the SLC ADU rules, then submit CDCU's ADU web inquiry form. Applications are accepted on a rolling basis as funding becomes available.

Step-by-step

- Confirm location. Verify the property is west of I-15 and inside Salt Lake City limits using the city's Zoning Lookup Map.

- Check 9-Line priority. See whether your address falls in the 9-Line area (≈900 South, I-15 to the Jordan River) for priority funding.

- Confirm owner-occupancy. You must live on the property as your primary residence.

- Pick your ADU type. Internal, attached, detached, garage conversion, prefab/modular, or a pre-approved standard plan — each carries different cost and feasibility.

- Rough out your budget. Compare an all-in estimate (site work, utilities, permits, contingency) against the $200,000 cap.

- Check your income lane. Compare household income to the 80% AMI figure for your size.

- Decide on the rent rule if you're above 80% AMI.

- Review SLC ADU code blockers (size, setbacks, height, parking, utilities).

- Call CDCU with your open questions (the checklist below) before spending money on design.

- Submit CDCU's ADU web inquiry form to start the process or get on the list for when funding opens.

Questions to ask CDCU before you spend a dollar on plans

- Is funding currently available, or is there a waitlist?

- Does my exact address qualify, and am I in the 9-Line priority area?

- Does the current program include any loan forgiveness? (Resolve the conflict for your loan.)

- What happens at the 5-year maturity if the extension isn't granted, and what qualifies me for the extension?

- Does the $200,000 cap include the financed origination fee?

- How are construction draws handled, and how long is the interest-only construction period?

- What exact rent schedule applies if I'm above 80% AMI, and who verifies tenant income?

- Does my detached ADU trigger any sustainability or energy requirement?

- Can I combine Backyard Keys with other financing if my project exceeds $200,000?

- What costs are ineligible, and what happens if the project goes over budget?

Checklist assembled by Dwelling Index to resolve the specific gaps and source conflicts documented on this page. Verified May 27, 2026.

CDCU is the actual administrator — the inquiry form is the real first step, and it isn't an affiliate link.

Go to CDCU's Official ADU Inquiry Form →Official program link — not an affiliate link.

Want the question list and a clean prep checklist to bring to that conversation?

Download the Free ADU Starter Kit →What happens if you don't qualify or funding runs out?

The short answer: If Backyard Keys doesn't fit your location, income plan, timeline, or budget, the common alternatives Salt Lake homeowners use are a cash-out refinance, a HELOC, or a renovation/construction loan. None offers a subsidized 3% rate, but none is restricted to the west-of-I-15 footprint either.

Most people who land here searching “Backyard Keys” won't fit the program — not because they did anything wrong, but because it was deliberately targeted at one side of one city. That's not a dead end. Here's how west-side homeowners who miss the window, and everyone outside the footprint, actually finance ADUs.

Financing paths, compared neutrally

We present these as financing lanes, not ranked lenders. Rates and terms depend entirely on your credit, equity, and the lender.

| Path | Best when | The trade-off |

|---|---|---|

| Backyard Keys | West of I-15, owner-occupant, OK with the rules | Tiny footprint; limited pilot funding; rent rules above 80% AMI |

| Cash-out refinance | You have substantial equity and want one loan | Resets your whole mortgage at today's rates |

| HELOC | You have equity and want to draw as you build | Variable rate; payment can rise |

| Renovation / construction loan | Limited current equity; lender lends against finished value | More paperwork; draws tied to build milestones |

Fallback decision matrix

| Your situation | Better next step |

|---|---|

| East of I-15 or outside SLC | Use a general ADU financing path |

| West side, but funding unavailable now | Get on CDCU's list and line up a fallback |

| Above 80% AMI and the rent rule doesn't fit | Consider non-restricted financing |

| Project will exceed $200,000 | Reduce scope, use a standard plan, or add a second source |

| Lot has zoning blockers | Solve feasibility before financing |

| Goal is short-term rental | Reconsider — SLC ADUs can't be short-term rentals |

| Investor-owned property | Use investor/rental financing, not Backyard Keys |

Framework assembled by Dwelling Index. Verified May 27, 2026.

Compare the financing lanes side by side before you set a budget. Approval, rates, and terms are never guaranteed.

Compare Financing Lanes →If you're weighing a prefab or standardized route in Utah, Nest Tiny Homes is one option to look at — and Salt Lake City's pre-approved plan list already includes one of its designs. The city does not endorse any specific provider.

See Utah ADU Builder Options →Also see: how to finance an ADU · ADU grants database · estimate your ADU funding gap

How we verified this page

We are an independent research resource covering ADU financing, costs, and regulations. We are not affiliated with Salt Lake City, the CRA, or CDCU, and we are not a lender or broker. We pulled program terms, fees, and eligibility directly from the Salt Lake City CRA's Backyard Keys page and from CDCU's “Finance ADU construction” page, reading both in full and comparing them line by line, then cross-checked the forgiveness and term details against the adopted 2026 CRA program documentation. We checked zoning rules against SLC Code §21A.40.200. We took the 80% AMI figures from Salt Lake City's published 2026 HUD AMI table.

What we verified

| Verified fact | Source | Verified |

|---|---|---|

| Backyard Keys is an SLC ADU loan program administered with CDCU | CRA / CDCU | May 27, 2026 |

| Eligibility: owner-occupants west of I-15 in SLC | CRA / CDCU | May 27, 2026 |

| Loans up to $200,000; 3% fixed; 30-yr amortization | CRA / CDCU | May 27, 2026 |

| 5-year term + possible 5-year extension | CRA / adopted 2026 terms | May 27, 2026 |

| $2,000 origination ($200 application) + $1,000 min. borrower funds | CDCU | May 27, 2026 |

| Income/rent rule based on 80% AMI; annual tenant verification | CRA / CDCU / adopted 2026 terms | May 27, 2026 |

| 80% AMI 2026 dollar figures (SLC metro) | SLC Housing Stability 2026 HUD AMI table | May 27, 2026 |

| ~$2.9M total allocation ($1.91M 9-Line + $1M west-side) | Adopted 2026 CRA documentation | May 27, 2026 |

| Detached ADU ≤1,000 sq ft; no min lot size; STR prohibited | SLC Code §21A.40.200 | May 27, 2026 |

| Good Landlord / business-license obligations | SLC Building Services / Landlord-Tenant | May 27, 2026 |

| Public sources conflict on loan forgiveness | CRA page vs. adopted 2026 terms vs. CDCU | May 27, 2026 |

| Builder cost examples (~$162K–$199K, compact models) | Utah ADU vendor (aduutah.com) | May 27, 2026 |

What still needs direct confirmation from CDCU

- Current funding availability and application-queue status

- Whether any loan forgiveness remains in current loan documents

- Exact 5-year maturity, payoff/refinance, and extension mechanics

- Whether the $200,000 cap includes financed fees/reserves

- The exact rent-cap formula and tenant-income verification method

- Eligible vs. ineligible project costs, and rules for combining financing

Backyard Keys ADU loan FAQ

Is Backyard Keys available outside Salt Lake City?

No. It's restricted to owner-occupied properties west of I-15 within Salt Lake City limits. A home west of the freeway but in West Valley City, South Salt Lake, or unincorporated county is not eligible.

Is every homeowner west of I-15 automatically eligible?

No. Location is only the first filter. You also need owner-occupancy, primary residence, program underwriting, a feasible and code-compliant ADU project, and available funding.

Is Backyard Keys a grant?

No — it's a loan you repay. Public sources conflict on whether any partial forgiveness still exists, so treat forgiveness as unconfirmed until CDCU verifies it for your loan in writing. Don't let anyone sell it to you as "free money."

Do I have to earn under 80% AMI to qualify?

No. At or below 80% AMI, there's no rent restriction. Above 80% AMI, you still qualify but must rent either the ADU or the main home affordably to a household at 80% AMI or below.

Can I use Backyard Keys for a detached ADU?

Potentially, yes — but a detached ADU may not exceed 1,000 square feet of gross floor area and must meet SLC's setback, height, and parking standards. Confirm your buildable size with SLC Planning before designing.

Can I use a Salt Lake City pre-approved ADU plan?

Yes, and it can speed permitting — but the city is explicit that a pre-approved plan doesn't eliminate site review, fees, code compliance, or documentation, and isn't a city endorsement of any designer.

Can I rent the ADU short-term (Airbnb)?

No. Salt Lake City prohibits short-term-renting an ADU. Long-term rentals of 30+ days are allowed where owner-occupancy is met.

Is there a minimum lot size?

No, SLC's ADU code sets no minimum lot size — but setbacks, height, parking, utilities, easements, and building code can still block or shrink a project on a small lot.

What if $200,000 isn't enough?

Reduce the scope, choose an internal/garage-conversion or standardized plan, or combine Backyard Keys with another financing source. Don't assume the cheapest advertised price is your all-in cost — budget for site work, utilities, permits, and contingency.

Where do I actually apply?

Through CDCU (Community Development Corporation of Utah) / Utah Community Investment Fund, which administers the program. Start with CDCU's ADU web inquiry form at cdcutah.org.

Not sure where to start?

See what's possible at your address → get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report