San Diego ADU Finance Program: What It Actually Offers and Who Qualifies (2026)

An independent guide from Dwelling Index, an independent research resource covering ADU financing, costs, and regulations.

· · Last verified: May 26, 2026

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Dwelling Index is not a lender and does not guarantee loan approval, rates, terms, or monthly payments.

We need to say one thing plainly before you read further, because it is the single most common reason homeowners waste weeks on this program: every competing page we checked describing the San Diego ADU Finance Program had at least one number wrong. We found pages citing a $200,000 cap (that was the 2022 pilot), pages citing a “1% rate,” and pages citing “4% fixed for 15 years” (a figure that appears nowhere in SDHC’s current materials). The terms below are pulled directly from SDHC’s own program page and its 2026 flyer, updated 05.21.26 — not from a contractor blog or a press release.

Should you apply first? A 30-second gut check

The San Diego ADU Finance Program fits a narrow homeowner: an owner-occupant of a detached single-family home inside the City of San Diego, earning at or below 80% of Area Median Income, with a credit score of 680 or higher, who can accept a seven-year affordable-rent restriction. If any one of those is a hard no, the program is not the path — but a standard financing route usually still is.

| Apply to SDHC first if… | Look elsewhere first if… |

|---|---|

| ✓You own and live in a detached single-family home in the City of San Diego | ×Your property is in the County, an unincorporated area, or another city (Chula Vista, Carlsbad, etc.) |

| ✓Your household income is at or below 80% AMI for your family size | ×Your income is above the 80% AMI limit |

| ✓Your credit score is 680 or higher | ×Your credit or your post-construction takeout financing is shaky |

| ✓You can accept seven years of below-market, capped rent | ×You need market-rate rent immediately to make the numbers work |

| ✓You will not rent the ADU to a family member for seven years | ×Your whole reason for building is to house Mom, Dad, or an adult child |

| ✓Your scope is modest, or you have cash/equity for the gap above $250,000 | ×You need the loan alone to cover a $400K+ detached ADU |

If you landed mostly in the right-hand column, skip to What are your alternatives if SDHC is not a fit? — we’ll point you to the right financing lane. If you’re mostly in the left column, keep reading; the rest of this page is your application playbook.

Not sure if your lot, income, or scope actually fits?

See what’s possible at your address — we’ll show you what you can build and which financing lanes match your situation before you spend a dollar on plans.

Get Your Free ADU Report →Is the San Diego ADU Finance Program available now?

Yes. As of SDHC’s program flyer updated May 21, 2026, the San Diego ADU Finance Program is marked “Available Now,” offering a construction loan up to $250,000 with no-cost technical assistance. Because program funding and terms can change, homeowners should verify current status directly with SDHC before paying for plans or application prep.

The program is live. But “available today” and “available the day you finish your plans” are not the same promise — government program funding can pause, deplete, or change terms with little notice. This is the one fact on this page we most want you to re-confirm yourself, by checking sdhc.org/housing-opportunities/adu and emailing adu@sdhc.org before you spend money.

The San Diego ADU Finance Program at a glance

The SDHC ADU Finance Program offers a construction loan of up to $250,000 at 3% fixed interest, capped at 75% loan-to-value, for income-eligible owner-occupants in the City of San Diego. It pairs the loan with no-cost technical assistance and requires the completed ADU to be rented affordably to households at 80% AMI for seven years. It is a repayable loan, not a grant.

| Feature | Current detail (2026) | What it means for you |

|---|---|---|

| Program type | Construction loan + free technical assistance | Not a grant — you repay it |

| Maximum loan | $250,000 (subject to SDHC and partner-lender underwriting) | May not cover a full detached build |

| Interest rate | 3% fixed | The construction-phase program rate; your takeout loan is priced separately |

| Max loan-to-value (LTV) | 75%, calculated under SDHC and partner-lender underwriting | Your existing mortgage balance and property value affect how much you can borrow |

| Income limit | Household income up to 80% of San Diego AMI | Depends on family size — see table below |

| Minimum credit score | 680 | Credit screen comes early |

| Owner’s contribution | 1% of the construction loan amount (per SDHC 2026 flyer) | Budget cash for this — on a $250K loan that’s $2,500 |

| Application fee | $2,500, due after SDHC approval at construction-loan closing | Not due to inquire or check eligibility |

| Eligible property | Detached single-family residence, owner-occupied, City of San Diego | Not for condos, investor properties, or out-of-city lots |

| Repayment | Loan repaid after construction via refinance or home equity loan/line of credit | Requires a “takeout” plan before you start |

| Lender pre-approval | Pre-approval with SDHC’s partner lender is required | A mandatory step many guides omit |

| Affordability covenant | Rent affordable to 80% AMI tenants for 7 years; no family-member tenants | Changes your rental-income math materially |

| Technical assistance | Free SDHC ADU consultant: pre-design, permits, construction, vendor tips | A genuine, dollar-valuable benefit |

| Plan templates | Four pre-reviewed SDHC plan sets (studio to 3BR) available | Speeds permitting, but still needs site-specific review |

Sources: SDHC ADU Finance Program page (accessed May 26, 2026); SDHC 2026 ADU Program Flyer (updated 05.21.26). Verified May 26, 2026.

One discrepancy to know about

SDHC’s 2026 flyer lists an “Owner’s Contribution equal to 1% of the construction loan amount.” SDHC’s web page does not include that line in its visible eligibility bullets. Because the flyer is current (updated 05.21.26), budget for the 1% contribution unless SDHC confirms otherwise when you apply. On a $250,000 loan, that’s $2,500 — separate from the $2,500 application fee.

How does the San Diego ADU Finance Program work?

SDHC lends an income-eligible City of San Diego homeowner up to $250,000 at 3% fixed to build one ADU, and provides a free consultant to guide the process. When construction finishes, the homeowner repays the construction loan by refinancing or taking a home equity loan or line of credit, through SDHC’s partner lender or a lender of their choice. Pre-approval with the partner lender is required before the project moves forward.

The program is built around a simple idea: lower-income homeowners often have equity and yard space but can’t get affordable construction financing on their own. SDHC bridges that gap during the build, then hands the homeowner off to permanent financing once the ADU exists and the property may appraise higher.

- 1You confirm eligibility and get pre-approved with SDHC’s partner lender. This is mandatory, not optional — the program is structured around that lender relationship.

- 2SDHC assigns you a free ADU consultant. This is the part most homeowners undervalue. The consultant helps with pre-design, navigating City of San Diego permits, vendor selection, and project management. On the open market, that guidance can cost thousands.

- 3The construction loan funds the build up to $250,000 at 3% fixed, capped at 75% LTV, for one ADU per property.

- 4The ADU gets built and permitted through the normal City of San Diego process. SDHC financing does not waive permits.

- 5You repay the construction loan after completion by refinancing your first mortgage or using a home equity loan or HELOC. You can use SDHC’s partner lender or shop your own.

Is the San Diego ADU Finance Program a grant?

No. The SDHC ADU Finance Program is a construction loan that must be repaid after construction, not a grant or free money. SDHC states the loan is repaid via refinance, home equity loan, or line of credit upon completion. This is the most important expectation to reset. The benefit is the rate and the free technical assistance, not free construction.

If you came here hoping for a grant, here’s the honest picture: the CalHFA ADU Grant Program (which once offered up to $40,000 toward pre-development and non-recurring closing costs) has exhausted its funding. CalHFA states the latest round of ADU Grant funding has been fully allocated, and its December 28, 2023 bulletin confirms that all funds for the application window that opened December 11, 2023 were exhausted and the reservation portal closed. (Last verified May 26, 2026.)

What older articles get wrong about this program

Several widely-cited pages list outdated SDHC terms. The current verified terms are a $250,000 maximum at 3% fixed, per SDHC’s program page and 2026 flyer.

| Claim you’ll see online | What SDHC actually says now | Where the wrong number came from |

|---|---|---|

| "Up to $200,000" | $250,000 maximum | The 2022 ADU Finance Pilot Program launched at $200K; it was later raised |

| "1% interest rate" | 3% fixed | Earlier SDHC pilot/flyer language listed lower figures; the current flyer lists 3% |

| "4% fixed for 15 years" permanent loan | No such term in SDHC materials | An estimate of the takeout mortgage rate, presented as if it were a program term |

| "Income up to 150% AMI" | Income up to 80% AMI | An earlier flyer listed a higher figure; the current page and flyer list 80% |

| "Low-income only, you won’t qualify" | Up to 80% AMI — about $132K–$140K for a family of four | Oversimplification; 80% AMI in high-cost San Diego is a generous threshold |

Sources: SDHC ADU Finance Program page and 2026 flyer (updated 05.21.26); 2022 SDHC ADU Finance Pilot Program launch release. Comparison assembled by Dwelling Index, verified May 26, 2026.

Who qualifies for the SDHC ADU loan?

To qualify, a homeowner must have household income at or below 80% of San Diego Area Median Income, own and occupy a detached single-family residence within the City of San Diego, have a minimum credit score of 680, and pass SDHC and partner-lender underwriting. There are four gates. You must clear all four.

Gate 1: Income — up to 80% of San Diego AMI, by household size

This is where most people misjudge themselves. In a high-cost region like San Diego, “80% AMI” is far higher than the phrase “low income” suggests — a family of four can earn well over $130,000 and still qualify.

Two official charts are in play right now. SDHC’s ADU page currently links to the 2025 chart. The County of San Diego has published 2026 limits (effective May 6, 2026) that are higher. We’re showing you both so you can self-qualify against either — but confirm with SDHC which chart it’s applying before you rule yourself in or out.

SDHC-linked chart (2025 values):

| Household size | 80% AMI income limit (2025) |

|---|---|

| 1 person | $92,700 |

| 2 people | $105,950 |

| 3 people | $119,200 |

| 4 people | $132,400 |

| 5 people | $143,000 |

| 6 people | $153,600 |

| 7 people | $164,200 |

| 8 people | $174,800 |

Source: SDHC / HUD 2025 San Diego Income Limits chart, effective 04/01/2025, revised 04/16/2025. San Diego 2025 median income: $130,800. Verified May 26, 2026.

County of San Diego chart (2026 values — confirm with SDHC):

| Household size | 80% AMI income limit (2026) |

|---|---|

| 1 person | $97,950 |

| 2 people | $111,950 |

| 3 people | $125,950 |

| 4 people | $139,900 |

| 5 people | $151,100 |

| 6 people | $162,300 |

| 7 people | $173,500 |

| 8 people | $184,700 |

Source: County of San Diego Income Limits, effective May 6, 2026. 2026 county AMI: $130,900. Verified May 26, 2026. AMI is updated annually — confirm the current chart SDHC uses before applying.

Gate 2: Property — detached single-family, owner-occupied, City of San Diego

The program is City of San Diego only. This single gate disqualifies a large share of “San Diego” homeowners, because “San Diego” colloquially means the whole county. If your property is in El Cajon, La Mesa, Chula Vista, the unincorporated county, or any other jurisdiction, SDHC can’t help you here — its authority is limited to the city.

Don’t rely on your ZIP code to confirm this — ZIP codes are postal routes, not jurisdiction boundaries. Some addresses with a “San Diego” mailing ZIP actually sit in another city or unincorporated county. See how to confirm your property is inside the City of San Diego below.

Gate 3: Credit — minimum score of 680

A 680 is a mid-tier score — achievable for many, but a real wall for some. Because pre-approval with the partner lender is required, your credit and your ability to refinance later are assessed up front, not at the end.

Gate 4: The contribution, fee, and LTV cap

The 1% owner contribution (per the 2026 flyer) and the $2,500 fee are real but back-loaded — you don’t pay them to ask questions or get pre-screened; they come at closing. The 75% LTV cap means SDHC and the partner lender won’t let your borrowing exceed 75% of the property’s value, so homeowners with thin equity or high existing mortgage balances may be limited below the $250,000 maximum.

Quick disqualifiers

- ×Property is outside the City of San Diego.

- ×The home is not owner-occupied (investor properties don’t qualify).

- ×It’s a condo or multifamily, not a detached single-family residence.

- ×Household income exceeds the 80% AMI limit for your size.

- ×Credit score is below 680.

- ×You have no realistic plan to repay (refinance/HELOC) after construction.

- ×Your goal is to house a family member (see the seven-year rule below).

Cleared all four gates — or not sure about your lot or income?

Explore what’s possible at your address and which lanes fit. It takes about a minute and costs nothing.

Get Your Free ADU Report →How do I confirm my property is inside the City of San Diego?

Because the SDHC ADU Finance Program is limited to the City of San Diego and ZIP codes don’t match jurisdiction boundaries, homeowners should confirm their property’s city using the parcel record or an official jurisdiction lookup before applying. A mailing address with a “San Diego” ZIP can still fall in another city or unincorporated county. Two minutes here saves weeks of wasted application effort.

- Check your property tax bill or parcel record (via the San Diego County Assessor) — it identifies the taxing jurisdiction.

- Use the City of San Diego’s official address/parcel lookup or the County’s parcel viewer to confirm the city of record.

- If still unclear, ask SDHC directly (adu@sdhc.org) with your full property address before you invest in plans.

If your parcel turns out to be in the unincorporated county or another city, jump to alternatives — you still have financing paths, just not this one.

How much does the $250,000 loan actually cover?

The SDHC loan caps at $250,000, but detached ADUs in San Diego typically cost $300,000 to $450,000 or more all-in, at roughly $375 to $600+ per square foot. The program comfortably covers smaller units and many garage conversions, but larger detached ADUs usually leave a funding gap the homeowner must cover with cash, equity, or additional financing.

| ADU scope | Typical all-in San Diego cost (2026) | SDHC max loan | Likely funding gap |

|---|---|---|---|

| Garage conversion | ~$150,000–$250,000 | Up to $250,000 | $0–$100K+ (depends on existing structure & utilities) |

| 1BR / 1BA detached, ~500 sq ft | ~$300,000 | Up to $250,000 | ~$50,000+ |

| 2BR / 1BA detached, ~750 sq ft | ~$350,000 | Up to $250,000 | ~$100,000 |

| 2BR / 2BA detached, ~1,000 sq ft | ~$425,000 | Up to $250,000 | ~$175,000 |

| 3BR / 2BA detached, ~1,200 sq ft | ~$450,000 | Up to $250,000 | ~$200,000 |

Cost source: SnapADU “Cost to Build an ADU in San Diego”, updated March 2026 — turnkey detached ADUs at $375–$600+/sq ft. Loan cap from SDHC program page. Verified May 26, 2026.

Public cost benchmarks are not quotes. Your actual ADU cost depends on site conditions, utilities, access, soils, fire requirements, finishes, and permitting. Get a property-specific estimate before committing.

Why the cap changes the conversation

The $250,000 is most powerful for modest scopes. Want a 1,200-square-foot, three-bedroom detached ADU? The program alone won’t get you there. Want a 500-square-foot one-bedroom or a garage conversion? It may cover most or all of it. This is a design decision as much as a financing one.

The hidden costs that widen the gap

ADU site work and utilities are the most variable costs and can add tens of thousands of dollars beyond headline per-square-foot figures. Basic site work commonly runs around $35,000, additional utility connections $15,000–$30,000+, and City of San Diego permit fees roughly $13–$28 per square foot — far higher than neighboring cities like Encinitas at $2–$4 per square foot.

Permit-fee benchmark: SnapADU permit-fee data. Site-work and utility ranges: SnapADU cost guide (updated March 2026). Verified May 26, 2026.

Want to size your gap before you fall in love with a floor plan?

See what’s buildable at your address and what it’s likely to cost. No quotes, no pressure — just a realistic starting picture.

Get Your Free ADU Feasibility Report →What happens when construction is complete?

When the ADU is built, the SDHC construction loan must be repaid. Homeowners do this by refinancing their first mortgage or taking a home equity loan or line of credit, either through SDHC’s partner lender or a lender of their choice. A construction loan solves the build-period cash problem. It does not automatically solve permanent financing. The 3% construction-loan rate is not your forever rate. When the build finishes, you replace that loan — and the replacement loan is priced at whatever the market offers when you refinance.

Why your takeout plan matters before you apply

Because the SDHC construction loan converts to permanent financing through a separate refinance or home equity product, homeowners should confirm they can qualify for that takeout loan before starting construction. Ask these questions before you apply, not after:

- •Will the partner lender (or your chosen lender) approve my refinance or home equity loan after construction?

- •What rate range should I plan for on the permanent loan? (No one can promise a rate — but you can stress-test a realistic range.)

- •Does the new, post-construction property value support the LTV the takeout lender needs?

- •What happens to my monthly payment when 3% construction financing converts to a market-rate permanent loan?

Can future ADU rent help me qualify for the takeout loan?

Possibly. Fannie Mae guidelines allow projected ADU rental income to be considered when qualifying for certain loans, subject to limits on how much rental income can count and documentation such as an appraiser’s rent schedule. Under the SDHC program, that projected rent is capped for seven years, so the rent an appraiser can schedule is the capped figure, not market. Plan conservatively.

Affiliate disclosure: Dwelling Index is reader-supported and may earn a commission when you use our links to explore financing options, at no extra cost to you. We do not rank lenders by compensation, do not promise rates or approval, and are not a lender.

The takeout loan is where most SDHC plans live or die.

Explore refinance, cash-out refinance, home equity, and construction-loan paths as your permanent financing through our financing partner — independent education on the lanes, not a lender ranking.

Explore ADU Financing Lanes →Via Mortgage Research Center, where available. We may earn a commission at no extra cost to you. No rate, payment, or approval is promised.

What do you give up for seven years? The rent covenant, decoded

In exchange for the 3% loan, the completed ADU must be rented at rents affordable to households earning up to 80% of AMI for seven years, and the owner may not rent to a family member during that period. For 2025, the maximum gross rents are roughly $2,318 for a studio, $2,649 for a one-bedroom, $2,980 for a two-bedroom, and $3,310 for a three-bedroom — and the actual cash rent is lower after a utility allowance is subtracted.

For many San Diego ADU projects, this covenant is the deciding factor. In a moderate-rent neighborhood, it may cost you almost nothing. In a coastal neighborhood, it can cost you the better part of $50,000–$80,000+ in foregone rent over seven years. Let’s put real numbers on it.

The 2025 SDHC rent caps, by bedroom count

| ADU bedroom count | 80% AMI gross rent cap (2025) | Cash rent after utility allowance |

|---|---|---|

| Studio | $2,318 | Lower (gross minus utility allowance) |

| 1 bedroom | $2,649 | Lower (gross minus utility allowance) |

| 2 bedroom | $2,980 | Lower (gross minus utility allowance) |

| 3 bedroom | $3,310 | Lower (gross minus utility allowance) |

Source: SDHC Income and Rent Calculations Chart, revised 05/05/2025. Gross rent minus utility allowance = maximum cash rent. Rent charts are updated annually. Verified May 26, 2026.

Example rent-cap gap by San Diego area

Whether the seven-year rent cap costs a homeowner money depends on how the SDHC cap compares to market rent for that unit size and neighborhood. The table below illustrates how the gap swings by area, using a two-bedroom ADU (2025 cap: $2,980 gross). These are illustrative market ranges, not ADU-specific quotes, and your cash rent under the covenant is lower than the gross cap after utility allowance.

| San Diego area type | Example 2BR market rent range | SDHC 2BR gross cap (2025) | Approx. monthly gap | Over 7 yrs (84 mo.) |

|---|---|---|---|---|

| Inland / moderate (e.g., East County-adjacent neighborhoods) | ~$2,800–$3,000 | $2,980 | Near $0, possibly favorable | Minimal |

| Central / urban (e.g., North Park, City Heights area) | ~$3,000–$3,300 | $2,980 | ~$20–$320/mo below market | ~$1,700–$27,000 |

| Coastal / high-rent (e.g., Pacific Beach, coastal communities) | ~$3,500–$4,000+ | $2,980 | ~$520–$1,000+/mo below market | ~$44,000–$84,000+ |

Cap source: SDHC Income and Rent Chart (2025). Market ranges are illustrative neighborhood benchmarks compiled from public rent platforms and are not ADU-specific guarantees; actual market rent varies block by block and over time. Methodology: monthly gap × 84 months. Verified May 26, 2026.

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals. SDHC rent figures are gross rents; maximum cash rent is lower after a utility allowance, and market-rent benchmarks are not ADU-specific guarantees.

Want your specific gap and rent tradeoff, not a generic range?

Our free ADU report combines your location and scope to flag eligibility, estimate the funding gap above $250,000, and frame your bedroom-specific rent-cap tradeoff.

See What’s Possible at Your Address →Can I use the SDHC ADU loan to house my parents or adult child?

No. The SDHC ADU Finance Program prohibits renting the ADU to a family member during the seven-year affordability period. If your honest reason for building is “a backyard home for Mom” or “a place for our kid to land after college,” stop here on this program. This section saves family-housing builders weeks of wasted application effort.

The ADU dream is very much alive for you — you just need a financing path without an affordable-rent covenant. Building for family is one of the most common and worthwhile reasons to add an ADU, and standard financing (cash-out refinance, home equity, construction loan) carries no family-tenant restriction. Without the covenant, you also keep full control of the unit and can house whoever you choose.

Building for family rather than rental income?

You have good options with no rent covenant. Explore the lanes that fit a family-housing ADU.

See Your ADU Financing Options →Do normal San Diego ADU permits and rules still apply?

Yes. SDHC financing does not remove or replace City of San Diego permitting. The loan and the permit are two separate tracks. SDHC’s free consultant helps you navigate permitting, but the City of San Diego Development Services Department still reviews and approves your project like any other ADU.

| Permit rule | Source | What it means for your SDHC-financed ADU |

|---|---|---|

| A building permit is required to create an ADU or JADU | City of San Diego Information Bulletin 400 | SDHC financing does not waive this; budget permitting time and fees |

| ADU permits reviewed ministerially (no hearing) when objective standards are met | CA Gov. Code § 66317 | Faster, by-right approval — but you still must meet the standards |

| SDHC plan templates still need site-specific review | SDHC ADU page | “Pre-approved” ≠ auto-approved for your lot |

| Coastal Overlay Zone projects may face added review | City of San Diego IB 400 | Coastal lots can add steps and time |

| SDHC-financed / rent-restricted ADUs can’t be sold separately as condos during the covenant | City of San Diego IB 400 | You can’t carve off and sell the ADU during the 7-year term |

ADU size and the California legal framework

Under California ADU law, codified in Government Code sections 66310–66342, ADU permit applications subject to state law must be reviewed ministerially — without discretionary review or a hearing — when they meet applicable objective standards, with a 60-day approval-or-denial clock after a complete application. Detached ADUs are generally capped at 1,200 square feet. A JADU is limited to 150–500 square feet within the existing or proposed home or attached garage.

Sources: City of San Diego Information Bulletin 400; CA Gov. Code § 66317. Verified May 26, 2026.

Need a local San Diego ADU builder familiar with City permitting?

SnapADU operates in San Diego County and publishes current build-cost and permit-fee data. Verify their service area and current availability before committing.

Explore SnapADU San Diego →Affiliate disclosure: we may earn a commission at no extra cost to you.

SDHC vs. a construction loan vs. HELOC vs. cash-out refinance

The SDHC ADU Finance Program offers the lowest rate (3% fixed during construction) but adds an 80% AMI income ceiling and a seven-year rent cap. Equity-based paths — HELOC, home equity loan, cash-out refinance, renovation loan — have no program income limit and no affordability covenant, but are priced at market rates and depend on the homeowner’s existing equity. We present these as lanes, not rankings.

| Decision point | SDHC ADU Finance Program | Standard equity / construction financing |

|---|---|---|

| Best for | Income-eligible City of San Diego owner-occupants who accept the covenant | Broader group: any income, any San Diego jurisdiction |

| Rate basis | 3% fixed (construction phase) | Market rate; varies by product, credit, equity |

| Income limit | Up to 80% AMI | No program income cap |

| Rent restriction | Yes — 7 years, 80% AMI tenants | Usually none |

| Family tenant | Not allowed for 7 years | Generally allowed (subject to local law) |

| Loan ceiling | $250,000 | Depends on equity, value, lender |

| Technical assistance | Free SDHC consultant included | Usually separate / DIY |

| Geography | City of San Diego only | Anywhere |

| Complexity | Program + lender + covenant + permits | Lender + permits |

Comparison assembled by Dwelling Index from SDHC program terms and general home-financing product categories. Verified May 26, 2026. This is financing-path education, not a lender ranking, and is not personalized financial advice.

Disclosure (repeated near this comparison): Dwelling Index is reader-supported and may earn a commission when you use our links to explore financing options, at no extra cost to you. We do not rank lenders by compensation, do not promise rates or approval, and are not a lender.

Editorial verdict

The SDHC program can be excellent for the right homeowner — but it’s narrow. The right question is not “Can I get this loan?” It’s “Does this loan still make sense after I account for the rent covenant, the family-tenant rule, the repayment requirement, and the funding gap above $250,000?” For a qualifying owner-occupant building a modest rental ADU in a moderate-rent neighborhood, the answer is often a clear yes. For a family-housing builder, a higher earner, or someone building a large coastal unit, the answer is usually a standard financing lane.

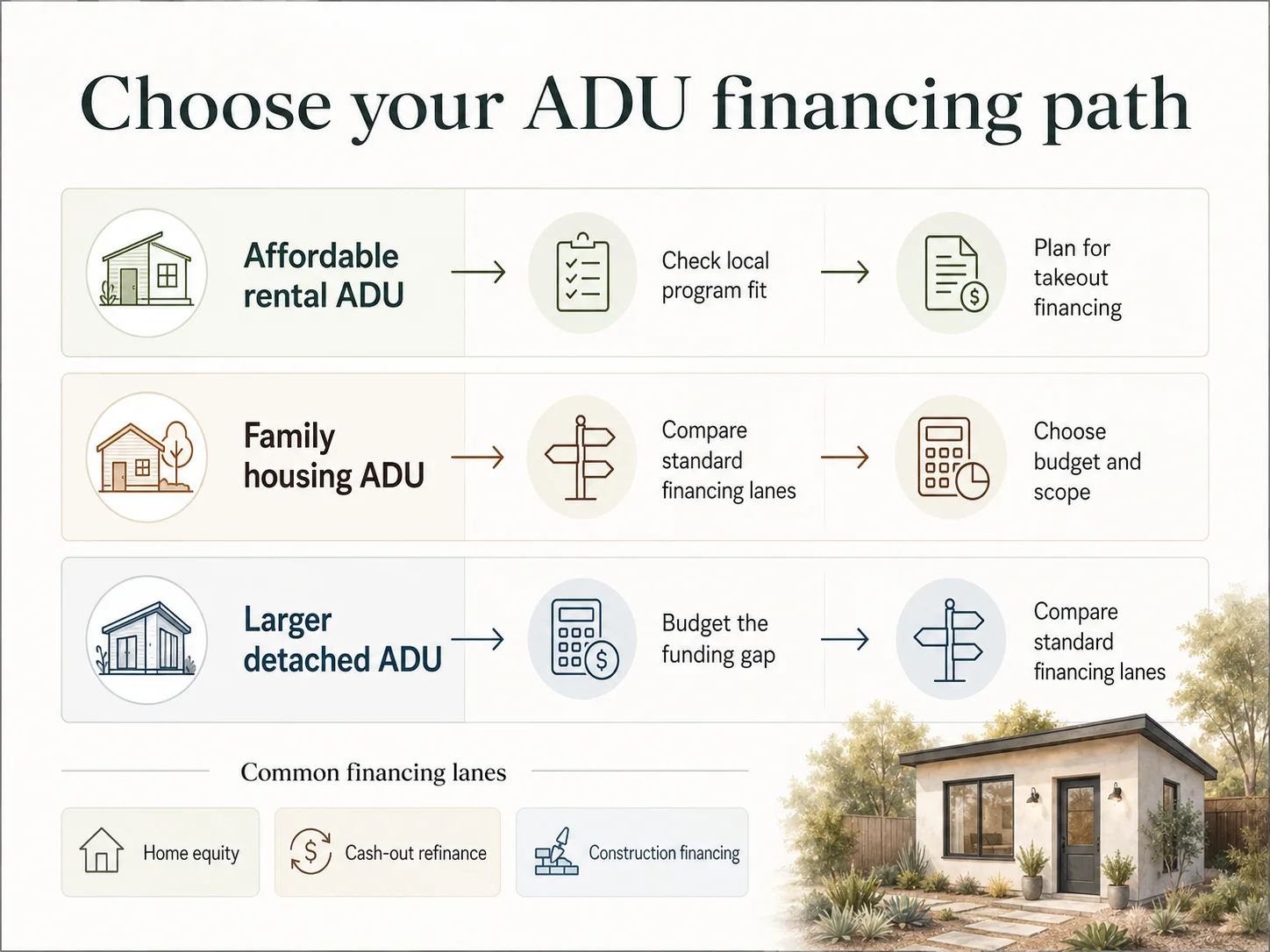

What are your alternatives if SDHC is not a fit?

Find your blocker; take the matching path.

| If your blocker is… | Consider this lane | Why it fits |

|---|---|---|

| Income above 80% AMI | HELOC, home equity loan, cash-out refinance, renovation loan | No program income cap |

| Goal is housing family | Any standard financing path | No affordable-rent / family-tenant restriction |

| ADU costs $350K–$450K+ | SDHC plus a takeout plan, or standard financing | $250K alone won’t cover it |

| Low equity / high LTV | Smaller scope, savings, or a lender review | SDHC caps at 75% LTV |

| Property outside City of San Diego | County of San Diego or your city’s planning department | SDHC is City-only |

| Want maximum rent flexibility | Standard financing | Avoids the 7-year covenant |

| Hoping for a grant | Verify current grant status; beware “free money” scams | CalHFA ADU Grant funds are exhausted |

A note on home equity investments (HEIs)

You’ll see HEI products marketed for ADUs — a company advances cash for a share of your home’s future appreciation, with no monthly payment. They can fit specific situations, but availability varies by state, and the long-run cost can exceed traditional financing if your home appreciates strongly. Check availability in California and model the total cost before committing. We treat HEIs as one neutral option among many, not a default recommendation.

Above the income cap, or just want market-rate flexibility?

Explore mortgage-backed lanes — cash-out refinance, home equity, renovation, and construction loans — through our financing partner, where available. Independent path education, not a ranking.

Explore Mortgage-Backed ADU Financing →Via Mortgage Research Center. We may earn a commission at no extra cost to you. No rate, payment, or approval is promised.

How do you apply for the San Diego ADU Finance Program?

Run these steps in order — skipping the verification step at the top is how homeowners get burned by stale numbers.

- 1Confirm the program is still open and funded. Program funding and terms can change. Check sdhc.org/housing-opportunities/adu and email adu@sdhc.org before spending money on plans. Don’t rely on this page — or any page — for live funding status.

- 2Confirm your property is in the City of San Diego (by parcel, not ZIP).

- 3Check the four gates. Income (80% AMI for your size, against the chart SDHC is currently using), property (detached single-family, owner-occupied, city), credit (680+), and your ability to refinance later.

- 4Get pre-approved with the partner lender. Required, not optional.

- 5Estimate your scope and funding gap using the cost table above. Decide whether $250K covers your plan or whether you need a smaller scope or a second source.

- 6Confirm your takeout plan before construction, not after.

- 7Confirm the rent covenant fits your tenant plan. Especially the no-family-member rule.

- 8Apply through SDHC at adu.sdhc.org; applications are reviewed in the order received. Keep copies of everything.

Documents to gather before you start

These are commonly requested for construction-loan and program applications. SDHC’s actual application may request different or additional documents — use this as a prep list, not the official checklist.

- •Government-issued ID

- •Proof of ownership / current mortgage statement

- •Income documentation (pay stubs, tax returns)

- •Credit authorization

- •Property insurance

- •Preliminary ADU scope or plan selection

- •Any contractor/design documents you have

- •Existing loan balance information

Ready to move but want a sanity check first?

Before you start the SDHC application, see what’s possible at your address and how the financing lanes line up.

Get Your Free ADU Report →Frequently asked questions

- Is the San Diego ADU Finance Program a grant?

- No. SDHC describes it as a construction loan that must be repaid after construction, not a grant. The benefit is the 3% fixed construction rate and free technical assistance, not free money.

- How much can I borrow through the SDHC ADU loan?

- Up to $250,000, subject to SDHC and partner-lender underwriting and a 75% loan-to-value cap. Many detached ADUs cost more, leaving a funding gap.

- What is the interest rate on the San Diego ADU Finance Program?

- SDHC’s current program flyer lists a 3% fixed interest rate for the construction loan. Older online figures of 1% or “4% fixed for 15 years” reflect superseded materials or an estimated takeout rate, not current program terms.

- What is the income limit for the SDHC ADU Finance Program?

- Household income up to 80% of San Diego AMI. SDHC’s ADU page links to the 2025 chart ($132,400 for a family of four); the County’s 2026 chart (effective May 6, 2026) lists $139,900. Confirm with SDHC which chart applies.

- Who qualifies for the San Diego ADU Finance Program?

- Owner-occupants of a detached single-family home in the City of San Diego, with household income at or below 80% AMI and a credit score of at least 680, who pass SDHC and partner-lender underwriting.

- Can I rent my SDHC ADU to my parents or adult child?

- No. The program prohibits renting the ADU to a family member during the seven-year affordability period. Homeowners building to house family should use a standard financing path instead.

- What rent can I charge under the SDHC ADU program?

- Rent is capped at the 80% AMI maximum for the unit’s bedroom count — for 2025, roughly $2,318 (studio), $2,649 (1BR), $2,980 (2BR), and $3,310 (3BR) gross, with actual cash rent lower after a utility allowance.

- Does the program cover the full cost of an ADU?

- Often not. Detached ADUs in San Diego commonly run $300,000–$450,000+, so the $250,000 cap may require a smaller scope, cash, or additional financing for the gap.

- Do I still need a building permit if I use SDHC financing?

- Yes. SDHC financing does not waive City of San Diego permitting. A building permit is required to create an ADU or JADU, per the City’s Information Bulletin 400.

- Does the San Diego ADU Finance Program work outside the City of San Diego?

- No. The program is limited to the City of San Diego. Properties in the County, unincorporated areas, or other cities should contact their local planning department or the County of San Diego.

- Is the CalHFA ADU Grant still available as a backup?

- No. CalHFA states the latest round of ADU Grant funding has been fully allocated, and its December 28, 2023 bulletin confirms the application-window funds were exhausted and the reservation portal closed. Confirm current status with CalHFA before counting on it.

How we researched this page (methodology)

This page was created by Dwelling Index, an independent research resource covering ADU financing, costs, and regulations. We are not a lender, a builder, or a government agency, and we have no affiliation with SDHC.

For program terms, income limits, rent caps, and permit rules, we relied on primary sources read directly: the San Diego Housing Commission’s ADU Finance Program page and its 2026 flyer (updated 05.21.26), the SDHC 2025 Income Limits chart, the County of San Diego 2026 income limits (effective May 6, 2026), the SDHC Income and Rent Calculations Chart (revised 05/05/2025), the City of San Diego Development Services Information Bulletin 400, and California Government Code §§ 66310–66342. For build costs and permit-fee benchmarks, we used a current local builder cost guide (SnapADU, updated March 2026) as public benchmarks, not quotes. Where sources conflicted — notably the 2025-vs-2026 AMI charts and the flyer-vs-webpage owner-contribution line — we surfaced the conflict rather than papering over it.

We deliberately did not publish fabricated testimonials, star ratings, or precise ADU-specific market-rent figures dressed up as guarantees.

Want this in your pocket?

Download the free ADU Starter Kit — our San Diego ADU application-prep checklist, the eligibility and rent-cap tables from this page, and the funding-gap worksheet, all in one PDF.

Get the Free ADU Starter Kit ↓Where to go next on The Dwelling Index

- Building for family? → ADU financing paths with no rent covenant

- Above the income cap? → HELOC vs. cash-out refinance for ADUs

- Outside the city? → County of San Diego ADU rules and financing

- San Diego ADU cost guide

- How to finance an ADU in 2026

- Verified ADU grants database

- San Diego ADU requirements and permit process

- Garage conversion ADU cost San Diego

- ADU financing in California

Not sure where to start?

See what’s possible at your address — get your free ADU report in 60 seconds.

See What You Can Build → Get Your Free ADU Report