VA Loan for ADU: 3 Real Paths in 2026 [Rules & Costs]

By The Dwelling Index Editorial Team · ·

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

The bottom line: yes, a VA loan can work for an ADU — three federal paths, plus a California state add-on

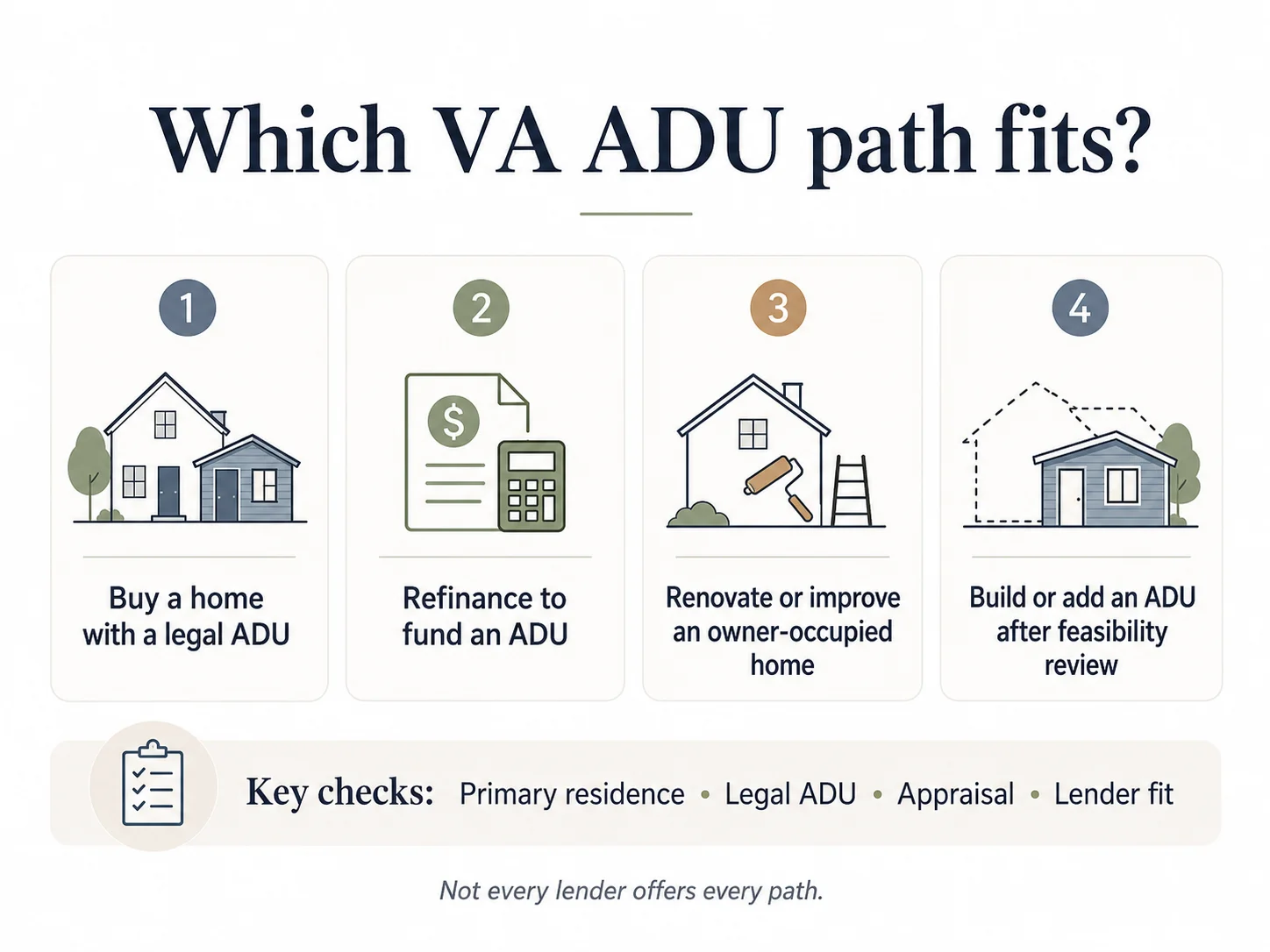

A VA loan for an ADU (accessory dwelling unit — a secondary living unit with its own kitchen, bath, and sleeping area on the same lot as a primary residence) works along three federal VA paths, with one state-level add-on for California veterans. Path 1: Buy a single-family home with an existing legal ADU using a VA Purchase Loan, with no down payment available when entitlement, appraisal, and lender requirements support it. Path 2: Buy a 2- to 4-unit property and occupy one unit. Path 3: Use a VA Cash-Out Refinance on a home you already own to fund an ADU build, or build an ADU alongside new primary construction with a VA Construction Loan.

One path that does not work: most VA renovation lenders will not fund a detached ADU not connected to the main residence — Chase publishes this restriction explicitly. One state hard stop: VA cash-out refinance is not available on Texas homesteads. Texas AG Opinion KP-0183 (2018) concluded that the VA guaranty itself is "additional collateral" prohibited under Texas Constitution Article XVI, Section 50(a)(6)(H). Texas veterans need different paths.

The official VA definition is in VA Pamphlet 26-7, Chapter 11, Section 6: an ADU is "a living unit including kitchen, sleeping, and bathroom facilities added to or created within a single-family dwelling, or detached on the same site." The dwelling and the ADU together "constitute a single real estate entity." That phrase decides whether the appraiser values the property as single-family with an ADU or as a two-family dwelling — driving appraisal form, comparables, and how rental income flows through.

Run the 60-second VA Path Picker on your address →See which path fits, your specific next two steps, and the permit-history questions to ask in your jurisdiction. Free.

Which VA loan for ADU path should you test first?

Answer capsule: There is no single "VA ADU loan." The right path depends on whether you already own the home, whether the ADU already exists, what you want to do with the unit, and which state you live in. The matrix below maps every veteran scenario to the matching VA product and the main blocker for each. Federal VA rules are separated from lender overlays.

This is the table we built because nobody else has assembled it in one place. Each row notes whether the limitation comes from a federal VA rule or from a common lender overlay. Sources are listed beneath the table.

The Three-Path VA-for-ADU Decision Matrix (2026)

| Your situation | VA path | What must be true | Rental-income treatment | Main blocker | Funding fee (first use, no down) |

|---|---|---|---|---|---|

| Path 1: Buy a home that already has a legal ADU | VA Purchase Loan | Primary residence; ADU is legally permitted; appraiser values it on Form 1004 with ADU as a separate market-grid line item (VA rule, Pamphlet 26-7 Ch. 11) | Lender-dependent. 75% factor common in multi-unit scenarios; whether a single-unit-with-ADU qualifies is a lender-overlay question (lender overlay) | Unpermitted ADU at appraisal | 2.15% (VA rule, VA.gov funding fee table) |

| Path 2: Buy a 2–4 unit property and house-hack | VA Purchase Loan | Owner-occupy one unit; all units meet MPRs; appraisal uses Form 1025 (VA rule) | 75% of market rent on non-owner units is standard underwriting practice; some lenders add 2 yrs landlord experience or 6 mo. reserves (lender overlay) | Reserve requirements; not technically "ADU" | 2.15% |

| Path 3a: Cash-out refi to build ADU on home you own | VA Cash-Out Refinance | Owner-occupied; full underwriting; up to 100% of reasonable value (VA rule, 38 CFR 36.4306). Most 2026 lender overlays cap LTV at 90–95% (lender overlay) | Future ADU rent typically not used to qualify (no lease yet) | Replacing a low-rate first mortgage; prohibited on Texas homesteads | 2.15% first use / 3.30% subsequent use, no equity discount |

| Path 3b: New construction with ADU built alongside primary | VA Construction Loan | Primary residence; participating lender's builder/contractor rules; ADU eligibility depends on the lender's product (mixed — VA general framework plus lender overlays) | Construction-product overlays usually exclude ADU rent | ADU paired with manufactured-home primary; pre-start rules; state/territory restrictions; acreage caps; GLA minimums | 2.15% |

| Path 4 (state add-on): CalVet for California veterans | CalVet Construction, Home Improvement, or Rehabilitation Loan | California veteran (90+ days active duty); CA owner-occupied property; product-specific eligibility (state program rules) | Per CalVet manual underwriting | Bond-fund availability is finite; eligibility varies by product | VA funding fee applies when the specific CalVet product uses the federal VA guaranty |

Sources: VA Pamphlet 26-7 Chapters 4, 11, and 12; VA.gov funding fee tables (rates effective April 7, 2023, in effect for 2026); 38 CFR 36.4306; Chase VA Renovation Loan guidance; VA buyer's guide on participating-lender construction loans; Veterans United 2026 VA construction loan guidance; CalVet program pages at calvet.ca.gov; Texas AG Opinion KP-0183 (2018). Last verified May 20, 2026.

What VA WILL NOT do (the honest, sourced list)

- ✗VA Renovation Loans typically cannot fund a detached ADU not connected to the main residence. Chase publishes this explicitly in its VA renovation loan guidance, and other VA renovation lenders describe similar scope limits. This is a lender/product limitation that holds true across most of the market.

- ✗VA cannot be used for a pure investment property. Owner-occupancy is required.

- ✗VA cannot pair an ADU with manufactured-home primary construction on a one-time-close construction loan under common lender overlays.

- ✗Some lenders won't finance properties with more than one ADU. VA Pamphlet 26-7 requires the appraiser to notify the lender of multiple ADUs; whether the lender will then proceed varies.

- ✗VA IRRRL is not a cash-out tool. The Interest Rate Reduction Refinance Loan refinances an existing VA loan into a new VA loan at a lower rate. It does not provide cash for an ADU build.

- ✗VA cash-out refinance is not available on Texas homesteads. Per Texas AG Opinion KP-0183 (2018) and Texas Constitution Art. XVI, § 50(a)(6)(H). Texas veterans see the dedicated Texas section below.

🏡 Not sure which row is yours?

The free Path Picker maps your property status, ADU plan, and state to the matching VA path — plus your next two specific steps.

Run the free 60-second Path Picker on your actual address →What the VA officially defines as an ADU (and why that one sentence decides everything)

Answer capsule: The VA defines an ADU in Pamphlet 26-7, Chapter 11, Section 6 (last revised February 22, 2019) as "a living unit including kitchen, sleeping, and bathroom facilities added to or created within a single-family dwelling, or detached on the same site." A manufactured home on the site can be an ADU. The dwelling and the ADU together "constitute a single real estate entity." That phrase is why the appraiser has to decide whether the property is a single-family dwelling with an ADU or a two-family property — a determination that drives the appraisal form, comparable sales, and how rental income flows through.

The single-real-estate-entity rule, in plain English

VA wants to see one property with an accessory unit, not two separate properties. That framing is what allows the VA Purchase Loan — designed for primary residences — to finance a home with a legal ADU.

This is why the VA appraiser's highest-and-best-use analysis matters. Per Pamphlet 26-7 Chapter 11 Section 6.b, the appraiser must decide whether the subject is (a) a single-family dwelling with an ADU or (b) a two-family dwelling. The factors include relative size, separate utilities, separate entrances, what comparable sales support, and local zoning. If they pick (a), the property gets appraised on Fannie Mae Form 1004 (the standard single-family form), and the ADU appears as a separate line item on the market data grid. If they pick (b), the property gets appraised on Fannie Mae Form 1025 (Small Residential Income Property Appraisal Report) — a different form, different comps, different rent treatment, different lender pricing.

The detached-building rule almost nobody talks about

Pamphlet 26-7 Chapter 11 Section 6.e says that a manufactured home, shed, or other detached structure that lacks kitchen, sleeping, and bathroom facilities, or that cannot legally be used as a dwelling, may be valued only as storage space — provided it presents no health or safety issue.

In practice, this rule quietly kills many "guest house" deals. A buyer sees a listing with a "guest house" or "in-law suite" in the backyard. The appraiser walks through and finds it has a kitchenette but no full bathroom — or was built without permits and cannot legally be used as a dwelling. The unit becomes "storage" for valuation purposes. The buyer's mental rental income disappears.

When a manufactured home can be an ADU

Pamphlet 26-7 explicitly allows it: a manufactured home permanently affixed on the site can qualify as the ADU. Where this typically breaks down: on most VA Construction Loan products, you cannot pair a manufactured-home primary residence with an ADU under the lender's product overlay. Verify with your specific lender in writing.

Can you use a VA loan for a guest house or mother-in-law suite?

Answer capsule: Sometimes, but the label does not decide. The VA defines an ADU by features — kitchen, sleeping, and bathroom facilities — not by nickname. A "guest house" or "mother-in-law suite" qualifies as an ADU only if it has all three core features and is legally permitted under local zoning. Suites missing a kitchen are typically valued as bonus living space attached to the primary residence rather than as a separate ADU.

What the VA appraiser actually looks for:

| The label says | What the appraiser checks |

|---|---|

| "Guest house" | Permanent kitchen, full bath, sleeping area, separate entrance, legal permitting |

| "Mother-in-law suite" | Same checklist — independent living features, legal status |

| "Casita" or "carriage house" | Same checklist plus zoning/setback compliance |

| "Granny flat" | Same checklist; in California, also AB-68-era ADU compliance |

| "ADU" (already labeled) | Permits, separate utilities, conformity to local code |

If your search led you here because you saw the words "guest house" or "in-law suite" on a listing, the next step is a permit-history pull from the city or county. The label on the listing is marketing language; the permit record is fact.

Path 1 — Buy a home that already has an ADU with a VA loan

Answer capsule: A VA Purchase Loan can be used to buy a single-family home with a legal existing ADU. You generally certify intent to occupy the property as your primary residence and move in within VA's occupancy window — commonly 60 days after closing, with documented exceptions such as Permanent Change of Station orders. The ADU must be legally permitted, self-contained, and conforming to local zoning. Rental income from a legal ADU may count with some lenders if the appraiser and lender document it correctly — do not treat it as guaranteed VA policy for every one-unit-with-ADU purchase.

What qualifies as a "legal existing ADU" for VA purposes

Five conditions must all be true:

- 1Permitted at the city or county level — pull the permit history before writing the offer. This is the single most common deal-killer.

- 2Self-contained: own kitchen, own full bathroom, own sleeping area, separate entrance.

- 3Single real estate entity with the main dwelling, per Chapter 11.

- 4Conforming to local zoning — or classified as "Legal Non-Conforming" with documentation that it could be legally rebuilt if destroyed (Chapter 12, Section 12.b).

- 5Marketable — the appraiser must find comparable properties with similar ADU configurations within the market area.

The occupancy rules, accurately stated

VA's official position is that you must certify intent to occupy the property as your primary residence. Common practice — and the framework Veterans United, Veterans Affairs published materials, and most VA-experienced lenders use — is the 60-day move-in window after closing, with documented life events (like PCS orders) treated as legitimate exceptions. Reasonable occupancy is commonly interpreted as a meaningful period of actual residence; verify your specific situation with the lender.

What this means for the ADU: you live in the main house or the ADU. The other unit is yours to rent. Many buyers prefer to live in the ADU and rent the main house because the ADU is smaller and easier to maintain, while the main house often commands stronger rent.

What you can actually rent, day one

If you occupy the main house, the ADU is rentable immediately under federal VA rules. Standard landlord rules apply: written lease, security deposit handled per state law, landlord insurance instead of homeowner-only coverage, and local rental-registration compliance if your city requires it. Short-term rental restrictions vary by city and HOA — Los Angeles, San Diego, and many coastal California cities have specific STR rules; California Junior ADUs face state-level STR restrictions. Verify locally before counting on Airbnb or VRBO income.

A documented public example: Mark Severino, a former U.S. Army captain, used a VA loan in 2015 to buy a property in Orlando with a backyard ADU, rented the ADU to cover the bulk of his mortgage, lived in the main house to fulfill occupancy, then sold in 2017 when he moved to Dallas and used restored entitlement to buy a duplex — also with no down payment. His story was covered by MilitaryMoney.com. We cite it because it is a real, attributable case study.

The unpermitted-ADU trap

⚠️ Most common deal-killer

Many "ADUs" on the market are unpermitted garage conversions. A homeowner finished a garage 15 years ago, the property lists with a "guest house" or "casita." The VA appraiser will flag it. The lender will require legalization, removal of dwelling features, or treatment as storage. The deal stalls.

Before you write the offer: request the property's permit history from the city or county. Many jurisdictions provide permit-history lookup online or by phone. If permits do not exist, the seller is on the hook for legalization, or you walk.

Pre-offer document checklist for an existing-ADU property

- ✓Permit history record for the ADU

- ✓Certificate of occupancy or final inspection record

- ✓ADU floor plan and square footage

- ✓Documentation of separate utilities or sub-metering

- ✓Septic or sewer approval covering both units

- ✓Lease history, if currently rented

- ✓Zoning confirmation letter from the city

- ✓HOA / CC&R disclosure on ADU and rental use

- ✓Local rental-registration and STR rule status

- ✓Photos of kitchen, bath, sleeping area, egress windows, and access path

🏡 Before you write that offer

The free feasibility check surfaces the permit-history questions to ask in your specific jurisdiction so you can investigate before paying for an inspection.

Run the free 60-second feasibility check on the address →How rental income from an ADU actually counts under VA rules (the lender-overlay grid)

Answer capsule: VA guidance clearly supports a 75% factor for documented rental-property and multi-unit scenarios. For a one-unit property with a legal ADU, whether that rent counts is a lender-overlay and appraisal-documentation question — and the public market gives different answers. Three conditions must typically be true before the rent flows to qualifying: the ADU is legally permitted, the appraiser assigns a separate fair-market rent value, and the lender's overlay accepts ADU rental income on a one-unit property.

The 75% factor — what it actually applies to

VA Lender's Handbook Chapter 4 discusses rental income from existing rental property and from multi-unit purchases. The 75% vacancy and maintenance reduction factor is standard underwriting practice in those documented scenarios — confirmed by published guidance from Veterans United, AmeriSave, and AD Mortgage.

For a one-unit property with an ADU — Path 1 in our matrix — whether the ADU's projected or current rent counts is not a clean federal VA rule. It is a lender-specific call, and different lenders give different answers.

The conflict in the marketplace — resolved with a policy grid

| Source | One-unit ADU rent counted? | 75% factor for multi-unit? | Reserve requirement | Landlord experience | Last verified |

|---|---|---|---|---|---|

| Mortgage Solutions Financial | "Potential rental income typically isn't factored into loan qualification" | Not specified | Not specified | Not specified | May 20, 2026 |

| Veterans United | Counts on multi-unit; ADU on one-unit is lender-discretionary | 75% of appraiser's rent or lease (conservative) | 6 months full PITI reserves | Generally required for new landlords | May 20, 2026 |

| AD Mortgage | Counted at "discounted rate" when documented | Confirms 75% standard | Required at lender discretion | Commonly 2 years | May 20, 2026 |

| LA Metro Home Finder (Justin Borges) | "Some VA lenders" will count 75% for a legally permitted ADU with separate entrance, kitchen, and bath | Confirms 75% | Required for ADU rent on 1-unit | Generally required | May 20, 2026 |

| Bridgepoint Funding | Multi-unit only; ADU on 1-unit not explicitly addressed | Emphasis on residual income | Aligned with VA standards | Aligned with VA standards | May 20, 2026 |

The honest conclusion

The VA framework supports counting rental income at 75% in documented multi-unit and rental-property scenarios. For a one-unit-with-ADU purchase, whether rent counts depends on the lender's overlay, the appraiser's documentation, and the legal status of the unit. Call two or three VA-experienced lenders before assuming either way.

The three conditions that have to be true for ADU rent to count

- 1The ADU is legally permitted with the city or county.

- 2The VA appraiser assigns it a separate fair-market rent value — line-item on the market data grid per Chapter 11.

- 3The lender's overlay accepts ADU rental income on a one-unit-with-ADU property.

If you fail any one of these, rent does not flow through to qualifying — even if it flows through to your bank account post-closing.

A worked rental-income example (illustrative)

Scenario: $550,000 home in San Diego County with legally permitted detached ADU. Appraiser assigns $2,200/month ADU rent. Lender's overlay counts ADU rent.

- Qualifying rental income: $2,200 × 75% = $1,650/month ($19,800/year)

- At a 40% DTI target, supports roughly $660–$700/month of additional qualifying mortgage payment capacity

- At illustrative 6.5% rate on 30-year fixed, supports approximately $100,000–$110,000 of additional loan amount

Illustrative examples only. Actual results depend on local market conditions, the appraiser's rent schedule, your lender's overlay, your residual income, credit, current interest rates, and the underwriting decision.

💬 Want to know whether your lender counts the rent before you order an appraisal?

Use our ADU Rental Income Calculator to run your specific scenario by ZIP code and ADU type before you call a lender.

Explore VA loan options through our editorial partner Mortgage Research Center →Educational referral only. Dwelling Index is not a lender or broker. Loan approval, terms, fees, state availability, and program fit depend on lender review. We may earn a commission if you proceed, at no cost to you.

How the VA appraisal treats an ADU — and when it becomes a two-family problem

Answer capsule: Per VA Pamphlet 26-7 Chapter 11, the appraiser must determine whether the property is a single-family dwelling with an ADU (appraised on Form 1004) or a two-family dwelling (appraised on Form 1025). The call drives comparables, rental-income treatment, and whether the loan stays in the single-family lane or shifts to multi-unit pricing. The appraiser must also notify the lender if the property has more than one ADU.

The highest-and-best-use analysis (Chapter 11, Section 10)

VA defines highest and best use as "the most probable use which is physically possible, appropriately supported, legally permissible, financially feasible, and results in the highest value." For a property with an ADU, the appraiser is essentially asking: is this property most logically used as a single-family home with a smaller accessory unit, or as a two-family rental property?

Factors weighed:

- Relative size of the ADU vs. the primary dwelling (a 1,200 sq ft ADU on a 1,400 sq ft primary often gets reclassified)

- Whether the units have separate utilities, addresses, or entrances suggesting two-family use

- What comparable sales in the market support

- How the local zoning treats the parcel

When the appraiser flips the property to two-family — what changes

The appraisal form switches from Form 1004 to Form 1025 (Small Residential Income Property Appraisal Report). The appraiser must produce a rent schedule for both units. Comparable sales must include similar income-producing two-family properties — which may be in shorter supply in primarily single-family neighborhoods. For the lender, this can shift pricing tier, reserve requirements, and rental-income treatment.

Properties with more than one ADU — the sleeper issue

Pamphlet 26-7 requires the appraiser to notify the lender if a property has more than one ADU. Some lenders won't finance properties with more than one ADU under their VA overlay. This matters increasingly in California, where current state law allows a primary residence plus an ADU plus a JADU on a single-family lot.

Mixed-use properties — what VA actually requires

VA appraisal guidance on mixed-use properties focuses on whether the property is primarily residential, whether nonresidential use impairs residential character, whether the use is legal or legal nonconforming, and whether there is no more than one business unit. Some lenders publish a 75% residential / 25% nonresidential overlay; treat this as a common lender threshold, not a universal VA rule. Verify with your specific lender.

The MPR checklist that applies to the ADU

Chapter 12 (Minimum Property Requirements) applies to the ADU as part of the property. The appraiser checks zoning compliance, safety, soundness, sanitation across all units, adequate utilities (potable water, sanitary sewage disposal, permanent heating, safe ingress and egress), backyard access without passing through another living unit (Chapter 12, Section 4.g), pre-1978 lead-based paint clearance where applicable, and termite or pest treatment in moderate/heavy activity zones where infestation evidence exists. A problem on the ADU side can stall closing as easily as a problem in the main house.

💬 VA appraisal questions are best handled by a VA-experienced loan officer before you write an offer.

Explore VA loan options through our editorial partner Mortgage Research Center →Educational referral only. Dwelling Index is not a lender or broker. We may earn a commission if you proceed, at no cost to you.

Path 2 — Buy a 2–4 unit property and house-hack with VA (when this beats the ADU play)

Answer capsule: Most veterans who search "VA loan for ADU" are actually trying to solve the problem a 2–4 unit purchase solves cleaner: buy a property where rental income offsets the mortgage. The VA allows purchase of duplexes, triplexes, and fourplexes when entitlement, appraisal, and lender requirements support it, provided the veteran occupies one unit. All units must meet Minimum Property Requirements. Rental income on non-owner-occupied units typically counts at 75% of appraised market rent under standard multi-unit underwriting.

The 2–4 unit rules in plain English

- One- to four-unit residential properties are allowed (no five-plus)

- Owner-occupy one unit within VA's occupancy window

- All units inspected and must meet MPRs — a problem in a non-owner unit can still kill the deal at appraisal

- Appraisal uses Form 1025 (Small Residential Income Property)

- 75% of market rent counts on non-owner units under standard multi-unit underwriting; some lenders add 2 years of landlord experience, with 6 months full PITI reserves as the common substitute

- Mixed-use properties are eligible under VA's primarily-residential framework; lender overlays may impose specific residential/commercial ratios — verify before relying on this for a specific deal

Why this often beats Path 1 economically

A 2–4 unit property is designed to be income-producing. The appraisal form is built for it. Comparable sales are other income properties. The lender's overlay is calibrated for it. ADU rental income on a one-unit property is a category mismatch — it works when it works, but it is not the loan's native habitat.

If your real question is "how do I use my VA benefit to buy a property where rent covers most of my mortgage," a duplex or triplex purchase is often the cleaner path than a single-family-with-ADU.

Restoration of entitlement — the strategic move

VA allows a one-time restoration of full entitlement when you refinance the VA loan into a non-VA loan (typically conventional) — without selling the property. This is the move that lets veterans build a small rental portfolio while still using their VA benefit on successive primary residence purchases. Mark Severino's documented Orlando-then-Dallas case is the public example: Orlando home with ADU → Dallas duplex with restored entitlement. The caveat: this works once via refinance. Beyond that, restoring entitlement requires actually selling the property.

Can you use a VA construction loan for an ADU?

Answer capsule: Sometimes. Some participating VA construction lenders allow an ADU to be built alongside a new primary residence on a one-time-close construction loan. Other one-time-close investor channels exclude ADUs entirely. The answer depends on which lender's product you can actually access. Confirm ADU eligibility in writing before contract.

Path 3a — VA Cash-Out Refinance to fund the ADU build

A VA Cash-Out Refinance replaces your existing mortgage (VA, FHA, conventional, or USDA) with a new, larger VA loan and pays you the difference at closing. You use that cash to fund the ADU build.

What's allowed under VA rules

- • Up to 100% of reasonable value (38 CFR 36.4306)

- • Most 2026 lender overlays cap LTV at 90–95%

- • Replaces any loan type into a new VA loan (drops PMI)

- • Cash can be used for ADU construction

- • Not available on Texas homesteads

Seasoning requirements (VA Circular 26-19-22)

- • VA-to-VA: first payment due ≥ 210 days before closing AND ≥ 6 consecutive payments made

- • Non-VA-to-VA: no VA-imposed seasoning requirement (lender overlays may apply)

Worked funding-fee math at four loan amounts

| New VA cash-out loan amount | First-use fee (2.15%) | Subsequent-use fee (3.30%) | If funding-fee-exempt |

|---|---|---|---|

| $300,000 | $6,450 | $9,900 | $0 |

| $500,000 | $10,750 | $16,500 | $0 |

| $700,000 | $15,050 | $23,100 | $0 |

| $900,000 | $19,350 | $29,700 | $0 |

Source: VA.gov funding fee tables, rates effective April 7, 2023, in effect for 2026. Funding fee can be financed into the loan within the 100%-of-reasonable-value cap.

The funding-fee exemption matters. Per VA's official funding-fee page, the exemption applies to veterans receiving VA compensation for a service-connected disability; veterans eligible to receive such compensation but receiving retirement or active-duty pay instead; surviving spouses receiving DIC; service members with a qualifying pre-discharge claim rating; and qualifying Purple Heart recipients on active duty.

⚠️ When the cash-out math doesn't pencil

If you bought your home in 2020–2022 at a low rate, doing a VA cash-out refi to fund a $150,000 ADU build replaces your low-rate first with a new, higher-rate, larger mortgage. The funding fee adds another $6,450–$23,100. Closing costs add 2–5%.

For low ADU build budgets (under $100,000 — many garage conversions) on a low-rate first mortgage, a HELOC often pencils better than a VA cash-out refi. For larger builds where the math supports replacing the first mortgage, or where the existing mortgage is already higher-rate (FHA with MI, conventional with PMI), the VA cash-out becomes the stronger tool. Compare HELOC vs. VA cash-out in detail →

Path 3b — VA Construction Loan with ADU built alongside primary

The VA Construction Loan finances new primary-residence construction with no down payment available when entitlement and appraisal support it, and some participating lenders allow an ADU to be built alongside the primary structure.

Common lender overlays to verify in writing before you sign a builder contract:

| Overlay area | What lenders commonly publish | Notes |

|---|---|---|

| Pre-start work | Appraisal timing changes if construction is past foundation completion. Some OTC products treat pre-start as disqualifying. | VA Buyer's Guide; OneTimeClose.com OTC investor guidelines exclude ADUs entirely |

| Manufactured-home + ADU pairing | Most paired-construction products exclude this combination | Lender overlay |

| Self-build | Generally not permitted; lender/contractor rules apply | Veterans United 2026 guidance notes builders no longer need a VA Builder ID |

| Geography | Hawaii, Alaska, and Puerto Rico may be ineligible under specific OTC products | Lender overlay; verify by product |

| Acreage | Some VA construction lenders cap property size (commonly 10 acres or less) | Lender overlay |

| GLA minimums | Some products set a minimum gross living area for the ADU (commonly around 600 sq ft) | Lender overlay |

| Container homes, geodomes, A-frames, tiny homes | Often excluded | Lender overlay |

The bottom line on construction: the VA framework permits new construction, but the ADU pairing depends entirely on which participating lender you can actually reach. OneTimeClose.com publishes that its FHA/VA OTC investor guidelines do not allow ADUs. Other channels (VA Loan Network, VA Nationwide) do allow paired-construction ADUs. Get the ADU eligibility in writing as a condition of the construction contract.

🏡 Already in a VA-financed home in San Diego and ready to scope a build?

Our San Diego County ADU Builders guide covers the local builder picture.

Compare VA-experienced lenders through Mortgage Research Center →Educational referral only. We may earn a commission if you proceed, at no cost to you.

The Texas exception — VA cash-out refinance is not available on Texas homesteads

⚠️ Texas veterans: VA cash-out is off the table on homesteads

Texas AG Opinion KP-0183 (2018) concluded that the VA's loan guaranty is "additional collateral" prohibited under Texas Constitution Article XVI, Section 50(a)(6)(H). The opinion stated that the VA guaranty serves as collateral other than the homestead and therefore precludes a VA cash-out refinance loan in Texas. Texas veterans on a homestead property cannot use a VA cash-out refinance to fund an ADU build.

What this means for a Texas veteran wanting to build an ADU

If you live in Texas and want to use home equity to fund an ADU build, the realistic paths are:

- 1Texas Section 50(a)(6) home equity loan ("Texas Cash Out") — capped at 80% combined LTV, with specific Texas closing requirements (in-person closing at a title company, lender's office, or attorney's office; 12-day cooling-off period; lender fee cap of 2% excluding certain fees; primary homestead only).

- 2HELOC structured under Texas law — separate product framework with different rules; verify with a Texas-licensed lender.

- 3VA Alteration and Repair structure for purchase or specific improvement scope through a lender that allows it.

- 4Non-VA construction-to-permanent financing for new primary-plus-ADU construction.

- 5VA Purchase Loan if you are buying a new property that already has an ADU (the prohibition is specific to cash-out refinances on Texas homesteads, not to VA purchase loans with ADUs).

💬 Texas veteran researching ADU financing?

VA cash-out is off the table on Texas homesteads, but other VA paths may apply.

Educational referral only. We may earn a commission if you proceed, at no cost to you.

How much does an ADU actually cost, and which VA path can carry it?

Answer capsule: National 2026 averages put garage and basement conversions at roughly $60,000–$150,000, attached new construction at $100,000–$216,000, above-garage ADUs at $128,000–$225,000, and detached new construction at $110,000–$285,000+ before soft costs and high-cost-market premiums. ADU cost per square foot generally runs $150–$300 nationally, with coastal California markets reaching $250–$400+ per square foot.

ADU cost ranges by type (2026 data, source-mapped)

| ADU type | Typical 2026 cost range | Cost per sq ft | VA path most likely to carry it | Source |

|---|---|---|---|---|

| Garage conversion (attached) | $60,000 – $150,000 | $150 – $400 | Cash-out refi; alteration/repair if scope fits | Angi 2026 ADU Cost Guide |

| Garage conversion (detached) | $75,000 – $225,000 | $150 – $400 | Cash-out refi; sometimes alteration/repair | Angi; GatherADU 2026 |

| Basement conversion | $60,000 – $150,000 | $100 – $200 | Cash-out refi; alteration/repair | Angi |

| Attached ADU (new build) | $100,000 – $216,000 | $200 – $350 | Cash-out refi; VA construction (with primary) | SelfStorage.com 2026 |

| Above-garage ADU | $128,000 – $225,000 | $250 – $400 | Cash-out refi; VA construction (paired) | SelfStorage.com 2026 |

| Detached ADU (new build) | $110,000 – $285,000+ | $200 – $400+ | Cash-out refi; VA construction (paired); rarely renovation loan | Angi; SelfStorage.com 2026 |

| Junior ADU (within existing footprint) | $80,000 – $150,000 | $200 – $350 | Alteration/repair; cash-out refi | SelfStorage.com 2026 |

| Prefab ADU (all-in installed) | $150,000 – $400,000+ | Varies by brand | Cash-out refi; rarely paired with construction | Industry pricing surveys, May 2026 |

National averages — California, coastal markets, and high-cost metros run materially higher. Last verified May 20, 2026. Illustrative ranges, not guarantees. Actual cost depends on local labor, utility upgrades, design, permits, site conditions, financing costs, and regulatory approvals.

What this means for your VA path choice

- Under $50,000 in scope (basic garage conversion, light basement finish): A VA cash-out refi is usually overkill given closing costs and the funding fee. A HELOC or home equity loan typically pencils better.

- $50,000–$150,000 in scope (most garage conversions, basement conversions, JADUs): VA cash-out refi can work if you are replacing a higher-rate first mortgage or qualifying for the funding-fee exemption. Otherwise, a HELOC often beats it.

- $150,000–$300,000 in scope (attached ADUs, detached new builds): VA cash-out refi or a paired VA construction loan if you are building a new primary as well.

- Over $300,000 in scope (large detached ADUs, prefab installs in coastal markets): You typically need a construction loan rather than equity-tap financing.

Path 4 — CalVet and state veteran loan programs

Answer capsule: Several states layer their own veteran home loan programs on the federal VA program. California's CalVet is the largest and most ADU-relevant for veteran homeowners. CalVet's Construction Loan, Home Improvement Loan, and Rehabilitation Loan can each apply to ADU-related work depending on the product, eligibility, and current bond fund availability. When a CalVet product uses the federal VA guaranty, VA funding-fee rules may apply.

CalVet for California veterans

Eligibility

- • Served ≥ 90 days active duty (excluding training), or active National Guard/Reserve under federal Title 10 or Title 32 with 30+ consecutive days

- • Discharge under honorable conditions

- • Purchasing or refinancing a California owner-occupied home

- • No current CalVet loan (previous CalVet loans paid in full are eligible again)

- • No prior California residency required

ADU-relevant products

- • CalVet Construction Loan — builds a new home or places a manufactured home on a property.

- • CalVet Home Improvement Loan — primarily for existing CalVet mortgage customers. Verify eligibility directly with calvet.ca.gov.

- • CalVet Rehabilitation Loan — purchase a home in need of repair and fund the rehab with one loan.

CalVet underwrites manually (no minimum credit score) and often combines the federal VA guaranty with state bond funding to deliver up to 100% financing with no monthly PMI. When the specific CalVet product uses the federal VA guaranty, the VA funding-fee rules apply. Verify the specific product structure with CalVet before assuming.

Other state veteran programs (brief survey)

- Texas Veterans Land Board (VLB) — home loans, land loans, and home improvement loans for eligible Texas veterans. Note that the Texas cash-out restriction still applies to any cash-out refinance on a Texas homestead, regardless of the program label.

- Oregon ORVET Home Loan — purchase loans only; not a construction or improvement product.

- Wisconsin WisVet — veteran assistance and grants; not a home loan program per se.

We did not verify every state veteran loan program for 2026 ADU treatment; check with your state's veteran affairs department before assuming.

VA disability housing grants — when SAH and SHA matter for an ADU

Answer capsule: Two VA disability housing grants can fund accessibility-related ADU work for eligible veterans with service-connected disabilities. The Specially Adapted Housing (SAH) grant provides up to $126,526 in FY 2026. The Special Housing Adaptation (SHA) grant provides up to $25,350 in FY 2026. These are grants, not loans — no repayment, and they do not reduce your VA loan entitlement. HISA does not pay for new construction or exterior buildings.

FY 2026 grant amounts (verified May 20, 2026)

| Grant | Maximum FY 2026 | Use | Important limitation |

|---|---|---|---|

| Specially Adapted Housing (SAH) | $126,526 | Build, buy, or adapt a permanent home for qualifying severe service-connected disabilities | Up to 6 uses across lifetime, cumulative |

| Special Housing Adaptation (SHA) | $25,350 | Smaller-scale modifications for qualifying upper-body or vision-related service-connected disabilities | Up to 6 uses across lifetime, cumulative |

| TRA — SAH-eligible | $50,961 | Modify a family member's home where the veteran temporarily resides | — |

| TRA — SHA-eligible | $9,100 | Same purpose, lower disability tier | — |

| HISA (service-connected) | $6,800 | Medically necessary alterations | Does not pay for new construction or exterior buildings |

| HISA (non-service-connected) | $2,000 | Medically necessary alterations | Does not pay for new construction or exterior buildings |

Source: VA.gov disability housing grants page; verified May 20, 2026.

Edge case: combining SAH with an ADU build

A growing use case: a veteran with mobility needs uses SAH funds to build an accessibility-adapted ADU on a property where the main home cannot easily be adapted. The grant funds the adaptive elements of the ADU; the veteran funds the non-adaptive elements through other means (cash, HELOC, or VA cash-out refi where state law allows). This requires close coordination with a VA SAH Agent and is not how every ADU builder will be familiar working — but it is permitted.

If accessibility is your driver, start at VA.gov disability housing grants before you start with a lender.

What to ask a VA lender before you apply (the 10-question vetting script)

Answer capsule: Not every VA-approved lender handles ADU deals well. The wrong loan officer will tell you "VA can't do that" when the issue is their own overlay, not VA policy. Vet the lender with these ten questions before you let them pull your credit. The answers separate VA-fluent lenders from VA-generic ones.

| Ask this | What you're really finding out |

|---|---|

| "Do you finance VA purchases with legally permitted ADUs?" | Separates ADU-capable from ADU-unfamiliar |

| "Will you treat a legal ADU as single-family with ADU (Form 1004) or two-family (Form 1025)?" | Affects appraisal, comps, eligibility, and pricing |

| "What is your policy on counting rental income from an ADU on a one-unit property?" | The lender-overlay answer that varies widely |

| "Do you require landlord experience or reserves to count ADU rent?" | Tells you whether the income flows to qualifying or sits on the sidelines |

| "What is your maximum LTV on a VA Cash-Out Refinance in 2026?" | Reveals overlay tightness vs. VA's 100%-of-reasonable-value framework |

| "Does your VA Construction Loan product allow an ADU paired with the primary build?" | Hard yes/no — the answer is product-specific |

| "Have you closed a VA loan on a property with a legally permitted detached ADU in the last 12 months?" | Recency of experience matters more than years of generic VA work |

| "What documents do you need from the appraiser regarding the ADU?" | Rent schedule, separate market-grid line item, permit verification — get the list before appraisal |

| "What is your funding-fee exemption verification process?" | Disability-exempt veterans sometimes get charged the fee in error and have to claim a refund |

| "What state restrictions apply to your VA cash-out product?" | Texas is the big one — but other state-specific overlays may apply |

If a loan officer can answer these without checking with their underwriter, you are talking to someone who actually does these deals. If they are checking on every question, keep dialing.

💬 Skip the cold-calling.

Our editorial partner Mortgage Research Center can help you explore VA loan options with participating mortgage professionals.

See your options through Mortgage Research Center →Educational referral only. Dwelling Index is not a lender or broker. Loan approval, terms, fees, state availability, and program fit depend on lender review. We may earn a commission if you proceed, at no cost to you.

High-demand market snapshot — where VA-for-ADU plays differently

Answer capsule: VA-for-ADU plays differently depending on where you live. California's ADU framework generally protects ADUs in specified configurations. Texas has the constitutional cash-out restriction. Florida and Virginia have growing veteran-buyer markets but less mature statewide ADU regulation.

| Market | ADU legality framework | VA cash-out availability | What to verify before offer |

|---|---|---|---|

| California — Greater San Diego | HCD 2026 ADU framework protects ADUs in specified configurations; San Diego County and city ordinances allow detached, attached, and JADU on most single-family lots | ✓ Available | Permit history; coastal-zone overlays (Del Mar, Solana Beach); city-specific fee schedule |

| California — Bay Area | HCD 2026 framework applies | ✓ Available | Local design standards; fire-zone restrictions; utility lateral capacity |

| California — Los Angeles County | HCD 2026 framework applies | ✓ Available | Hillside/seismic overlays; LADBS plan-check timelines; rent-control implications |

| Texas — San Antonio / Killeen / Houston / Austin / Dallas | Varies widely by city; veteran-heavy markets near military installations | ✗ Not available on Texas homesteads — AG Opinion KP-0183 | Section 50(a)(6) alternatives; local STR restrictions |

| Florida — Tampa / Jacksonville / Pensacola / Orlando | Varies by county; no statewide ministerial framework | ✓ Available | Storm/wind code; flood-zone insurance; HOA disclosure |

| Virginia — Norfolk / Virginia Beach / Loudoun | Varies; "Affordable Dwelling Unit" programs in some VA counties are not the same as accessory dwelling units — confirm which you mean | ✓ Available | Local zoning; military-housing market overlap |

| Washington — JBLM / Spokane | Detached ADUs permitted in most cities; King County has expanded ADU allowances | ✓ Available | City-specific permit timelines; design standards |

| Colorado — Colorado Springs / Denver metro | Denver and many metro cities allow ADUs; rural areas vary | ✓ Available | Lot size minimums; utility extension costs |

Verification sources: California HCD 2026 ADU handbook; Texas AG Opinion KP-0183; municipal ordinances and zoning codes accessed May 2026. Verify with your local planning department before committing to a property.

San Diego County — our deepest local coverage

For veterans buying or building in Greater San Diego — including San Diego, Oceanside, Carlsbad, Encinitas, Del Mar, Solana Beach, Poway, San Marcos, Escondido, La Mesa, El Cajon, Vista, Chula Vista, Santee, Lemon Grove, Imperial Beach, National City, Bonsall, Camp Pendleton, Cardiff By The Sea, La Costa, and unincorporated San Diego County — our San Diego County ADU Builders guide covers local builders, real fees by city, and the 14-point bid checklist we use.

🏗️ Planning a build in Greater San Diego?

SnapADU is our approved partner for ADU builds in San Diego County.

See current pricing and floor plans →Service area: Greater San Diego only. Affiliate disclosure applies. We may earn a commission if you proceed.

The honest limitations — what we tell every veteran asking us this question

Answer capsule: VA-for-ADU works, but the program is built for veteran housing, not investment portfolio building. Four real limitations affect almost every borrower: the unpermitted-ADU appraisal trap, lender-overlay variation on rental income, the cash-out math when you have a low-rate first mortgage, and the entitlement arithmetic if you want to repeat the play.

Limitation 1: The unpermitted-ADU appraisal trap

Most "ADUs" on resale listings are unpermitted. Many were finished garages from 10–20 years ago, basement conversions without separate egress, or sheds with kitchenettes added. The VA appraiser will flag them. Three outcomes are possible: (1) the seller agrees to legalize the unit before closing (usually requires plan check, permits, sometimes structural work, and a 30–90 day delay), (2) the seller agrees to remove the unit's "dwelling" features (kitchen typically) so it can be valued as bonus space or storage, (3) the deal falls apart.

Limitation 2: Lender-overlay variation on rental income

VA permits counting ADU rent under documented multi-unit and rental-property scenarios. Whether your lender counts it on a one-unit-with-ADU property — and at what rate, with what reserves, requiring what landlord experience — varies. We have seen identical scenarios approved at one lender and declined at another, both VA-approved, both reputable. Plan to call two or three.

Limitation 3: The cash-out math when your first mortgage is low-rate

If you bought your home with a VA loan in 2020–2022 at a low rate, the cash-out refi math to fund a $100,000–$150,000 ADU build is unforgiving. You would replace your low-rate first with a current-rate first, add the funding fee, plus closing costs.

Limitation 4: Entitlement arithmetic

VA allows one-time restoration of full entitlement via refinance into a non-VA loan. Beyond that, restoration requires sale. If you want to 'house hack' three properties in five years using VA, the math runs out before the strategy does. This is by design — VA is a housing benefit, not an investment-portfolio subsidy.

Frequently asked questions

Can I use a VA loan to buy a home with an ADU?▾

Yes, with conditions. A VA Purchase Loan can buy a single-family home with a legal, permitted ADU on the same lot, with no down payment available when entitlement, appraisal, and lender requirements support it. You must intend to occupy the home as your primary residence and move in within VA's occupancy window — commonly 60 days after closing, with documented exceptions. The ADU must comply with local zoning, and the appraiser values the property as a single real estate entity per VA Pamphlet 26-7, Chapter 11.

Can I use a VA loan to build an ADU in my backyard?▾

Sometimes, but not as a standalone product. The two realistic paths are (a) a VA Cash-Out Refinance on a home you already own — not available on Texas homesteads — or (b) a VA Construction Loan that builds your new primary residence and the ADU simultaneously, subject to the participating lender's product overlays. Most VA renovation lenders cannot fund a detached ADU not connected to the main residence; Chase publishes this restriction explicitly.

Can a VA cash-out refinance pay for an ADU?▾

In most states, yes. VA Cash-Out Refinance can let eligible borrowers take cash out for home improvements, including ADU construction. VA permits up to 100% of reasonable value (38 CFR 36.4306); most 2026 lender overlays cap at 90–95%. The funding fee is 2.15% first use / 3.30% subsequent use of the new loan amount, with no equity discount. Not available on Texas homesteads per Texas AG Opinion KP-0183.

Can I use a VA IRRRL to build an ADU?▾

No, not directly. The Interest Rate Reduction Refinance Loan (IRRRL) is a rate-reduction product that refinances an existing VA loan into a new VA loan at a lower rate. It cannot provide cash for an ADU build. The funding fee is a flat 0.5%. For ADU funding, use a VA Cash-Out Refinance instead (outside Texas).

What are VA loan ADU requirements?▾

The key requirements: (1) the ADU is part of the same property as the primary dwelling and treated as a single real estate entity per Pamphlet 26-7 Chapter 11; (2) the ADU is legally permitted under local zoning; (3) the borrower will occupy the main home or the ADU as primary residence; (4) the property meets VA Minimum Property Requirements per Chapter 12; (5) the appraiser values the property correctly (Form 1004 for single-family-with-ADU, Form 1025 if reclassified as two-family); and (6) the lender's specific overlay allows the deal.

Does VA count rental income from an ADU?▾

VA underwriting guidance supports counting rental income at 75% for documented multi-unit and rental-property scenarios. Whether your specific lender counts ADU rent on a one-unit-with-ADU property depends on their overlay. Some lenders will not count it; others will if the ADU is legally permitted, self-contained, and the appraiser assigns it a separate fair-market rent value. Call two or three VA-experienced lenders before assuming either way.

Does a property with an ADU count as a two-unit property for VA?▾

It depends on the VA appraiser's highest-and-best-use analysis (Pamphlet 26-7 Chapter 11 Section 10). If they determine the property is a two-family dwelling, the appraisal uses Fannie Mae Form 1025. If they determine it is a single-family with an ADU, the appraisal uses Form 1004 and the ADU appears as a separate line item on the market data grid. The call is the appraiser's, based on relative size, separate utilities, and what market comparables support.

Can a manufactured home be an ADU under VA rules?▾

Yes. VA Pamphlet 26-7 Chapter 11 explicitly says a manufactured home on the site can be an ADU. However, on most VA Construction Loan products, you cannot pair a manufactured-home primary residence with an ADU under the lender's product overlay.

How does the VA funding fee work on a cash-out refinance to build an ADU?▾

The funding fee is 2.15% of the new loan amount for first-time VA use and 3.30% for subsequent use. There is no equity-based discount on the cash-out funding fee. The exemption applies to veterans receiving VA compensation for a service-connected disability, those eligible but receiving retirement or active-duty pay instead, qualifying surviving spouses, qualifying pre-discharge claim ratings, and qualifying Purple Heart recipients on active duty. The fee can be financed into the new loan within VA's 100%-of-reasonable-value cap.

Can I rent the ADU on Day 1 after closing with a VA loan?▾

Federally, yes — provided you occupy the main home as your primary residence and meet VA's occupancy framework. Local rules can still restrict your plans: rental registration requirements, HOA covenants, and short-term rental ordinances vary widely. The ADU is rentable under federal VA rules; local rules may add steps.

What if the ADU is unpermitted?▾

Almost certainly a problem. The VA appraiser will flag unpermitted living units. The lender will typically require legalization, removal of the dwelling features so the unit can be valued as bonus space, or treatment of the structure as storage. Many deals stall at this stage. Pull permit history before writing the offer.

Does a mother-in-law suite count as an ADU?▾

It can, but the label does not decide it. VA appraisal guidance defines an ADU by its features — kitchen, sleeping, and bathroom facilities — not by its nickname. If the in-law suite has its own kitchen, full bath, and sleeping area, and is legally permitted, the appraiser will likely treat it as an ADU. If it lacks a kitchen, it is typically valued as bonus living space.

Does CalVet finance ADUs in California?▾

CalVet offers construction loans, home improvement loans, and rehabilitation loans that can apply to ADU projects for eligible California veterans. The CalVet Home Improvement Loan is primarily for existing CalVet mortgage customers making improvements to CalVet-financed homes — verify your specific eligibility directly with calvet.ca.gov. When a CalVet product uses the federal VA guaranty, the VA funding-fee rules may apply.

Can VA disability housing grants help with an ADU?▾

Yes, for accessibility-related ADU work. The SAH grant ($126,526 in FY 2026) and SHA grant ($25,350 in FY 2026) can fund construction or adaptation of housing for qualifying service-connected disabilities. The grants are separate from your VA loan entitlement and require coordination with a VA Specially Adapted Housing Agent. They are not general ADU funding tools — they fund the adaptive portion of the build. HISA ($6,800/$2,000) covers medically necessary alterations but does not pay for new construction or exterior buildings.

How long do I have to wait to use a VA cash-out refinance after closing on a VA loan?▾

For a VA-to-VA cash-out refinance, the loan being refinanced must be seasoned per VA Circular 26-19-22: the first monthly payment must be due at least 210 days before the refinance closing AND you must have made at least six consecutive monthly payments on the original loan. For non-VA-to-VA cash-out (refinancing an FHA, conventional, or USDA loan into VA), there is no VA-imposed seasoning requirement, though individual lenders may impose their own overlays.

What we verified for this guide

Last verified:

| Source category | Specific sources cross-referenced |

|---|---|

| Primary VA documents | VA Pamphlet 26-7 Chapter 11 (Appraisal Report); Chapter 4 (Credit Underwriting); Chapter 12 (Minimum Property Requirements); VA.gov funding fee tables; VA.gov Purchase Loan; VA.gov Cash-Out Refinance; VA.gov IRRRL; VA.gov Disability Housing Grants; VA Circular 26-19-22 (cash-out seasoning); 38 CFR 36.4306 |

| Lender policy | Veterans United (multi-family, rehab, rental income, 2026 construction loan guidance); Chase VA Renovation Loan; VA Loan Network 2026 construction loan policy; AmeriSave VA loans for investment property; AD Mortgage 2026 VA investment property guide; Bridgepoint Funding multi-unit policy; OneTimeClose.com one-time-close investor guidelines |

| VA ADU rental income | Veterans United 75% rule; AD Mortgage 2026 guidance; LA Metro Home Finder (Justin Borges); Mortgage Solutions Financial (cited as counterpoint) |

| Texas exception | Texas AG Opinion KP-0183 (2018); Texas Constitution Art. XVI, § 50(a)(6)(H); Polunsky Beitel Green legal analysis |

| California ADU framework | California HCD 2026 ADU Handbook; local municipal ordinances |

| CalVet | calvet.ca.gov product pages |

| Cost data | Angi 2026 ADU Cost Guide; SelfStorage.com 2026 ADU Construction Cost report; GatherADU 2026 Garage Conversion Guide |

| SAH / SHA / HISA grants | VA.gov disability housing grants page; VA Prosthetics HISA page |

| Internal site inventory | dwellingindex.com Financing category review |

Editorial conclusions we made (stated as such):

- •That the three-path framework (Buy with existing ADU / 2–4 unit house-hack / Cash-out or paired construction to build) is the cleanest decision structure for veterans searching this term — based on our review of 15+ competitor pages and four forum threads.

- •That lender-overlay variation on ADU rental income is the largest source of public confusion — based on direct conflicts observed between Mortgage Solutions Financial and Veterans United / AD Mortgage / LA Metro Home Finder.

What we did not verify:

- •Pending Congressional legislation that may alter VA funding fee tables beyond their April 7, 2023 base.

- •Exact 2026 ADU treatment under every state veteran loan program outside CalVet.

Next scheduled review: August 2026 (quarterly cadence).

How we built this guide

We read VA Pamphlet 26-7 Chapters 4, 11, and 12 directly. We cross-referenced the guidance against the published policies of seven VA-experienced lenders. We reconciled three points where lender claims publicly conflict — most importantly the rental-income question — and converted what we found into the decision matrix at the top of this page. Dollar figures are calculated from VA.gov's published funding fee tables effective April 7, 2023. The Texas cash-out restriction is sourced directly to Texas AG Opinion KP-0183 and the Texas Constitution. Cost ranges are sourced row-by-row to published 2026 data, with the source named in the cost table. Where lender practice varies, we say so plainly rather than picking one answer.

We are not a lender, broker, or builder. We do not sort comparison tables by commission. We disclose every affiliate relationship at the link and again in the affiliate disclosure. Full methodology: /methodology/. Affiliate disclosure: /affiliate-disclosure/.

Your next step

You are at one of five points right now, and the right next move depends on which:

If you are targeting a specific property with an existing ADU →

Verify the ADU's permit status today. Many counties provide permit lookup online or by phone. If permits do not exist, you need a contingency in the offer or a different property. Then run the address through our free property feasibility check.

Run the free feasibility check →If you already own a home and want to build an ADU (outside Texas) →

Run the cash-out-vs-HELOC math first. If your existing first mortgage rate is at or below current market, a HELOC often beats a VA cash-out refi for sub-$100K builds. If your rate is above current market or you are funding a $150K+ build, the VA cash-out math gets stronger.

Compare ADU financing paths →If you are a Texas veteran →

VA cash-out refinance is off the table on Texas homesteads. Look at Texas Section 50(a)(6) home equity loans, HELOCs, or VA Purchase / VA Construction paths if you are buying or building rather than refinancing.

Compare ADU financing paths →If you are buying new construction and want an ADU built alongside →

Confirm in writing that your lender's VA construction loan product allows paired ADU construction (not all do) and verify the pre-start rule. Then identify a participating-lender-approved builder familiar with the paired-construction product.

If accessibility is your driver →

Start at VA.gov disability housing grants before you start with a lender. The SAH or SHA grant may fund significant portions of the adaptive scope, and the grant arithmetic affects how much loan you actually need.

VA.gov disability housing grants →Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds. No email required.

🏡 Run the free Path Picker →See your matching VA path, your specific next two steps, and the permit-history questions to ask in your jurisdiction.

📄 Download the free ADU Starter KitIncludes the 10-question lender vetting checklist, the funding-fee math table at six common loan amounts, and the unpermitted-ADU pre-offer checklist.