RenoFi Alternatives for ADU Financing: 9 Real Paths Compared (2026)

The bottom line on RenoFi alternatives for an ADU (read this first)

RenoFi is a renovation-financing broker — not a direct lender — that uses your home’s after-renovation value (ARV), meaning what your home will be worth once the ADU is built, instead of its current value. That’s a genuine advantage if your current equity won’t cover the build. It’s the wrong tool if you already have enough current equity, live in a state RenoFi can’t serve, or need the fastest possible timeline.

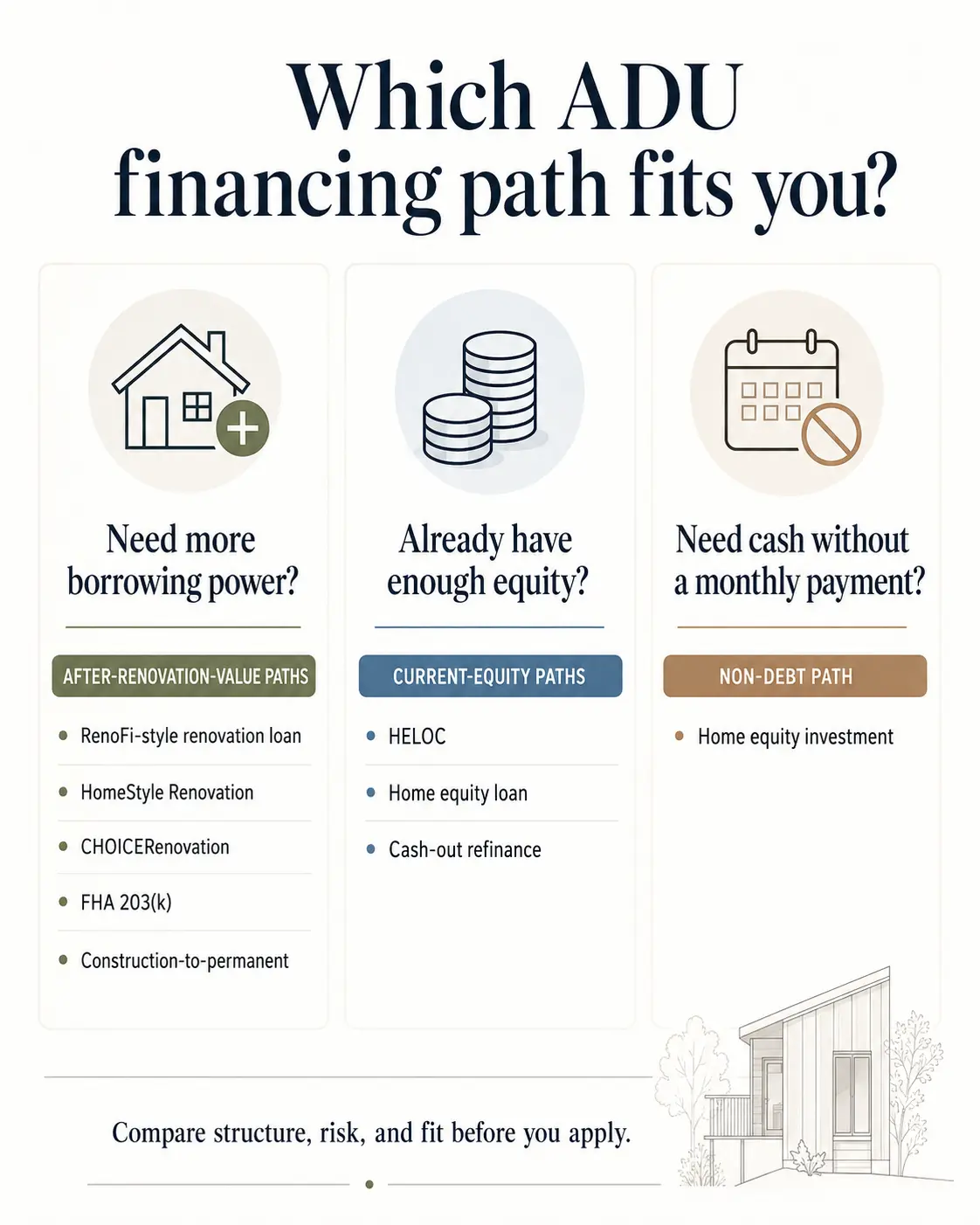

Your nine realistic alternatives fall into three buckets:

- Other after-renovation-value paths — Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA 203(k) (Standard and Limited), and direct construction-to-permanent loans. These also use the as-completed appraised value. They differ from RenoFi in lien position, transaction type, draw mechanics, and whether they replace your first mortgage — but they’re direct-lender products, often on conforming terms.

- Current-equity paths — a traditional HELOC, a fixed-rate home equity loan (HELOAN), or a cash-out refinance. These ignore your future ADU value. They’re faster and more widely available, but only work if you have enough equity in your home today.

- Non-debt paths — Home Equity Investments (HEIs) from Hometap, Unlock, or Point. You get cash now in exchange for a share of your home’s future value, with no required monthly payment. Useful when you can’t qualify for debt or can’t add a payment — but the eventual settlement can cost more than a comparable loan, and these carry real consumer-protection concerns.

If you live in Texas, New York, Hawaii, or Massachusetts: RenoFi’s flagship ARV Renovation Loan is currently unavailable or restricted in your state. The strongest ARV alternatives are a Fannie Mae HomeStyle Renovation loan or a construction-to-permanent loan from a national lender.

See What You Can Build → Get Your Free ADU ReportCheck your lot fit, size cap, and city fee math before you spend an hour comparing lenders. Free, no signup, 60 seconds.

By the Dwelling Index Editorial Team · Last updated: May 21, 2026 · Last verified: May 21, 2026 · ~40 min read

Independent editorial comparison. The Dwelling Index is not a lender, broker, or builder. See our affiliate disclosure below.

The 9 RenoFi alternatives at a glance (2026 decision matrix)

Built from primary sources: RenoFi’s own product pages and corporate disclosures (NMLS #1802847 and #2412747), Fannie Mae’s Selling Guide and Announcement SEL-2025-08, Freddie Mac’s CHOICERenovation page, HUD 203(k) documentation and 2026 FHA loan-limit announcement, FHFA 2026 conforming loan limits, and Curinos/Bankrate rate data for mid-to-late May 2026.

| ID | Path | Lender type | Uses ARV? | Rate range (May 2026) | Max borrow ceiling | Disbursement | State gaps | Replaces 1st mortgage? |

|---|---|---|---|---|---|---|---|---|

| A | RenoFi HELOC | Broker → partner credit union | ✅ Up to 95% of ARV | Variable, prime + margin; partner-CU pricing | Up to $750,000 | Revolving line; draw as needed for up to 10 years | Not in NY (DFS notice); Bankrate also lists HI and MA; TX excluded from ARV network | No (second lien) |

| B | RenoFi Fixed-Rate Renovation HELoan | Broker → partner credit union | ✅ Up to 90% of ARV | Fixed; 10-, 15-, or 20-yr terms | Up to $750,000 | Lump-sum; no draws/inspections per RenoFi | Same gaps as Path A | No (second lien) |

| C | Fannie Mae HomeStyle Renovation | Direct lender (conforming GSE) | ✅ As-completed appraisal | Conforming first-mortgage rates | 97% LTV; 2026 limit $832,750 / $1,249,125 high-cost | Construction draws; up to 50% of reno costs at closing | Nationwide | Yes (first mortgage) |

| D | Freddie Mac CHOICERenovation | Direct lender (conforming GSE) | ✅ As-completed appraisal | Conforming rates | Same conforming limits as HomeStyle | Construction draws | Nationwide; purchase and no-cash-out refinance only | Yes |

| E | FHA 203(k) Standard | FHA-insured direct lender | ✅ As-completed appraisal | FHA-rate region + mortgage insurance | 2026 floor $541,287; ceiling $1,249,125 | Draws via HUD consultant | Nationwide; requires ≥$5,000 in rehab costs | Yes |

| E2 | FHA 203(k) Limited | FHA-insured direct lender | ✅ As-completed appraisal | FHA-rate region | Rehab budget capped at $75,000 (HUD) | Limited draws | Nationwide; must fit Limited scope | Yes |

| F | Construction-to-Permanent Loan | Direct lender (bank/CU) | ✅ As-completed appraisal | Conforming + ~0.5%–1.5% during construction | Lender-set; jumbo options available | Construction draws; converts to permanent on CO | Nationwide; lender-set criteria | Yes (converts to permanent) |

| G | Cash-Out Refinance | Direct lender | ❌ Current value only | Conforming first-mortgage rate range (~6.75%) | Typically 80% of current value | Lump-sum | Nationwide; TX Section 50(a)(6) caps at 80% | Yes (replaces 1st) |

| H | Traditional HELOC | Direct lender (bank/CU) | ❌ Current value only | ~7.21%–7.41% avg (Curinos/Bankrate, May 2026) | Typically 80–85% CLTV on current value | Revolving line | TX caps CLTV at 80% per Tex. Const. §50(a)(6) | No (second lien) |

| I | Hometap Home Equity Investment (HEI) | Equity-share investor (not a loan) | ❌ Current value only | Not a loan — value-sharing formula | Up to $600,000; ≥25% current equity required | Lump-sum | 16 states (AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, VA); MA AG suit ongoing | No |

| J | Figure HELOC (current-equity, digital) | Direct lender (fintech) | ❌ Current value only | Variable HELOC range | Lines up to $750,000; funding in as few as 5 days | Lump-sum draw at origination | Not for NY mortgage applications per Figure's site | No (second lien) |

About this matrix: Rate ranges reflect published averages, not personal offers. State availability and product caps change. Verify directly with the provider before you apply. We re-verify this matrix monthly.

See your lot fit, size cap, and city fees first — then you’ll know which financing ceiling you actually need.

What is RenoFi, and why do people look for alternatives?

How after-renovation value (ARV) works

A traditional HELOC or home equity loan looks at your home’s current fair-market value, subtracts your mortgage balance, and lends you a percentage of what’s left. An ARV-based loan looks at what your home will be worth after the ADU is finished, using an “as-completed” appraisal based on your contractor’s bid and plans.

Here’s the gap in real numbers. Say your home is worth $750,000 today, you owe $500,000, and you want to build a $300,000 ADU that the appraiser believes will lift the as-completed value to $1,050,000:

- Traditional 80%-CLTV HELOC: $750,000 × 80% − $500,000 = $100,000 available. Doesn’t cover the build.

- Traditional 85%-CLTV HELOC (where allowed): $750,000 × 85% − $500,000 = $137,500. Still short.

- ARV-based path at 90% of completed value: $1,050,000 × 90% − $500,000 = $445,000 theoretical. Covers the build with contingency room.

These numbers are illustrative; your appraisal, lender’s LTV cap, and the ADU’s actual value-add determine your real figure.

RenoFi is a broker, not a direct lender

RenoFi’s footer states it plainly on every page: “RenoFi is not a lender, rather we’ve partnered with lenders that leverage RenoFi’s technology to seamlessly provide RenoFi Loans. Loans are arranged through these partner third-party lenders.” (Verified at renofi.com, May 21, 2026.) The lender on your closing documents is a credit union — not RenoFi. That means two layers of underwriting before funding. Some homeowners experience this as a useful concierge. Others experience it as a longer timeline than going straight to a HELOC lender.

The three triggers that send people searching

- State exclusions. Texas, New York, and — per Bankrate’s February 2026 review — Hawaii and Massachusetts can’t get RenoFi’s flagship ARV product. We cover each below.

- Process speed. RenoFi’s own testimonials describe the process as “thorough” but “long.” For homeowners with expiring contractor bids or a tight build window, broker-routed timelines are real friction.

- Discovery of direct-lender ARV options. Most people don’t know Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA 203(k), and construction-to-permanent loans also use as-completed appraisals. Once they learn it, RenoFi stops being the only ARV game in town.

Sources: renofi.com/how-it-works/; Bankrate RenoFi review, Feb 27, 2026.

One honest tradeoff up front: ARV lending — RenoFi’s or anyone else’s — is the right tool for a specific borrower. If you bought recently, hold a 3%–4.5% pandemic-era mortgage you want to keep, and don’t have enough current equity for a traditional HELOC, RenoFi (or an equivalent direct credit-union second-lien renovation HELOC) can unlock borrowing power nothing else will. If you have enough equity today, or you’re willing to refinance into a HomeStyle Renovation first mortgage, you can usually get a better rate and faster funding elsewhere.

Where can’t RenoFi serve you? The state-availability problem

Texas — Section 50(a)(6) and the 80% CLTV cap

Texas has the most restrictive home-equity lending rules in the country, written into the state constitution. Texas Constitution Article XVI, Section 50(a)(6) caps total combined loan-to-value on a home-equity loan against your Texas homestead at 80%, requires a 12-day cooling-off period between application and closing, and restricts certain fee structures. ARV-based second-lien products don’t fit cleanly inside that frame. RenoFi’s own site notes a personal-loan product is available in Texas, but that’s a different product — not the ARV Renovation Loan.

Texas ADU homeowner alternatives that work: Fannie Mae HomeStyle Renovation (nationwide, as-completed appraisal, conforming rates); a construction-to-permanent loan from a Texas bank or credit union; or a traditional Texas HELOC if you have enough current equity to stay inside the 80% cap.

New York — the DFS authorization gap

RenoFi’s footer carries an explicit notice: “This site is not authorized by the New York State Department of Financial Services. No mortgage solicitation activity or loan applications for properties located in the State of New York can be facilitated through this site.” (Verified May 21, 2026.) New York ADU homeowners should look at HomeStyle Renovation, CHOICERenovation, FHA 203(k), or a direct New York HELOC or HELOAN.

Hawaii and Massachusetts — Bankrate’s flagged exclusions

Bankrate’s February 27, 2026 RenoFi review lists Hawaii, New York, and Massachusetts as states where RenoFi is not a licensed broker. We have not seen RenoFi confirm Hawaii and Massachusetts on its own corporate pages, so we attribute this to Bankrate. Massachusetts is worth a special note: the state has become hostile territory for several alternative home-equity products after the Massachusetts Attorney General sued Hometap in February 2025 — more on that in the HEI section below.

Everywhere else — RenoFi’s national footprint

Outside Texas, New York, Hawaii, and Massachusetts, RenoFi describes its partner network as covering the rest of the country, though the exact partner credit union and product depend on your state. RenoFi operates as Renovation Technologies Holdings Inc. in California (NMLS #2412747), Renovation Technologies LLC in Nebraska, and RenoFi LLC in New Mexico, and as Renovation Finance LLC elsewhere.

Explore current renovation, refinance, and construction-loan rates from licensed mortgage lenders →

Compare Lender Rates →Disclosure: we may earn a commission if you proceed. Rates and approval depend on your lender, credit profile, and property. This is not a guarantee of approval or rate.

Sources: renofi.com footer (NY DFS notice); Bankrate RenoFi review Feb 27, 2026; Texas Constitution Article XVI, Section 50(a)(6).

Is RenoFi a real lender, or a middleman?

The published RenoFi flow has four stages: a discovery call with a RenoFi advisor; “renovation underwriting” where you upload plans and a contractor bid through RenoFi’s portal; a current-value and after-renovation-value appraisal; and a handoff to a partner credit union that underwrites and closes the loan. That’s two complete underwriting passes by two organizations.

A broker like RenoFi earns its keep when your situation is unusual enough that one lender’s “no” shouldn’t end your search, when you don’t already have a renovation-lending relationship, or when your project hinges on the ARV mechanic and you want help building the case. A direct lender is usually faster when you already bank somewhere that does HELOCs, your current equity covers the project, or you want a HomeStyle Renovation, CHOICERenovation, or 203(k) first mortgage — none of which route through RenoFi at all.

Sources: renofi.com footer and How It Works; RenoFi FAQ.

Which RenoFi alternatives also use after-renovation value (ARV)?

Fannie Mae HomeStyle Renovation — the direct-lender ARV closest to RenoFi

HomeStyle Renovation is a conventional, conforming first mortgage that finances a home purchase or refinance plus the renovation cost in a single loan, underwritten against the as-completed appraised value. For ADU homeowners, it’s the most important alternative on this list.

Two recent updates made it materially better for ADU buyers:

- Lenders may now disburse up to 50% of total renovation costs at closing. Additional draws require periodic inspections, and the lender may not increase the loan amount to offset cost overruns — those fall to the borrower. (Fannie Mae Selling Guide B5-3.2-04.)

- Rental income from an existing ADU can count toward qualifying income on a one-unit principal residence (one ADU only), capped at 30% of total qualifying income, on purchase or limited cash-out refinance transactions, with property-management-experience and current-housing-payment conditions. (Selling Guide B3-3.8-01, via Announcement SEL-2025-08, in Desktop Underwriter 12.1 effective March 21, 2026.)

- The 2026 conforming loan limit is $832,750 for a single-family home and $1,249,125 in high-cost metros (FHFA), with up to 97% LTV on the as-completed value for owner-occupied purchases.

Sources: Fannie Mae HomeStyle Renovation; Selling Guide B3-3.8-01 (10/08/2025); FHFA 2026 conforming loan limits.

Freddie Mac CHOICERenovation — the Freddie equivalent

CHOICERenovation is Freddie Mac’s parallel product. It uses the same as-completed appraisal logic and the same conforming loan limits, and Freddie lists its transaction types as purchase and no-cash-out refinance. The choice between HomeStyle and CHOICERenovation usually comes down to which one your lender supports and which prices better the day you lock. Source: Freddie Mac CHOICERenovation.

FHA 203(k) Standard and Limited — the federally insured ARV option

FHA’s 203(k) program is the original ARV-based renovation loan. 203(k) Limited covers up to $75,000 in eligible rehabilitation and is quicker to close. 203(k) Standard handles larger projects, requires at least $5,000 in rehab costs, and uses a HUD consultant who monitors the work and ties draw releases to inspections; the contractor obtains permits before work starts. The 2026 FHA one-unit floor is $541,287, with a high-cost ceiling of $1,249,125 (HUD; effective for case numbers assigned on or after January 1, 2026). FHA financing accommodates credit scores as low as 580 with 3.5% down (some lenders add overlays at 620+). The tradeoff is FHA mortgage insurance in most cases. For owner-occupant garage, basement, and attached ADUs, 203(k) is often underused and can beat conventional ARV products on rate.

Sources: HUD 203(k); HUD 2026 loan limits (HUD No. 25-145).

Construction-to-Permanent loans — direct from your bank or credit union

A construction-to-permanent loan funds the build in draws (typically interest-only during construction, secured against the as-completed value) then converts to a permanent mortgage once the certificate of occupancy issues. Most banks and credit unions offer a version; smaller community banks and credit unions are often the best fit for ADU-specific construction-to-perm because they’re more flexible on the as-completed appraisal for unusual properties. Construction- phase rates typically run the conforming rate plus 0.5%–1.5%. This is the right path for a detached new-build ADU with a complex draw schedule, or when you’re buying a property and adding the ADU at once.

Which one is most likely to beat RenoFi for you

| If your situation looks like… | Direct-lender ARV path to compare first |

|---|---|

| Recently bought, low equity, want to keep a low first mortgage, straightforward project | RenoFi or a second-lien ARV renovation HELOC from a local CU (HomeStyle won’t fit — it replaces the first mortgage) |

| Buying a property and adding an ADU at purchase | Fannie Mae HomeStyle Renovation or FHA 203(k) |

| Refinancing anyway, or willing to refinance for the cash | HomeStyle, CHOICERenovation (purchase / no-cash-out), or cash-out refi |

| Detached new-build ADU with a significant draw schedule | Construction-to-permanent loan |

| FHA-eligible, owner-occupant, project between $5,000 and $75,000 | FHA 203(k) Limited |

| Live in Texas, NY, Hawaii, or Massachusetts | HomeStyle, CHOICERenovation, FHA 203(k), or construction-to-perm — any of these works |

Explore current renovation, HELOC, cash-out refi, and construction-loan rates from licensed mortgage lenders →

Compare Lender Rates →Affiliate disclosure: we may earn a commission if you complete a loan via this link. Rates depend on lender, credit, and property. Not a guarantee of approval or rate.

How does each option compare on real cost? A $300K ADU financed 8 ways

The 5-year financing cost matrix (illustrative)

| Path | Amount borrowed | Rate (illustrative, May 2026) | Monthly payment, post-build | Approx. 5-yr interest | The tradeoff |

|---|---|---|---|---|---|

| RenoFi HELOC (2nd lien, ARV) | $300,000 | ~8.0% variable | Interest-only ~$2,000/mo during draw, then P&I | ~$120,000 | Variable rate; broker-routed timeline; depends on ARV appraisal |

| RenoFi Fixed-Rate HELoan (2nd lien) | $300,000 | ~7.5%–8.5% fixed, 20-yr | ~$2,500/mo | ~$110,000 | Fixed rate higher than first-mortgage rates; broker timeline |

| Fannie Mae HomeStyle Renovation (new $800K 1st) | $800,000 | ~6.75% conforming, 30-yr | ~$5,190/mo | ~$265,000 on full $800K | You lose your 4.5% mortgage — the rate-preservation trap |

| Freddie Mac CHOICERenovation | $800,000 | ~6.75% conforming, 30-yr | ~$5,190/mo | ~$265,000 | Same rate-preservation tradeoff |

| FHA 203(k) Standard | $800,000 | ~6.50% FHA + MIP | ~$5,055/mo + MIP | ~$255,000 + MIP | Lower rate offset by mortgage insurance; same rate-preservation issue |

| Construction-to-Permanent | $800,000 | ~7.5% build, ~6.75% after | ~$5,000/mo then ~$5,190/mo | ~$280,000 | Rate-preservation tradeoff; complex draws |

| Cash-out Refinance | $800,000 | ~6.75%, 30-yr | ~$5,190/mo | ~$265,000 | Rate-preservation tradeoff; simplest mechanics |

| Traditional 80%-CLTV HELOC | Capped at $100,000 | ~7.21%–7.41% variable | ~$1,200/mo P&I | ~$30,000 on $100K | Doesn’t cover the project — only $100K available |

Read it this way: the first-mortgage paths (HomeStyle, CHOICERenovation, FHA 203(k), construction-to-perm, cash-out refi) look cheaper on the new $300K, but they all replace your 4.5% mortgage with a ~6.75% one. Keeping a 4.5% rate on $500,000 instead of refinancing to 6.75% saves roughly 2.25% × $500,000 = about $11,250 per year, or roughly $56,000 over five years. That saving frequently outweighs the higher second-lien rate on the $300K — which is why, in this specific scenario, RenoFi or a traditional HELOC (if it fit) often wins on total cost.

The break-even by existing mortgage rate (illustrative)

| Your existing 1st-mortgage rate | Refinance into a ~6.75% product? | Why |

|---|---|---|

| 3.25% | Almost never | Giving up 3.25% for 6.75% on $500K costs ~$17,500/yr — far more than the rate gap on the new $300K. Keep the mortgage; use a second lien. |

| 4.5% | Usually not | Giving up 4.5% costs ~$11,250/yr on $500K. A second-lien ARV path usually still wins. |

| 5.5% | It’s close | The lost-rate cost (~$6,250/yr) and the second-lien premium are similar. Run both. |

| 6.5%+ | Often yes | You’re giving up almost nothing. A single first-mortgage HomeStyle or cash-out refi is usually cleanest and cheapest. |

Illustrative break-even math on a $500,000 balance; your closing costs, term reset, and holding period change the exact crossover. This is a framework, not advice.

Free, no signup; built for exactly this rate-preservation question.

Sources: Curinos/Bankrate home-equity rate data, mid-to-late May 2026. HELOC ~7.21%–7.41% (Bankrate May 20, 2026: 7.41%; Curinos week of May 13–20: 7.21%); HELOAN ~7.36%–8.03% (Curinos: 7.36%; WSJ Buyside May 15: 8.03%). We present the range because surveys differ in methodology and as-of dates.

Will an alternative give me as much borrowing power as RenoFi?

RenoFi publishes these caps: its HELOC goes up to 95% of after-renovation value; its fixed-rate Home Equity Loan up to 90% of ARV; both max out at $750,000 (some older RenoFi comparison pages still show $500,000, so confirm your specific lender’s cap).

The direct-lender alternatives: HomeStyle Renovation allows up to 97% LTV on as-completed value inside the conforming limit; CHOICERenovation matches it; FHA 203(k) works inside the county FHA limit (2026 floor $541,287, ceiling $1,249,125); construction-to-perm is lender-set with jumbo options for higher-balance projects.

RenoFi’s strongest case is the equity-light, rate-rich recent buyer: low current equity, a 3%–4.5% mortgage worth preserving, a traditional HELOC that won’t reach. Outside that profile, the direct-lender ARV options usually offer better rates, faster timelines, and equal or greater borrowing power.

Will I lose my low first mortgage?

| Preserves your existing 1st mortgage (2nd lien) | Replaces your existing 1st mortgage (1st lien) |

|---|---|

| Traditional HELOC | Cash-out refinance |

| Fixed-rate Home Equity Loan (HELOAN) | HomeStyle Renovation |

| RenoFi HELOC | CHOICERenovation (purchase / no-cash-out) |

| RenoFi Fixed-Rate Renovation Loan | FHA 203(k) |

| Figure HELOC | Construction-to-permanent (most structures) |

| Hometap / Unlock / Point HEI (records a lien, but no new monthly debt) |

The math: a homeowner with a $500,000 mortgage at 3.25% who refinances into an $800,000 HomeStyle at 6.75% pays roughly $17,500 more per year in interest on the existing $500,000 balance alone — before the new $300,000 renovation portion. That’s why, with a sub-5% first mortgage, a second-lien path is frequently cheaper in total even though its headline rate is higher.

What if my equity is too low for a traditional HELOC? The no-monthly-payment options

How HEIs work, and what they really cost

An HEI is not a loan. The company invests cash in your home today for a percentage share of your home’s future value, settled when you sell, refinance, or buy them out — typically within a 10-year term (Hometap) or up to 30 years (Point). There’s no monthly payment because there’s no interest in the traditional sense; you owe a share of the home’s eventual value under the contract’s formula, which can grow quickly if your home appreciates. The qualifying logic differs: HEI companies look at your current equity (generally ≥25% required), your credit (Hometap states a minimum FICO of 575), and — most binding — your state.

Hometap, Unlock, and Point — current state coverage

| Provider | Investment range | State availability | Term | Notable |

|---|---|---|---|---|

| Hometap | Up to $600,000 | 16 states: AZ, CA, FL, IN, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, UT, VA. Min. ~25% equity. | 10 years | MA AG sued Feb 19, 2025; suit ongoing; MA no longer listed as served |

| Point | Up to $600,000 | By state/region — verify on Point’s official eligibility page | Up to 30 years | Advertises no income requirement; underwriting still applies |

| Unlock | $15,000–$500,000 | AZ, CA, FL, HI, ID, IN, KY, MI, MO, MT, NV, NH, NJ, NM, NC, OH, OR, PA, SC, TN, UT, VT, VA, WI, WY (25 states per Unlock.com) | 10 years | No age or income requirement per site; underwriting, property, and lien checks still apply |

When an HEI beats RenoFi: you can’t qualify for debt (DTI too high, irregular income, lower credit), or you can’t add a monthly payment but can plan to settle through a future sale or refinance. When it’s worse: you have the income to service a payment (a HELOC or RenoFi Loan is almost always cheaper over 5–10 years), your local market is appreciating fast (the settlement balloons), or you plan to stay indefinitely and can’t comfortably refinance or sell.

How fast can each option actually close?

| Path | Typical closing window | What delays it | Source basis |

|---|---|---|---|

| Direct HELOC (existing bank) | ~2–6 weeks | Appraisal backlog, title issues | Lender-published averages |

| Cash-out refinance | ~30–45 days | Appraisal, income docs | Lender-published averages |

| HomeStyle Renovation | ~45–60 days | As-completed appraisal, contractor docs, escrow setup | Fannie Mae process; lender averages |

| FHA 203(k) | ~60–90 days | HUD consultant, draw schedule, MIP setup | HUD process |

| Construction-to-perm | ~45–90 days + build | Draw schedule, inspections | Lender averages |

| RenoFi | Several weeks to several months | Two-layer underwriting, ARV appraisal, partner capacity | RenoFi testimonials (“long”); Bankrate review; BBB records |

| HEI (Hometap/Unlock/Point) | ~30–60 days | Property verification, title, lien checks | Provider sites |

The most common reason a homeowner switches from RenoFi to a direct-lender alternative mid-process is timeline pressure — a contractor’s bid is expiring or material prices are moving. If you’re inside 90 days of needing to start construction, a direct HELOC, HELOAN, or construction-to-perm loan from your existing bank usually beats a broker-routed product on speed.

When is RenoFi genuinely the right call?

Profile 1 — equity-light, rate-rich recent buyer. Bought in 2021–2022, refinanced into a 3.0%–4.5% mortgage, under 20% equity today, wants a $250,000–$400,000 ADU. A traditional HELOC won’t reach. HomeStyle could fund it but would replace the low rate, costing tens of thousands over the loan’s life. RenoFi — or an equivalent direct credit-union second-lien renovation HELOC — is genuinely the cheapest total-cost path.

Profile 2 — needs a revolving line on ARV. Most direct ARV alternatives are amortizing loans, not revolving lines. If you want HELOC flexibility (draw as needed, pay interest only on what you draw) but need ARV-based borrowing power, RenoFi’s HELOC is one of few mainstream products that delivers both. Some local credit unions offer comparable products — ask before assuming RenoFi is your only option.

Profile 3 — local lender market has no ARV alternative. In some areas the local CU and community-bank market simply doesn’t carry an ARV second-lien renovation product. RenoFi’s national partner network fills that gap.

When RenoFi isn’t the call: you have enough current equity for a traditional HELOC (faster, often cheaper); you’re buying a property and adding an ADU at purchase (HomeStyle or 203(k) is structurally better); you’re doing a major detached new-build with a complex draw schedule (construction-to-perm is built for it); or you live in Texas, NY, Hawaii, or Massachusetts.

Can I use a RenoFi alternative for my ADU type?

| ADU type | First lane to check | Backup lane | The financing question that decides it |

|---|---|---|---|

| Detached stick-built ADU | Construction-to-perm or RenoFi-style ARV | HomeStyle / HELOC | Does the lender support detached ADU construction draws? |

| Garage conversion | HELOC or renovation mortgage | FHA 203(k) | Is the scope eligible and permitted? |

| Basement ADU | HELOC or renovation loan | FHA 203(k) | Does it meet code and habitability standards? |

| Prefab / modular ADU (permanent foundation) | HELOC or construction loan | HomeStyle | Is it real property after installation? |

| Manufactured (HUD-code) ADU | Fannie/FHA manufactured-home rules | Construction loan | Renovation costs on manufactured homes capped at 50% of as-completed value (Fannie Mae, late-2025 update) |

| JADU (junior ADU, ≤500 sq ft within the home) | HELOC or small renovation loan | Cash reserve | Is the budget small enough for simpler financing? |

| Movable / tiny home on wheels | Specialty / chattel financing | Cash | Is it legally an ADU or personal property? |

A JADU (junior accessory dwelling unit) is a unit of up to 500 square feet created within the walls of an existing single-family home. Chattel financing is a loan secured by movable personal property rather than real estate — relevant when a unit isn’t permanently affixed. Always confirm classification with the lender before ordering a prefab or manufactured unit.

What can stop your ADU even after financing is approved?

HOA covenants and CC&Rs

California’s AB 670 prohibits HOAs from outright banning ADUs on single-family lots, but architectural review committees, height limits, and exterior-material rules can still effectively block a project. Verify your HOA’s stance before financing.

Setbacks

California state ADU law generally prevents cities from requiring more than a 4-foot side and rear setback for qualifying detached ADUs; conversions and local exceptions can differ. Your lot’s buildable footprint is set by these rules, not by your financing.

Owner-occupancy and 2025–2026 rule changes

AB 1033 went into effect in 2024 and allows cities to opt in to local rules permitting ADUs to be sold separately as condominiums; San José adopted the rules first. AB 2533, effective January 1, 2025, expanded legalization protections for unpermitted ADUs and JADUs — extending the cutoff date to January 1, 2020. For 2026, AB 1154 loosens JADU owner-occupancy so the mandate applies only to JADUs that share sanitation facilities with the main house. If you plan to rent the ADU and use the income to qualify, your loan path determines what’s allowed — and recall that Fannie Mae only counts rental income from an existing ADU, not a proposed one.

Utilities and impact fees

Separate meters, sewer connections, and electrical service can add cost late in the design process, and city impact and school fees vary widely by jurisdiction. Make sure your contractor’s bid and your lender’s as-completed appraisal both account for them, or you’ll discover a financing gap mid-build.

Free, no signup required.

How do you compare lender offers without getting misled?

12 questions to ask every lender or broker

- Are you the lender, the broker, the marketplace, or an equity investor?

- Is this a loan, a line of credit, a renovation mortgage, a construction loan, or an equity investment?

- Does underwriting use current value or as-completed value?

- Does this replace my first mortgage, or sit behind it as a second lien?

- What are all fees and closing costs — origination, appraisal, title, recording, and any monthly renovation fee during construction?

- Are there draw, inspection, or contractor-licensing requirements?

- What happens if the as-completed appraisal comes in lower than expected?

- Is my specific ADU type (detached, attached, garage conversion, basement, prefab, JADU) eligible?

- Is this product currently available in my state?

- Are there prepayment penalties? Can I refinance out without cost?

- What happens if I sell, refinance, or can’t complete the project?

- Is the rate and payment you’re quoting binding, or contingent on appraisal and final underwriting?

Red flags

- “Approval without underwriting” or “everyone qualifies.”

- “Lowest rates” without APR, points, and fees.

- “Your future ADU rent will cover it” before the lender confirms rental-income treatment.

- “We don’t need to see permits.”

- “Same product available in every state.”

- Reviews or ratings with no verifiable source.

What documents should you gather before applying?

Financial

- Current mortgage statement

- Homeowners insurance declarations

- Two years of tax returns (+ W-2s/1099s/P&Ls if self-employed)

- Recent paystubs

- Two months of bank statements

- Credit authorization

- List of all existing debts

ADU project

- Plans or concept drawings

- Licensed contractor’s bid with scope of work

- Detailed budget with at least 10% contingency

- Permit status

- Site plan showing setbacks, lot coverage, footprint

- Timeline and draw schedule

Property

- Estimate of current value or recent appraisal

- Property tax bill

- HOA documents and CC&Rs if applicable

- City zoning verification

- Septic/well documentation if applicable

- Intended use (rental, owner-occupied, etc.)

Use-case note (for lenders that consider ADU rental income): Intended use; for rental, a long-term lease estimate based on local rent comps (not short-term-rental projections); a property-management plan if you’ll rent.

Every document checklist, every fee category, and the questions to ask before you sign — updated quarterly.

Methodology — how we built this guide

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For this guide we reviewed primary sources: RenoFi’s corporate disclosures and NMLS filings, the Fannie Mae Selling Guide and Announcement SEL-2025-08, Freddie Mac’s CHOICERenovation page, HUD’s 203(k) documentation and 2026 FHA loan-limit announcement, FHFA’s 2026 conforming limits, Curinos/Bankrate home-equity rate data, the Texas Constitution Section 50(a)(6), the CFPB’s home equity contracts research, the Massachusetts Attorney General’s press release, and current state-availability pages published by Hometap, Unlock, and Point. We cross-checked product mechanics against Bankrate, LendEDU, FinanceBuzz, U.S. News, and HousingWire. We do not rank lenders by compensation; comparison tables are sorted by product structure and neutral fit criteria, and every affiliate relationship is disclosed.

| Claim type | Source standard |

|---|---|

| RenoFi product mechanics, fees, terms | renofi.com official pages; NMLS Consumer Access |

| HomeStyle / rental-income rules | Fannie Mae Selling Guide and Announcements |

| CHOICERenovation rules | Freddie Mac Seller/Servicer Guide and product page |

| FHA 203(k) rules and limits | HUD 203(k) documentation; HUD 2026 loan-limit announcement |

| Conforming loan limits | FHFA annual publication |

| Current HELOC / HELOAN rates | Curinos / Bankrate, dated, with the survey noted |

| State legal restrictions | State constitutions and statutes (primary); press only as cross-check |

| HEI provider state coverage, ranges, terms | Each provider’s own site (primary) |

| HEI consumer risks | CFPB research; Massachusetts AG press release; court reporting |

| California ADU statutes | Legislative bill text and law-firm legal alerts |

| Borrower experience | Bankrate reviews, BBB records, public forums — context only, never as proof of loan terms |

How we update this page: we re-verify the matrix monthly; refresh rate ranges against Curinos/Bankrate (weekly during Fed policy changes); verify RenoFi, Hometap, Unlock, Point, and Figure state availability monthly via direct site check; and review immediately on any Fannie Mae or HUD rule update.

Check before you apply (availability changes — verify these directly)

Because state availability and product caps move, confirm these on the provider’s own site before you apply:

| Provider / path | What to verify | Where to check |

|---|---|---|

| RenoFi | Whether the ARV Renovation Loan is available in your state (esp. TX, NY, HI, MA) | renofi.com (and your state’s licensing notice) |

| Hometap | That your state is on the current 16-state list; current FICO/equity terms | hometap.com |

| Unlock | That your state is on the current list; current $15K–$500K range | unlock.com/about |

| Point | State/region eligibility; current cap and term | point.com eligibility page |

| Figure HELOC | Current-equity HELOC availability (not for NY) | figure.com |

| HomeStyle / CHOICERenovation / FHA 203(k) | Lender overlays, current rate, and your county loan limit | Your lender; FHFA and HUD limit lookups |

What we verified (and what we couldn’t)

Verified for this page — Last verified: May 21, 2026:

- RenoFi’s broker status and ARV mechanic — renofi.com “How It Works” and footer; Bankrate RenoFi review Feb 27, 2026; NMLS #1802847 and #2412747.

- RenoFi’s New York DFS non-authorization — direct quote from renofi.com footer.

- RenoFi’s Texas exclusion for the ARV product — RenoFi’s site (personal-loan-only in Texas) plus Texas Constitution Section 50(a)(6).

- Hawaii and Massachusetts exclusions — Bankrate RenoFi review Feb 27, 2026 (not independently confirmed on RenoFi’s own corporate pages).

- 2026 FHA loan limits — HUD announcement HUD No. 25-145: one-unit floor $541,287, ceiling $1,249,125, effective for case numbers on/after Jan 1, 2026.

- 2026 FHFA conforming limits — $832,750 single-family / $1,249,125 high-cost.

- Fannie Mae existing-ADU rental income rule — Selling Guide B3-3.8-01 (10/08/2025) via Announcement SEL-2025-08: existing ADU, one-unit principal residence, one ADU, purchase or limited cash-out refinance, capped at 30% of total qualifying income, with property-management and housing-payment conditions; implemented in DU 12.1 effective March 21, 2026.

- HomeStyle 50%-at-closing disbursement — Selling Guide B5-3.2-04; additional draws require inspections; loan amount can’t increase to offset overruns.

- CHOICERenovation transaction types — Freddie Mac: purchase and no-cash-out refinance.

- FHA 203(k) parameters — HUD: Limited up to $75,000; Standard requires at least $5,000 in rehab; contractor permits before start; draws tied to inspections.

- HELOC/HELOAN May 2026 rates — Curinos/Bankrate; we present a range (HELOC ~7.21%–7.41%; HELOAN ~7.36%–8.03%) because surveys differ in method and as-of date.

- Hometap — 16 states, up to $600,000, 10-year term, ~25% equity, FICO 575/585 (hometap.com).

- Unlock — $15,000–$500,000, 25-state list (unlock.com).

- Point — up to $600,000, up to 30-year term, no income requirement advertised (point.com).

- Massachusetts AG v. Hometap — filed Feb 19–20, 2025; the suit was allowed to proceed in 2025; Massachusetts is no longer listed among Hometap’s served states.

- CFPB home equity contract risks — CFPB Issue Spotlight.

- California ADU statutes — AB 670, AB 1033, AB 2533, AB 1154 (legislative text and law-firm alerts).

What we could not fully reconcile (flagged in line):

- The precise list of states RenoFi’s ARV product serves. Bankrate (Feb 27, 2026) says HI, NY, MA; RenoFi’s marketing references “every state except Texas.” Most likely RenoFi’s broker footprint covers most states while partner-credit-union availability gates which products are offered where. Verify with RenoFi for your state before applying.

- Specific RenoFi APRs. RenoFi does not publish rate sheets; we use ranges from its prime-plus-margin sample disclosures.

- A single national HELOC rate. Curinos/Bankrate surveys reported 7.21%–7.41% the same week; we present the range.

Frequently asked questions

- What is the best alternative to RenoFi for an ADU?

- It depends on your constraint. For more borrowing power than current equity allows, compare Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA 203(k), or a construction-to-permanent loan — all of which use as-completed value. With enough current equity, compare a traditional HELOC or fixed-rate HELOAN. If you can't add a monthly payment, compare an HEI from Hometap, Unlock, or Point, weighing their costs and risks. There's no single best alternative; the right one depends on your equity, your first-mortgage rate, your state, and your ADU type.

- Is RenoFi available in Texas?

- RenoFi's flagship after-renovation-value Renovation Loan is not available in Texas, because Texas Constitution Section 50(a)(6) caps home-equity combined loan-to-value at 80% and adds restrictions that conflict with RenoFi's ARV structure. RenoFi's site notes a personal-loan product is available in Texas — a different product. For Texas ADU homeowners, a Fannie Mae HomeStyle Renovation loan or a construction-to-permanent loan from a Texas-licensed lender is usually the better path. (Verified May 21, 2026.)

- Is RenoFi available in New York?

- No. RenoFi's footer states the site is “not authorized by the New York State Department of Financial Services” and that no loan applications for New York properties can be facilitated through it. New York homeowners should look at HomeStyle Renovation, CHOICERenovation, FHA 203(k), or a direct New York HELOC or HELOAN. (Verified May 21, 2026.)

- Is RenoFi available in Hawaii and Massachusetts?

- Per Bankrate's February 27, 2026 RenoFi review, RenoFi is not available in Hawaii or Massachusetts. We have not seen RenoFi confirm those exclusions on its own corporate pages, so verify directly if you live there.

- Is RenoFi the same as a HELOC?

- No. RenoFi offers a HELOC variant (a revolving line you can draw on for up to 10 years) and a fixed-rate Home Equity Loan variant, both underwritten on after-renovation value rather than current value. A traditional HELOC from your bank uses your current home value. The difference matters most when your current equity is low.

- Who actually funds a RenoFi loan?

- A partner credit union. RenoFi states it “is not a lender, rather we’ve partnered with lenders that leverage RenoFi’s technology.” RenoFi qualifies you, prepares your file, and routes you to a credit union, which holds the loan.

- What's the minimum credit score for a RenoFi alternative?

- It varies. FHA 203(k) allows scores as low as 580 with 3.5% down (lenders may require 620+). HomeStyle typically wants 620+. Conventional HELOC/HELOAN usually want 680+ for best pricing. Hometap states a minimum FICO of 575 (and notes 585+ may qualify). RenoFi partner credit unions can go as low as 620 per Bankrate, with stricter requirements on larger loans.

- Can I use a HomeStyle Renovation loan for a detached ADU?

- Yes. Fannie Mae's HomeStyle Renovation permits accessory units, including detached ADUs, provided all improvements comply with local and state codes. Recent updates expanded ADU flexibility and allow rental income from an existing ADU to count toward qualifying income under specific conditions.

- Can rental income from my future ADU help me qualify?

- For Fannie Mae, the rule applies to an existing ADU, not a proposed one: rental income from an existing ADU on a one-unit principal residence (one ADU only) can count on purchase or limited cash-out refinance transactions, capped at 30% of total qualifying income, with property-management and current-housing-payment conditions (Selling Guide B3-3.8-01, via SEL-2025-08, in DU 12.1 from March 21, 2026). FHA has separate rules that may allow a percentage of expected ADU rent in some scenarios. HELOCs and HELOANs generally don't count projected ADU rent. Confirm treatment with your specific lender before assuming it works.

- What's the cheapest RenoFi alternative on a $300K ADU?

- In our worked example, it depends on your existing mortgage rate. If your first mortgage is 6%+, a HomeStyle, CHOICERenovation, or cash-out refinance into a ~6.75% loan is usually cheapest in total. If your first mortgage is below 5%, preserving it usually wins — so a second-lien path (a traditional HELOC if equity allows, otherwise RenoFi or a similar ARV second lien) is cheapest. Run your specific rates; the rate-preservation question is the biggest variable. (Illustrative; not a guarantee.)

- What's the fastest RenoFi alternative if I'm in a hurry?

- A traditional HELOC at your existing bank or credit union, if you have enough current equity — typically 2–6 weeks, faster than RenoFi's broker-routed timeline, HomeStyle, or FHA 203(k), and roughly comparable to an HEI.

- What if I'm an owner-builder?

- Owner-builder projects are harder to finance because most lenders want a licensed general contractor, bids, and inspection-driven draws. Some FHA 203(k) Standard loans permit owner-builder structures with HUD-consultant oversight, and some local credit unions work with experienced owner-builders. RenoFi typically requires a licensed contractor and bid. Verify eligibility with each lender first.

- What if my ADU is prefab or modular?

- Modular ADUs permanently installed on a foundation are usually treated as site-built for financing — HomeStyle, CHOICERenovation, construction-to-perm, and most HELOCs work. Manufactured (HUD-code) ADUs follow Fannie Mae and FHA manufactured-home rules (renovation costs on manufactured homes are now capped at 50% of as-completed value per a late-2025 Fannie Mae update). Movable or container units not permanently affixed may be personal property and require chattel financing. Confirm classification with the lender before ordering.

- Should I use a personal loan for an ADU?

- Only for a small gap. Personal loans are unsecured, carry much higher rates than home-equity products, and rarely exceed $100,000 — far too small and expensive for a typical $200K–$400K build. They make sense only for soft costs (design, permits) or early gap funding before your main loan closes.

- What should I do before applying to any lender?

- Three steps: verify your lot can support the ADU (run the free Property Eligibility Check below before paying for plans); gather the documents above, especially your contractor bid and permit status; and compare two or three financing paths with real pre-qualification numbers before choosing.

Next steps — your decision in 60 seconds

- Confirm the project is feasible. Run our Property Eligibility Check for your lot’s ADU fit, size cap, city fee math, and any state-law overrides. Free, 60 seconds, no signup.

- Match your situation to a lane. Use the comparison matrix and the break-even-by-rate table above: identify whether your constraint is equity, first-mortgage preservation, monthly-payment capacity, state availability, or project type. That single answer points to your path.

- Get current rates from licensed mortgage lenders. Once you know your lane, compare current renovation, HELOC, cash-out refinance, and construction-loan rates from licensed mortgage lenders to pick the actual product.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Free. No signup required. Results in 60 seconds.

Check My Property →Sources cited on this page

- RenoFi. “How It Works.” renofi.com/how-it-works/. Verified May 21, 2026.

- RenoFi. Footer disclosure and NY DFS notice; NMLS #1802847 and #2412747. renofi.com. Verified May 21, 2026.

- RenoFi. “FAQ.” renofi.com/faq/.

- Bankrate. “RenoFi: 2026 Home Equity Review.” Published Feb 27, 2026.

- Bankrate. “Current HELOC Rates In May 2026” (7.41% as of May 20, 2026).

- Yahoo Finance / Curinos. HELOC and home equity loan rates, week of May 13–20, 2026 (HELOC 7.21%, HELOAN 7.36%).

- WSJ Buyside. Home equity loan rates (8.03% average as of May 15, 2026).

- Fannie Mae. Selling Guide B3-3.8-01, Rental Income (10/08/2025). selling-guide.fanniemae.com.

- Fannie Mae. Selling Guide B5-3.2-04, HomeStyle Renovation Mortgages: Costs and Escrow Accounts.

- Fannie Mae. Announcement SEL-2025-08 (Oct 8, 2025); DU 12.1 Release Notes (effective March 21, 2026).

- Fannie Mae. HomeStyle Renovation product page.

- Freddie Mac. CHOICERenovation product page (purchase / no-cash-out refinance).

- HUD. “203(k) Rehabilitation Mortgage Insurance Program.” hud.gov. (Limited up to $75,000; Standard minimum $5,000.)

- HUD. “HUD’s FHA Announces 2026 Loan Limits” (HUD No. 25-145): one-unit floor $541,287, ceiling $1,249,125.

- FHFA. 2026 Conforming Loan Limits ($832,750 / $1,249,125 high-cost).

- Hometap. Hometap.com (16 states; up to $600,000; 10-year term; ~25% equity) and credit guidance blog (FICO 575/585).

- Unlock. Unlock.com cost page ($15,000–$500,000) and About page (state list).

- Point. Point.com (up to $600,000; up to 30-year term; no income requirement advertised).

- Massachusetts Office of the Attorney General. Press release, Feb 20, 2025 (suit against Hometap). HousingWire reporting on the suit proceeding (2025).

- CFPB. “Issue Spotlight: Home Equity Contracts — Market Overview.”

- Texas Constitution, Article XVI, Section 50(a)(6).

- BBK Law (AB 2533); Shute Mihaly & Weinberger (AB 1154); CapRadio (AB 1033), for California ADU statutes.

- LendEDU, FinanceBuzz, U.S. News — secondary cross-checks on RenoFi and HEI reviews.

Related ADU financing guides

- Best ADU financing options for 2026

- ADU loan vs HELOC — real rates, real decision

- ADU loan requirements: credit, equity & permits

- How to qualify for ADU financing

- ADU equity calculator — run your own numbers

- Bridge financing for an ADU

- Cheaper ADU financing paths most homeowners qualify for

- RenoFi vs HELOC for ADUs

- RenoFi vs construction loan: 9 ADU decision rules

- RenoFi vs Figure HELOC: 2026 ADU decision guide

- Our methodology

- Affiliate disclosure