LendingTree ADU Financing Review: When It Fits — and When It Doesn’t

By The Dwelling Index Editorial Team · · Last verified: May 25, 2026

Bottom line up front: This LendingTree ADU financing review is for homeowners who already have an accessory dwelling unit (ADU) in mind and are deciding whether to hand LendingTree their information to shop for a loan. Here’s the honest answer. LendingTree is a loan marketplace and licensed mortgage broker — not a lender, and it has no product called an “ADU loan.” It takes one form and matches you with up to five lenders from a network of 300-plus whose products can be used to build an ADU. LendingTree is most useful when you already know your loan lane and want multiple offers fast; it’s a poor fit if you need ADU-specific structuring, have little current equity, or are sensitive to heavy outreach after you submit.

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. We earn nothing from LendingTree — every LendingTree mention on this page is editorial, not sponsored.

LendingTree for an ADU, at a glance

| The verdict | Use LendingTree when… | Pause or skip when… |

|---|---|---|

| Good comparison tool, not an ADU specialist | You know your loan lane and want several offers fast | You need a lender to structure the whole project |

| Marketplace, not a lender | You're comfortable comparing offers side by side | You want one direct lender and no marketplace outreach |

| Best for equity-based paths (HELOC, home equity, cash-out) | Your project can be funded from current equity | You need future-value lending or staged construction draws |

| Data sharing is the business model | You can manage calls, texts, and emails | You're highly sensitive to sales outreach |

| Free to you; no hard pull at the initial match | You want to shop without an upfront credit hit | You're not ready to compare full loan terms yet |

Source basis: LendingTree Terms of Use and LendingTree homepage; soft-inquiry mechanic per U.S. News mortgage review. Verified May 2026.

Free property check

See what you can build → Get your free ADU report

Before you compare any loan, start with the property and the project. Knowing your buildable square footage and rough cost tells you which financing lane to test first — and keeps you from sharing your information before you’re ready. Free, takes about 60 seconds.

Check my property for free →Is LendingTree actually an ADU lender?

LendingTree is not a lender, and it does not make ADU loans. It is an online marketplace and licensed mortgage broker that collects your information, may run a soft credit check, and matches you with lenders whose products can be used to build an ADU. The lenders — not LendingTree — approve the loan, set the rate, and fund the money. LendingTree’s own Terms of Use state plainly that it is not a lender or creditor and does not make credit decisions.

This distinction is the single most important thing to understand before you start, because it reframes the whole question. People type “LendingTree ADU loan” expecting a product. There isn’t one. What LendingTree (NMLS #1136, headquartered in Charlotte, North Carolina, operating since 1996) actually offers is speed of comparison — one form instead of five, and up to five competing offers in return.

What LendingTree does

- ✓Collects your details (ZIP, credit band, home value, mortgage balance, loan type).

- ✓May run a soft credit inquiry at matching — does not affect your credit score.

- ✓Matches you with up to five lenders from a network of 300-plus.

- ✓Lets you compare conditional offers side by side at no cost.

What LendingTree does not do

- ✕Does not approve, fund, or service your loan.

- ✕Does not guarantee a match or that any lender will make an offer.

- ✕Does not guarantee the matched lender understands ADU construction or draws.

- ✕Does not replace lender underwriting, the appraisal, or your Loan Estimate comparison.

- ✕Does not answer your local zoning, setback, or permit questions.

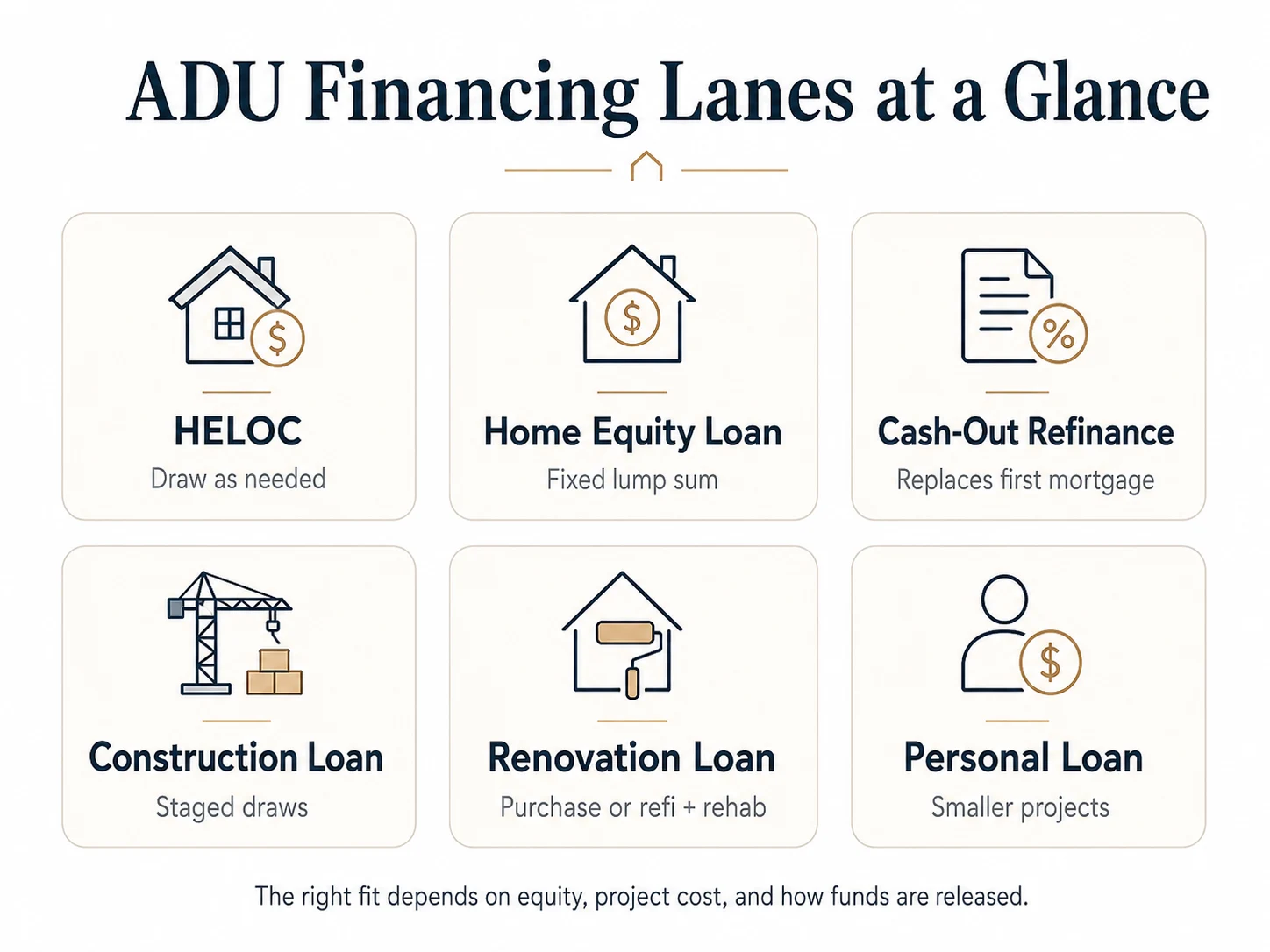

Which LendingTree loan types can actually fund an ADU?

There is no single “best” loan for an ADU. LendingTree can help you compare several product categories, and each one solves a different problem depending on your equity, your existing mortgage rate, your project cost, and whether you need money released in stages. The right question isn’t “Does LendingTree finance ADUs?” It’s “Which product am I asking lenders to quote — and does that product fit my ADU?”

Home equity line of credit (HELOC) for an ADU

A HELOC is a revolving line of credit secured by your home — you draw against it as you need cash during a set draw period. That structure can suit an ADU build where you pay contractors in stages. The catch: the rate is typically variable, so your payment can rise; your home is collateral; and your borrowing power is capped by your current equity, not the home’s future value after the ADU is built. Verify ADU eligibility and lien position with any matched lender.

Home equity loan for an ADU

A home equity loan is a fixed lump sum at a fixed rate — a “second mortgage.” It can fit a fixed ADU budget better than a revolving line because you know the rate and payment up front. The lump-sum structure is also its weakness — if your ADU runs over budget (and ADUs often do), a second loan or savings must bridge the gap. Confirm ADU eligibility, closing costs, and whether the lump sum covers the full scope plus a contingency.

Cash-out refinance for an ADU

A cash-out refinance replaces your existing mortgage with a larger one and hands you the difference in cash. It can deliver a large sum at first-mortgage pricing. But it replaces your current loan — a poor trade if you’re sitting on a low pandemic-era rate. For the millions of homeowners who locked low rates in 2020–2021, “I don’t want to lose my rate” is the single biggest reason to look at a HELOC or home equity loan instead. Run the math both ways before deciding.

Construction loan or construction-to-permanent loan

A construction loan funds the build in stages tied to inspection milestones (“draws”), then either comes due or converts to a permanent mortgage. This is the lane built for ground-up ADUs that need staged disbursement. It also carries the most paperwork: detailed plans, contractor approval, inspections at every draw, and often a reserve. LendingTree can surface construction-loan offers, but whether a matched lender actually runs ADU construction draws is a question you need to ask each one directly.

Renovation mortgages: Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, FHA 203(k)

These are purchase-or-refinance loans that bundle renovation funds based on the home’s as-completed value — which is what makes them powerful for owners short on current equity. Fannie Mae confirms its loan products can be used to “renovate an existing ADU or add an ADU to a borrower’s existing home.” On the FHA side, HUD’s 203(k) rolls purchase/refinance and rehabilitation into one loan; the Limited 203(k) caps rehab at $75,000 for case numbers on or after November 4, 2024 (Mortgagee Letter 2024-13). Full 203(k) carries no cap but requires a HUD consultant for complex projects. Match availability and a willing lender matter more than breadth here.

Personal or home improvement loan

An unsecured personal loan is fast and doesn’t put your home on the line, but it’s usually too small and too expensive to fund a full ADU. Treat a personal loan as gap funding or a tool for a very small conversion — not the default path for a six-figure build.

The ADU Financing Marketplace Fit Matrix

The Dwelling Index is reader-supported and may earn a commission when you use our links to explore financing options. We earn nothing from LendingTree; the table below is editorial. We never sort lenders by compensation — the order reflects neutral criteria (equity required and project fit). Read our full disclosure.

| ADU situation | Lane to test | Why it may fit | Why it may fail | Verify before you commit |

|---|---|---|---|---|

| Strong current equity, want staged draws | HELOC | Draw flexibility matches phased construction; widely used for improvements | Variable rate; home is collateral; capped by current equity | CLTV cap, draw period length, rate margin, ADU eligibility, lien position |

| Fixed ADU budget, enough equity | Home equity loan | Fixed rate and payment match a one-time build cost | Cost overruns create a second funding gap; closing takes weeks | ADU use allowed, closing costs, appraisal basis, contingency buffer |

| Want to keep a low first mortgage | HELOC or home equity loan (before cash-out refi) | Second lien leaves your low first mortgage untouched | Higher second-lien pricing; two payments; equity-limited | Whether keeping the first mortgage beats the cash-out math |

| Low current equity, ADU adds value | Renovation mortgage (HomeStyle / CHOICERenovation / 203(k)) | Underwrites on as-completed value, not today's equity | Match not guaranteed; lender must understand ADU scope and draws | As-completed appraisal, contractor approval, draw schedule, permit docs |

| Buying or refinancing and adding an ADU | HomeStyle, 203(k), construction-to-perm | Bundles purchase/refi with renovation funds in one loan | More paperwork; contractor approval; product-specific limits | ADU scope eligibility, occupancy rules, local permits, lender overlays |

| Small garage conversion / limited scope | FHA Limited 203(k) or personal loan | Limited 203(k) funds up to $75,000 in rehab (post 11/4/2024) | Many full ADUs exceed these caps; personal loans run small and pricey | Total budget vs. cap, structural work, contractor bids |

| Rental / investor ADU | Mortgage with ADU rental income, or investor financing | Some agency programs now count ADU rental income to qualify | Investor underwriting differs; rules are specific | Whether ADU rent counts, lease/appraisal docs, occupancy, property type |

Sources: LendingTree HELOC, HUD 203(k) ($75,000 Limited cap effective 11/4/2024, Mortgagee Letter 2024-13); Fannie Mae ADU page; Freddie Mac ADU guidance. Verified May 2026.

Not sure which lane fits?

Use the free ADU Financing Fit Finder → See which lane to test before you submit

Answer a few quick questions — your state, ADU type, rough budget, whether you have equity, and your tolerance for lender calls — and get a real starting point. Nothing is shared with a lender until you decide to move.

Get my free ADU report →The 2025 Fannie Mae ADU rental-income change that matters in 2026

As of the October 8, 2025 Selling Guide update, Fannie Mae allows rental income from an existing accessory dwelling unit on a one-unit principal residence to be used toward qualifying, on purchase and limited cash-out refinance transactions. Per Fannie Mae’s announcement (SEL-2025-08) and Selling Guide section B3-3.8-01: the income may come from only one ADU even if the property has more; the rental income used can’t exceed 30% of the borrower’s total qualifying income; and a market-rent appraisal supports it (Form 1007 for one-unit properties). For loans through Fannie Mae’s automated underwriting, eligibility lands in Desktop Underwriter version 12.1 in Q1 2026; manual underwriting could use it from October 8, 2025.

Two cautions so you don’t over-read this. First, the rule is written around an ADU that already exists — it is not a blanket promise that rent from an ADU you’re about to build will count toward a construction loan. Second, lender adoption varies. Ask any matched lender plainly: “Will you count rental income from the ADU on this property toward my qualifying income, and under which program?” Freddie Mac has separately allowed ADU rental income in certain cases for longer — don’t assume the answer is yes without confirming it.

Sources: Fannie Mae SEL-2025-08 (Oct. 8, 2025); Selling Guide B3-3.8-01; Fannie Mae ADU page; Freddie Mac ADU guidance. Verified May 2026.

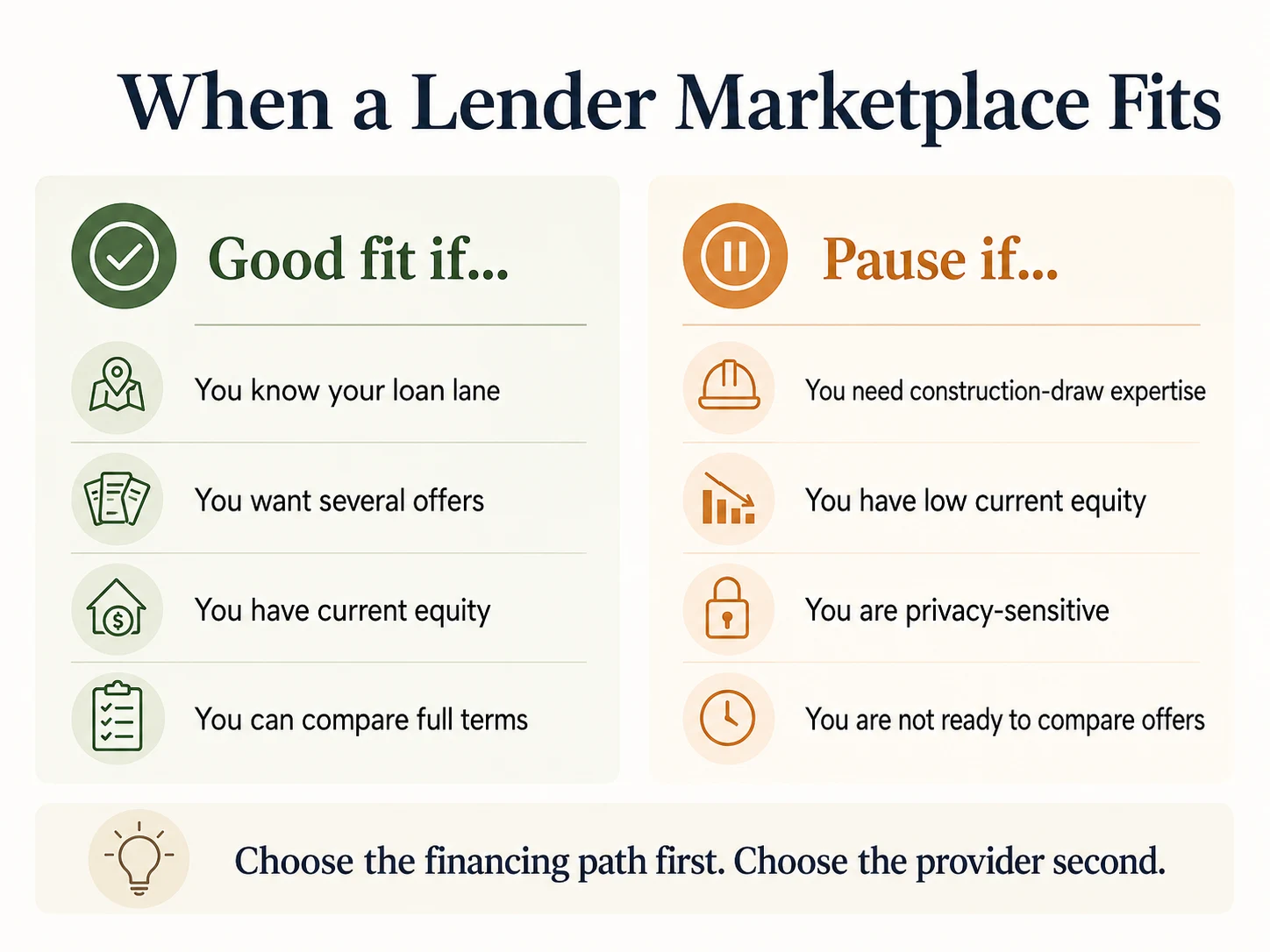

When is LendingTree a good fit for ADU financing?

LendingTree is most useful when your ADU financing problem is comparison, not diagnosis. If you already know you want to compare HELOC offers or home equity loans, a marketplace can save real time. If you don’t yet know which product fits, a marketplace just speeds you toward the wrong form.

You have enough current equity

Equity-based products — HELOC, home equity loan, cash-out refinance — are the simplest ADU financing paths, and they’re exactly what a marketplace is good at comparing. If you’ve owned your home for years and have substantial equity, getting several lenders to quote a second lien from one form is a legitimate time-saver.

You want multiple lenders to compete

This is LendingTree’s core pitch, and it’s not empty. The company states it works with a network of 300-plus lenders and matches each borrower with up to five. For a borrower who would otherwise call three banks one at a time, the one-form-many-offers model has real value — if you’re prepared for the follow-up contact.

You’re prepared to compare offers carefully

The Consumer Financial Protection Bureau (CFPB) advises borrowers to compare official Loan Estimates from multiple lenders and weigh loan costs, the lender’s reliability, and closing timing — not just the headline rate. A marketplace gets you the offers; the CFPB’s framework is how you actually pick.

You know the ADU-specific questions to ask

This is where most reviews stop short. Getting matched is easy; getting matched with a lender who understands ADUs is the real game. Before you accept any offer, ask:

- 1.Is ADU construction an eligible use of these funds?

- 2.Is the loan based on current home value or after-improved (as-completed) value?

- 3.Will you require approved plans or permits before closing?

- 4.How are funds disbursed — lump sum or staged draws?

- 5.Can the loan cover prefab deposits and milestone payments?

- 6.Is a contingency reserve required, and how much?

- 7.Can rental income from the ADU help me qualify, and under which program?

- 8.What happens if the city delays permit approval?

- 9.Are utility hookups, impact fees, design fees, and site work eligible costs?

- 10.What are all the closing costs, points, fees, and any prepayment penalty?

- 11.When does the soft inquiry become a hard inquiry?

- 12.Who services the loan after closing?

Know your numbers first

See what’s possible at your address → Get your free ADU report

Walk into any lender conversation knowing your buildable size and rough cost. That single step turns vague offers into apples-to-apples comparisons — and it’s free.

Check my property →When is LendingTree a bad fit for ADU financing?

LendingTree can be the wrong first step if you need ADU-specific structuring, have little current equity, depend on future value, dislike sales outreach, or simply aren’t ready to compare full loan terms. In those cases, identify the financing path first and choose the provider second.

You have low current equity

If your equity is thin, the equity-based products LendingTree shines at comparing — HELOC, home equity loan — may not work at all. The better starting point is a renovation or as-completed-value product, where availability and a willing lender matter more than marketplace breadth. Don’t assume the finished ADU’s value will automatically support the loan; that depends on an as-completed appraisal the lender controls.

You need construction draws or prefab payment timing

Ground-up and modular ADUs often need deposits, milestone payments, inspections, and retainage that a standard loan disbursement doesn’t match. A marketplace prequalification won’t answer disbursement questions — those require a lender who runs construction draws. If your prefab manufacturer needs a deposit before delivery, that timing has to line up with how the loan releases money, and that’s a conversation, not a form.

You’re sensitive to calls, texts, and partner outreach

If the thought of fielding offers from companies you didn’t choose makes you wince, a marketplace model is structurally a poor fit. A direct lender or local credit union — one relationship, one conversation — will feel better. See the downsides section below for the full picture.

You’d mistake a conditional offer for an approval

LendingTree’s terms make clear that the qualification form is a request to be matched, not a credit application, and that conditional offers can change or require verification. Read every offer as a starting point, not a promise.

The marketplace tradeoff (our one honest admission)

The same thing that makes LendingTree useful — getting several lenders to compete for you at once — is also its biggest drawback: submitting a request can put your information in front of multiple partners, and the outreach can be heavy. That’s not disqualifying. Plenty of homeowners use it, pick a lender in a day or two, and move on. But it means you should know your loan lane and your comparison criteria before you fill out the form, not after.

Not sure which loan lane fits your project? Start with our ADU Financing Options guide — it compares every path before you talk to a single lender.

What happens after I submit the LendingTree form?

Submitting LendingTree’s form starts a chain: you enter your details, LendingTree may run a soft credit inquiry to match you, you receive conditional offers and contact from matched companies, and a hard credit pull happens only later if you proceed with a full application at a chosen lender. Knowing the sequence in advance is how you stay in control of it.

Here’s the typical path, step by step:

- 1

You fill out the Qualification Form

ZIP code, loan type, estimated credit, home value, and similar. LendingTree's Terms note you're representing that the information is true and accurate, so use real details.

- 2

A soft inquiry may run

This is what powers the match and does not affect your credit score.

- 3

You're matched with up to five providers

You see conditional offers — rate ranges and terms based on the limited information you gave.

- 4

Matched companies contact you

By phone, text, and email. For home-loan requests, that outreach can include not just lenders but real estate companies, brokers, and agents in LendingTree's network, per its Terms.

- 5

You pick one or two and apply

Comparing and talking to lenders is free; you only pay fees once you formally proceed.

- 6

A hard credit pull happens at the application stage

With your chosen lender, and the lender begins underwriting.

- 7

You receive a Loan Estimate

For mortgage products — the standardized cost sheet you use to compare the real numbers, and the lender orders an appraisal.

- 8

Underwriting proceeds

The lender verifies income, property, title, insurance, and ADU-specific documentation.

The real downsides: calls, data sharing, hard pulls, and conditional offers

The downsides of LendingTree aren’t mysterious or hidden — they’re structural to any lead marketplace: outreach from network partners, personal-data sharing, conditional offers that aren’t final approvals, and the possibility of a hard credit inquiry once you actually apply with a lender.

Data sharing is the business model

LendingTree’s privacy policy (last updated February 11, 2026) describes how your information may be disclosed to network partners when you submit a request, and notes that those partners may retain your information whether or not you ultimately use their services. For home-loan requests, the Terms also authorize sharing with real estate companies, brokers, and agents — not just lenders. LendingTree is paid by its partners, which is why the service is free to you. Treat the form as the start of marketing contact.

How to limit the contact: use a dedicated email address and a phone number you actually monitor; decide on your top one or two offers quickly; and give the companies you’re not using a clear “no thank you” early.

Calls and texts

Public complaint records show this is the most common friction point. Documented patterns on LendingTree’s Better Business Bureau profile and on review sites include heavy call and text volume and consumers asking to be added to do-not-call lists. We’re presenting this as a known risk pattern, not a universal experience — many users report a smooth process — but if you’ve read complaints about “the phone won’t stop ringing,” they’re not invented. They’re the cost of the compete-for-you model.

Soft pull vs. hard pull — when your credit actually gets hit

LendingTree’s matching form advertises personalized quotes with no hard credit pull — the initial match may use a soft inquiry, which doesn’t affect your score. The hard pull comes later, when you proceed with an actual application at a chosen lender. You can shop and compare conditional offers without a credit hit; the score impact arrives only when you formally apply. Before you authorize any lender’s full application, confirm the exact moment the soft inquiry becomes a hard one.

Conditional offers are not approvals

A conditional offer is a quoted range based on the limited information you entered — it can change after the lender verifies your income, pulls full credit, and orders an appraisal. For an ADU specifically, the appraisal step is where surprises live: the lender’s valuation of your project (especially on as-completed-value products) can move your borrowing power up or down.

Is LendingTree legit or safe to use for ADU financing?

Yes — LendingTree is a legitimate, long-established company, not a scam. It’s a publicly traded business (NASDAQ: TREE) that has operated since 1996, is licensed as a mortgage broker (NMLS #1136), and is accredited by the Better Business Bureau with an A+ rating. The honest caveat is “legit but noisy.”

Its BBB profile lists LendingTree as accredited since November 6, 2019, with an A+ rating and roughly 29 years in business; complaints logged there cluster around service, advertising, and sales/outreach rather than fraud. On Trustpilot, the company showed a TrustScore of 4.5 across about 17,000 reviews when we checked on May 25, 2026, with the large majority rating it five stars. The recurring negative theme is contact volume, not stolen money or fake lenders.

If “safe” means “will my information be handled by a real, licensed company,” the answer is yes. If “safe” means “will I avoid sales calls,” the answer is no — and that’s a feature of the model.

Sources: BBB profile (A+, accredited since 11/6/2019); Trustpilot profile (4.5, ~17K reviews, checked May 25, 2026); LendingTree corporate filings (NASDAQ: TREE). Verified May 2026.

What do LendingTree reviews actually tell you?

Public review signals are mixed in the way marketplace platforms usually are: a large, broadly positive Trustpilot profile alongside complaint sources showing recurring friction around calls, texts, and unwanted outreach. Use reviews to understand the marketplace experience — not to decide whether a specific ADU loan is right for you.

| Signal | What we found (verified May 25, 2026) | What it means for you |

|---|---|---|

| Trustpilot | 4.5 TrustScore, ~17,000 reviews, large majority 5-star; company replies to negative reviews | The typical experience is positive, but reviews are mostly about personal loans, mortgages, and insurance — not ADUs |

| Better Business Bureau | A+ rating, accredited since Nov. 6, 2019 | Established, accountable company; complaints skew toward outreach, not fraud |

| Complaint themes | Heavy calls/texts; requests to be suppressed or added to do-not-call lists | Plan to limit contact up front; pick an offer fast |

We do not attach our own star rating or review schema to this page, because we have not conducted a first-party scored review of LendingTree. The Trustpilot and BBB figures above are cited as third-party data, not repackaged as a Dwelling Index rating. Sources: Trustpilot, BBB.

How to compare LendingTree offers for an ADU without choosing the wrong loan

Compare the same loan type against the same ADU use case. A HELOC, a construction loan, a renovation mortgage, and a personal loan are not interchangeable just because each can produce cash — they differ on rate structure, lien position, disbursement, and total cost.

Compare Loan Estimates, not headlines

For mortgage products, the CFPB recommends using the standardized Loan Estimate to compare offers — it lays out the rate, monthly payment, closing costs, and key features in a consistent format. A headline rate can hide points and closing costs; the Loan Estimate is where the real number lives. Request one from every lender you’re seriously considering.

Compare these fields, every time

| Field | Why it matters for an ADU |

|---|---|

| Loan type | Determines draw structure, lien position, rate risk, and total cost |

| APR and fees | The headline rate can hide points and closing costs |

| Loan amount | A full detached ADU often runs into six figures — beyond small personal/home-improvement loans |

| Disbursement schedule | Staged builds and prefab deposits need money released in stages |

| Permit requirements | Some lenders require approved plans/permits before funding |

| Appraisal basis | Current value vs. as-completed value changes what you can borrow |

| Rental income treatment | Income from an existing ADU may or may not count toward qualifying |

| Prepayment terms | Matters if you'll refinance after the ADU is complete |

| Servicing | Determines who you deal with for the life of the loan |

Framework assembled from CFPB Loan Estimate guidance and ADU-specific underwriting factors. Verified May 2026.

Free resource

Download the free ADU Starter Kit

It includes this lender-question checklist, the Loan Estimate comparison fields, and a one-page financing-lane cheat sheet you can take into any lender call. No cost, no obligation — just the worksheet.

Get the free Starter Kit →Will a personal loan or home improvement loan cover a full ADU? A cost reality check

Usually not. Recent 2026 cost guides commonly place detached ADUs well into six figures — often $180,000 to $400,000 depending on size, finishes, and site work — which is far above the limits and pricing of most unsecured personal or home improvement loans. That gap is exactly why the equity-based and renovation lanes above exist.

| ADU type | Typical 2026 cost range | Practical financing implication |

|---|---|---|

| Garage conversion | ~$80,000–$150,000 | A Limited 203(k) ($75K cap) may cover the smallest projects; larger ones need equity or renovation lending |

| Junior ADU (JADU, within the existing home) | ~$80,000–$150,000 | Smaller scope, but still typically beyond a personal loan |

| Attached ADU | ~$150,000–$300,000 | Equity-based or renovation/construction lending territory |

| Detached new ADU | ~$200,000–$400,000+ | Almost always needs equity, construction, or as-completed-value lending |

Cost ranges synthesized from 2026 construction-cost guides including Angi and SelfStorage.com’s 2026 ADU cost guide. Ranges vary widely by location, size, and site conditions; get a site-specific estimate before sizing any loan. Verified May 2026.

LendingTree vs. a direct lender, credit union, or ADU specialist

LendingTree is best for comparison breadth. A direct lender is best for control and a single relationship. A local credit union can be best for relationship underwriting and local property knowledge. An ADU or renovation specialist is best when the financing depends on future value, construction draws, or ADU-specific documentation. There’s no universal winner — there’s a best fit for your bottleneck.

| Route | Best for | Main weakness | The ADU question to ask |

|---|---|---|---|

| LendingTree marketplace | Comparing several lenders quickly from one form | Partner outreach; not ADU-specialized | "Which of these matched lenders actually finance ADUs?" |

| Direct bank / lender | A controlled, single-relationship process | Fewer offers to compare | "Does this product allow ADU construction?" |

| Local credit union | Local underwriting and relationship banking | May have a narrow product menu | "Do you lend on ADU projects in this jurisdiction?" |

| Renovation / ADU specialist | Future-value lending, draws, complex projects | Availability and pricing vary | "Can you fund permits, draws, prefab deposits, and contingencies?" |

| Your existing mortgage lender | Keeping the relationship simple | May not carry the right product | "Can I keep my first mortgage and add a second lien?" |

The honest synthesis: if you already know your lane and your equity supports it, a marketplace is a reasonable time-saver. If your project is structurally complex — low equity, ground-up build, prefab deposit timing, rental-income qualifying — a specialist or a direct construction lender will usually serve you better, because the hard part isn’t finding a lender, it’s finding one who structures the loan correctly.

Alternatives to LendingTree for ADU financing

The right alternative depends on the financing problem, not the brand. Compare paths first, providers second.

If you have equity: compare HELOC and home equity loan offers — directly with a few lenders, or through a marketplace if you want the breadth. This is the most straightforward ADU financing path. Our Hometap vs. HELOC for ADU comparison breaks down second-lien options in detail.

If you want to keep a low first mortgage: look at a second lien (HELOC or home equity loan) before a cash-out refinance, so you don’t trade away your existing rate. Run the math both ways before deciding.

If your project depends on future value: prioritize renovation and as-completed-value lending — Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, FHA 203(k), or a renovation specialist. See our renovation-loan alternatives guide for how this category works.

If you’re building a prefab or modular ADU: the financing has to match the manufacturer’s deposit and delivery schedule. See our prefab ADU financing guide for how to line up draws with milestone payments.

If you’re converting a garage: smaller scopes open up loan types that don’t fit a full detached build. Our garage conversion financing guide covers the lanes that fit.

If you’re building for rental income: treat it as an investor-leaning decision and confirm whether ADU rent counts toward qualification. Our ADU rental financing guide walks through the documentation.

The Dwelling Index is reader-supported and may earn a commission, at no extra cost to you, when you use the link below to explore financing options. We present financing lanes, never compensation-ranked lenders, and our recommendations are based on independent research. Read our full disclosure.

Compare mortgage-backed paths

Explore mortgage-backed ADU financing options → Compare cash-out refinance, construction, and renovation paths

If you’d rather look at the mortgage and construction-loan lanes with a lender directly — instead of fielding several marketplace calls — this is a straightforward place to start. Educational only; no obligation, and you compare your own Loan Estimates.

Compare ADU mortgage options →Edge cases most reviews skip

Whether you can rent your ADU, sell it separately, or even need your loan to survive a future home sale depends on rules that vary by state and city — and these can change how much you actually need to finance.

Owner-occupancy and renting

California law currently bars local agencies from imposing owner-occupancy requirements on standard ADUs — meaning, in California, you generally don’t have to live on the property to rent out the ADU (California Government Code § 66315). Junior ADUs are different: § 66333 requires owner occupancy only when the JADU shares sanitation facilities with the main home. Rules differ sharply by state, so verify your local ordinance before you assume you can rent.

Selling the ADU separately

California’s AB 1033 (effective since January 1, 2024) lets cities opt in to allow ADUs to be sold separately as condominiums. Verified participating jurisdictions include the City of San José and the unincorporated County of San Diego; press reporting in August 2025 indicated Santa Monica, Santa Cruz, San Francisco, and San Diego had followed San José. San Diego County adopted its local ADU ordinance amendment implementing AB 1033 on March 4, 2026, with implementation effective April 4, 2026. Confirm your specific city’s status directly — adoption is local and still expanding.

Utility hookups, setbacks, and site work

A detached ADU often needs new utility laterals (the lines connecting your unit to the main sewer, water, and power), and running them adds to the budget. Setback requirements and site work (grading, drainage, access) can move the cost enough that the loan amount you thought you needed isn’t enough. Get a site-specific estimate before you size the loan.

What happens if you sell the property

A home equity loan, HELOC, or cash-out refinance is tied to the home — when you sell, the loan is paid off from the proceeds at closing. If you’ve drawn heavily and the ADU hasn’t fully boosted the appraised value yet, your net proceeds shrink. Factor your exit horizon into which product you choose.

Sources: California Gov. Code § 66315 and § 66333; San Diego County ADU Zoning Ordinance Amendment (adopted March 4, 2026). Verified May 2026. Always confirm current local rules with your city or county planning department.

What we verified

| Verified item | Source (linked) |

|---|---|

| LendingTree is not the lender/creditor and does not make credit decisions | LendingTree Terms of Use |

| Network of 300+ lenders; matches up to five | LendingTree homepage |

| No hard pull at initial match; soft inquiry may be used; hard pull at provider application | LendingTree Terms of Use; U.S. News review |

| Home-loan requests may be shared with lenders and real estate companies/brokers/agents | LendingTree Terms of Use |

| Privacy policy permits disclosure to network partners (updated Feb. 11, 2026) | LendingTree Privacy Policy |

| FHA Limited 203(k) cap is $75,000 for case numbers on/after Nov. 4, 2024 | HUD 203(k) — Mortgagee Letter 2024-13 |

| Fannie Mae products can add/renovate an ADU | Fannie Mae ADU page |

| Fannie Mae counts income from an existing ADU (≤30% of qualifying income; one ADU; purchase/limited cash-out; one-unit principal residence) | Fannie Mae SEL-2025-08; Selling Guide B3-3.8-01 |

| Freddie Mac may allow ADU rental income in certain cases | Freddie Mac ADU guidance |

| CFPB recommends comparing Loan Estimates across lenders | CFPB Loan Estimate |

| CA Gov. Code §66315 (owner-occupancy) and §66333 (JADU); AB 1033 (separate sale) | Justia §66315; San Diego County |

| 2026 ADU cost ranges by type | Angi; SelfStorage.com |

| Trustpilot 4.5 / ~17K reviews; BBB A+ accredited since 11/6/2019 | Trustpilot; BBB |

Last verified: May 25, 2026.

Lending terms, partner status, agency rules, review counts, and local ordinances change. Re-verify dated figures before relying on them.

Methodology

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. For this review, we examined LendingTree’s official Terms of Use, privacy policy, and product pages (home equity, HELOC, home improvement, construction, and renovation loans); cross-checked those claims against primary and authoritative federal and agency sources from the CFPB, HUD, Fannie Mae, and Freddie Mac; reviewed third-party signals from Trustpilot and the Better Business Bureau; pulled 2026 ADU cost ranges from multiple construction-cost guides; and mapped each financing lane to common ADU situations. We did not sort providers by compensation, and we present financing as paths rather than “best lender” rankings. We do not guarantee approval, rates, loan terms, ADU rental income, or project feasibility — those depend on lender underwriting, your property’s value, equity, credit, debt-to-income ratio, the ADU’s scope, permits, and local regulations.

Frequently asked questions

Can LendingTree finance an ADU?

LendingTree does not directly finance ADUs. It is a marketplace that can connect you with lenders offering products usable for an ADU — home equity loans, HELOCs, cash-out refinances, construction loans, and renovation mortgages — depending on the product, lender, property, and state. Its own Terms of Use state it is not a lender or creditor and does not make credit decisions.

Is LendingTree a lender?

No. LendingTree is an online marketplace and licensed mortgage broker (NMLS #1136). It does not originate, service, or make credit decisions on loans — lenders in its network do that. LendingTree is paid by those partners, which is why the matching service is free to you.

Is LendingTree legit and safe to use?

Yes. LendingTree is a publicly traded company (NASDAQ: TREE) operating since 1996, licensed as a mortgage broker, and BBB-accredited with an A+ rating since November 6, 2019. It's a real, regulated company — not a scam. The honest caveat is 'legit but noisy': expect heavy calls, texts, and broad data sharing as part of the marketplace model.

Does LendingTree do a hard credit pull?

Not at the initial match. The match may use a soft inquiry, which does not affect your credit score. A hard inquiry typically occurs later, only if you proceed with a full application at a chosen lender. Confirm the exact timing with the lender before authorizing a full application.

Will LendingTree lenders call me?

Probably, yes. LendingTree's privacy policy says it may disclose your information to network partners when you submit a request, and those partners may keep that information whether or not you use their services. For home-loan requests, the Terms also allow sharing with real estate companies, brokers, and agents. Expect calls, texts, and emails — and use a dedicated email and a monitored phone line to manage the volume.

What loan type is best for an ADU?

There's no universal best. HELOCs and home equity loans suit owners with current equity; renovation mortgages (HomeStyle, CHOICERenovation, FHA 203(k)) suit owners using as-completed value; construction-to-permanent loans suit ground-up builds with staged draws; personal loans suit only small scopes or gap funding. The right product depends on your equity, mortgage rate, project cost, draw needs, and lender rules.

Can I use a HELOC to build an ADU?

Often, yes — if you qualify and the lender allows the use of funds. HELOCs are secured by your home, usually carry variable rates, and are limited by your current equity. The draw flexibility can suit a staged build, but the variable rate and foreclosure risk are real tradeoffs.

Can I use a home equity loan for an ADU?

Yes, in many cases — but verify ADU eligibility, closing costs, lien position, and whether the lump sum covers the full project plus a contingency. The home secures the loan, and cost overruns can leave a funding gap since you've already drawn the full amount.

Is a personal loan enough for an ADU?

Usually not for a full detached ADU, which commonly runs into six figures. A personal loan can help with a small conversion or as gap funding. Compare loan amount, APR, fees, term, and funding timeline carefully before relying on one.

Can ADU rental income help me qualify?

Sometimes. As of October 8, 2025, Fannie Mae allows rental income from an existing ADU on a one-unit principal residence (up to 30% of qualifying income, one ADU, purchase or limited cash-out refinance), with a market-rent appraisal. Freddie Mac allows ADU rental income in certain cases. Rules are program- and lender-specific, and lender adoption varies — ask directly.

Is LendingTree better than a local credit union for an ADU?

LendingTree may be better for comparing multiple offers quickly. A local credit union may be better if it understands local ADU permitting, local appraisals, or relationship underwriting. The best choice depends on whether your bottleneck is comparison breadth or ADU-specific structuring.

Keep going

Building an ADU is a sequence of decisions — what you can build, what it’ll cost, and how you’ll pay for it — and financing is just one link. Once you know your lane, the rest gets a lot less overwhelming.

Know your buildable size before you talk to any lender

Get your free ADU report in 60 seconds — your lot, your ADU type, your likely cost range. That’s the first step, no matter which financing lane you choose.

Get my free ADU report →