Hometap vs HELOC for ADU: Real Costs, Risks & the Right Fit

Bottom Line

Hometap vs HELOC for ADU comes down to one question: are you solving for monthly-payment relief, or do you want to keep all the value your ADU creates? If your current equity covers the project and you can handle a second monthly payment, a HELOC is almost always the smarter ADU financing move — you pay interest, but every dollar of value your ADU adds stays with you. Hometap makes more sense when monthly payments would strain your budget or when you can't qualify for a HELOC.

The financing choice you make today will shape how much of your ADU's value you actually keep.

This guide breaks down exactly how each financing path works for ADU construction specifically — not kitchens, not debt consolidation, not generic “home improvement” — so you can stop second-guessing and start building.

Last verified: April 2026 · Independent ADU resource — not a lender or broker · By The Dwelling Index Editorial Team

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure · Editorial methodology

Quick Verdict: Hometap vs. HELOC vs. Figure for ADU Projects

Before the details, here's the comparison at a glance.

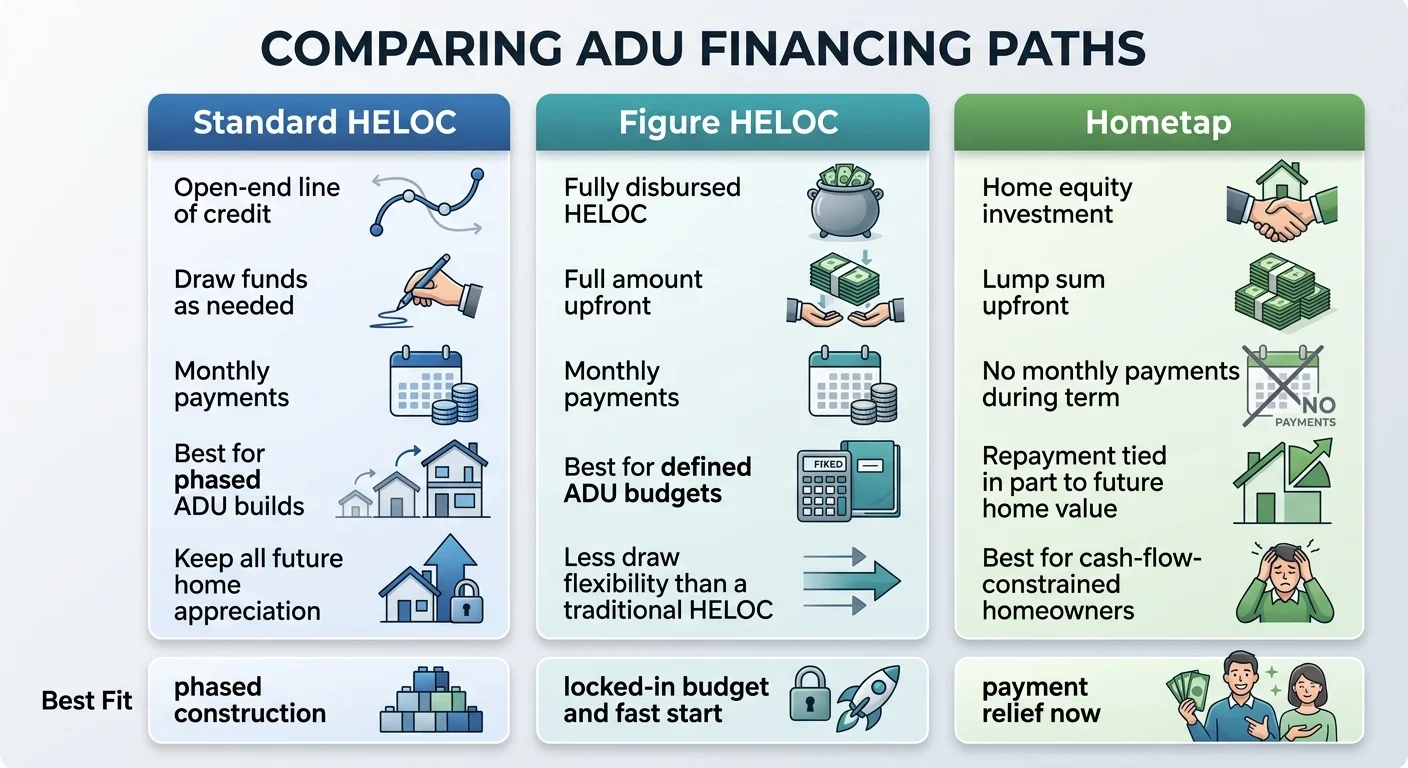

| Standard HELOC | Figure (HELOC lane) | Hometap (HEI) | |

|---|---|---|---|

| Product type | Revolving credit line — draw as needed | Fully disbursed HELOC — full amount at closing | Equity sharing agreement — not a loan |

| How funds arrive | Draw in stages as construction progresses | Full amount disbursed upfront | Lump sum at closing |

| Monthly payments | Yes — interest-only during draw, then principal + interest | Yes — payments begin immediately | None during the 10-year term |

| Best ADU fit | Phased builds with contractor milestone payments | Defined budget, immediate start, full amount needed upfront | Equity-rich homeowner who can't take on another monthly payment |

| Biggest watch-out | Variable rates can rise; line can be frozen | Less draw flexibility than traditional HELOC | You share ADU appreciation; must settle within 10 years |

| State availability | Most states | Check directly — restrictions vary | 16 states (as of April 2026) |

| Wrong-reader warning | If monthly payments would strain your budget during construction | If you need phased draws over many months | If you plan to stay 10+ years without a settlement plan, or your state isn't covered |

Product details verified from Figure.com, Hometap.com, and provider documentation as of April 2026. Terms, availability, and qualification requirements change — confirm directly with each provider before applying.

Choose based on your cash flow, project structure, and how long you plan to keep the home.

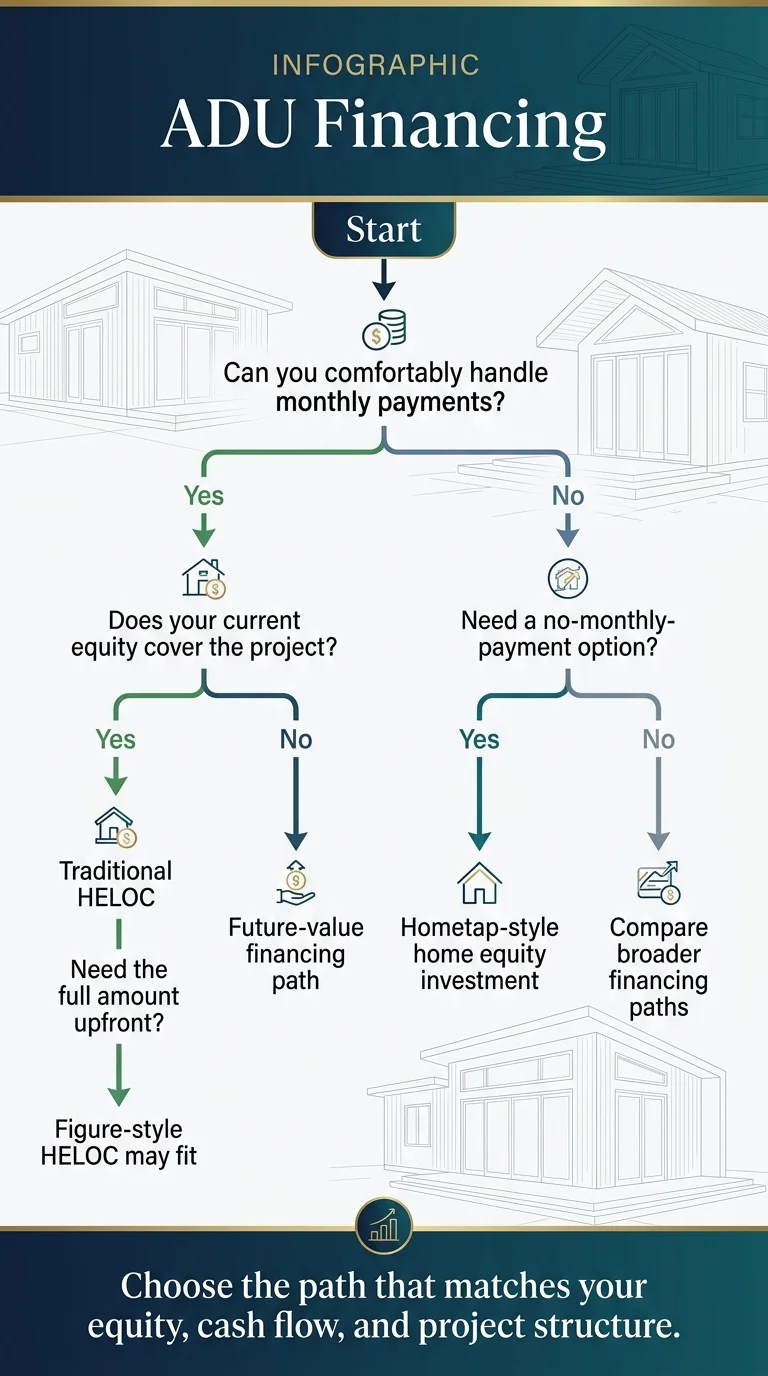

Which Path Fits Your Situation? Start Here

Most people don't need to read 8,000 words before they know their lane. The right financing path depends on three things: your current equity, your monthly cash-flow tolerance, and how long you plan to keep the home. Everything else is detail.

If: You can handle monthly payments and your current equity covers the project

Start in the HELOC lane.

You'll pay interest on what you borrow, but you keep 100% of the value your ADU creates. For most homeowners with solid equity and steady income, this is the path that costs less over time — often significantly less.

If: Cash flow is tight and "no monthly payments" matters more than total long-term cost

Look at a Home Equity Investment like Hometap.

You're trading future appreciation for payment relief now. That trade isn't free — the CFPB has noted that home equity contracts can end up costing more than HELOCs when the home appreciates — but it may be the right trade for your situation. (Source: CFPB, "Issue Spotlight: Home Equity Contracts," January 2025)

If: Your current equity doesn't cover the ADU budget

Stop comparing Hometap and HELOCs — neither is designed to solve a current-equity shortfall.

You need a product that lends based on what your home will be worth after the ADU is built — a renovation HELOC or construction loan.

If: You need speed and have a defined, locked-in budget

Figure's fully disbursed HELOC structure may be a fit.

Unlike a traditional HELOC where you draw funds in stages, Figure delivers the full amount at closing. That works well when you know exactly what the project costs and want to move fast.

Match Your Situation to the Right Lane

| Your situation | Best first lane | Why | Biggest risk to watch |

|---|---|---|---|

| Strong equity, comfortable with monthly payments | Standard HELOC | Lowest total cost; keep all future appreciation | Variable rate may rise; payments start immediately |

| Equity-rich but cash-flow-constrained (retiree, self-employed, single income) | Hometap HEI | No monthly payments; no DTI impact | You share future appreciation; 10-year settlement clock |

| Low current equity, recent home purchase | Renovation HELOC or construction loan | Borrows against after-renovation value | Higher qualification bar; limited lender availability |

| Defined ADU budget, want fast funding | Figure HELOC | Full amount at closing; fast approval | Less flexibility for phased draws during construction |

| Not sure / complicated situation | Compare across lanes | See what you actually qualify for | Don't force a product that doesn't fit |

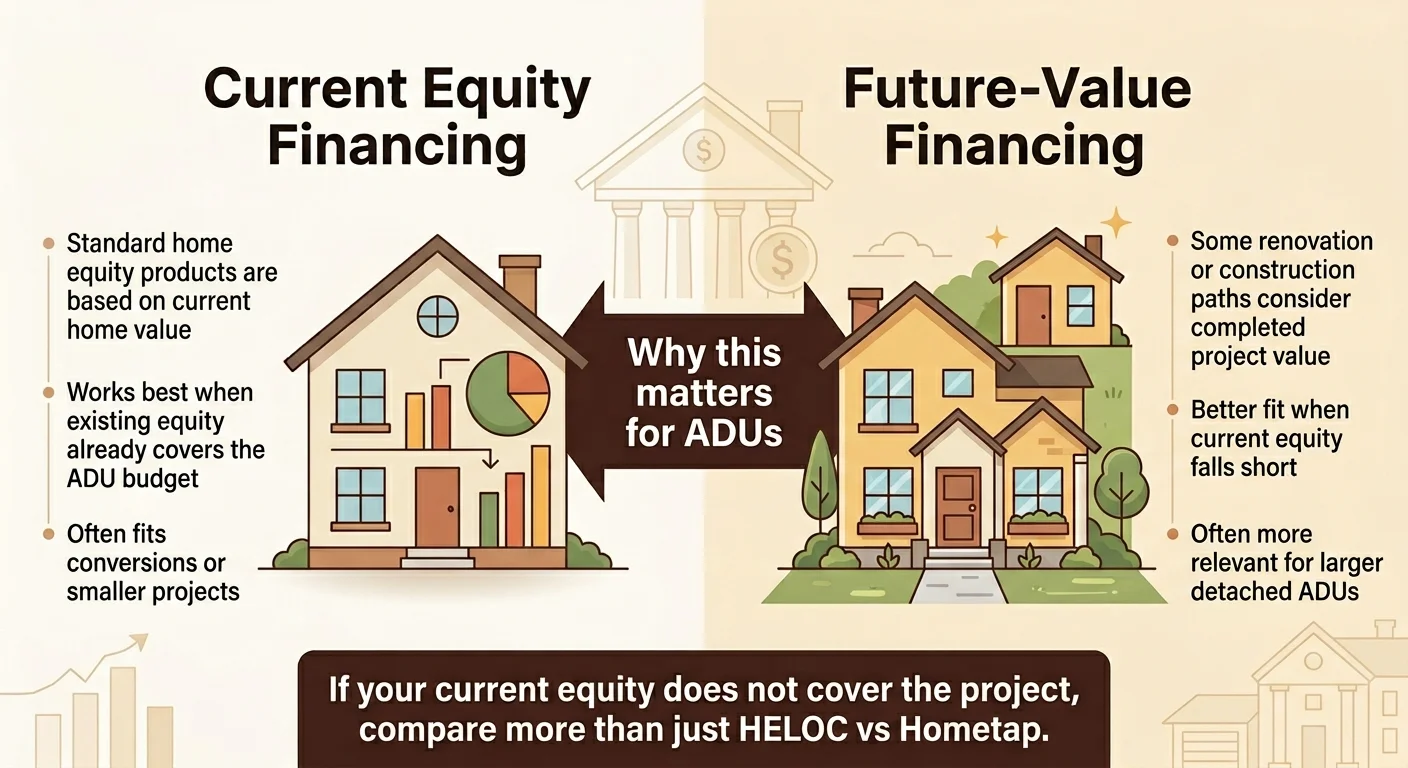

Does Your Current Equity Even Cover the ADU You Want?

This is the gating question that most comparison pages bury on page three. If your current equity can't cover the project, the entire Hometap-vs.-HELOC debate is moot — and you need a different financing product entirely.

Both standard HELOCs and Hometap's Home Equity Investment are capped by your home's current appraised value — not what it'll be worth after the ADU is built. The Urban Institute highlighted this in its 2024 ADU financing analysis: home equity extraction vehicles are generally constrained by current market value, which is why ADU projects — especially detached new-construction units — frequently exceed standard borrowing capacity. (Source: Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing,” April 2024)

If your current equity does not cover the project, compare more than just HELOC vs. Hometap.

The Borrowing-Room Formula

Available HELOC Amount

(Current home value × max CLTV) − mortgage balance

Most lenders cap combined loan-to-value (CLTV) at 80–85%. Some go to 90% for primary residences with strong qualifications.

Example: $500,000 home, $300,000 owed, 80% CLTV

$500,000 × 0.80 = $400,000 − $300,000 = $100,000 available

If your ADU project is budgeted at $175,000, a standard HELOC won't get you there. You need a renovation HELOC or different product.

For Hometap:

The investment cap is typically up to 25% of your home's current value, with a maximum of $600,000. On a $500,000 home, that's up to $125,000 — which may or may not cover the full ADU budget depending on scope.

Why Detached ADUs Break Current-Value Math Faster

Garage conversion

Typically $50,000–$120,000 — a range that frequently fits inside standard HELOC borrowing room for homeowners with moderate equity.

Detached new-build ADU

Typically $150,000–$300,000+. Frequently exceeds available borrowing capacity under current-value lending, creating a gap between what you can access and what the project costs.

What to Do If the Math Falls Short

Renovation HELOC

Products like RenoFi lend based on your home's after-renovation value, not just current value. Since an ADU adds meaningful value to your property, this can dramatically expand borrowing power. Available in all states except Texas.

Explore RenoFi →Construction loan

Designed for ground-up builds, evaluated on after-completion value. Higher documentation requirements, but purpose-built for this use case.

Fannie Mae HomeStyle or Freddie Mac CHOICERenovation

Renovation mortgage products that can cover ADU construction. Some programs allow projected rental income to help with qualification. (Source: Fannie Mae, singlefamily.fanniemae.com)

See What's Possible at Your Address

Not sure how much ADU your property can support? Get your free ADU feasibility report in 60 seconds.

Get Your Free ADU ReportWhy a HELOC Is Usually the Better ADU Move (If You Can Handle the Payment)

For homeowners who have the equity and the monthly cash flow, a HELOC is typically the most cost-effective way to finance an ADU. Here's why it aligns with how ADU construction actually works.

Staged draws match contractor payment schedules

ADU construction happens in phases: design and permitting, site prep, foundation, framing, mechanical rough-in, finishes, final inspection. Most contractors bill at milestones — not all at once. A traditional HELOC's revolving draw structure mirrors this perfectly. You pull $15,000 for design and permits. Another $30,000 when the foundation goes in. Another $40,000 at framing. You only pay interest on what you've actually drawn, which keeps costs lower during the months before the ADU is generating income.

In the Urban Institute's summary of a California homeowner survey, 43% of respondents used mortgage products to finance an ADU, and among that subgroup, 56% used a HELOC or home equity loan — making it the most common mortgage-based ADU financing method. (Source: Urban Institute, 2024)

You keep your existing first mortgage

This matters enormously in 2026. If you locked in a first mortgage at 3–4% during 2020–2021, a HELOC sits alongside that mortgage as a second lien. Your first mortgage terms stay exactly the same. No refinancing required, no rate reset, no new closing costs on your primary loan.

You keep all the value your ADU creates

This is the single biggest financial argument for the HELOC lane in ADU financing, and most comparison articles gloss over it. When you build an ADU that adds substantial value to your property, every dollar of that appreciation belongs to you. With a HELOC, you pay interest on the borrowed amount — but the value the ADU creates is 100% yours. With a Home Equity Investment, you're sharing that appreciation.

The HELOC Risks You Need to Hear

Variable rates. Most HELOCs have variable interest rates. If rates rise during your draw or repayment period, your monthly payment increases.

Your home is collateral. A HELOC is secured by your house. If you can't make payments, foreclosure is a possibility. CFPB guidance notes that lenders can freeze or reduce your credit line in certain circumstances — declining home values, changes in your financial situation, or broader economic conditions. (Source: CFPB, "What You Should Know About Home Equity Lines of Credit")

Payments start before rental income. If you're building an ADU for rental income, there's a gap — typically months of construction — where you're making HELOC payments with no rental revenue to offset them. Budget for carrying costs during the build.

A HELOC can affect refinancing. If you want to refinance your first mortgage later, you may need your HELOC lender to approve a subordination agreement. If that lender refuses, you may need to pay off the HELOC before refinancing. (Source: CFPB)

How Is Figure Different from a Standard HELOC for ADU Builds?

Figure gets lumped into the “HELOC” bucket, but it works differently — and that difference matters for ADU projects.

Figure's Fully Disbursed Structure, in Plain English

Unlike a traditional HELOC where you draw funds incrementally, Figure delivers the full approved amount at closing. Payments begin immediately. You can redraw funds as you pay down the balance, but the initial disbursement is the full line amount. Figure offers both fixed- and variable-rate options depending on the product. (Source: Figure.com, product documentation, verified April 2026)

When Figure Works Better for an ADU

- You have a defined, locked-in ADU budget with a GC who wants full funding secured before breaking ground

- You want fast funding — Figure markets rapid approval and funding timelines

- You're building a prefab or modular ADU where the manufacturer requires full payment or large deposits upfront

- You prefer certainty — you know exactly what you're borrowing and what you'll pay from day one

When Figure May Not Be the Best Fit

- You're doing a phased, stick-built ADU over 8–12 months and want to draw funds incrementally — a traditional HELOC's staged draw structure may save interest during the build

- Your budget is uncertain and you want flexibility to borrow only what you need

- You'd rather minimize interest charges by deploying money only as it's actually spent on construction

State availability varies and has changed over time. Always check directly at Figure.com.

Comfortable with monthly payments? Explore current HELOC options for ADU financing

Including Figure and traditional staged-draw HELOCs.

Affiliate disclosure: See full disclosure.

When Does Hometap Actually Make Sense for an ADU?

Let's be direct about what Hometap is and isn't.

Hometap is a Home Equity Investment (HEI) company — not a lender. Instead of borrowing money and paying interest, you receive a lump sum of cash in exchange for a percentage of your home's future value. There are no monthly payments during the 10-year term. When the term ends — or sooner, if you choose — you settle by selling the home, refinancing, using savings, or taking out a loan to buy out Hometap's share. (Source: Hometap.com, product terms and FAQ, verified April 2026)

The Real Hometap Buyer: Equity-Rich, Cash-Flow-Poor

Hometap's sweet spot is the homeowner who has significant home equity but can't — or doesn't want to — add another monthly payment. That profile includes:

Retirees on fixed income

Building an ADU for an aging parent or supplemental rental income where a monthly payment would strain the budget.

Self-employed homeowners

Irregular income or non-traditional documentation can make HELOC qualification difficult. Hometap's criteria are generally more flexible.

High debt-to-income ratio

If existing debt rules out traditional lending, a HEI doesn't add to your DTI.

Credit profile below typical HELOC thresholds

Hometap generally has more flexible credit requirements than most HELOC lenders.

Which Costs Less Over Time for an ADU?

If your home is likely to appreciate — and you're building an ADU, which will add value — a HELOC is usually easier to model and often costs less overall. You're paying a known interest rate on a known balance, and you keep 100% of the appreciation.

With Hometap, the eventual settlement amount is harder to predict because it's tied to your home's future value. The CFPB has specifically noted that repayment on home equity contracts can be difficult to predict, can run very high, and will often be more expensive than a HELOC if the home appreciates. (Source: CFPB, “Issue Spotlight: Home Equity Contracts,” January 2025)

For an ADU, a HELOC is usually better if you can afford the payment and your current equity covers the project. Choose Hometap mainly when cash flow is the problem — not when total long-term cost is the problem.

When Hometap Is the Wrong ADU Move

You plan to stay in the home 10+ years without a clear settlement plan.

Hometap's term is 10 years. At the end, you must settle — by selling, refinancing, using savings, or taking out a loan. If you cannot repay the settlement amount, you may have to sell the home or face foreclosure risk. (Source: CFPB, January 2025; Hometap records a lien in the form of a mortgage or deed of trust)

Your local market is appreciating rapidly.

The faster your home gains value, the more the settlement costs. In high-appreciation markets, the effective cost of a Hometap investment can significantly exceed what you'd pay in HELOC interest.

Your state isn't covered.

As of April 2026, Hometap says it is making investments in 16 states: Arizona, California, Florida, Indiana, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia. If your state isn't on that list, this comparison ends here.

Need to avoid monthly payments?

Check whether Hometap is available in your state and see if a home equity investment fits your ADU project.

Affiliate disclosure: See full disclosure.

Will Hometap Count the Value Your ADU Adds?

This is the most important ADU-specific question on this page — and almost every generic “Hometap vs. HELOC” article skips it entirely.

Here's why it matters: if you invest $150,000 in an ADU that adds substantial value to your home, does Hometap's settlement calculation credit you for creating that value — or does their share grow alongside it?

What the CFPB says about home improvements and HEIs

The CFPB's January 2025 report on home equity contracts specifically notes that some HEI companies credit homeowners for renovations or improvements, while others do not. The CFPB recommends asking before signing whether improvements will be excluded from the settlement calculation. (Source: CFPB, “Issue Spotlight: Home Equity Contracts,” January 2025)

What Hometap says about renovation adjustments

Hometap says some qualified renovations costing $25,000 or more may qualify for a renovation adjustment. After the renovation, the homeowner provides evidence such as receipts and photographs. If the request is approved following appraisal, the adjustment is based on the difference between the post-renovation appraised value and the hypothetical value of the property without the renovation. Accepted renovation adjustments are not guaranteed. (Source: Hometap.com, renovation adjustment documentation, verified April 2026)

What this means for ADU builders

An ADU project will almost certainly exceed the $25,000 minimum threshold, so it should qualify for a renovation adjustment request. If approved, the value your ADU directly adds to the property could be excluded from Hometap's share — potentially saving you a significant amount at settlement.

But “could” is doing heavy lifting. The adjustment isn't automatic, isn't guaranteed, and Hometap determines the methodology for separating renovation-driven value from baseline appreciation.

Before signing any agreement, get clarity in writing on:

- Whether a detached ADU is treated the same as an interior renovation

- What documentation you'll need (receipts, photos, contractor records, permits)

- What appraisal method will be used to isolate the ADU's contribution to value

- What costs count — just hard construction, or also design, permits, and landscaping?

- How the "hypothetical non-renovated value" is determined at settlement

On a $150,000 ADU project, the renovation adjustment could be the difference between a manageable settlement and a painful one.

How Your ADU Type Changes the Answer

Not all ADUs are created equal — and project type shifts the financing equation more than most people realize.

ADU type is the biggest variable in your financing math. Project cost and equity requirements differ dramatically across types.

Garage conversion

Best lane: HELOCTypically costs $50,000–$120,000 — a range that frequently fits within standard HELOC borrowing room. The project timeline is shorter, permitting is generally simpler, and the overall budget is easier to contain. For most homeowners with moderate-to-strong equity, a HELOC covers a garage conversion comfortably.

Detached ADU

Best lane: Depends on equityAt $150,000–$300,000+, many homeowners discover their available HELOC amount falls short — especially if they purchased in the last few years. This is also where the Hometap appreciation question becomes most acute, because a detached ADU tends to add more value to the property — which means a potentially larger share going to Hometap at settlement.

Aging-parent ADU

Best lane: Hometap if cash-flow-constrainedIf you're building an ADU for a parent who needs nearby housing, the primary motivation isn't rental income — it's care, proximity, and peace of mind. Monthly HELOC payments may feel like an unwelcome burden on top of an already demanding situation, and Hometap's no-payment structure becomes more defensible.

See our ADU for aging parents guideRental ADU

Best lane: HELOCIf you're building specifically for rental income, the financial case for a HELOC is strongest. Rental revenue can offset or exceed monthly HELOC payments — often creating positive cash flow — and you keep 100% of the property value increase. Sharing that appreciation through an HEI means giving away part of the very asset you're building to generate income.

| ADU type | Typical cost range | Usually best lane | What matters most |

|---|---|---|---|

| Garage conversion | $50K–$120K | Standard HELOC | Fits within most borrowing limits |

| Detached new build | $150K–$300K+ | Depends on equity — may need renovation HELOC | Current equity may fall short |

| Aging-parent suite | $80K–$200K | Hometap if cash-flow-constrained; HELOC if not | Payment relief vs. total cost |

| Rental ADU | $100K–$250K | HELOC | Rental income offsets payments; keep full appreciation |

| Home office / guest | $50K–$100K | Standard HELOC or Figure | Smaller scope, easier to fit in borrowing room |

Cost ranges are national estimates and vary significantly by location, size, complexity, and site conditions. Get local contractor bids for accurate project-specific numbers.

Curious what type of ADU your property supports?

See your lot size, zoning eligibility, estimated costs, and ADU options for your specific address.

Get Your Free ADU Feasibility ReportWhat Happens If You Sell, Refinance, or Keep the Home Beyond 10 Years?

The right financing choice today can look very different five or ten years from now. Here's how each path ages.

If you sell in 2–5 years

HELOC

You pay off the remaining balance from sale proceeds. Straightforward.

Hometap

You settle the investment from sale proceeds. If the home has appreciated meaningfully — especially with an ADU — Hometap's share will reflect that higher value. Review your specific terms carefully.

If you want to refinance later

HELOC

A HELOC is a second lien. If you want to refinance your first mortgage, you may need HELOC lender approval for a subordination agreement. If the lender declines, you may need to pay off the HELOC first. (Source: CFPB)

Hometap

Refinancing while a Hometap investment is active can be complicated. Hometap holds a lien on your property. The CFPB has noted that homeowners may face difficulty refinancing with an active home equity contract. (Source: CFPB, January 2025)

If you plan to keep the home 10+ years

HELOC

You continue making payments until the balance is paid off. The timeline is defined, the math is predictable, and the home's appreciation is entirely yours.

Hometap

The 10-year term means you must settle by term end. If you haven't sold, you need to buy out Hometap's share using savings, a refinance, or a new loan. If you cannot repay, you may have to sell or face foreclosure risk. (Source: CFPB, January 2025; Hometap terms)

If you want to pass the property to your kids

HELOC

The balance can be paid off at any time, and the property transfers cleanly.

Hometap

The investment must be settled before or during any property transfer — adding complexity to estate planning.

Bottom line:

If you're building an ADU because you plan to age in place or keep the property long-term, make sure you have a realistic plan for how you'll settle before signing.

What Risks Do Most Comparison Pages Bury?

Good financial content doesn't hide the downsides behind the CTA buttons. Here's what you should understand before choosing either path.

The HELOC Risks

- Payment strain during construction — you're paying interest before the ADU generates any income. Budget for months of carrying costs.

- Variable rate exposure — most HELOCs have variable rates. In a rising-rate environment, your payments can increase.

- Line freezes and reductions — CFPB guidance notes that lenders can freeze or reduce your credit line in certain circumstances.

- Subordination friction — if you want to refinance your first mortgage later, the HELOC lender may need to approve subordination.

- Your home is collateral — default on a HELOC and you face potential foreclosure.

The Hometap Risks

- Unpredictable total cost — because the settlement amount is tied to your home's future value, you can't know exactly what you'll owe. The CFPB has flagged this as a significant consumer concern.

- Appreciation sharing hits harder for ADUs — the value created by your ADU directly increases what you owe Hometap. Even with a renovation adjustment, baseline market appreciation compounds over time.

- 10-year settlement pressure — if you cannot repay at term end, you may have to sell the home or face foreclosure risk.

- Limited availability — only 16 states as of April 2026.

What timeline and cash-flow risks should you plan for?

A financing path that works on paper can still create stress if permits, contractor milestones, or occupancy take longer than expected. Before choosing a product, make sure your financing structure matches how your contractor will actually bill — and that you can comfortably carry costs for longer than your best-case construction timeline. Build in buffer. Every experienced ADU builder will tell you: projects take longer than the quote says.

A note on taxes

For HELOCs used to build or substantially improve the home that secures the loan, the interest may be tax-deductible under current IRS rules, subject to overall mortgage interest deduction limits. (Source: IRS Publication 936) Hometap investments are structured as equity agreements, not loans, which creates different and more complex tax implications. Consult a CPA or tax advisor before making decisions based on tax assumptions.

What If Neither Hometap nor a Standard HELOC Is the Right Move?

If neither product fits your situation, pretending otherwise helps nobody. Here's what separates an honest resource from a thin affiliate page.

You're a recent buyer with limited equity

If you purchased your home in the last 2–5 years, you may not have enough equity for either a standard HELOC or a Hometap investment to cover an ADU project. You need a product that accounts for the value the ADU will add.

Renovation HELOC (e.g., RenoFi)

Lends based on after-renovation value — up to 90% of what your home will be worth with the ADU completed. This can increase borrowing power dramatically. Available in all states except Texas.

Explore RenoFi →Your ADU budget exceeds current borrowing room

Even if you have some equity, it may not be enough. A $175,000 detached ADU on a home with $80,000 in available borrowing room means you're $95,000 short.

Construction loan

Purpose-built for ground-up projects. The lender evaluates after-completion value and disburses funds at construction milestones.

You want more options on the table

Fannie Mae HomeStyle Renovation Mortgage and Freddie Mac CHOICERenovation

Renovation mortgage products that can finance ADU construction. Some programs allow projected rental income to help with qualification. (Source: Fannie Mae, singlefamily.fanniemae.com)

LendingTree

If you want to compare offers across multiple lender types — HELOC, home equity loan, renovation loan — a lending marketplace lets you see what you qualify for without committing to a single path.

Compare lenders on LendingTree →Your equity math came up short?

That doesn't mean your ADU project is dead. Explore financing paths that use your home's future value — not just current equity.

The Decision in One Frame

Choose the path that matches your equity, cash flow, and project structure.

You already know you want to build an ADU. The question is how to pay for it without making a mistake you'll feel for the next decade. The answer, for most people, is simpler than the internet makes it:

Can you handle the payment and does your equity cover the project?

→ HELOC. You pay interest, keep the appreciation, and own the outcome.

Is cash flow the problem, not total cost?

→ Hometap, if your state is covered and you have a realistic plan to settle within 10 years.

Does your equity fall short?

→ Renovation HELOC or construction loan. Don't force a product that doesn't fit.

That's it. Everything else on this page is supporting evidence for those three paths. The next step is yours.

How We Evaluated These Financing Paths

We built this comparison using product documentation directly from Hometap.com and Figure.com, consumer-protection analysis from the CFPB, ADU financing research from the Urban Institute, IRS guidance on mortgage interest deductibility, and Fannie Mae/Freddie Mac ADU program documentation.

What we verified directly: Product structures, qualification requirements, state availability, renovation adjustment terms, and settlement mechanics — confirmed against official provider documentation as of April 2026.

What we estimated editorially: Cost ranges and rental income ranges are based on publicly available market data. They are illustrative, not quotes, guarantees, or financial advice.

Why we don't rank lenders by payout: Our comparison tables are organized by product type, financing lane, and documented features — never by which partner pays us more.

Sources consulted:

- Consumer Financial Protection Bureau, "Issue Spotlight: Home Equity Contracts" (January 2025)

- CFPB, "What You Should Know About Home Equity Lines of Credit"

- CFPB, "Does a HELOC Affect My Ability to Refinance?"

- Urban Institute, "To Increase the Housing Supply, Focus on ADU Financing" (April 2024)

- Fannie Mae Single-Family, "Accessory Dwelling Units"

- IRS Publication 936

- Hometap.com (product terms, FAQ, renovation adjustments) — verified April 2026

- Figure.com (product documentation) — verified April 2026

The Dwelling Index is reader-supported. When you use our links, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure · Editorial methodology

Frequently Asked Questions

Which is better for an ADU — Hometap or a HELOC?

For most homeowners who qualify for both, a HELOC costs less over time because you're paying interest rather than sharing home appreciation. But Hometap can be the better choice when monthly payments would strain your budget or when you can't qualify for a HELOC.

Is Figure a normal HELOC?

Figure is in the HELOC lane but works differently from a traditional staged-draw HELOC. Figure delivers the full approved amount at closing with payments starting immediately, and offers fixed- or variable-rate options. That works well for defined ADU budgets but offers less draw flexibility during phased construction.

Does Hometap require monthly payments?

No. Hometap's Home Equity Investment has no monthly payments during the 10-year term. You settle the investment at the end of the term or earlier by selling the home, refinancing, using savings, or taking out a loan to buy out Hometap's share.

How much equity do I need for a HELOC vs. Hometap?

For a HELOC, most lenders require combined loan-to-value below 80-85%. Hometap generally requires at least 25% equity and invests up to 25% of the home's current value, with a maximum of $600,000. Exact requirements vary by provider.

Can I use a HELOC to build a detached ADU?

Yes, if your available borrowing room covers the project budget. Detached ADUs typically cost $150,000 to $300,000 or more, which exceeds standard HELOC capacity for many homeowners. If your current equity falls short, consider a renovation HELOC or construction loan.

Will Hometap take a share of the value my ADU adds?

Hometap's settlement is based on your home's total value at settlement. However, Hometap says some qualified renovations of $25,000 or more may qualify for a renovation adjustment that could exclude ADU-driven value from their share, subject to documentation, appraisal, and approval. Get these terms in writing before signing.

What happens if I want to keep my home longer than 10 years?

With a HELOC, you continue payments until the balance is paid off with no forced timeline beyond the loan terms. With Hometap, the 10-year term means you must settle the investment. If you cannot repay the settlement amount, you may have to sell the home or face foreclosure risk.

Can I refinance after using Hometap?

You can, but it may be complicated. Hometap holds a lien on your property, and the CFPB has noted that homeowners may face difficulty refinancing with an active home equity contract.

Is HELOC interest tax-deductible for ADU construction?

If the HELOC funds are used to build or substantially improve the home securing the loan, the interest may be tax-deductible under current IRS rules, subject to overall limits. Hometap settlements have different and more complex tax implications. Consult a qualified tax professional. (Source: IRS Publication 936)

What if I don't qualify for either option?

A renovation HELOC like RenoFi lends based on after-renovation value. Construction loans are designed for ground-up builds. Fannie Mae HomeStyle and Freddie Mac CHOICERenovation mortgages can also finance ADU projects.

Is Hometap available in my state?

As of April 2026, Hometap says it is making investments in 16 states: Arizona, California, Florida, Indiana, Michigan, Minnesota, Missouri, Nevada, New Jersey, New York, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia. Availability can change, so confirm directly with Hometap before applying.

Should I use Hometap or a HELOC for an aging-parent ADU?

If monthly payments would add financial stress to caregiving, Hometap's no-payment structure may serve you better even at higher total cost. If you can comfortably carry a HELOC payment, the HELOC will cost less and let you keep all the appreciation. The right answer depends on your cash flow, not the ADU's purpose.

Not sure where to start?

See what's possible at your address — zoning, lot eligibility, ADU types, and estimated costs for your specific property.

Get Your Free ADU ReportWant a head start on planning?

Download the free 2026 ADU Starter Kit — financing comparison worksheets, permit checklists, and cost-planning tools delivered to your inbox.

Download the Free 2026 ADU Starter KitLast verified: April 2026. If you notice anything on this page that needs updating, contact our editorial team.