Mortgage Research Center ADU Financing Review: When VA Cash-Out Fits — and When It Doesn’t

By The Dwelling Index Editorial Team · · Last verified: May 25, 2026

Bottom line up front: This Mortgage Research Center ADU financing review has one blunt answer: the path is real but indirect — there is no dedicated “ADU loan” product. Mortgage Research Center, LLC is the licensed entity behind Veterans United Home Loans (NMLS #1907), the nation’s #1 VA purchase lender — not a standalone ADU lender. For an accessory dwelling unit (ADU — a secondary home on the same lot as your main house), the path that actually fits is the VA Cash-Out refinance, which Veterans United offers directly and whose proceeds can fund construction. Everything else — a HELOC, a construction loan, a VA renovation loan — is either referred out, not offered, or blocked by a hard legal limit in Texas. Most borrowers will need to compare this against a second lane before deciding.

Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. We are not a lender, broker, builder, tax advisor, or law firm, and this page is educational — it does not guarantee approval, rates, monthly payments, loan terms, rental income, or property values.

The short answer

There is no dedicated “ADU loan” product at Mortgage Research Center. ADU financing is a use case, not a single product. The VA Cash-Out refinance is the one ADU-relevant product Veterans United offers directly — you replace your existing mortgage with a larger VA loan and receive the difference as cash spendable on construction. VA rules can allow up to 100% loan-to-value (LTV), though most lenders cap it around 90%.

The damaging admission, up front: Mortgage Research Center is not the right first move for every ADU. If you need construction draws, want to protect a 3% first mortgage, or need a lender that will count your future ADU rent, the fit matrix below should send you elsewhere — and we’d rather tell you that now than after you’ve filled out three forms.

Free property check

See what you can build → Get your free ADU report

Before you pick a loan, check the build. Financing can’t fix a lot that won’t pass zoning. See what type and size of ADU your property may support first. Free, takes about 60 seconds.

Check my property for free →Should you use Mortgage Research Center for your ADU? (Start here)

Whether Mortgage Research Center fits your ADU comes down to one thing: your financing constraint, not the brand. It’s a strong path to compare for VA-eligible homeowners weighing a cash-out refinance, a weak direct fit for HELOC-only or construction-draw borrowers, and the wrong first click if your real problem is permits, zoning, or protecting a low mortgage rate. The table below is the fastest way to find your row.

We built this matrix by cross-referencing Veterans United’s own published product pages against the financing realities of ADU construction and federal agency rules. You won’t find this exact assembly anywhere else — most “ADU loan” articles list every loan type generically without telling you what this lender actually offers.

| Your situation | MRC / Veterans United fit | Why | Where to start if not MRC |

|---|---|---|---|

| VA-eligible, current mortgage rate near or above today's market, need a lump sum to build | ✅ Strong fit to compare | Veterans United offers VA Cash-Out refinances directly. VA rules can allow up to 100% LTV; most lenders cap it at 90%. | Compare against a home equity loan and HELOC before committing. |

| VA-eligible but holding a very low first mortgage (e.g., a sub-4% pandemic-era rate) | ⚠️ Conditional / risky | A cash-out refinance replaces your entire first mortgage at today's rate — you could surrender a great rate on your whole balance to access a smaller amount. | A HELOC or home equity loan, which sit behind your existing mortgage and leave its rate intact. |

| You want a HELOC or home equity loan specifically | 🔁 Indirect fit | Veterans United states it doesn't offer HELOCs or home equity loans directly, but can refer you to a partner. | A bank, credit union, or HELOC lender that underwrites the product directly. |

| You need a lender to fund construction in draws | ⚠️ Weak direct fit | Veterans United generally doesn't fund the construction itself; the VA-friendly path is to refinance into permanent VA financing after the build is complete. | A construction-to-permanent lender, local bank, or builder financing. |

| You want a VA renovation/rehab loan for the ADU | ❌ Poor fit | Veterans United doesn't provide VA renovation loans and points borrowers to non-VA options. VA renovation loans also generally can't build a detached ADU. | FHA 203(k), Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or a local renovation lender. |

| You want future ADU rent to help you qualify | ❓ Ask before applying | Agency rules differ sharply — Fannie Mae caps qualifying ADU rent at 30% of income on eligible transactions; FHA allows it but not on cash-out refinances. | A lender that explicitly underwrites ADU rental income under the right program. |

| You're a Texas homestead owner wanting a VA cash-out for an ADU | 🚫 Not available | The VA's loan guaranty counts as prohibited "additional collateral" under the Texas Constitution, so a VA cash-out can't be done on a Texas homestead. | A Texas Section 50(a)(6) conventional cash-out (80% LTV cap) or a HELOC. |

Sources: Veterans United VA Cash-Out; Veterans United home equity referral; Texas AG Opinion KP-0183; HUD ML 2023-17. Verified May 2026.

Affiliate disclosure: This comparison includes a financing partner (Mortgage Research Center / Veterans United) we may be compensated by. We sort by fit, never by payout, and we point you elsewhere wherever the honest answer points there.

Is Mortgage Research Center a lender, a lead form, or Veterans United?

All three labels point to the same family, but they’re not interchangeable: Mortgage Research Center, LLC is the licensed legal entity (NMLS #1907), Veterans United Home Loans is its consumer-facing VA lending brand, and “Mortgage Research Center” also runs a lead-technology operation — so the form you land on matters. Knowing which one you’re using tells you whether you’re talking to a direct lender or a referral route.

- •Mortgage Research Center, LLC — The licensed mortgage entity; the name you see on disclosures and regulatory filings, operating under NMLS #1907.

- •Veterans United Home Loans — The direct-to-consumer VA mortgage brand, headquartered in Columbia, Missouri, and the consumer face most borrowers actually deal with.

- •The lead-technology side — Mortgage Research Center's own corporate site describes real-time mortgage lead delivery, lead validation, a client portal, and licensed lead sales across all 50 states. That means some "Mortgage Research Center" forms are lead-generation experiences, not a direct loan application.

None of this is a red flag — it’s a large, legitimate mortgage company with multiple arms. But the single highest-friction question for anyone who typed this lender’s name into a search bar is: before you submit personal financial details, confirm whether the form is a direct Veterans United lending path or an MRC-branded lead form that routes you to a partner.

What is Mortgage Research Center, and is it legitimate?

Yes — Mortgage Research Center is a real, licensed mortgage company and the parent entity of the nation’s #1 VA purchase lender. Legitimacy, though, is a separate question from whether it fits your ADU. Veterans United reports licensing in all 50 states and displays a 4.8 out of 5 customer rating across 463,707 reviews on its own site (checked May 25, 2026) [Veterans United]. Treat that as service-experience context — not proof that a VA cash-out is right for your backyard build.

What to verify before you submit any information

Before sharing financial details with any lender — Mortgage Research Center included — confirm five things: the NMLS number, your state’s availability, the exact product, whether the link is direct or a referral, and whether the loan officer understands ADU construction. This five-point check takes minutes and heads off the most common ADU financing dead ends.

- NMLS #1907 — verify the license at nmlsconsumeraccess.org.

- State availability — confirm the product is offered in your state (especially Texas, where VA cash-out is barred).

- Direct vs. referral — ask whether the product is offered directly or through a partner.

- Product clarity — make sure it’s a VA Cash-Out refinance, not a HELOC or renovation loan you’d actually need elsewhere.

- ADU literacy — ask whether the loan officer has handled ADU projects: permits, after-improved appraisal value, construction timing, and rental income.

Does Mortgage Research Center offer ADU loans?

No — neither Mortgage Research Center nor Veterans United sells a dedicated “ADU loan.” ADU financing is a use case, not a single product. What’s available here to fund an ADU is the VA Cash-Out refinance, where the cash can be spent on construction. Everything else an ADU might need — a HELOC, a draw-based construction loan, a VA renovation loan — is either referred out or not offered.

This is where most of the internet gets sloppy. A surprising number of lender pages blur “you can buy a home that already has an ADU with a VA loan” together with “you can build an ADU with a VA loan.” Those are completely different transactions. Buying a property with a permitted ADU already on it is straightforward VA purchase territory. Building a new one on land you own is a financing problem the VA program solves mainly through one door: the cash-out refinance.

Why “financing an ADU” is a use case, not a product

Several loans can technically fund an ADU, but each works differently, and the lender underwrites you and the property regardless of the “ADU” label. A cash-out refinance gives you a lump sum. A HELOC gives you a revolving line you draw as costs hit. A construction loan releases funds in draws against completed work. A renovation loan can lend against the home’s after-improved value.

The point: the words “ADU loan” on a marketing page don’t mean a special, easier product exists. The type of loan you choose determines whether you get money upfront, in stages, or against future value — and that choice is the whole game.

Why this distinction matters financially

Don’t assume a “home improvement loan” means easy ADU approval — improvement lending carries materially higher denial rates than purchase or cash-out lending. The Urban Institute, analyzing 2022 HMDA (Home Mortgage Disclosure Act) data, reported a 35.4% denial rate for home improvement loans — higher than for cash-out refinance or purchase loans [Urban Institute, 2024].

That one statistic reframes the whole decision. It’s why matching your situation to the right lane — rather than clicking the first “ADU loan” link you see — is the highest-leverage move you can make. The same analysis found that among homeowners who used mortgage products to finance an ADU, roughly 56% used a home equity loan or HELOC, 35% used cash-out refinancing, and only about 6% used construction or renovation financing [Urban Institute, 2024] — a strong signal that equity-based paths dominate real ADU financing.

Find your lane first

Before you pick a loan, check the build

Financing can’t fix a lot that won’t pass zoning. See what type and size of ADU your property may support before you spend a dollar on financing.

Get my free ADU report →What a VA Cash-Out refinance for an ADU actually costs

A VA Cash-Out refinance replaces your existing mortgage with a new, larger VA loan and hands you the difference as cash you can spend on an ADU — VA rules can allow up to 100% LTV, though most lenders cap it around 90%, and the VA charges a one-time funding fee of 2.15% (first use) or 3.3% (subsequent use). That funding fee is the defining cost, and it’s waived for veterans receiving VA disability compensation.

Let’s work a real example so the math is concrete. These are illustrative figures, not an offer or a quote.

Worked example — $700,000 home, $400,000 existing balance:

| Line | Amount | Note |

|---|---|---|

| Home value | $700,000 | Illustrative |

| Illustrative 90% LTV ceiling | $630,000 | Based on Veterans United's statement that most lenders cap VA cash-out at 90% |

| Existing mortgage paid off | –$400,000 | |

| Gross cash available before costs | $230,000 | |

| VA funding fee, first use (2.15% of $630,000) | ≈ –$13,545 | Often rolled into the loan; waived with disability compensation |

| Estimated closing costs (≈3%–5% of loan) | ≈ –$18,900 to –$31,500 | Typical VA cash-out range |

| Net cash toward your ADU | ≈ $185,000–$197,000 | Before any lender-specific items |

These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, appraisal, underwriting, and regulatory approvals. Typical ADU build cost: ~$100,000–$300,000 nationally; ~$150,000 median (~$250/sq ft) in California survey data [RenoFi; Terner Center/USC, verified May 2026].

The VA funding fee, decoded

The VA funding fee is a one-time charge that keeps the VA loan program self-sustaining; on a cash-out refinance it’s 2.15% for first-time benefit use and 3.3% for subsequent use, and unlike a purchase loan, it does not drop based on your equity [VA.gov]. You can pay it at closing or roll it into the loan.

| Funding fee scenario (VA cash-out refinance, 2026) | Rate |

|---|---|

| First use of VA benefit | 2.15% |

| Subsequent use | 3.3% |

| Borrower receiving VA compensation for a service-connected disability | $0 — exempt |

| Surviving spouse receiving Dependency and Indemnity Compensation (DIC) | $0 — exempt |

| Active-duty service member with Purple Heart evidence on or before closing | $0 — exempt |

Source: VA.gov funding fee page. The exemption also reaches borrowers who are eligible to receive VA compensation but receive retirement or active-duty pay instead, and those with a proposed or memorandum rating before closing.

The honest tradeoff: the rate-reset trap

The biggest risk of a VA Cash-Out refinance for an ADU is that it replaces your entire mortgage at today’s rate — if you hold a low pandemic-era rate, the cost of refinancing the whole balance can dwarf the value of the cash you pull out. This is the objection that should stop some readers cold, and we’d rather you hear it from us than discover it at closing.

Say you owe $400,000 at 3.25% and want $150,000 for an ADU. A cash-out refinance doesn’t just put a higher rate on the new $150,000 — it puts today’s rate on all $550,000+. For many homeowners with a sub-4% loan, a HELOC or home equity loan (which sits behind the existing mortgage and leaves its rate alone) is the smarter structure, even at a higher second-lien rate, because you only pay that rate on the ADU portion. Veterans United doesn’t offer those second-lien products directly, which is one honest reason the MRC path isn’t always the right first click.

VA Cash-Out refinances also require a “net tangible benefit” — a clear, measurable financial improvement — and VA-to-VA cash-outs are subject to recoupment rules [Veterans United]. Translation: the loan has to genuinely help you, and your lender must document why.

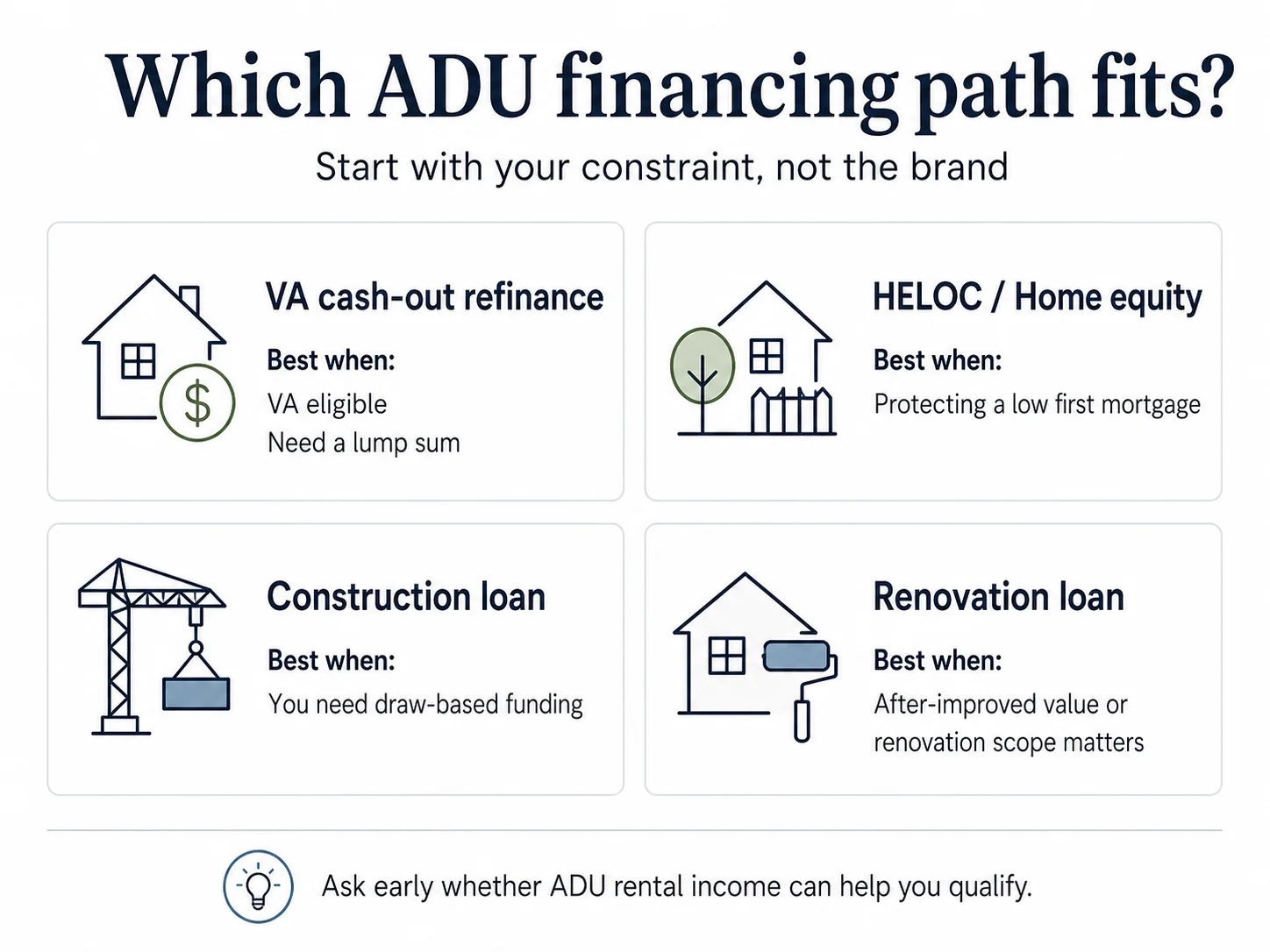

Which ADU financing paths fit Mortgage Research Center — and which don’t?

Mortgage Research Center fits the VA Cash-Out lane directly and refers out almost everything else — so it’s a strong comparison stop for VA-eligible homeowners and a weak one for HELOC-only, construction-draw, or renovation borrowers. Here’s each path, what Veterans United actually does with it, and where to go if it’s not a fit.

VA Cash-Out refinance for an ADU (the strongest fit)

This is the one ADU-relevant product Veterans United offers directly, and it’s the best fit for a VA-eligible homeowner with equity whose current mortgage rate isn’t worth protecting. You get a lump sum upfront, a single payment, and VA-backed terms — at the cost of the funding fee and replacing your existing loan.

Best when: you’re VA-eligible, you have equity, your current rate is near market, and your build needs money in one shot rather than in draws. Watch for: the funding fee, closing costs, the rate-reset risk, occupancy requirements, and state restrictions (Texas, below). See our guide on cash-out refinance for an ADU.

HELOC or home equity loan for an ADU (referred out)

A HELOC (home equity line of credit — a revolving credit line secured by your equity) or a home equity loan is often the best fit when you want to preserve a low first mortgage, but Veterans United doesn’t offer either directly. It states it can connect you with a trusted partner instead [Veterans United].

Because these are second liens that sit behind your existing mortgage, they leave your current rate untouched — exactly what you want if you’re protecting a sub-4% loan. The VA itself doesn’t guarantee HELOCs or home equity loans (it backs only first-lien mortgages), so any veteran pursuing this uses a conventional product from a private lender. See our guides on home equity loans for an ADU and HELOC vs. construction loan for an ADU.

Construction loan for an ADU (weak direct fit)

ADU construction usually needs a loan that releases funds in draws as work is completed, and Veterans United generally doesn’t fund the construction itself — the VA-friendly play is to refinance into permanent VA financing after the build is done [Veterans United]. So if you need a true draw-based construction loan, this isn’t the direct path. A construction-to-permanent loan from a local bank, credit union, or specialized lender handles the build phase; a VA loan can then take out that financing once the ADU is complete. See construction-to-permanent loan for an ADU.

VA renovation/rehab loan for an ADU (poor fit, with a hard limit)

Veterans United doesn’t offer VA renovation loans, and even where available, a VA renovation loan generally can’t build a detached ADU — it’s tied to the primary residence and to work that brings a home up to standard. Veterans United doesn’t offer VA renovation loans and lists strict limits on the program [Veterans United], and Chase states plainly that VA renovation loans “can’t be used to build an accessory dwelling unit (ADU) that isn’t connected to the main residence” [Chase, verified May 2026]. For renovation-style ADU financing, look to FHA 203(k), Fannie Mae HomeStyle, or Freddie Mac CHOICERenovation. See VA loan rules for ADUs and HomeStyle Renovation loan for ADUs.

How the four agencies handle ADUs (2026 comparison)

When your plan depends on after-improved value or on counting ADU rent, conventional and FHA programs frequently beat the VA path — and the differences between agencies are decisive.

| Program | Counts ADU rent to qualify? | Detached ADU build? | Cash-out allowed? | Notes |

|---|---|---|---|---|

| VA (via Veterans United) | Underwriting-dependent; not the program's strength | Not via VA reno; build then refinance | ✅ Yes (cash spendable on ADU) | Funding fee 2.15%/3.3%; Texas homestead prohibited |

| Fannie Mae | ✅ Yes — capped at 30% of qualifying income, one-unit principal residence, one ADU, purchase or limited cash-out | ✅ via HomeStyle Renovation | Limited cash-out for rent-qualifying | 2026 UAD 3.6 update allows up to 3 ADUs on one-unit properties |

| FHA | ✅ Yes (incl. projected rent), capped at 30% of effective income | ✅ via 203(k) | ❌ ADU rent cannot be used to qualify a cash-out | 203(k) can add/convert/renovate an ADU |

| Freddie Mac | ✅ Yes, for eligible borrowers | ✅ via CHOICERenovation | Program-dependent | ADU must be legally permissible or legal non-conforming |

Sources: Fannie Mae Selling Guide & UAD 3.6 Policy Supplement (2026); HUD Mortgagee Letter 2023-17; Freddie Mac Seller/Servicer Guide. Verified May 2026. A key 2026 update: Fannie Mae expanded ADU eligibility effective March 31, 2026 (UAD 3.6), now allowing up to three ADUs on a one-unit property — though qualifying rental income is still limited to one ADU and capped at 30% of income. See ADU loan requirements.

When should you not use Mortgage Research Center first?

Skip Mortgage Research Center as your first move if your real obstacle is local ADU eligibility, permit feasibility, a draw-based construction loan, protecting a very low mortgage rate, qualifying on future ADU rent, or a Texas homestead — start with the constraint, not the lender. Naming the constraint first is what keeps you out of the wrong loan.

You have a low first mortgage rate

If you hold a sub-4% mortgage, a cash-out refinance that resets your entire balance to today’s rate is usually the wrong tool — a HELOC or home equity loan preserves your rate and only charges the higher rate on the ADU portion. Route yourself to second-lien (home equity) options. See home equity loan for an ADU.

You need future ADU rent to qualify

Whether a lender will count your future ADU rent depends entirely on the program and transaction — ask the precise question before assuming. The right question to a loan officer: “Will you count proposed ADU rent, existing ADU rent, neither, or only on certain transactions — and under which agency program?” Fannie Mae caps it at 30% of qualifying income on purchase or limited cash-out; FHA allows it but not on a cash-out refinance; Freddie Mac differs again. Lender overlays (a lender’s own stricter rules layered on agency rules) can tighten it further.

Your ADU isn’t permit-legal yet

Financing can’t fix zoning or permit ineligibility — if you don’t yet know whether your lot qualifies, start with feasibility, not a loan application. A loan estimate is meaningless if the city won’t approve the unit. Confirm setbacks (the minimum distance a structure must sit from a property line), size limits, owner-occupancy rules, and utility connections first.

Start here

Stop guessing about your lot

We’ll show what your address may support before you spend a dollar on financing.

Get my free ADU report →You’re building in Texas

If your ADU is on a Texas homestead and you’re a veteran, a VA Cash-Out refinance is off the table — Texas law prohibits it — so plan around a Texas Section 50(a)(6) conventional cash-out or a HELOC instead. This is a verified legal limit, decoded in the next section. See VA loan rules for ADUs.

What if you’re not VA-eligible?

If you’re not a veteran, service member, or eligible surviving spouse, Mortgage Research Center’s direct ADU fit is weak — its strength is the VA lane — so compare conventional and FHA paths instead. Look at conventional renovation loans, FHA 203(k), Freddie Mac CHOICERenovation, a HELOC or home equity loan, or a construction-to-permanent loan, and confirm whether any MRC-branded route is a direct product or a partner referral. See compare all ADU financing paths.

The Texas exception: why veterans can’t do a VA cash-out there

Texas is the one state where a VA Cash-Out refinance on your homestead is flatly prohibited — Texas Attorney General Opinion KP-0183 (2018) holds that the VA’s loan guaranty counts as “additional collateral,” which the Texas Constitution forbids on a home-equity loan. If you’re a Texas veteran planning to fund an ADU, this changes your entire plan.

Here’s the rule decoded. Texas Constitution Article XVI, Section 50(a)(6)(H) says a homestead home-equity loan can be secured only by the homestead — no extra collateral, no guarantees. A VA loan, by definition, comes with a federal guaranty (the VA backs a percentage of the loan). The Texas Attorney General concluded that this guaranty is exactly the “additional collateral” the constitution prohibits, so a VA cash-out refinance can’t legally be done on a Texas homestead — even if you’d stay under the loan-to-value cap [Texas Attorney General Opinion KP-0183; Texas Constitution Art. XVI §50(a)(6)(H), verified May 2026].

What Texas veterans use instead:

- A Texas Section 50(a)(6) conventional cash-out, capped at 80% of the home’s appraised value (versus the 90%–100% available on a VA cash-out elsewhere).

- A HELOC or home equity loan from a private lender, which preserves the existing first mortgage.

- A VA IRRRL (Interest Rate Reduction Refinance Loan — a streamline refinance) if you only need a better rate, not cash.

The practical upshot: a Texas homestead ADU build leans on conventional equity products, and you’ll want a lender — and, where appropriate, counsel — who handle Texas 50(a)(6) loans correctly.

How to compare Mortgage Research Center against HELOCs, cash-out refis, renovation, and construction loans

Compare by your constraint, not by brand: decide first whether you must protect an existing mortgage, need funds in draws, need to borrow against after-improved value, need ADU rent to qualify, or want no monthly payment — then Mortgage Research Center becomes one lane in that comparison, not the whole decision. This table turns the choice into a lookup.

| Your constraint | Best first lane | Is MRC / Veterans United relevant? | What to ask |

|---|---|---|---|

| Preserve a low first mortgage | HELOC or home equity loan | Indirect (refers out) | "Can you connect me to a HELOC partner, or should I go direct?" |

| Need more than your current equity | Renovation or construction loan | Weak direct fit | "Do you fund construction, or only refinance after completion?" |

| VA-eligible, current rate not worth protecting | VA Cash-Out refinance | ✅ Strong direct fit | "What's my funding fee, LTV cap, and net cash after costs?" |

| Need future ADU rent counted | Agency-specific lender (FHA/Fannie/Freddie) | Ask first | "Will you count proposed vs. existing ADU rent, under which program?" |

| Want no monthly payment | Home equity investment or deferred/grant programs | Not a fit | "Is there a no-monthly-payment equity product available in my state?" |

| Investor / non-owner-occupied property | DSCR or commercial path | Not a fit (VA is owner-occupied) | "What occupancy does this product require?" |

The five questions to ask any Mortgage Research Center / Veterans United loan officer

Before you commit, get clear answers to five questions that expose whether the product actually matches your ADU project.

- Do you offer this product directly, or are you referring me to a partner?

- Will this loan use my home’s current value or its after-renovation value?

- Will funds come as a lump sum at closing or in construction draws?

- Can you count ADU rental income to help me qualify — and under which agency program?

- What happens to my approval if permits, appraisal, or contractor bids change?

If those answers don’t line up with what your build needs — draws you don’t get, rent that won’t count, after-value you can’t use — that’s your signal to compare another lane.

What do reviews and complaints say — and how much should they matter for your ADU?

Lender reviews tell you about customer service, not whether a loan fits your ADU — use reviews for process expectations, official product pages for what’s actually offered, and regulatory records for due diligence. Don’t let a strong service reputation convince you a product exists that doesn’t.

Veterans United maintains a large, public customer review section — a 4.8 out of 5 rating across 463,707 reviews on its own site as of May 25, 2026 [Veterans United] — and is consistently rated highly for service among VA borrowers. That’s useful context for how a transaction tends to feel: responsiveness, communication, closing experience. It says nothing about whether a VA Cash-Out refinance is the right structure for your backyard cottage. We’re deliberately not attaching our own star rating to this review, because we don’t run a verified first-party review program for ADU outcomes, and inventing one would mislead you.

Doing your own due diligence

Run three standard checks before trusting any lender with your financial information. Here’s what each one does and doesn’t tell you:

| Check | What it proves | What it does not prove |

|---|---|---|

| NMLS #1907 (nmlsconsumeraccess.org) | License status and entity identity | That an ADU loan will be approved |

| CFPB Consumer Complaint Database (consumerfinance.gov) | Complaint patterns and how they were resolved | Pricing or your odds of approval |

| Your state mortgage regulator | State-level records and any actions | Day-to-day product availability |

Read public regulatory records as due-diligence context, not a verdict — large lenders accumulate records simply by volume.

What you can’t conclude from reviews

Reviews can’t tell you a lender is “best” or “cheapest,” or that your ADU loan will be approved — those depend on your numbers and your property, not on other borrowers’ experiences. Read reviews to set service expectations. Read product pages and agency rules to learn what’s possible. Run your own due diligence to confirm legitimacy. Then decide on fit.

The Mortgage Research Center ADU Financing Fit Checker

The fastest way to avoid the wrong loan is to identify your financing constraint before you talk to a lender — our free feasibility report does exactly that, using your address to point you to the most likely path.

Possible outcomes include:

- →MRC strong fit — proceed to compare a VA Cash-Out refinance.

- →MRC comparison fit — worth a quote alongside other lanes.

- →MRC weak direct fit — your need (draws, HELOC, renovation) points elsewhere.

- →Start with feasibility — permits and zoning come before financing.

- →Start with a construction lender — your build needs draws.

- →Start with HELOC / home equity — protect that low rate.

- →Start with a no-payment / deferred path — explore equity products that don't add a monthly bill.

Free in 60 seconds

Get your routing in two minutes

See what your address may support — and which financing lane fits your situation — before you talk to any lender.

Use the free ADU Feasibility Report →Mortgage Research Center ADU financing review: should you use it?

Use Mortgage Research Center / Veterans United as a comparison path when you’re a VA-eligible homeowner weighing a cash-out refinance and your current rate is near market — and start elsewhere for HELOCs, construction draws, VA renovation loans, low-rate protection, rent-dependent qualifying, or a Texas homestead. It’s a legitimate, capable VA lender; it is not a universal ADU solution, and it doesn’t pretend to be.

Best fit

VA-eligible homeowner doing a cash-out refinance, not protecting a low first mortgage, with enough equity for the build.

Possible fit

Homeowner comparing broad mortgage-backed paths who wants a VA quote in the mix.

Weak fit

HELOC-only shopper, true construction-draw borrower, VA renovation seeker, or anyone wanting no monthly payment.

Start elsewhere

Permit or zoning uncertainty, Texas VA cash-out, financing that hinges on future ADU rent, or non-VA-eligible borrowers.

The honest theme of this entire review: the most expensive ADU mistake isn’t choosing the “wrong” lender — it’s choosing the wrong loan structure for your rate and your build. Get the structure right, and a VA Cash-Out refinance through Mortgage Research Center can be a clean, single-payment way to fund a backyard unit. Get it wrong, and you could trade a great mortgage rate for cash you could have borrowed more cheaply.

Primary — free property check

See what’s possible at your address → Get your free ADU report

Get my free ADU report →Tertiary — free starter kit

Download the free ADU Starter Kit

Get the checklist, budget worksheet, and the five questions to bring to any lender.

Download the ADU Starter Kit →What we verified (May 25, 2026)

We confirmed the load-bearing facts in this review against primary and official sources:

- ✓Mortgage Research Center, LLC is the entity behind Veterans United Home Loans, NMLS #1907 — a private lender not affiliated with the VA, licensed in all 50 states, showing a 4.8/5 rating across 463,707 reviews on its site — Veterans United.

- ✓Mortgage Research Center also operates a lead-technology business — with real-time lead delivery and licensed lead sales in all 50 states — mortgageresearchcenter.org.

- ✓Veterans United offers VA Cash-Out refinances directly; VA rules can allow up to 100% LTV, most lenders cap at 90% — Veterans United.

- ✓Veterans United does not offer HELOCs or home equity loans directly — and refers borrowers to a partner — Veterans United.

- ✓Veterans United generally does not fund construction directly — and refinances into permanent VA financing after completion — Veterans United.

- ✓Veterans United does not provide VA renovation loans; VA renovation loans generally can't build a detached ADU — Veterans United; Chase.

- ✓VA Cash-Out funding fee: 2.15% first use / 3.3% subsequent use; exempt with disability compensation and other categories — VA.gov.

- ✓Texas prohibits VA cash-out refinances on a homestead — Texas AG Opinion KP-0183; Texas Constitution Art. XVI §50(a)(6)(H).

- ✓Fannie Mae caps qualifying ADU rent at 30% of income; 2026 UAD 3.6 update expands ADU eligibility to up to three ADUs on one-unit properties — Fannie Mae Selling Guide & UAD 3.6 Policy Supplement.

- ✓FHA allows ADU rental income to qualify (capped at 30% of effective income) but not on cash-out refinances; 203(k) can add or renovate an ADU — HUD Mortgagee Letter 2023-17.

- ✓Home improvement loans had a 35.4% denial rate (2022 HMDA); equity products dominate real ADU financing — Urban Institute (2024).

- ✓Typical ADU build cost: ~$100,000–$300,000 nationally; ~$150,000 median (~$250/sq ft) in California survey data — RenoFi; Terner Center/USC.

Items that go stale — funding fees, LTV caps, state availability, and agency rules — are re-verified on the cadence in our methodology.

Methodology

This review was produced by the Dwelling Index Editorial Team, an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, builder, tax advisor, or law firm. To build it, we reviewed official Mortgage Research Center and Veterans United product pages; primary regulatory and legal sources (the U.S. Department of Veterans Affairs, the Texas Attorney General, the Texas Constitution); federal agency guides (Fannie Mae, Freddie Mac, HUD/FHA); independent housing research (Urban Institute, Terner Center/USC); and homeowner discussion threads used only for voice-of-customer language and objections — never as proof for laws, costs, or loan rules.

We do not rank lenders by compensation, quote rates or payments as guarantees, or use schema for content not visible on this page. Our financing guidance presents lanes, not “best lender” rankings, sorted by fit. We re-verify license status and partner availability monthly; VA fees, LTV caps, occupancy, and agency rental-income rules quarterly or on any rule change; and cost ranges semi-annually. This page is educational and is not financial, legal, tax, lending, or construction advice.

Last updated: May 25, 2026 · Last verified: May 25, 2026.

Frequently asked questions

- Is Mortgage Research Center the same as Veterans United?

- Effectively yes. Mortgage Research Center, LLC is the legal/licensing entity (NMLS #1907) and Veterans United Home Loans is its consumer-facing VA mortgage brand. The same parent also runs a mortgage lead-technology business, so confirm whether a given form is a direct lending path or a lead route.

- Is Mortgage Research Center legitimate?

- Yes — it's a real, licensed mortgage company and the parent of the nation's #1 VA purchase lender. Legitimacy is separate from fit. Verify NMLS #1907, your state's availability, and whether your link is direct or a referral before applying.

- Does Mortgage Research Center offer ADU loans?

- Not as a dedicated product. ADU financing is a use case. The relevant path here is a VA Cash-Out refinance, which Veterans United offers directly; the cash can fund construction.

- Can you use a VA loan to build an ADU?

- Generally not via a VA construction or renovation loan for a detached unit — those are tied to the primary residence. The realistic VA path is a cash-out refinance to fund the build, or refinancing into VA financing after a separate construction loan completes.

- Does Veterans United offer HELOCs for ADUs?

- No. Veterans United states it doesn't offer HELOCs or home equity loans directly, but can connect you with a partner. The VA itself doesn't guarantee HELOCs.

- Does Veterans United offer construction loans for ADUs?

- Generally not directly. It typically doesn't fund the construction phase but may refinance a completed build into permanent VA financing.

- Does the VA funding fee apply to a cash-out refinance for an ADU?

- Yes — 2.15% for first use of the benefit and 3.3% for subsequent use, on the new loan amount. It's waived for veterans receiving VA compensation for a service-connected disability, among other exempt categories.

- Should I use a VA cash-out refinance if I have a low mortgage rate?

- Be careful. A cash-out refinance replaces your entire first mortgage at today's rate. If you're protecting a sub-4% loan, a HELOC or home equity loan that leaves your first mortgage in place is often cheaper.

- Can future ADU rent help me qualify?

- Sometimes, and it's program-specific. Fannie Mae caps qualifying ADU rent at 30% of income on purchase or limited cash-out; FHA allows it but not on a cash-out refinance; Freddie Mac differs. Ask your lender exactly which rule applies.

- Can I do a VA cash-out refinance for an ADU in Texas?

- No. Texas Attorney General Opinion KP-0183 holds that the VA's guaranty is prohibited "additional collateral" under the Texas Constitution, so VA cash-out refinances aren't allowed on a Texas homestead. Texas veterans use a conventional Section 50(a)(6) cash-out (80% LTV cap) or a HELOC.

- What if I'm not a veteran — can I still use Mortgage Research Center?

- Its strength is the VA lane, so the direct ADU fit is weaker for non-veterans. Compare conventional renovation loans, FHA 203(k), Freddie Mac CHOICERenovation, a HELOC or home equity loan, or a construction-to-permanent loan instead.

- Is Mortgage Research Center the best ADU financing option?

- There's no single "best." It's one comparison path — strong for VA cash-out, weak for HELOCs, construction draws, and renovation loans. The right path depends on your constraint.

- What should I do before applying?

- Confirm your ADU is buildable on your lot, estimate your budget, identify your financing constraint, and compare loan estimates across at least two lanes.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.