ADU Financing Without Monthly Payments: Should You Use a Home Equity Investment?

The bottom line: ADU financing without monthly payments is possible — usually through a home equity investment (HEI), or for homeowners 62 and older, a reverse mortgage. But “no monthly payments” does not mean free. You’re trading cash-flow relief today for a share of your home’s future value later. The four HEI providers we compare on this page — Hometap, Unlock, Point, and Splitero — each cover different states, and each one treats the value your ADU creates differently. That single detail — whether the provider shares in the new value your ADU adds — can materially change your settlement amount years from now.

This guide breaks down how these products work for ADU builders, which companies serve your state, whether you keep the value your ADU creates, and how to build a real exit plan before you sign anything. If this path isn’t the right fit, we’ll point you to the one that is.

Independent educational resource · Not a lender or broker · State availability verified against official provider documentation · Sources: CFPB, HUD, official provider materials

Affiliate Disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Read our full editorial methodology and affiliate disclosure.

What Are the Main Ways to Finance an ADU Without Monthly Payments?

The real first decision isn’t “which company?” — it’s “which financing structure fits my situation?”

| Financing Path | Monthly Payment? | Keeps Current Mortgage? | Best For | Biggest Catch | Restrictions |

|---|---|---|---|---|---|

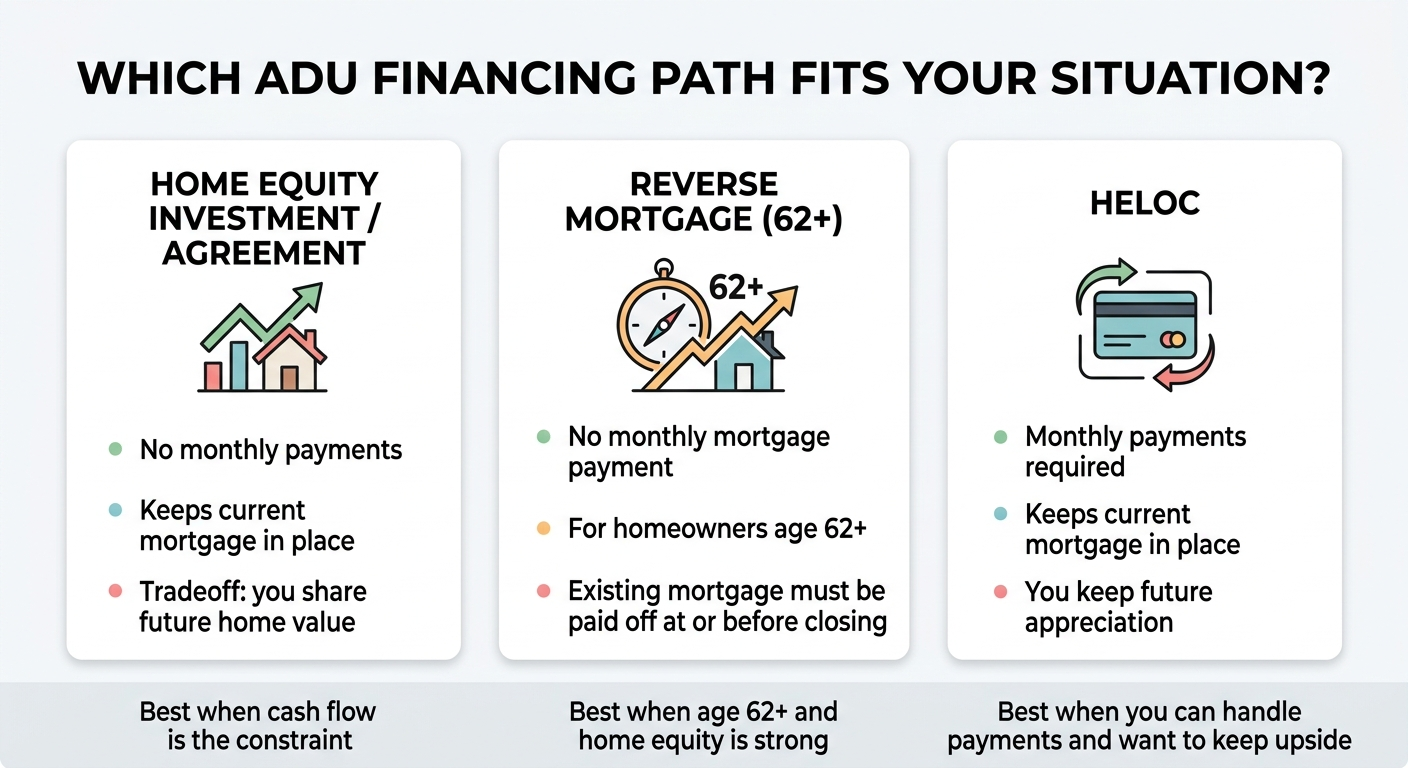

| Home Equity Investment (HEI/HEA) | No payment to HEI company | Yes | Equity-rich homeowners who can't or won't carry a new monthly payment | You share future home appreciation; settlement can be hard to predict | Limited state availability; most require 25–30% equity |

| Reverse Mortgage (HECM) | No monthly mortgage payment | HECM becomes the first mortgage; existing mortgage must be paid off at or before closing | Homeowners 62+ with significant equity | Balance grows over time; reduces inheritance; must stay current on taxes, insurance, and property charges | Age 62+ only; primary residence only; HUD counseling required |

| HELOC | Yes (interest-only during draw, then P+I) | Yes | Homeowners with strong equity and income who want to keep all future appreciation | Monthly payments can be substantial; variable rates | Credit score, DTI, and equity requirements |

| Renovation HELOC | Yes | Yes | Homeowners with low current equity — lends on after-renovation value | Still requires monthly payments; underwriting complexity | Varies by lender; approval based on projected post-ADU value |

| Cash / Savings | No | Yes | Homeowners with liquid assets | Depletes reserves; opportunity cost | Requires significant available capital |

This page focuses on the first two rows — the paths that eliminate monthly payments. If a HELOC or renovation loan turns out to be a better fit for your situation, we’ve written separate guides for those:

Can You Finance an ADU Without Monthly Payments?

Yes — but for most homeowners, the realistic no-monthly-payment path is a home equity investment or home equity agreement. For homeowners 62 and older, a reverse mortgage can also work. Here’s what each path looks like.

The main path: home equity investments and agreements

An HEI gives you a lump sum of cash in exchange for a percentage of your home’s future value. There are no required monthly payments to the HEI company during the term. You continue paying your existing mortgage, property taxes, insurance, and maintenance like normal. When the term ends (usually 10 to 30 years), or when you sell or refinance, you settle the agreement by paying back the company’s share based on your home’s appraised value at that point.

An important distinction: HEI providers typically market these as alternatives to traditional monthly-payment financing — not loans. But they are still home-secured financial contracts. A lien is placed on your property, and you have a real future settlement obligation. The CFPB has noted that the legal classification of these products is still evolving, and consumers should compare them carefully against other home-secured options before signing. (Source: CFPB Issue Spotlight — Home Equity Contracts, 2024)

The providers we compare on this page — Hometap, Unlock, Point, and Splitero — each have different terms, different state coverage, and different policies on whether the value created by your new ADU gets shared with the investor or credited back to you.

The 62+ path: reverse mortgage (HECM)

If you’re 62 or older, a Home Equity Conversion Mortgage (HECM) — the FHA-insured version of a reverse mortgage — lets you access home equity without monthly mortgage payments. You can receive funds as a lump sum, line of credit, or monthly disbursement. If you have an existing mortgage, the HECM proceeds must pay it off at or before closing — a HECM must be in first-lien position.

The balance grows over time as interest accrues, and the obligation is typically settled when you sell the home, move out permanently, or pass away. You must remain current on property taxes, homeowner’s insurance, and home maintenance — failure to do so can put the loan in default. Reverse mortgages are federally regulated through HUD and require counseling from a HUD-approved agency before closing. (Source: HUD HECM program guidelines)

Why “no monthly payments” does not mean low cost

We need to say this plainly: a no-monthly-payment structure can still be expensive. In some appreciation scenarios, an HEI can cost more over time than a traditional HELOC or home equity loan.

The CFPB published an issue spotlight on home equity contracts noting that these products can be complex, use non-standardized disclosures, create settlement amounts that are hard to predict, and in many scenarios cost more than other home-secured financing. Consumer complaints have included surprise repayment amounts, difficulty refinancing to exit, appraisal disputes at settlement, and feeling pressured to sell to pay off the agreement. (Source: CFPB Issue Spotlight — Home Equity Contracts, 2024)

That doesn’t make HEIs a bad choice. For the right homeowner — someone who genuinely cannot carry a monthly payment and has a clear exit plan — an HEI can be the only realistic path to building an ADU that changes their life. The point is to understand the tradeoff before you sign. That’s exactly what the rest of this page delivers.

Who Is This Path Actually For?

A home equity investment makes the most sense for a specific kind of homeowner. If you see yourself in the profiles below, this page was written for you. If you don’t, we’ll route you somewhere better.

You have meaningful equity and want to protect your current mortgage.

Maybe you locked in a rate in the 2–3% range during 2020–2021 and the thought of refinancing into today’s rates makes you cringe. An HEI sits behind your existing mortgage as a second-position lien. Your first mortgage stays exactly where it is, rate and all.

You’re building for aging parents or multigenerational housing.

This is one of the most common ADU use cases — and one where cash-flow sensitivity is highest. Your parent may be contributing to household costs, but they’re probably not covering a new monthly loan payment. An HEI lets you build the unit without that monthly burden.

You’re on a fixed income or approaching retirement.

Social Security, a pension, or a modest retirement portfolio may give you plenty of equity but not enough monthly cash flow to qualify for — or comfortably carry — a HELOC. HEI qualification focuses on property equity, not income or debt-to-income ratios.

You’re self-employed or have irregular income.

Traditional lenders want two years of tax returns and consistent W-2 income. If that’s not your reality, HEI qualification — based primarily on home value and equity — can be dramatically simpler.

You’d rather preserve cash flow now than preserve every dollar of future appreciation.

This is the core tradeoff, and it’s worth naming clearly. If your priority is payment freedom today, an HEI delivers it. If your priority is maximizing long-term net worth, a HELOC likely costs less in total — but it comes with monthly obligations.

Does that sound like your situation? Before you solve financing, confirm your property can actually support an ADU.

See what’s possible at your address

Get your free ADU feasibility report in 60 seconds. Check what you can build before you solve financing.

What Is the Biggest Downside of No-Monthly-Payment ADU Financing?

Here’s what we’d want someone to tell us before we signed a home equity agreement for an ADU project.

In appreciation scenarios, a no-monthly-payment structure can cost more than a traditional loan over time.

The HEI company’s share of your home’s future appreciation — their compensation for giving you cash today — can exceed what you’d have paid in HELOC interest over the same period. The CFPB confirms this: home equity contracts are frequently more expensive than other home-secured options when home values rise. (Source: CFPB Issue Spotlight, 2024)

Your settlement amount depends on a future appraisal.

Unlike a loan where you can calculate total cost upfront, HEI payoff depends on your home’s appraised value at settlement — a number neither you nor the company controls today.

Providers treat renovations and improvements differently.

This is the critical point for ADU builders, and we’ll cover it in detail below. Some providers credit you for value you create through improvements. Others share in that value. The difference matters.

You still owe taxes, insurance, and maintenance.

“No monthly payment” refers to the HEI itself. You’re still responsible for property taxes, homeowner’s insurance, and keeping the property in reasonable condition. Failing to do so can trigger default provisions in some agreements.

Without an exit plan, the end of term can arrive fast.

Whether that’s 10 or 30 years from now, you need to settle. That means selling, refinancing, or coming up with cash.

Now — does any of that mean you should avoid this path? Not if you fit the profile above. It means you should go in with a clear plan, which is what the rest of this page equips you to build. For the right homeowner, an HEI is the bridge between “wanting an ADU” and actually having one.

Can handle a monthly payment? A HELOC or renovation loan might be a better fit. Compare all ADU financing paths →

How Does a Home Equity Investment Work for an ADU Project?

Here’s the mechanical walkthrough — what actually happens from application to building your ADU.

- 1

Check eligibility and prequalify.

Most HEI providers offer online prequalification. They’ll estimate how much you could receive based on your home’s estimated value and outstanding mortgage balance. Check each provider’s site for their specific process and credit-check policies.

- 2

Get an offer based on a home appraisal.

If you move forward, the company orders a professional appraisal. Based on that appraised value, they present a formal offer: a specific dollar amount today in exchange for a defined share of your home’s value at settlement. Fees — which vary by provider — are typically deducted from your payout.

- 3

Close and receive funds.

A lien is recorded against your property (typically in second position behind your mortgage). You receive the cash.

- 4

Build your ADU.

Use the funds toward your contractor, permits, design, site work, utility connections — whatever your ADU project requires.

- 5

Settle later.

At some point during the term — when you sell, refinance, or reach the agreement’s maturity date — a new appraisal determines your home’s current value. You pay the company its agreed-upon share. If the home appreciated, they share in that gain. Terms for scenarios where the home loses value vary by provider — review your specific agreement.

Practical tip for ADU builders: Get your ADU design and permits lined up before you apply for HEI funding. The initial appraisal captures your home’s current value — you want to lock that in before the ADU adds value. Once the ADU is built and your home is worth more, you can settle the HEI (through a refinance, for example, using the higher value) or let it ride.

Which Financing Path Is Best for Your ADU: HEI, HELOC, Renovation Financing, or Reverse Mortgage?

The right comparison isn’t “who has the flashiest offer.” It’s which structure actually solves your constraint.

| Feature | HEI / HEA | HELOC | Renovation HELOC | Reverse Mortgage (HECM) |

|---|---|---|---|---|

| Best for | Equity-rich, payment-averse | Strong equity + income, wants to keep appreciation | Low current equity, strong projected post-ADU value | 62+ homeowners with significant equity |

| Monthly payment | None to HEI company | Interest-only during draw, then P+I | Yes | None (balance grows) |

| Keeps first mortgage? | Yes | Yes | Yes | No — HECM must be in first position |

| Current equity needed | 25–30%+ | 15–20%+ | Can be low — lends on projected after-renovation value | Significant (varies by age and home value) |

| State / age restrictions | Limited state availability | Broadly available | Varies by lender | 62+ only; primary residence; HUD counseling required |

| Main risk | Sharing appreciation; hard-to-predict payoff | Payment burden; variable rates | Payment burden; underwriting complexity | Growing balance; reduced inheritance |

| Best exit path | Sell, refinance, or cash buyout | Pay off from savings or refinance | Pay off or refinance | Sell or heir repayment |

Why this matters for ADU builders specifically: The whole financial case for an ADU rests on the value it creates — rental income, property appreciation, or both. A financing method that adds monthly payments reduces the net benefit of rental income. A financing method that shares in appreciation reduces the net benefit of the property value increase. Neither is universally “better.” The right answer depends on whether your constraint is monthly cash flow or future equity preservation.

Sources: CFPB Issue Spotlight — Home Equity Contracts, 2024; HUD HECM program guidelines; individual provider documentation

Which No-Monthly-Payment Providers Serve Your State?

This is the section most pages on this topic skip — and it’s the one that matters most practically. HEI availability is not national. Each provider covers a different set of states, and some only serve select regions within those states.

We verified state coverage from each company’s official eligibility documentation. Coverage can change — always confirm directly with the provider before applying.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure →

HEI Provider Comparison for ADU Financing

Providers listed alphabetically. Dwelling Index does not rank providers by compensation.

| Feature | Hometap | Point | Splitero | Unlock |

|---|---|---|---|---|

| Published State Footprint | 16 states | 27 jurisdictions incl. D.C. | Eligible areas of 14 states | 25 states |

| Term Length | 10 years | Up to 30 years | Tied to senior mortgage (10-yr min, 30-yr max) | 10 years |

| Early Full Buyout | Yes, without penalty | Yes, without penalty | Yes, without penalty | Yes, without penalty |

| Partial Buyback During Term | No | No | No | Yes (unique feature) |

| Improvement Treatment | Qualified renovations of $25K+ may receive a Renovation Adjustment (approval not guaranteed) | Improvements made during agreement are included in the value shared at repayment | Not clearly documented in public materials — verify in writing before signing | Documented Improvement Adjustment — states it does not share in value created by homeowner improvements |

| Published Equity Baseline | At least 25% equity | Home value above $155K; 500+ credit baseline | At least 30% equity; 500 min. credit score | At least 30% equity; min. property value $175K; 500 min. credit score |

| Best Fit for ADU Builders | High funding need; value dashboard for tracking | Longest term; widest state coverage | Mortgage-matched term flexibility | Partial buyback + favorable improvement treatment |

Data sourced from official provider websites, help centers, and eligibility pages. Last verified: April 2026. Terms, availability, and policies change — confirm all details directly with each provider before applying.

The 11-state overlap

Based on current published coverage, all four providers overlap in 11 states: Arizona, California, Florida, Nevada, New Jersey, Ohio, Oregon, Pennsylvania, South Carolina, Utah, and Virginia. If you’re in one of these states, you have the most options to compare. If you’re outside this overlap, Point’s broader footprint may be your primary or only HEI option.

If your state has zero HEI coverage, this path isn’t available — but others are. A renovation HELOC (which lends on after-renovation value), a standard HELOC, or a reverse mortgage (62+) may still work. Compare all ADU financing paths →

Explore no-monthly-payment ADU financing options

Check Hometap

10-year term, 16 states

Check Unlock

Best improvement treatment, 25 states

Check Point

Widest coverage, up to 30 years

Check Splitero

Mortgage-matched term flexibility

Affiliate links. See full disclosure. Providers listed alphabetically. Rankings not influenced by compensation.

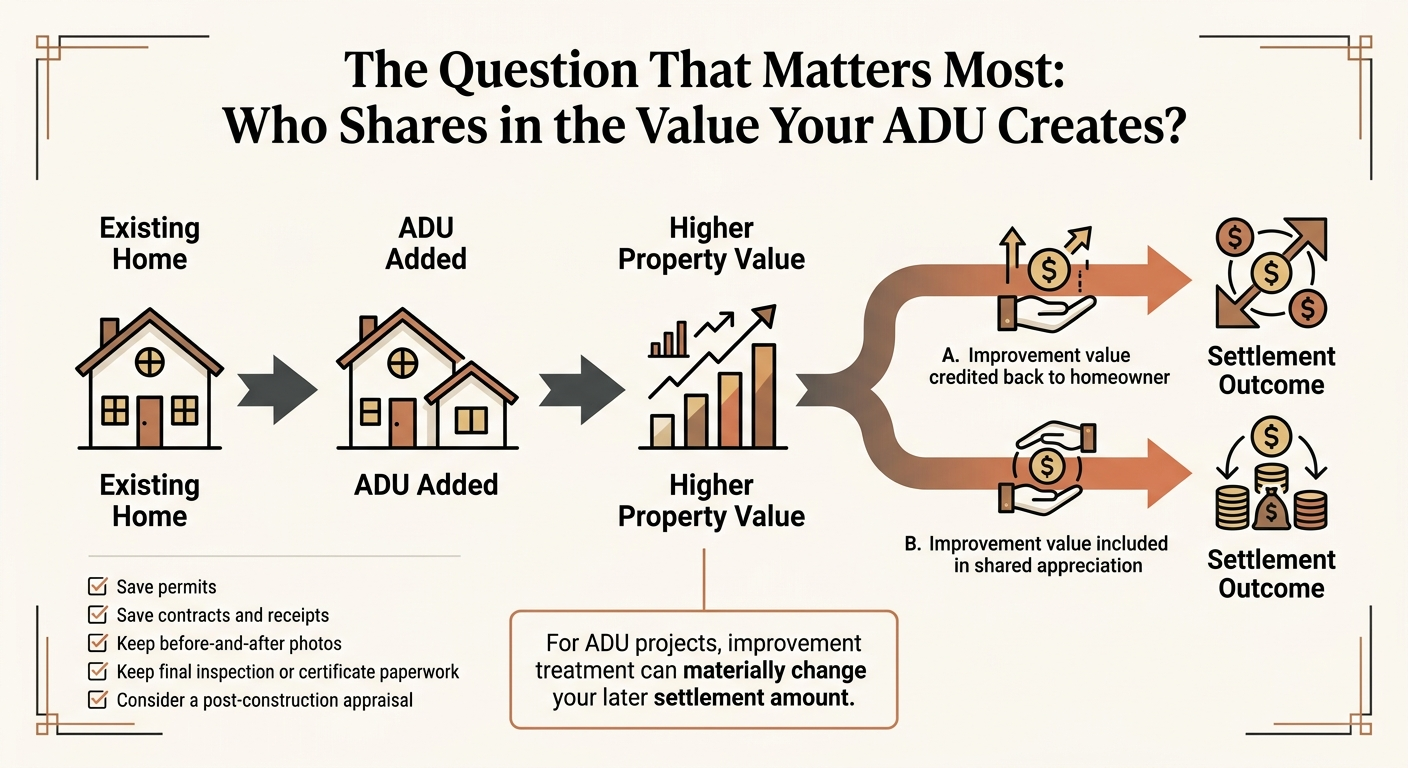

Will You Keep the Value Your ADU Creates?

This is the section that should be on every page covering HEIs for ADU projects. It almost never is.

Here’s why it matters: you’re taking an HEI specifically to build an ADU. That ADU will increase your home’s appraised value — potentially by a meaningful amount depending on your market. When it’s time to settle, a new appraisal captures that increased value. The question is: does the HEI company share in the value your ADU created, or do you get credit for it?

The answer depends entirely on which provider you choose. And the differences are significant.

Who Shares in the ADU-Created Value?

| Provider | Documented Treatment | What It Means for ADU Builders | What to Do |

|---|---|---|---|

| Hometap | Qualified renovations costing $25,000+ may receive a “Renovation Adjustment” — approval is not guaranteed and requires documentation and review | If approved, Hometap adjusts the baseline so it doesn’t share in value you created through improvements. But adjustment is discretionary. | Document everything. Submit renovation details to Hometap for review. Get the adjustment decision in writing before construction. |

| Point | Point states that appreciation from improvements made during the agreement is included in the home value shared at repayment | Point shares in ALL appreciation, including the value your ADU adds. This increases your settlement cost relative to providers that exclude improvement value. | Factor this into your cost comparison. The convenience of Point’s 30-year term and wide availability comes with this tradeoff. |

| Splitero | No clear public documentation found on improvement-treatment specifics | Unknown — and unknown is not acceptable for a decision this large. | Get Splitero’s improvement policy in writing before signing. Do not assume favorable treatment. |

| Unlock | Homeowner can request an “Improvement Adjustment” — Unlock states it does not share in value created by the homeowner’s improvements, subject to appraisal and documentation | Most favorable documented treatment for ADU builders. Designed to exclude improvement-created value from Unlock’s share. | Keep meticulous records: permits, contracts, receipts, before/after photos, and consider an independent post-construction appraisal. |

Sources: Hometap blog — Home Renovation Loans; Unlock FAQ — Improvement Adjustment; Point Help Center — “Can I remodel the home at any time?”; Splitero eligibility page. Last verified: April 2026.

What to document for any HEI-funded ADU project (regardless of provider):

- Pre-construction appraisal or property valuation

- All permits, architectural plans, and engineering reports

- Contractor agreements with itemized costs

- Receipts for materials and labor

- Photos of the property before and after construction

- Certificate of occupancy or final inspection sign-off

- Post-construction appraisal (consider ordering one independently)

This documentation protects you at settlement, whether or not the provider formally offers an improvement adjustment. It’s also good practice for any major home improvement project — it protects your property value and simplifies future transactions.

This table is why you’re reading this page instead of a generic ADU financing article. The improvement-treatment question is the highest-stakes detail for any homeowner using an HEI to build an ADU — and almost nobody else covers it.

Ready to see what an ADU could look like on your property?

Check what you can build at your address — free ADU feasibility report.

What Happens When You Sell, Refinance, or Hit the End of the Term?

Most HEI pages focus on getting you the cash. Few spend real time on the exit — which is the part that determines whether this was a smart decision or an expensive one.

If you sell the home

The simplest exit. When you sell, the HEI company receives its share from the sale proceeds at closing. The title company handles the payoff like any other lien.

If you refinance

Many homeowners plan to refinance after the ADU is built, using the increased home value to take out a new mortgage or HELOC that covers the HEI payoff. This can work well — especially if the ADU significantly increased your property value. But the CFPB notes that some consumers have reported difficulty refinancing to exit their home equity contracts. Don’t assume a refinance exit will be easy. Run the numbers with a mortgage professional before relying on this path.

If you buy out with savings, a HELOC, or a home equity loan

Most providers allow settlement at any time during the term without a prepayment penalty. If you come into cash — inheritance, savings, or a new HELOC — you can buy out the company’s share based on a fresh appraisal. Unlock stands out here with its partial buyback option, letting you repurchase a portion of the company’s share during the term rather than settling all at once.

If you want to stay in your home indefinitely

This scenario requires the most planning. If you never sell and never refinance, you still need to settle at the end of the term. For a 10-year agreement (Hometap, Unlock), that maturity date arrives faster than most people expect. For a 30-year agreement (Point, Splitero), you have more runway — but you still need a plan.

At maturity, if you haven’t settled, the provider may have the right to require you to sell or refinance. Read the maturity provisions in any agreement very carefully before signing.

Your pre-signing exit checklist

Before you apply for any HEI, answer these questions:

- What is my realistic hold period? Am I likely to sell within 5, 10, or 15 years?

- What is my buyout plan if I stay? Can I realistically refinance or accumulate cash by maturity?

- Could the ADU's rental income help fund a buyout over time?

- Does this provider offer partial buyback (Unlock) or early settlement without penalty?

- How does this provider treat improvement-created value? (See the table above.)

The homeowners who struggle most with HEIs are those who never thought about the exit. The ones who do well mapped it out before they signed.

Four Homeowner Scenarios — Find Yours

Numbers and tables are useful, but seeing yourself in a scenario is what makes the decision real. Here are four common situations.

The retiree building for mom

The situation: Sandra, 64, owns a home worth roughly $550,000 with about $120,000 remaining on a 3.1% mortgage from 2020. Her mother needs to move nearby but values independence. Sandra wants to build a detached ADU. Her retirement income covers her current lifestyle but wouldn’t comfortably absorb a new monthly loan payment.

The fit: Sandra is a strong HEI candidate. Significant equity, cash-flow constrained, protecting a favorable first mortgage, and building for family rather than maximum rental ROI. She plans to sell or downsize within 10–12 years, giving her a natural exit timeline. She documents every dollar of ADU construction for a potential improvement adjustment.

Key move: Choose a provider with favorable improvement treatment (Unlock or Hometap) so the ADU’s value is credited back to her at settlement.

The low-rate-mortgage protector

The situation: James and Maria bought their home in 2021 at a favorable rate. It’s appreciated, but they still owe most of the mortgage. They want a garage conversion ADU to rent out — but refinancing into today’s rates would cost them significantly more on the first mortgage.

The fit: With moderate equity, they’re at the lower end of HEI qualification thresholds. A renovation HELOC — which lends based on the home’s after-renovation value — may actually provide a better fit, since their ADU will push the appraised value up and increase their borrowing power. The monthly payment could be partially offset by rental income.

Verdict: HEI is possible but tight for this equity profile. A renovation loan is worth exploring first. Learn more about renovation financing for ADUs →

The self-employed homeowner

The situation: Priya runs a consulting business. Her home has significant equity, and she wants a detached ADU for short-term rental income. Her tax returns — optimized for deductions — show modest income, making traditional HELOC qualification difficult.

The fit: Strong HEI candidate. Her equity is well above minimums, the HEI underwriting won’t penalize her for tax-optimized income, and the rental income from the ADU won’t need to service a monthly payment. She should prioritize a provider with favorable improvement treatment so the ADU-created value is credited back at settlement.

The high-equity homeowner who should probably skip HEI

The situation: David owns a high-value home in a strong appreciation market with modest remaining mortgage balance. He wants a detached ADU for long-term rental income. He can easily qualify for a HELOC, and the projected rental income from the ADU would comfortably cover the monthly payments.

The verdict: For David, monthly-payment financing likely costs less over time — and rental income covers the payments. An HEI would mean sharing in appreciation he doesn’t need to share. David should use a HELOC and keep all the upside.

This is exactly why we’re not an HEI sales page. For David, the right answer is a different financing path. For Sandra and Priya, an HEI genuinely solves a problem nothing else does. Knowing the difference is the whole point of this guide.

These are illustrative examples, not guarantees of returns or costs. Actual results depend on local market conditions, construction costs, provider terms, and individual circumstances. Consult a financial advisor before making equity decisions.

Which scenario sounds closest to yours?

The first step is the same for all of them. See what you can build at your address — get your free ADU feasibility report.

How to Decide in the Right Order

Most homeowners shop for financing too early. They try to solve the money question before they’ve confirmed the project makes sense. That leads to wasted applications and frustration.

Here’s the sequence that prevents regret:

- 1

Confirm your ADU is feasible.

Does your property allow an ADU under current zoning? What types can you build — attached, detached, garage conversion? What are the size limits and setback requirements? Don’t solve financing for a project your lot can’t support.

- 2

Build an all-in budget.

Include design, engineering, permits, utility connections, site work, landscaping, and a 10–15% contingency. ADU projects routinely cost more than initial quotes.

- 3

Identify your real constraint.

Monthly cash flow? Low equity? Income documentation? Each constraint points to a different financing path. HEI solves the payment-burden constraint. Renovation HELOCs address low equity. Traditional HELOCs work when you have both equity and income.

- 4

Check provider availability in your state.

Don’t fall in love with a product that isn’t available where you live.

- 5

Check how each provider treats improvements.

For ADU projects, this is non-negotiable. (See the improvement treatment table above.)

- 6

Choose your exit strategy before applying.

Not vaguely — specifically. How will you settle?

- 7

Compare actual provider terms.

By this point, you’ve filtered out the wrong paths and can evaluate offers with real clarity.

Start at the beginning. See what you can build at your address — get your free ADU feasibility report.

Who Should Avoid This Path?

We’ve been clear about who HEIs serve well. Here’s who should look elsewhere.

Less than 25% equity.

Most HEI providers won’t qualify you. A renovation HELOC or construction loan is likely a better fit. See all ADU financing paths →

Your state has no HEI coverage.

Point covers the most states (27 jurisdictions plus D.C.), but if you’re outside their footprint, explore HELOCs, renovation lending, or — if you’re 62+ — a reverse mortgage.

You want to preserve 100% of future appreciation.

An HEI is structurally the wrong product if this is your priority. A HELOC costs you monthly payments but lets you keep every dollar the ADU adds.

You plan to stay indefinitely with no realistic buyout plan.

A 10-year maturity date (Hometap, Unlock) arrives fast. Even a 30-year term (Point, Splitero) requires planning.

There’s no shame in any of these — they just point to a different path. The fastest way to waste time and money is forcing a financing product that doesn’t match your situation.

Methodology and Editorial Standards

We built this page as an independent educational resource. We are not a lender, broker, or financial advisor. We do not endorse any specific provider.

- Provider data was sourced from official company websites, help centers, eligibility pages, and FAQ documentation for Hometap, Unlock, Point, and Splitero. Where provider documentation was unclear (particularly Splitero’s improvement treatment policy), we noted the gap and instructed readers to verify directly.

- Regulatory context draws primarily from the CFPB’s Issue Spotlight on Home Equity Contracts (2024) and HUD HECM program guidelines.

- State availability was verified against each provider’s published eligibility information. Because coverage changes, every state claim directs readers to confirm with the provider.

- No provider paid for placement, ranking, or favorable coverage. Providers are listed alphabetically in comparison tables. Dwelling Index earns commissions when readers use our links. Those commissions do not influence editorial recommendations or table ordering.

- Financial examples are illustrative and are not guarantees of returns, costs, or outcomes. Individual results depend on home values, market conditions, provider terms, and personal circumstances. We recommend consulting a licensed financial advisor before making equity decisions.

Author: Dwelling Index Editorial Team · Last verified: April 2026

Read our full editorial methodology and affiliate disclosure →

Frequently Asked Questions

Can you finance an ADU without monthly payments?

Yes. A home equity investment gives you a lump sum for your ADU in exchange for a share of your home's future value — with no required monthly payments during the term. For homeowners 62 and older, a reverse mortgage is another option. Both paths have tradeoffs detailed above.

Is a home equity investment the same as a loan?

HEI providers market these products as alternatives to traditional monthly-payment loans, but they are still home-secured financial contracts — a lien is placed on your property, and you have a future settlement obligation. The CFPB notes that the legal classification of these products is evolving. Compare them carefully against other options before signing.

Is an HEI better than a HELOC for building an ADU?

It depends on your constraint. An HEI eliminates monthly payments, which preserves cash flow — critical if you're on fixed income or building for family. A HELOC costs you monthly payments but lets you keep all future appreciation. If the ADU will generate rental income that can cover monthly payments, a HELOC may cost less overall.

Do I keep the value my ADU creates?

This varies by provider and is one of the most important details for ADU builders. Unlock has the most favorable documented policy, stating it does not share in improvement-created value. Hometap may offer a Renovation Adjustment for qualifying projects. Point states that improvement appreciation is included in the shared value. See the detailed comparison table above.

What happens if I never want to sell my home?

You still need to settle the HEI at the end of the term — through a refinance, cash buyout, or other means. If you can't settle, the provider may have the right to require a sale. Read the maturity provisions carefully and build your exit plan before signing.

Which companies offer no-monthly-payment ADU financing?

The four providers compared on this page are Hometap (10-year term, 16 states), Unlock (10-year term, partial buyback, 25 states), Point (up to 30-year term, 27 jurisdictions plus D.C.), and Splitero (mortgage-matched terms, eligible areas of 14 states). All have limited and varying state availability.

Are these options available in every state?

No. Coverage varies significantly. Point has the widest availability. All four providers overlap in 11 states: AZ, CA, FL, NV, NJ, OH, OR, PA, SC, UT, and VA. Always verify directly with the provider.

Can I keep my current first mortgage?

Yes. HEIs are recorded as a second-position lien. Your first mortgage stays in place with its existing rate and terms. This is one of the primary reasons homeowners with favorable locked-in rates choose HEIs.

Can I buy the investment back early?

Most HEI providers allow early settlement without a prepayment penalty. Unlock uniquely offers partial buyback, letting you repurchase a portion of the company's share during the term.

Is a reverse mortgage better if I'm over 62?

Not necessarily. A reverse mortgage accrues interest (balance grows over time), while an HEI does not charge interest. But reverse mortgages are federally regulated, require HUD counseling, and don't involve appreciation sharing. For 62+ homeowners, comparing both with a HUD-approved counselor is the right move.

What if my property doesn't qualify for an ADU?

If zoning, lot size, or setback requirements don't allow an ADU, financing is a moot point. Start with your local zoning code or use our feasibility tool to check what's buildable at your address before exploring financing.

Can I combine an HEI with other funding?

Yes. Some homeowners use an HEI for the bulk of the project and supplement with savings or a small personal loan for the gap. There's no rule requiring a single funding source.

What to Do Next

You’ve read the full analysis. Here’s the right next step depending on where you are:

"I want to explore no-monthly-payment options for my ADU."

Check HEI availability in your state"I'm not sure HEI is the right fit. I want to see all financing paths."

Compare every ADU financing option side by side"I need to check if I can even build an ADU on my property."

See what’s possible at your address — get your free ADU feasibility reportNot sure where to start?

That’s normal — most homeowners feel that way. The fastest path to clarity is checking what your property actually allows.

See What You Can Build — Free ADU Report in 60 SecondsWant the full picture before you build?

Our free 2026 ADU Starter Kit covers costs, financing paths, permit timelines, and builder selection — everything you need in one guide, no strings attached. Download the free 2026 ADU Starter Kit →

Last verified: April 2026. If you notice anything on this page that needs updating, contact our editorial team.