Quick-Reference: Which Fannie Mae ADU Scenarios Work Right Now?

Find your situation. We built this table from the current Selling Guide and the UAD 3.6 Supplement so you don't have to piece it together from six different PDFs.

| Your Scenario | Allowed? | ADU Rent for Qualifying? |

|---|---|---|

| Buying a 1-unit home with an existing ADU | Yes | Yes — 30% cap, purchase only |

| Refinancing a 1-unit home with an existing ADU | Yes | Yes — limited cash-out refi only |

| Adding a new ADU to your current home | Yes | No — not for planned ADU's projected rent |

| Building a new home with an ADU | Yes | Depends on transaction details |

| 2-unit or 3-unit property with an ADU | Yes — new Mar. 2026 | Subject-property rental income rules apply |

| 1-unit property with multiple ADUs | Yes — new Mar. 2026 | Only 1 ADU's income counts (30% cap) |

| Manufactured home as the ADU | Yes | Same qualifying rules as above |

Sources: Selling Guide B2-3-04; SEL-2025-10; UAD 3.6 Policy Supplement; DU 12.1 Release Notes, Feb. 2026.

Why Does the Internet Keep Giving You Contradictory Answers?

The web looks contradictory because it is. The older Fannie Mae Selling Guide text still shows the pre-expansion baseline — one ADU per single-unit property, no ADUs on multi-unit properties. The newer announcements from late 2025 and the UAD 3.6 Supplement expand several of those rules. Both sets of text are technically “current” depending on whether your lender has adopted UAD 3.6.

That means a blog post from 2023 saying “Fannie only allows one ADU” was correct at the time. An article from January 2026 saying “Fannie now allows three ADUs” is also correct — but only for lenders using the newer appraisal framework. And a lender bulletin from October 2025 saying “ADU income now counts” is correct too, but with conditions most articles skip over.

The 2025–2026 Fannie Mae ADU Policy Timeline

| Date | What Changed |

|---|---|

| Oct. 8, 2025 | ADU rental income allowed for mortgage qualifying |

| Dec. 10, 2025 | Expanded ADU eligibility — multiple ADUs, multi-unit properties, broader MH scenarios |

| Jan. 26, 2026 | UAD 3.6 broad production begins |

| Mar. 21, 2026 | Desktop Underwriter Version 12.1 goes live |

| Mar. 31, 2026 | Expanded ADU/MH rules take effect |

| Nov. 2, 2026 | UAD 3.6 mandatory for all appraisals |

The bottom line on lender readiness

If your lender is using UAD 3.6, you have access to the full expanded rules today. If they're not, you're operating under the older baseline. Either way, the core ADU financing products (standard conventional, HomeStyle Renovation, Construction-to-Permanent) and the rental income rules from October 2025 apply across the board.

The part that actually matters for your next lender conversation: Fannie Mae is not a lender — it buys loans from lenders. Your lender originates the loan under Fannie-compatible rules, and some lenders add their own stricter requirements (called overlays). That means two lenders can look at the exact same property and give you different answers. One “no” doesn't mean the property is impossible under Fannie. It may mean that lender isn't ready for your scenario yet.

Not sure if your property qualifies?

Skip the guesswork — get a property-specific ADU report that factors in your local zoning, lot size, and financing options.

See What You Can Build — Free ADU ReportWhich Fannie Mae ADU Scenario Are You In?

Most readers don't need more definitions — they need to find themselves in the answer. Pick the scenario that matches your situation, then follow the path.

You're Buying a Home That Already Has an ADU

This is the most straightforward Fannie Mae ADU scenario, and it's the one that changed the most in October 2025. The property with an existing ADU can be financed with any Selling Guide loan product — standard conventional, HomeReady, or an affordable lending product. There is no special “ADU loan” required.

The game-changer since October 2025

You can now use ADU rental income to help qualify for the mortgage. The rent from that above-garage apartment or backyard cottage counts toward your qualifying income — with conditions.

The conditions that matter:

- The property must be a one-unit, principal residence (you're living there)

- Transaction type must be a purchase or limited cash-out refinance

- Only one ADU's income counts, even if multiple ADUs exist

- The ADU income is capped at 30% of your total qualifying income

- You'll need either a current lease or a Form 1007 (Comparable Rent Schedule) from the appraiser

- Lenders typically apply a 25% vacancy/expense reduction to the rent amount

The classification risk — where deals get stuck

The appraiser must determine whether the property is a “one-unit home with an ADU” or a “two-unit property.” If they call it a two-unit, your down payment requirements, LTV limits, and loan terms change significantly. We cover this in the property classification section below.

Sources: SEL-2025-08; Selling Guide B2-3-04; B3-3.8-01.

Above-garage ADUs like this one are among the most common Fannie Mae ADU configurations — and since October 2025, the rental income can count toward your qualifying income.

You Already Own the Home and Want to Add an ADU

Your path: HomeStyle Renovation loan

This is Fannie Mae's primary vehicle for financing ADU construction on an existing property. HomeStyle Renovation wraps your existing mortgage and the ADU construction costs into a single loan, based on the property's future value with the ADU completed. Even if you don't have a ton of equity right now, the appraisal is done “as-completed” — so the ADU's projected contribution to property value helps you qualify for enough funding to build it.

Key details:

- Maximum LTV up to 97% depending on transaction type and eligibility matrix

- No minimum renovation dollar amount

- Borrowers choose their own contractor, subject to lender review; DIY is allowed on one-unit properties up to 10% of as-completed value (not for manufactured homes — no sweat-equity reimbursement)

- Renovation work must be completed within 15 months of closing; lenders can grant limited extensions up to 18 months for extenuating circumstances

- Funds are held in a custodial account and released in stages as construction progresses (draw system)

- Can be combined with HomeReady for income-eligible borrowers

- You can even install a manufactured home ADU through HomeStyle Renovation

What you should not assume

That you can count projected rental income from the ADU you haven't built yet toward your qualifying income. The October 2025 rental income rule applies to existing ADUs. Once the ADU is built and you have a lease or rental history, future refinancing could leverage that income.

Sources: Fannie Mae HomeStyle Renovation product page; Selling Guide B5-3.2-01; SEL-2025-08.

You're Building a New Home With an ADU

Your path: Construction-to-Permanent loan

If you're building from the ground up — new primary home plus ADU — Fannie Mae's Construction-to-Permanent (C-to-P) financing rolls the construction phase and the permanent mortgage into one or two closings. Your lender must be approved for C-to-P delivery.

This is a construction workflow, not a regular purchase with bonus rent. Expect plans and specs, contractor documentation, appraisal based on plans, and a draw schedule. It's more paperwork and more moving parts, but it's the right tool for the job.

You Have a Duplex or Triplex and Want an ADU

This is new territory — effective March 31, 2026

Before this date, Fannie Mae did not allow ADUs on two- to four-unit properties at all.

Under the expanded UAD 3.6 rules, a two- or three-unit property can now include ADUs, provided the total number of dwelling units plus ADUs does not exceed four:

- A duplex can have up to 2 ADUs (2 units + 2 ADUs = 4 total)

- A triplex can have 1 ADU (3 units + 1 ADU = 4 total)

- A fourplex still cannot have any ADUs

Important distinction on rental income

For owner-occupied 2–4 unit properties, Fannie's standard subject-property rental income rules apply — these are different from the special one-unit ADU income rules (30% cap). Don't assume the same formula applies. Verify with your lender.

The operational catch: Your lender must be submitting UAD 3.6 appraisals for this to work. UAD 3.6 becomes mandatory for all lenders on November 2, 2026 — but many are already using it.

Source: SEL-2025-10; UAD 3.6 Policy Supplement.

You Have (or Want) Multiple ADUs on a Single-Unit Property

Also new under the expanded rules: a one-unit property can now have up to three ADUs — but only one ADU's rental income can be counted toward qualifying, and only under the same conditions described in Scenario 1. Each additional ADU adds appraisal complexity and documentation requirements. The same UAD 3.6 requirement applies.

How ADU Rental Income Actually Works for Qualifying (With Real Math)

This is the section that separates this page from every other article on the internet. We're going to walk through the actual math using Fannie Mae's published methodology so you can see exactly how ADU income affects your purchasing power.

The core rules, one more time:

- One-unit principal residence

- Purchase or limited cash-out refinance only

- One ADU's income, even if multiple exist

- Capped at 30% of total qualifying income

- Lenders apply a 25% vacancy/expense factor (you get credit for 75% of rent)

- Documentation: current lease + Form 1007, or tax returns if rental history exists

Example 1: First-Time Buyer — ADU Income Expands Purchasing Power

A couple earns $6,000/month combined. They're buying a home with an above-garage ADU currently leased at $1,400/month. They've never been landlords before.

| Step | Calculation | Result |

|---|---|---|

| Gross monthly ADU rent | Per lease | $1,400 |

| Apply 75% factor (25% vacancy/expense) | $1,400 × 0.75 | $1,050 |

| Check 30% cap | $1,050 ÷ ($6,000 + $1,050) = 14.9% | ✓ Under 30% |

| Total qualifying income | $6,000 + $1,050 | $7,050/month |

New landlord catch: Because these buyers have never been landlords, Fannie Mae limits the ADU rental income to no more than their monthly PITIA (principal, interest, taxes, and insurance). So if their PITIA is $1,000/month, qualifying rental income gets capped at $1,000 — not the full $1,050.

Example 2: Homeowner Refinancing — High-Earning ADU

A homeowner earns $10,000/month and rents a detached backyard ADU for $2,500/month. She wants a limited cash-out refinance. She has rental history on her tax returns.

| Step | Calculation | Result |

|---|---|---|

| Gross monthly ADU rent | Per lease | $2,500 |

| Apply 75% factor | $2,500 × 0.75 | $1,875 |

| Check 30% cap | $1,875 ÷ ($10,000 + $1,875) = 15.8% | ✓ Under 30% |

| Total qualifying income | $10,000 + $1,875 | $11,875/month |

No new-landlord restriction here — she has rental history on her tax returns. The full $1,875 counts.

Example 3: When the 30% Cap Actually Bites

A borrower earns $3,000/month and has an ADU renting for $2,000/month. The ADU income is large relative to base income.

| Step | Calculation | Result |

|---|---|---|

| Gross monthly ADU rent | Per lease | $2,000 |

| Apply 75% factor | $2,000 × 0.75 | $1,500 |

| Check 30% cap | $1,500 ÷ ($3,000 + $1,500) = 33.3% | ✗ Over 30% |

| Solve for max ADU income | ADU = 0.30 × ($3,000 + ADU) → ADU ≈ $1,286 | $1,286 |

| Total qualifying income | $3,000 + $1,286 | $4,286/month |

The borrower loses about $214/month of qualifying power to the cap. When ADU income is large relative to your base salary, the 30% ceiling matters.

These are illustrative examples, not guarantees of results. Actual qualifying income depends on your complete financial picture, property details, lender requirements, and current documentation standards. Talk to a lender for your specific numbers. Sources: SEL-2025-08; Selling Guide B3-3.8-01; Fannie Mae ADU/Boarder Income matrix, Nov. 2025.

When ADU Rent Counts — and When It Doesn't

| Scenario | Can Rent Count? |

|---|---|

| Buying 1-unit primary with existing ADU, tenant in place | Yes |

| Buying 1-unit primary with vacant ADU | Yes |

| Limited cash-out refi on 1-unit primary with existing ADU | Yes |

| Full cash-out refinance | No |

| Investment property with ADU | No |

| Second home with ADU | No |

| Adding a new ADU (hasn't been built yet) | No |

| 2–3 unit property with ADU | Different rules apply |

If the math is working in your favor

Compare lenders who are current on these rules

See current conventional and renovation loan options from multiple lenders — side by side.

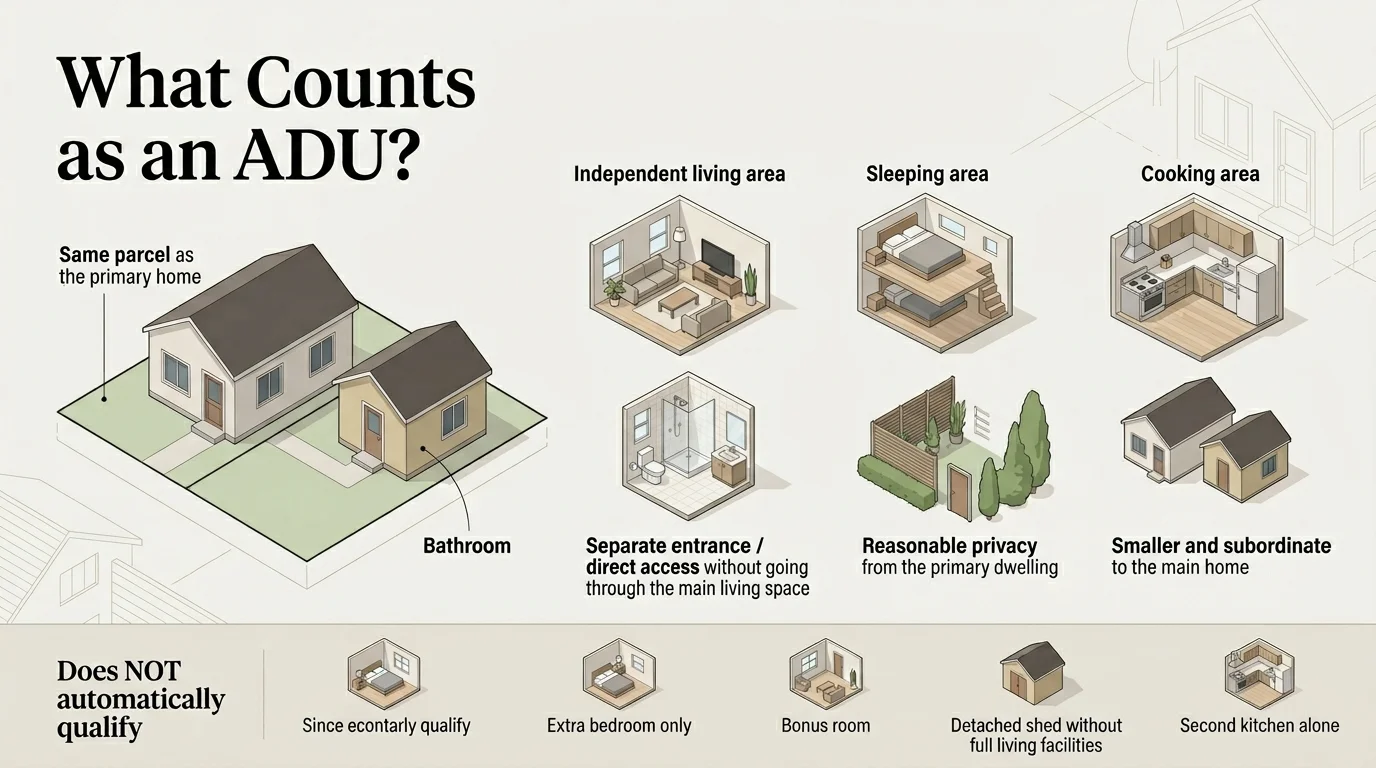

What Counts as an ADU Under Fannie Mae?

For Fannie Mae purposes, an ADU must function as an independent living area on the same parcel as the primary dwelling, with its own living, sleeping, cooking, and bathroom facilities. It must be accessible without going through the main home, and there must be a reasonable expectation of privacy. An extra kitchen by itself does not make an ADU.

Fannie Mae's definition requires all six elements. Missing any one of them means the space doesn't qualify as an ADU.

The Fannie Mae ADU Eligibility Checklist

| Requirement | What It Means |

|---|---|

| Independent living area | Separate from the primary home's living space |

| Living + sleeping + cooking + bathroom | Must have all four — a microwave doesn't count as a stove |

| Separate access | Own entrance — can't only be accessed through the main house |

| Privacy expectation | Not an open loft, great room, or pass-through space |

| Same parcel | ADU must be on the same legal lot as the primary dwelling |

| Subordinate in size | Smaller than the primary dwelling |

ADU Types Fannie Mae Accepts

Interior

Basement apartment, converted space within the home

Attached

Above-garage apartment, addition with separate entrance

Detached

Standalone backyard cottage, garden suite, carriage house

Manufactured home

Single-width or multi-width, titled as real property (not personal property), HUD Code standards met, wheels/axles/hitch removed, permanent foundation installed. HUD Data Plate and Certification Labels must be evidenced in the appraisal.

Manufactured Home ADUs: Legacy vs. Expanded Rules

Legacy rules (UAD 2.6)

The primary dwelling must be site-built or modular for the property to include a manufactured home ADU. If your main house is a manufactured home, this configuration was not eligible.

Expanded UAD 3.6 rules (effective Mar. 31, 2026)

Fannie Mae expanded eligibility for some manufactured-home-primary configurations with ADUs. Your lender must be using UAD 3.6 to access these expanded rules. Confirm your lender's UAD 3.6 status before relying on the expanded rule.

What Does NOT Qualify as an ADU

A second kitchen without the other required facilities

A bedroom suite accessible only through the main house

An open loft or bonus room with no separation or privacy

A park model home (typically still on wheels/axles)

A detached structure without living, sleeping, cooking, and bathroom facilities (classified as an ancillary structure, not an ADU)

Sources: Selling Guide B2-3-04; B4-1.3-05; UAD 3.6 Policy Supplement.

Is Your Property a “One-Unit Home With an ADU” — or a Two-Unit Property?

This classification question kills more ADU deals than almost any other issue.

If you've ever seen a forum post that says “underwriting is coming back saying it's a 2–4 unit,” this is why. That classification changes everything — your down payment, LTV limits, interest rate, and qualifying requirements all shift.

No single factor determines the classification. Appraisers look at the overall picture.

How the Appraiser Draws the Line

| Factor | Pushes Toward “1-Unit + ADU” | Pushes Toward “2-Unit Property” |

|---|---|---|

| Size relationship | ADU clearly smaller than primary | ADU similar in size to primary |

| Utility meters | Shared meters | Separate meters for each unit |

| Postal address | One address | Separate addresses |

| Legal rental status | ADU may or may not be rented | Both units independently rentable |

| Layout/configuration | ADU feels like an addition or accessory | Property feels like two independent residences |

| Market perception | Neighborhood views it as a single-family with bonus space | Market treats it as an income property |

What This Means for You

If you're buying a property with an ADU and you're worried about classification, ask your lender these questions before you're deep into the process:

How will the appraiser likely classify this property?

If it's classified as a two-unit, how does that change my loan terms?

Is this a Fannie Mae rule issue or a lender overlay issue?

Can we order a preliminary property review before committing to the full appraisal?

The appraiser's determination goes in the “Highest and Best Use” section of the appraisal report. It's a professional judgment call based on the property's actual characteristics. Source: Selling Guide B2-3-04; B4-1.3-05.

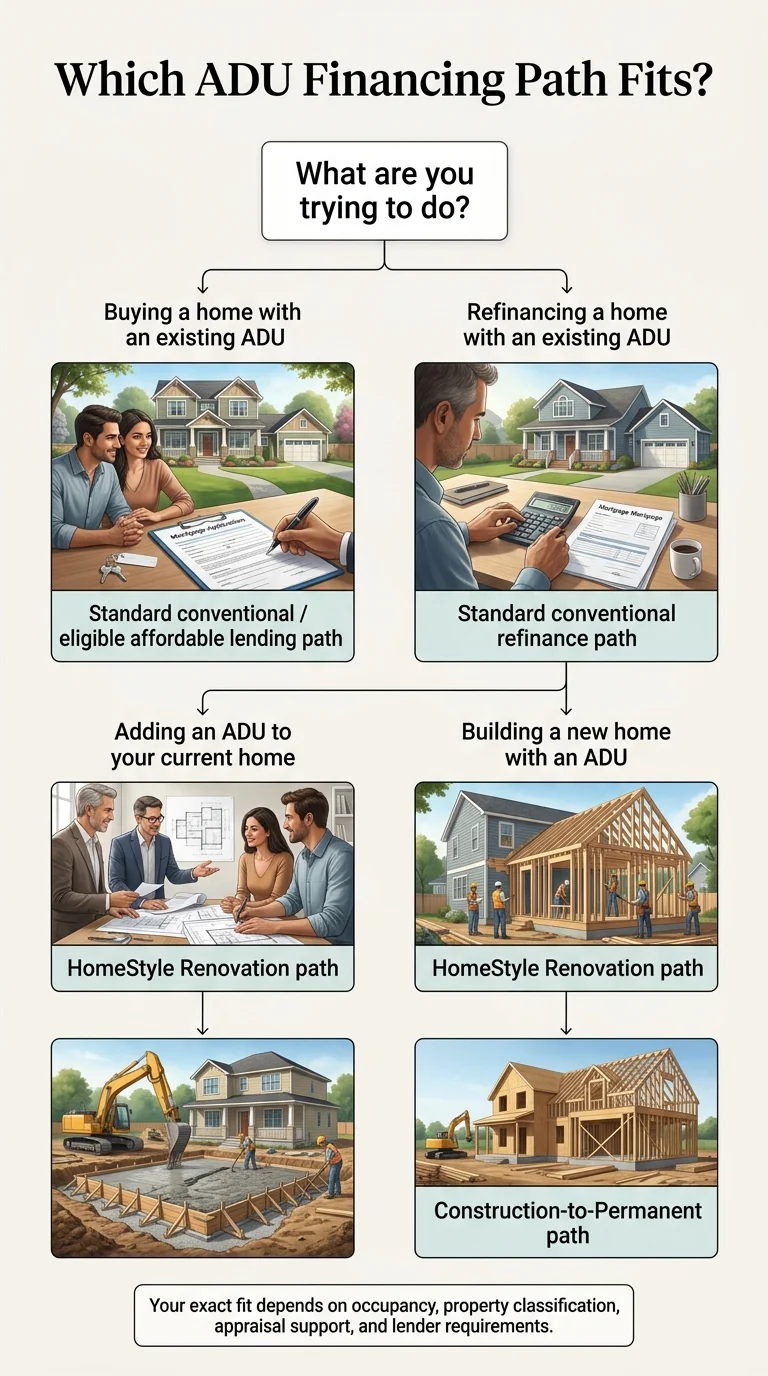

Which Fannie Mae Loan Path Fits Your ADU Project?

There is no single “Fannie Mae ADU loan.” The right product depends entirely on your situation. Here's the decision matrix.

Your exact fit depends on occupancy, property classification, appraisal support, and lender requirements.

Loan Path Comparison Table

| Your Situation | Best-Fit Product |

|---|---|

| Buying a home with an existing ADU | Standard conventional |

| Buying with existing ADU, income-eligible | HomeReady |

| Adding an ADU to your current home | HomeStyle Renovation |

| Building a new home + ADU from scratch | Construction-to-Permanent |

| Refinancing a home with an existing ADU | Standard conventional |

| Energy/resiliency upgrades to ADU | HomeStyle Refresh (new Mar. 2026) |

HomeStyle Renovation — The Most Underused Tool for ADU Construction

HomeStyle Renovation lets you refinance your existing mortgage and roll in the entire cost of building an ADU — and the loan amount is based on what your property will be worth after the ADU is built. So even if you bought your home recently and haven't built up much equity yet, the ADU's projected value contribution can help you qualify for enough funding to build it.

How it works, step by step:

You select a contractor (your choice, subject to lender review) and develop ADU plans and specs

Your lender reviews the scope and docs

An appraiser values the property "as-completed" — as if the ADU were already built

The loan closes and renovation funds go into a custodial account

Your contractor draws funds in stages as construction progresses

The lender inspects at each draw milestone

Final draw, completion certification, and you're done — typically within 15 months of closing

The numbers: Up to 97% LTV on the as-completed value (varies by transaction and eligibility). No minimum renovation dollar amount. DIY is allowed on one-unit properties up to 10% of as-completed value. You can combine HomeStyle with HomeReady for income-eligible borrowers. You can even use it to install a manufactured home ADU.

The FHA 203(k) loan is a similar concept but runs through FHA instead of Fannie Mae. It allows an even higher LTV (97.75%) and may have lower credit-score requirements, but you'll carry mortgage insurance for the life of the loan on most terms. Worth comparing both with your lender.

Considering a HomeStyle Renovation loan or a construction path for your ADU?

The next step is to talk to a lender who works with these products regularly. Compare options side by side.

Fannie Mae vs. Freddie Mac vs. FHA: How ADU Rules Compare

If you're shopping for the best financing path for an ADU, you're not limited to Fannie Mae. Freddie Mac and FHA both have their own ADU-friendly rules — and in some cases, they're more flexible.

| Criteria | Fannie Mae | Freddie Mac | FHA |

|---|---|---|---|

| ADU financing allowed? | Yes — any Selling Guide product | Yes — all mortgage offerings | Yes — including 203(k) |

| ADU rental income to qualify? | Yes (since Oct. 2025) | Yes (since June 2022) | Yes (since Oct. 2023) |

| ADU rental income cap | 30% of total qualifying income | 30% of total monthly income | 30% of total monthly effective income |

| ADU-income eligible transactions | Purchase + limited cash-out refi (1-unit principal residence) | Purchase + no-cash-out refi | Purchase + refinance (not cash-out) |

| Max ADUs on 1-unit | Up to 3 (Mar. 2026, UAD 3.6 required) | 1 | 1 |

| ADUs on multi-unit? | Yes — 2–3 unit (units + ADUs ≤ 4; UAD 3.6 required) | Yes — 1–3 unit (1 ADU only) | Verify current HUD guidance |

| Manufactured home as ADU? | Yes (single or multi-width, titled as real property) | Yes (multi-width; verify current Freddie requirements) | Yes |

| Renovation loan for ADU | HomeStyle Renovation | CHOICERenovation | FHA 203(k) |

| Max LTV (renovation) | Up to 97% (as-completed, varies by transaction) | Up to 97% (as-completed, varies) | 97.75% of as-completed value |

| Automated underwriting | DU 12.1 (live Mar. 2026) | Loan Product Advisor | FHA Connection |

Key takeaways

- All three agencies cap ADU rental income at 30% of total qualifying income. This is consistent across the board, though the specific calculation methods differ slightly.

- Freddie Mac got there first on ADU rental income (June 2022 vs. Fannie's October 2025 and FHA's October 2023).

- Fannie Mae is the most aggressive on multi-ADU scenarios — up to three ADUs on a single-unit property is a Fannie-only policy right now.

- Manufactured-home-primary configurations are expanding across agencies. The UAD 3.6 expansion opened new Fannie Mae options — verify current guidelines with your lender.

All policies verified as of April 2026. These are general guidelines — individual lender overlays apply. Confirm details with your specific lender before making decisions. Sources: Selling Guide B2-3-04; SEL-2025-08; SEL-2025-10; UAD 3.6 Policy Supplement; Freddie Mac Section 5601.2; Freddie Mac ADU Fact Sheet, Jan. 2025; HUD Mortgagee Letter 2023-17.

What If Your ADU Is Legal Nonconforming, Unpermitted, or Not Allowed by Zoning?

This section matters more than most people think. A huge number of ADUs in the U.S. were built decades ago under previous zoning rules, and many technically don't conform to current codes. That doesn't automatically mean your Fannie Mae loan is dead.

Legal Nonconforming ADUs

A “legal nonconforming” ADU is one that was legally built under the rules that existed at the time but doesn't meet current zoning or building codes. Many cities grandfather these units. Fannie Mae does finance properties with legal nonconforming ADUs. The appraiser must document the status and confirm the ADU can continue under existing grandfathering provisions. A letter from the municipality confirming legal nonconforming status can help smooth the process.

What About Unpermitted ADUs?

Fannie Mae's Selling Guide does not automatically exclude properties where the ADU doesn't comply with current zoning — but additional conditions must be met:

The appraiser must state the noncompliant use in the report

The noncompliant use must conform to the neighborhood (it's not unique to this property)

The property must be appraised based on its current use

There must be at least two comparable sales with the same noncompliant use, and a minimum of three settled sales total

The lender must confirm no insurance-claim jeopardy from the noncompliant use

This does not mean “all unpermitted ADUs are fine.”

It means this is exactly where appraiser quality and lender competence matter most. If your ADU's permit status is uncertain, bring it up with your lender early — not after you're already in underwriting.

Source: Selling Guide B2-3-04; B4-1.3-05.

What Appraisal and Documentation Will Your Lender Need?

More ADU deals fail from documentation issues than from the rules themselves.

Here's the paperwork checklist so nothing catches you off guard.

| Document | Common Mistake |

|---|---|

| Standard appraisal (Form 1004) | Appraiser doesn't adequately describe the ADU |

| Form 1007 — Comparable Rent Schedule | Not requesting Form 1007 early enough; appraiser can't find ADU rent comps |

| Current lease agreement | Lease is expired, unsigned, or missing required details |

| Schedule E (tax return) | Forgetting to include prior-year rental documentation |

| Zoning/permit documentation | Assuming legal nonconforming status without documentation |

| Plans, specs, and contractor bids | Submitting incomplete plans that delay appraisal |

| HUD Data Plate / Certification Labels | Photos must be in the appraisal; if originals unavailable, use IBTS verification, IPIA, or manufacturer documentation |

What the Appraiser Looks For

Confirm the ADU meets Fannie Mae's definition

Determine whether the property is a 1-unit + ADU or a multi-unit property

Report the ADU's living area separately (not rolled into the main home's square footage in most cases)

Analyze the ADU's effect on property value and marketability

Show market acceptance through comparable sales that include ADUs

Provide rental support if income is being used for qualifying

Under UAD 3.6 (new appraisal format)

Rental support is generally built into the URAR Rental Information section and Rental Comparison Grid rather than a separate Form 1007. In rare cases — such as when the original appraiser is unavailable to amend the URAR — Form 1007 may still be used by another appraiser to satisfy the requirement. For appraisals still using the older UAD 2.6 format, Form 1007 remains a standalone companion document.

Sources: Selling Guide B4-1.3-05; Fannie Mae Appraiser Update, Q1 2026; UAD 3.6 Policy Supplement.

The Honest Part: What's Still Hard About Fannie Mae ADU Financing

Here's what we'd tell you if we were sitting across the table: Fannie Mae's ADU rules on paper are better than they've ever been. But the real-world experience still depends on your lender's readiness, your appraiser's competence, and your local market's ADU history.

DU Version 12.1 only went live in March 2026. The expanded multi-ADU rules require UAD 3.6 appraisals that won't be mandatory until November 2026. That means some lenders are fully up to speed and some are still operating on the old playbook.

This is not a reason to wait. It's a reason to be strategic. The homeowners successfully using Fannie Mae's ADU rules right now are the ones who:

Choose a lender who has specifically adopted the latest guidelines (ask the five questions below)

Prepare their documentation early and completely

Work with appraisers who have experience valuing properties with ADUs in their market

Don't take one lender's 'no' as a universal answer

The ADU-friendly lending landscape is expanding every month. Properties with ADUs are increasingly common, appraiser familiarity is growing, and by November 2026, every Fannie-approved lender will be on the same expanded ruleset. The window of lender confusion is closing. Your job is to find a lender who's already through it.

What If One Lender Says Your ADU Doesn't Qualify?

A “no” from one lender does not mean the property is impossible under Fannie Mae.

It may mean the lender is applying a stricter overlay. It may mean the appraiser classified the property differently than you expected. It may mean the lender hasn't adopted UAD 3.6 yet. Or it may mean you're trying to use ADU income in a way the rules don't actually support.

The 5 Questions to Ask Your Lender

“Is the issue a Fannie Mae rule or a lender overlay?”

Overlays are extra restrictions your lender adds on top of Fannie's rules. A different lender may not have the same overlay.

“Is the property being classified as a one-unit with ADU or as a two-unit?”

If it's a classification issue, the problem might be the appraisal, not the property.

“Are you using DU Version 12.1 and UAD 3.6 for this loan type?”

If not, the expanded rules may not be available through this lender.

“Are you declining the property, the income, or both?”

A property can be eligible even if the rental income can't be used for qualifying.

“What specific document or appraisal issue needs to be resolved?”

Sometimes the answer is fixable — a missing Form 1007, an unclear zoning letter, or an appraisal that didn't describe the ADU adequately.

When to Try Another Lender

If the deal is theoretically within Fannie Mae's current rules but your lender can't or won't make it work, shop around. Some lenders specialize in ADU transactions and are fully current on the latest guidelines. The difference between a lender who “kind of knows ADUs” and one who works with them regularly can be the difference between a dead deal and a closed loan.

Ready to compare lenders who are current on Fannie Mae's ADU guidelines?

See conventional, renovation, and construction loan options side by side.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Full disclosure

Edge Cases That Would Otherwise Send You Back to Search

We built this section to catch the follow-up questions that usually trigger another search.

Does Fannie Mae require the ADU to have a separate entrance?

Yes. The ADU must be accessible without going through the primary dwelling. If the only way to reach the ADU is through the main house — like a locked interior door with no exterior access — it doesn't meet Fannie's definition. There must also be a reasonable expectation of privacy between the ADU and the primary home.

Source: Selling Guide B2-3-04

Does ADU square footage get included in the main house's total?

Generally, no. The ADU's finished area should be reported separately from the primary dwelling's above-grade living area. The exception is if the ADU space is above-grade, part of the primary dwelling's footprint, and has interior access — in which case, classification gets complicated and the appraiser makes the call.

Source: Selling Guide B4-1.3-05

Do you automatically need 20% down for a home with an ADU?

No. There is no blanket Fannie Mae rule that says ADU = 20% down. If the property is classified as a one-unit with an ADU, standard one-unit down payment rules apply. HomeReady offers 3% down. The standard 97% LTV purchase option is also available for eligible first-time buyers. The 20% myth may come from lender overlays or confusion with two-unit property requirements (which do require higher down payments).

Source: Fannie Mae Product Eligibility Matrix; 97% LTV FAQs

Can you use a garage conversion as an ADU for Fannie Mae?

If the converted garage includes living, sleeping, cooking, and bathroom facilities with a separate entrance and privacy expectation, yes — it would qualify as an interior or attached ADU. The conversion must comply with local zoning and building codes (or qualify as legal nonconforming).

Source: Selling Guide B2-3-04

Can you use ADU income on a cash-out refinance?

No. ADU rental income for qualifying is limited to purchase and limited cash-out refinance transactions only. Full cash-out refinances cannot use ADU income to qualify. You'll need to qualify on your other income alone.

Source: SEL-2025-08

What about investment properties and second homes?

The special ADU rental income rules (30% cap) require the property to be a one-unit principal residence — meaning you must live there. Investment properties and second homes don't get this benefit. The ADU can still exist on the property and add value, but its rental income won't be counted under the special one-unit ADU rules.

What happens when you sell a home with an ADU?

The ADU adds value. A future buyer may be able to finance the home under current ADU rules, and eligible buyers may be able to use existing ADU income to help qualify — but only if their transaction fits the one-unit principal-residence ADU-income rules described above. This makes your property more marketable to the right buyer.

Is Fannie Mae the lender on my current mortgage?

Fannie Mae isn't a direct lender — it buys loans from lenders. But if you're refinancing, you can check whether your current loan is owned by Fannie Mae using Fannie Mae's Loan Lookup tool. This can help determine your refinancing options.

Source: fanniemae.com/loan-lookupHow to Verify Your Scenario Before You Apply

Before you talk to a lender, run through this checklist. It'll save you time, prevent surprises, and make you the most prepared borrower your loan officer sees that week.

Property questions

- Does the ADU already exist, or are you planning to build one?

- Does it have living, sleeping, cooking, and bathroom facilities with a separate entrance?

- Is the ADU on the same parcel as the primary dwelling?

- Is the ADU legal, legal nonconforming, or unpermitted? (Check with your municipality)

- Is the primary dwelling site-built, modular, or manufactured? (Affects which rules apply)

Transaction questions

- Are you buying, refinancing (limited cash-out), or building?

- Will this be your principal residence?

- Do you want to use ADU rental income to qualify?

Lender questions to ask

- "Have you adopted the October 2025 ADU rental income guidelines (SEL-2025-08)?"

- "Are you using DU Version 12.1?"

- "Are you submitting UAD 3.6 appraisals?"

- "Do you offer HomeStyle Renovation loans for ADU construction?"

- "What are your overlays on ADU properties?"

This is the step that makes everything else easier

See what's possible at your address — takes 60 seconds, it's free

Our free ADU feasibility report covers your local zoning, estimated ADU sizes for your lot, and financing options that match your situation.

Get Your Free ADU ReportADU Financing Paths Beyond Fannie Mae

If you've determined that a Fannie Mae conventional loan isn't the right fit for your specific situation, you have options. Here's the quick map:

Freddie Mac CHOICERenovation

Nearly identical to HomeStyle Renovation, but Freddie's rules differ on manufactured home configurations and rental income history.

FHA 203(k)

Higher LTV (97.75%) and potentially lower credit requirements, but mortgage insurance for the life of the loan on most terms.

HELOC or Home Equity Loan

If you have substantial equity and want fast, flexible funding without refinancing your first mortgage.

Renovation HELOC

Some lenders offer HELOCs based on after-renovation value — useful if you have low current equity but the ADU will significantly increase your home's worth. Availability varies by lender and state.

Cash-Out Refinance

If you have strong equity and your current rate is close to or higher than current market rates.

Construction Loan

For larger ADU projects that need staged funding tied to construction milestones.

For a full comparison, see our ADU financing overview. Each path has tradeoffs — the right one depends on your equity position, credit profile, timeline, and whether you're buying, building, or refinancing.

Frequently Asked Questions

Does Fannie Mae finance ADUs?

Yes. Fannie Mae treats a qualifying ADU as a property feature — not a special loan category. It can be financed with any Selling Guide loan product, including standard conventional purchase, refinance, HomeStyle Renovation, Construction-to-Permanent, and HomeReady.

Can you use ADU rental income to qualify for a Fannie Mae mortgage?

Yes, since October 2025. The property must be a one-unit principal residence, the transaction must be a purchase or limited cash-out refinance, and the ADU income is capped at 30% of total qualifying income. Lenders apply a 25% vacancy factor.

How many ADUs does Fannie Mae allow?

Under the expanded rules effective March 31, 2026: up to three ADUs on a single-unit property, and ADUs on two- to three-unit properties (total units plus ADUs cannot exceed four). These expanded rules require UAD 3.6 appraisals.

Can you add an ADU with a HomeStyle Renovation loan?

Yes. HomeStyle Renovation explicitly allows financing ADU construction, including installing a manufactured home ADU. The loan is based on the property's as-completed value. Maximum LTV up to 97%.

Does the ADU have to already exist to use its rental income?

Yes, for mortgage qualifying purposes. The October 2025 rental income rule applies to existing ADUs, not projected income from a unit you plan to build.

What is Form 1007 and when do you need it?

Form 1007 is the Single-Family Comparable Rent Schedule — a form the appraiser completes to establish fair market rent for the ADU. You need it when ADU rental income is being used for qualifying under the UAD 2.6 appraisal format. Under UAD 3.6, rental support is generally built into the URAR, though Form 1007 may still be used in rare cases.

What if the ADU is legal nonconforming?

Fannie Mae can finance properties with legal nonconforming ADUs. The appraiser must document the status and confirm the ADU can continue under existing grandfathering provisions. Municipal documentation helps.

Does Fannie Mae allow manufactured homes as ADUs?

Yes — both single-width and multi-width, provided they are titled as real property, meet HUD Code standards, and are on a permanent foundation with wheels and axles removed. HUD Data Plate and Certification Labels must be evidenced in the appraisal.

Can a manufactured home be the primary residence with an ADU?

Under legacy Selling Guide rules, generally no. Under the expanded UAD 3.6 rules effective March 31, 2026, some manufactured-home-primary configurations are eligible. Verify that your lender is using UAD 3.6 before relying on the expanded rule.

Do you automatically need 20% down for a home with an ADU?

No. There is no blanket Fannie Mae rule requiring 20% down for a home with an ADU. If the property is classified as a one-unit with an ADU, standard one-unit down payment rules apply. HomeReady offers 3% down. The 20% myth may come from lender overlays or confusion with two-unit property requirements.

Does one lender's denial mean the property is impossible?

No. A denial may reflect a lender overlay, an appraiser classification issue, or a lender that has not adopted the latest guidelines. Ask whether the issue is a Fannie Mae rule or a lender overlay, and consider working with a different lender.

Get Your Free ADU Report

See what's possible at your address — local zoning, estimated ADU sizes, and financing options. Takes 60 seconds.

Get My Free ReportDownload the Free 2026 ADU Starter Kit

Financing comparison worksheets, permit checklists, cost estimators, and a state-by-state law summary. No strings, instant download.

Download the Starter KitSources and Methodology

This page was built by independently reviewing Fannie Mae's published Selling Guide, official announcements, and supplemental policy documents. We cross-referenced multiple sources for every rule cited and verified each against the most current available version.

Primary sources cited:

- —Fannie Mae Selling Guide B2-3-04: Special Property Eligibility Considerations

- —Fannie Mae Selling Guide B3-3.8-01: Rental Income

- —Fannie Mae Selling Guide B4-1.3-05: Improvements Section of the Appraisal Report

- —Fannie Mae Selling Guide B5-3.2-01: HomeStyle Renovation Mortgages

- —Selling Guide Announcement SEL-2025-08 (October 8, 2025)

- —Selling Guide Announcement SEL-2025-10 (December 10, 2025)

- —DU Version 12.1 Release Notes (February 18, 2026)

- —Fannie Mae Selling Guide Supplement: UAD 3.6 Policy

- —Fannie Mae ADU Product Page

- —Fannie Mae HomeStyle Renovation Product Page

- —Fannie Mae Appraiser Update Newsletter, Q1 2026

- —Freddie Mac Single-Family Seller/Servicer Guide Section 5601.2

- —Freddie Mac ADU Fact Sheet (January 2025)

- —HUD Mortgagee Letter 2023-17 (October 16, 2023)

This page provides general educational information about Fannie Mae's ADU-related policies. It is not legal, financial, or lending advice. Fannie Mae is not a direct lender — loans are originated by approved lender-servicers. Individual lender overlays, state regulations, and property-specific factors affect eligibility. Consult with a qualified mortgage professional for advice about your specific situation. All financial projections and rental income estimates on this page are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, and regulatory approvals.

More from The Dwelling Index

ADU Financing Options Guide

Compare all paths — HELOC, construction loans, HEIs — by your equity and goals.

How to Finance an ADU With No Equity

Renovation HELOCs and other paths for recent buyers with limited equity.

HELOC for ADU

When a standard HELOC works and when it doesn't — with real math.

Colorado ADU Laws 2026

Zoning rules, permit requirements, and income limits by city and county.

ADU for Aging Parents

Best setups, real costs vs. assisted living, and financing options for families.

Best Prefab ADU Companies

Compared by price, quality, timeline, and delivery area.

© 2026 The Dwelling Index. All rights reserved. For educational purposes only — not legal, financial, or lending advice. Product availability, rates, and program rules change frequently — verify all details directly with lenders before making decisions.