RenoFi vs. HELOC for ADU Financing: Which Path Fits Your Equity?

Bottom Line

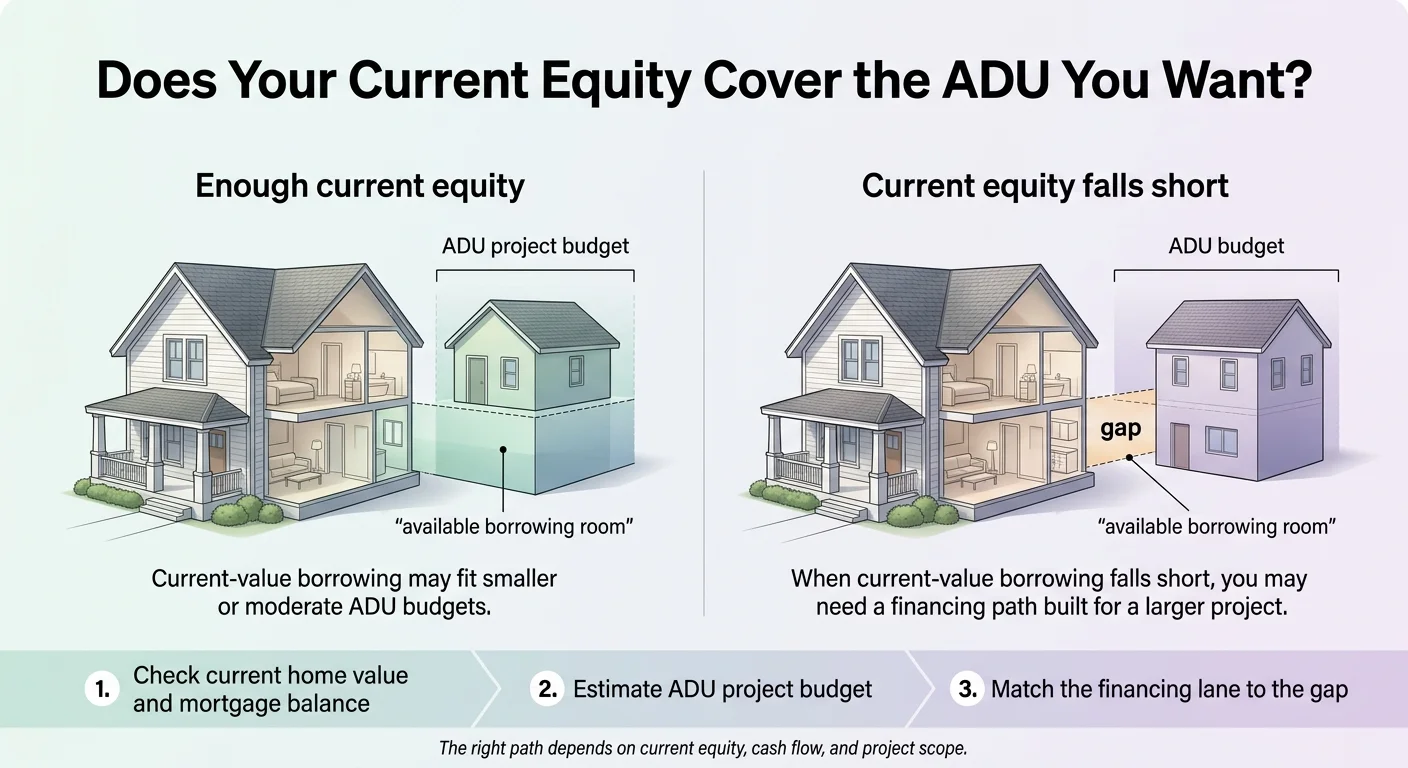

RenoFi vs HELOC for ADU financing comes down to one question — does your current home equity already cover the build? If it does, a standard HELOC is usually the faster, simpler path. Some lenders fund in days. If it doesn't — and it often won't for homeowners who bought in the last five to seven years — RenoFi is usually the stronger option because it underwrites against your home's after-renovation value, not just today's appraised value. The borrowing-power difference can be six figures.

A well-built detached ADU can add 20–30% to a property's appraised value — the core logic behind after-renovation-value financing.

Most ADU financing guides never answer the question you're actually asking: does a standard current-value HELOC cover my build, or do I need future-value borrowing to close the gap? That's what this page resolves. We run the math at four different equity levels below, show you exactly where the fork is, and help you pick the right lane in about 15 minutes.

One thing upfront: ADU permitting and construction timelines aren't instant. Most cities take 4–12 weeks just for plan review, and the build itself typically runs 6–12 months depending on scope and ADU type. That's actually good news for financing — it means you have time to get the right loan in place before a single nail gets hammered. Homeowners who line up financing before breaking ground close faster, avoid stalled projects, and negotiate from a position of strength with contractors.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full affiliate disclosure · Editorial methodology

RenoFi or a Standard HELOC: Which Is Better for Your ADU?

Neither — in the abstract. The right answer depends on a single variable: how much borrowable equity you have right now.

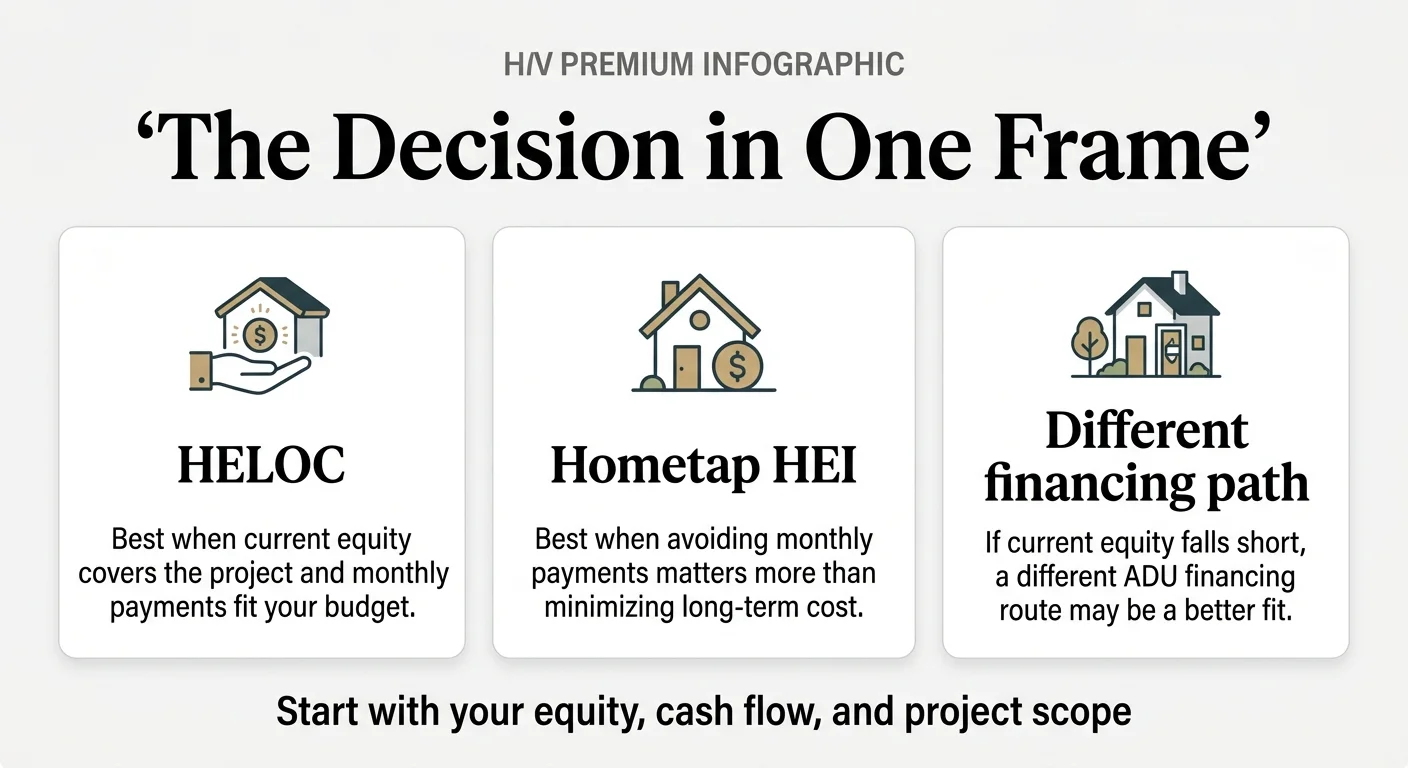

Choose a standard current-value HELOC when your available equity already covers the project and you want the fastest second-lien option. Choose RenoFi when standard HELOC math falls short but the completed ADU should meaningfully increase your home's appraised value.

This isn't “which brand is better?” It's “does current-value borrowing already solve this?”

Here's the quick verdict for three common homeowner profiles:

You've owned for 10+ years and have substantial equity.

A standard HELOC is almost certainly enough. You don't need after-renovation-value underwriting. Get funded, start building.

You bought in the last 3–7 years.

This is the gray zone. Run the math in the next section. A standard HELOC might cover a garage conversion or smaller attached ADU, but a detached new-build will likely outrun your borrowing ceiling. RenoFi becomes relevant here.

You bought recently and you're equity-light.

Standard HELOC math probably produces a borrowing number uncomfortably close to zero. RenoFi — or another after-renovation-value product — is likely your only equity-based path.

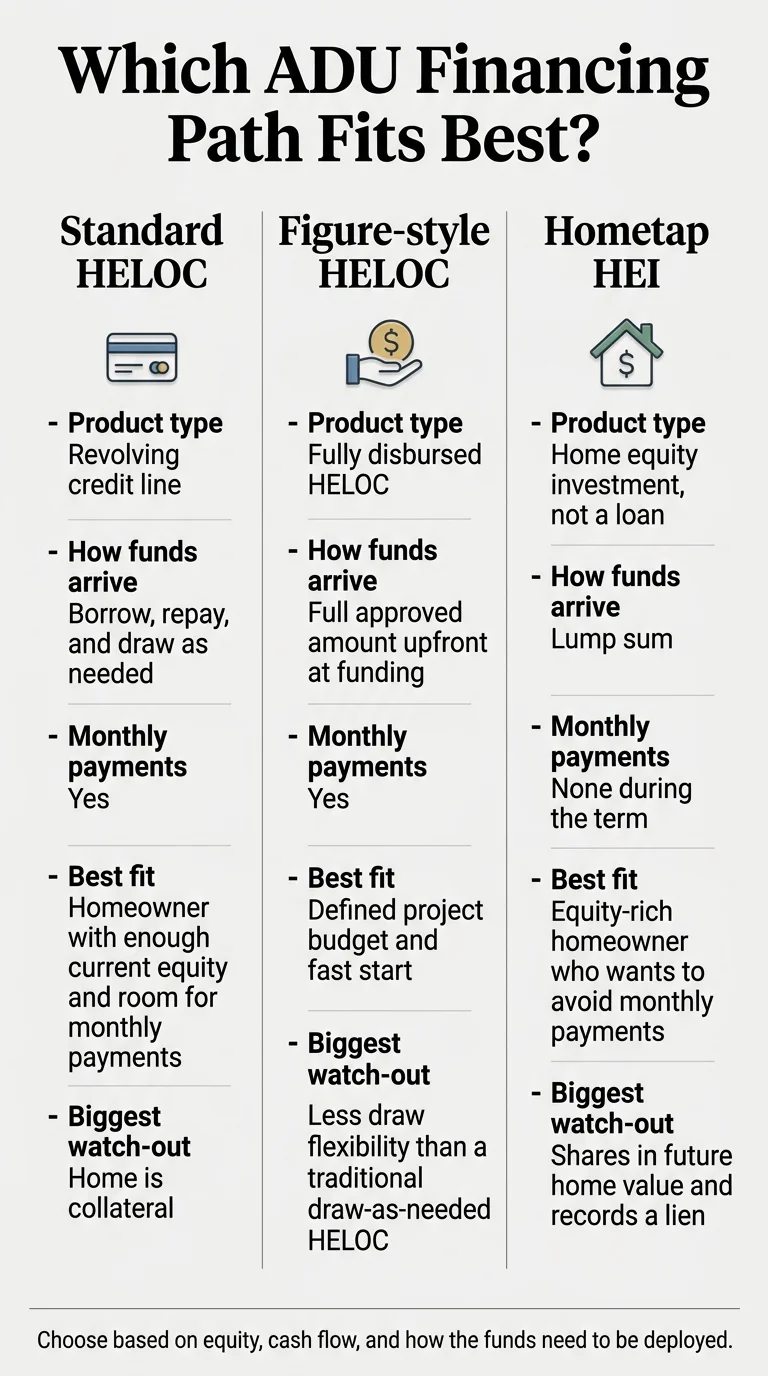

What This Page Means by “Standard HELOC”

Throughout this page, “standard HELOC” means any home equity line of credit that lends based on your home's current appraised value. Figure is a well-known example, but many banks and credit unions offer current-value HELOCs. “RenoFi” refers to RenoFi's after-renovation-value HELOC and loan products specifically, though the same principles apply to any lender using ARV (after-renovation value) underwriting.

The Side-by-Side at a Glance

Affiliate disclosure: This table includes brands we may earn commissions from. See full disclosure. Placement and recommendations are based on independent research, not compensation.

| Standard Current-Value HELOC | RenoFi After-Renovation-Value Financing | |

|---|---|---|

| Borrowing basis | Current appraised home value | Projected value after ADU is complete |

| Typical max LTV | 80–95% of current value (varies by lender) | Up to 90% of after-renovation value (confirm directly with RenoFi) |

| Best for | Homeowners with 30%+ equity who need straightforward funding | Equity-light homeowners whose ADU budget exceeds current HELOC room |

| Keeps your first mortgage? | Yes — second lien position | Yes — second lien position |

| Speed to funding | As fast as 5 days with some lenders (Source: Figure.com, April 2026) | Typically 3–8 weeks (requires appraisal + renovation plan review) |

| Requires renovation plans? | No | Yes — architectural plans and contractor bids needed |

| Disbursement | Varies — some lenders fully disburse upfront, others offer staged draws (see Figure section below) | Draw-based through partner credit unions |

| State availability | Generally nationwide | Most states — verify current availability directly with RenoFi |

| Biggest watch-out | Borrowing limited by current equity; may not cover full ADU cost | Longer timeline; depends on future-value appraisal supporting the projected number |

Sources: Figure.com product pages (reviewed April 4, 2026), RenoFi.com product pages (reviewed April 4, 2026). Terms, availability, and structure vary by lender and state. Confirm details directly before applying.

Choose based on equity, cash flow, and how the funds need to be deployed.

How Much Can You Actually Borrow? The Equity Math Nobody Shows You

This is the section that ends the search for most readers. We run the same property through both formulas at four different equity levels. Find the scenario closest to yours and you'll know your lane in under a minute.

The right path depends on current equity, cash flow, and project scope.

The Two Formulas

Standard Current-Value HELOC

(Home value × max LTV%) − mortgage balance

= borrowing power

We use 85% as the base assumption. Individual lenders range from 80% to 95%. (Source: Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing,” April 2024.)

RenoFi After-Renovation-Value Financing

(After-renovation value × 90%) − mortgage balance

= borrowing power

RenoFi's published materials reference up to 90–95% of after-renovation value. We use 90% as the conservative base. (Source: RenoFi.com, reviewed April 4, 2026.)

The Setup — Same Property, Four Equity Levels

- Current home value: $600,000

- ADU projected to increase value to: $780,000 (30% increase — conservative for a well-built ADU in most markets)

- ADU construction budget: $200,000 (mid-range for a detached ADU)

Actual impact depends on local comp data, ADU type, and market conditions.

| Standard HELOC (85% LTV) | RenoFi (90% ARV) | |

|---|---|---|

| Maximum total debt allowed | $510,000 | $702,000 |

| Minus mortgage balance | −$540,000 | −$540,000 |

| Borrowing power | $0 (already over limit) | Up to ~$162,000 |

| Covers the $200K ADU? | No | Covers most — ~$38K gap remains |

| Standard HELOC (85% LTV) | RenoFi (90% ARV) | |

|---|---|---|

| Maximum total debt allowed | $510,000 | $702,000 |

| Minus mortgage balance | −$450,000 | −$450,000 |

| Borrowing power | ~$60,000 | Up to ~$252,000 |

| Covers the $200K ADU? | No — $140K gap | Yes, with headroom |

| Standard HELOC (85% LTV) | RenoFi (90% ARV) | |

|---|---|---|

| Maximum total debt allowed | $510,000 | $702,000 |

| Minus mortgage balance | −$360,000 | −$360,000 |

| Borrowing power | ~$150,000 | Up to ~$342,000 |

| Covers the $200K ADU? | Tight — covers a modest build or garage conversion | Yes, comfortably |

| Standard HELOC (85% LTV) | RenoFi (90% ARV) | |

|---|---|---|

| Maximum total debt allowed | $510,000 | $702,000 |

| Minus mortgage balance | −$200,000 | −$200,000 |

| Borrowing power | ~$310,000 | Up to ~$502,000 |

| Covers the $200K ADU? | Yes, with over $100K to spare | Yes, with major headroom |

What the Math Tells You

The pattern is clear: the fork happens around 30–40% equity. Below that, standard HELOC math falls short for anything beyond a modest garage conversion. Above it, a standard HELOC can cover most ADU budgets comfortably.

These are illustrative examples, not personalized loan offers. Actual borrowing power depends on your credit score, debt-to-income ratio, lender-specific LTV limits, and the property appraisal. Confirm your specific borrowing capacity directly with a lender before making decisions.

If you just found your scenario and the numbers look workable — that's the moment most homeowners say the project shifts from “someday” to “let's actually do this.” The next step is seeing what's buildable at your specific address.

See What You Can Build at Your Address

Get your free ADU feasibility report in 60 seconds — zoning, setbacks, ADU type, and estimated value add.

Get My Free ADU ReportIs Figure the Same as a Traditional Staged-Draw HELOC?

Not exactly. And this matters for ADU construction.

Most homeowners picture a HELOC as a credit line you draw from gradually — pull $30K when the foundation goes in, another $40K when framing starts, more when the plumber shows up. That's how a classic staged-draw HELOC works, and it's ideal for construction because you only pay interest on what you've actually drawn.

Figure sits on the current-value HELOC side, but its disbursement structure works differently. Figure's published materials describe a model where the full loan amount is disbursed upfront at closing, with the option to redraw funds as you repay principal. Figure offers both fixed-rate and variable-rate structures depending on the product and state. (Source: Figure.com, “What Is a Fixed-Rate HELOC and How Does It Work?,” reviewed April 4, 2026.)

Why This Matters for an ADU Build

Interest cost during construction

With a traditional staged-draw HELOC, you might only be paying interest on $30K for the first two months while the foundation gets poured. With a fully disbursed structure, you're paying on the full amount from day one — even if your contractor won't need the second half for four months.

Cash flow simplicity

On the flip side, having the full amount available immediately simplifies contractor payments and eliminates draw-delay risk. Some contractors actually prefer this because they know the money is there. Neither structure is inherently better.

What to Ask Before You Apply for Any HELOC

These questions apply whether you're looking at Figure, a local bank, or a credit union:

- Do I receive the full amount upfront, or draw as needed?

- When do principal-and-interest payments start?

- Is the rate fixed, variable, or a hybrid?

- Are detached ADUs eligible, or only renovations to the existing structure?

- Do you require contractor bids, building permits, or draw inspections?

- What is the combined loan-to-value maximum?

The answers will tell you more about whether a specific HELOC fits your ADU project than any comparison article — including this one.

When Does a Standard HELOC Beat RenoFi for an ADU?

A standard HELOC wins when the math already works in your favor and you want the simpler path. Here's the checklist:

Your equity already covers the build.

If your current-value borrowing room covers the full ADU budget with a 10–15% buffer for cost overruns, a standard HELOC is faster and less complicated. No renovation plans needed to apply. No future-value appraisal. No extra underwriting steps.

You want speed.

Some standard HELOC lenders approve and fund in days. (Source: Figure.com states applications can take as little as 5 minutes with funding in as few as 5 days, reviewed April 4, 2026.) If your contractor is ready to break ground and you need money quickly, the 3–8 week RenoFi underwriting process may not work with your timeline.

Your project budget is moderate.

Garage conversions and smaller attached ADUs often fall within standard HELOC range for homeowners with 30%+ equity. If the numbers work without future-value borrowing, keep it simple.

You want fewer moving parts.

A standard HELOC is a well-understood financial product. Your bank or credit union probably offers one. The underwriting is straightforward. Sometimes the best financing choice is the one with the fewest complications.

Standard HELOC Wins When (Quick Checklist)

- Your current equity covers the ADU budget plus a 10–15% buffer

- You want funding in days, not months

- You prefer simpler underwriting without renovation-plan requirements

- Your project is a garage conversion, JADU, or smaller attached ADU

- You'd rather deal with a single lender than a broker-plus-credit-union structure

If that checklist matches your situation, you already know your lane. The next step is seeing what current-value HELOC terms look like for your property.

Explore Current-Value HELOC Options

See current rates and terms for standard equity-based HELOC products.

Affiliate disclosure: See full disclosure.

When Does RenoFi Beat a Standard HELOC for an ADU?

RenoFi wins when standard HELOC math leaves you short — and there's a strong case that the finished ADU will meaningfully increase your home's appraised value.

You bought recently and you're equity-light.

This is RenoFi's core use case. If you purchased your home in the last few years and haven't built up significant equity, a standard HELOC might produce borrowing power close to zero. RenoFi's after-renovation-value underwriting changes the math entirely by factoring in what the ADU adds to your property value. (Source: RenoFi.com, reviewed April 4, 2026.)

Your standard HELOC math doesn't cover the build.

Go back to the equity scenarios above. If your borrowing power under a standard HELOC falls $50K, $100K, or $150K short of your ADU budget, that gap is the entire reason RenoFi exists.

You want to keep your first mortgage rate.

Just like a standard HELOC, a RenoFi product sits in second lien position. Your existing mortgage rate and terms stay untouched. For homeowners who locked in rates below 4% during 2020–2021, this alone makes RenoFi worth evaluating over cash-out refinancing or construction-to-permanent loans.

The completed ADU should materially raise your home's value.

RenoFi underwrites against projected post-renovation value. If an appraiser can credibly support that your $200K ADU adds meaningful value to the property, the numbers work. The strength of that appraisal depends on comparable sales data in your area — and in markets where ADU-equipped homes are becoming more common, that data is getting stronger every year.

You have time in your timeline.

RenoFi's underwriting typically takes 3–8 weeks because it involves a dual appraisal plus review of your plans and contractor documentation. If you're still in design or permitting — which is most homeowners at this stage — that timeline works naturally alongside your pre-construction prep.

RenoFi Wins When (Quick Checklist)

- Your standard HELOC borrowing power falls short of your ADU budget

- You bought your home within the last 5–7 years and haven't built much equity

- You want to keep your current mortgage rate

- The ADU should add significant appraised value to your property

- You have 2+ months before construction begins

- You already have (or will soon have) architectural plans and contractor bids

What RenoFi Actually Is

A common misconception: RenoFi is a lender. It's not. RenoFi is a fintech platform that connects homeowners with a network of partner credit unions offering after-renovation-value loan products. RenoFi handles the initial advisory process and pre-qualification, then connects you with a credit union for the actual loan. Think of them as a concierge that prepares you for the right lending partner. (Source: RenoFi.com; Bankrate RenoFi Home Equity Review, February 2026.)

If your equity math came up short in the scenarios above, the renovation-HELOC lane is designed for exactly your situation. Thousands of homeowners have used it to build ADUs they couldn't have financed with a standard HELOC alone.

See If a Renovation HELOC Closes Your Funding Gap

Find out what after-renovation-value financing could unlock for your ADU project.

Affiliate disclosure: See full disclosure.

Can You Use Either Option for a Detached ADU, Garage Conversion, or Attached ADU?

ADU type is the biggest variable in your financing math. Garage conversions and detached new-builds live in different financing lanes.

Yes to both — but project type changes the financing math, and that's what matters.

The cost difference between a $90K garage conversion and a $280K detached ADU is the difference between “standard HELOC handles this easily” and “you probably need future-value borrowing.” Here's the breakdown:

| ADU Type | Typical Budget Range | Standard HELOC Sufficient? | RenoFi More Likely Needed? | Biggest Financing Risk |

|---|---|---|---|---|

| Garage conversion | $80,000–$150,000 | Yes, for most homeowners with 20%+ equity | Rarely, unless very equity-light | Underestimating utility and structural upgrade costs |

| JADU (Junior ADU) | $50,000–$120,000 | Usually, even with modest equity | Rarely needed | Zoning eligibility — not all properties qualify |

| Attached ADU | $120,000–$220,000 | Depends on equity — works for 30%+ | Common for buyers in the 10–25% equity range | Foundation and structural tie-in costs can spike |

| Detached new-build ADU | $180,000–$350,000+ | Only with substantial equity (40%+) | Very common — RenoFi's sweet spot | Budget overruns on site prep, utilities, and permitting |

Budget ranges are national estimates reflecting 2025–2026 construction cost data across metro and suburban markets. Actual costs vary significantly by location, size, finishes, and site conditions. Get contractor bids specific to your project before finalizing your financing approach.

The pattern: as the ADU type gets more complex and expensive, the likelihood that you'll need after-renovation-value borrowing increases. Garage conversions are the easiest to finance conventionally. Detached ADUs are where the financing question gets serious.

See detailed ADU cost ranges by type and locationCan Rental Income, Tax Rules, or the Appraisal Change the Answer?

They can — but not as simply as most blog posts suggest. Here's what's actually verified.

Can Projected ADU Rent Help You Qualify?

For most financing products, no — not if the ADU doesn't exist yet. Standard HELOC lenders qualify you based on your current income and debts. They aren't interested in projections for a unit that hasn't been built.

Here's where it gets nuanced:

Rental income from an existing ADU on the subject property can be used for qualification on a one-unit principal residence for purchase or limited cash-out refinance transactions, capped at 30% of total qualifying income. This applies to properties that already have a rental unit — not ones you're planning to build. (Source: Fannie Mae Selling Guide B3-3.8-01, reviewed April 4, 2026.)

Freddie Mac's guidelines allow borrowers to use ADU income under certain Guide rules. However, for CHOICERenovation mortgages specifically, rental income from a unit included in the renovation project funded by the mortgage proceeds cannot be used to qualify. That's an important restriction many guides miss. (Source: Freddie Mac CHOICERenovation guidelines; Freddie Mac Bulletin 2026-2, February 2026.)

The practical takeaway: finance the build using your current financial position. The rental income comes after it's occupied — and it can meaningfully offset your HELOC payment. In many markets, ADU rents range from $1,200–$2,500/month depending on size, finish level, and location. (Source: Ranges reflect aggregated rental market data; verify with local rental comparables.)

Is HELOC Interest Tax-Deductible for ADU Construction?

Potentially. IRS Publication 936 states that interest on home equity debt may be deductible when the funds are used to “buy, build, or substantially improve” the home that secures the loan. Building an ADU on your property could qualify, but tax law is specific and individual. (Source: IRS Publication 936, reviewed April 4, 2026.)

Consult your tax advisor. The potential deductibility is another reason equity-based financing (HELOC or RenoFi) often makes more sense for ADUs than unsecured personal loans, where interest is generally not deductible.

What If the After-Renovation Appraisal Comes In Low?

This is the risk that doesn't get enough attention in RenoFi marketing. With a RenoFi product, your borrowing power depends on what an appraiser says your home will be worth after the ADU is built. If the appraiser can't find strong comparable sales data for ADU-equipped homes in your area, the projected value may come in lower than expected.

If that happens, your borrowing power shrinks. You'd need to bridge the gap with savings, scale down the project, or explore alternative financing.

The way to manage it: get realistic about your post-ADU value before you apply. Look at recent sales of homes with ADUs in your area. Ask a local real estate agent what the ADU would actually add to your property's market position. If the comparable data is strong — and it's getting stronger as ADU development accelerates in most metro markets — the appraisal will likely support your numbers.

The Honest Downsides of Each Path

We're not going to pretend either option is painless. Here's what we'd want a friend to know.

Standard HELOC Downsides

- Hard borrowing ceiling. The lender doesn't care that your ADU will add significant value. They see what the home is worth today, period.

- Variable rates mean payment uncertainty. Most HELOCs carry variable interest rates. During a multi-month construction timeline, your rate could change. (Source: CFPB, HELOC consumer guide.)

- Your home is collateral. A HELOC uses your home as collateral. If you fall behind on payments, you risk foreclosure. CFPB explicitly warns consumers to understand this before taking on home-equity debt.

RenoFi Downsides

- Process takes weeks, not days. You need architectural plans, contractor bids, and a future-value appraisal before closing. That's 3–8 weeks in most cases.

- Higher closing costs. The dual appraisal, origination fees, and additional underwriting steps mean higher total closing costs than a typical standard HELOC.

- Future-value projection isn't guaranteed. RenoFi's own site states there is no guarantee the renovation will increase your home's value. In rare cases borrowers may owe more than the property is worth.

- State availability varies. RenoFi's product availability and lender programs vary by state. Verify current availability directly before investing time in the application process.

The Tradeoff Matrix

| Risk | Standard HELOC | RenoFi |

|---|---|---|

| Not enough borrowing power | Higher risk if equity is limited | Lower risk — ARV underwriting expands capacity |

| Rate changes during construction | Possible — variable rates are common | Depends on product structure selected |

| Long approval timeline | Low — some lenders fund in days | Expect 3–8 weeks |

| Appraisal doesn't support the numbers | Not applicable (current value only) | Real risk — especially with thin ADU comp data |

| Home as collateral | Yes | Yes |

| Losing your low first-mortgage rate | No — second lien preserves your rate | No — second lien preserves your rate |

Every financing product has downsides. The homeowners who build successfully aren't the ones who found a perfect option — they're the ones who picked the option that best matched their situation and moved forward with clear eyes. You now have the information to do exactly that.

Are All Non-RenoFi HELOCs Capped at 80% of Current Value?

No. The 80–85% current-value cap is the right base assumption for a national educational page, but it's not the complete picture. The lending landscape for ADU-specific products is evolving.

Some credit unions have created specialty ADU HELOC products that blur the line between a standard HELOC and renovation financing. Patelco Credit Union in California, for example, offers an ADU-specific HELOC that can lend up to 125% of current home value and 90% of post-construction value, and may consider projected rental income in qualification. (Source: Patelco.org, ADU Line of Credit product page, reviewed April 4, 2026.)

If you're in a state with heavy ADU activity — California, Oregon, Washington, Colorado — check whether local credit unions have created ADU-specific HELOC products with expanded terms. These may give you more borrowing power than a standard national HELOC without the full complexity of RenoFi's underwriting process.

That said, for most homeowners nationwide, the primary fork remains: standard current-value HELOC vs. after-renovation-value financing. The specialty products are regional exceptions, not the rule.

See all ADU financing paths compared side by sideWhat If Neither RenoFi Nor a HELOC Is the Right Fit?

If both HELOC paths come up short, you still have options. Here are the realistic alternatives, ordered by how commonly ADU builders use them.

Construction-to-permanent loan.

Lends based on after-completion value, similar to RenoFi's logic, but typically replaces your first mortgage rather than sitting in second position. If you're currently at a higher mortgage rate and would benefit from refinancing anyway, this can work well. If you're protecting a sub-4% rate, it's costly.

Fannie Mae HomeStyle Renovation Loan.

Rolls ADU construction costs into a single first mortgage based on as-completed value. Available through many lenders. Fannie Mae's guidelines specifically cover ADU additions. (Source: Fannie Mae Single-Family, Accessory Dwelling Units guidelines, reviewed April 4, 2026.)

Read our Fannie Mae ADU guideFreddie Mac CHOICERenovation.

Similar concept to HomeStyle — finances the renovation based on projected after-completion value. Freddie Mac's guidelines specifically mention ADUs as eligible. Note the rental-income restriction mentioned above. (Source: Freddie Mac CHOICERenovation guidelines.)

Read our Freddie Mac ADU guideFHA 203(k).

A government-backed option combining purchase or refinance with renovation financing. Funds are held in escrow and released as construction progresses. Lower credit score requirements than conventional products, but carries mortgage insurance premiums and more complex draw processes. (Source: HUD 203(k) program guidelines.)

Home equity investment (no monthly payments).

Companies like Hometap, Unlock, Point, and Splitero offer cash in exchange for a share of your home's future equity appreciation — no monthly payments during the term. These are not loans; they're equity investments. Can be a fit for homeowners who are equity-rich but cash-flow constrained — retirees, fixed-income households, or aging-parent use cases. Important: HEI companies have limited state availability that varies by provider. (Source: CFPB, "Home Equity Contracts: Market Overview," January 2025.)

Combination strategies.

Some homeowners piece together funding from multiple sources: a smaller HELOC plus personal savings plus a short-term personal loan for soft costs. Not elegant, but functional.

Prefab ADU with manufacturer financing.

Several prefab ADU companies offer their own financing packages, and the unit cost for a prefab ADU can be significantly lower than site-built construction. The financing need drops substantially when the unit itself costs less.

How to Choose the Right Path in 15 Minutes

Most homeowners waste time talking to lenders before they know their lane. Here's the order of operations.

Start with your equity, cash flow, and project scope.

Run the Equity Math (5 Minutes)

Pull up your most recent mortgage statement. Find your current balance. Look up your home's estimated current value (Zillow, Redfin, or a recent appraisal). Plug both into the formula:

(Current home value × 0.85) − mortgage balance = your standard HELOC ceiling

Compare that number to your ADU budget. If it covers the budget with a 10–15% buffer, you're in the standard HELOC lane. If it falls short, you're in the RenoFi / after-renovation-value lane.

Confirm Your ADU Budget (5 Minutes)

If you don't have contractor bids yet, use the cost ranges in the project-type table above to estimate. Be honest about scope — a garage conversion is not the same budget as a detached new-build with full kitchen and bath.

Check State and Lender Availability (2 Minutes)

Verify that the product you're leaning toward is available in your state. Check directly with the lender — availability changes and we cannot guarantee real-time accuracy for every state and product.

Gather Documents Before You Apply (3 Minutes to Start)

Every lender will want some version of these:

- Recent mortgage statement (current balance and payment)

- Proof of income (pay stubs, tax returns, or bank statements for self-employed borrowers)

- Property details (address, estimated value, property type)

- For RenoFi specifically: architectural plans, contractor bids, and a description of the planned ADU

Ask the Right Questions When You Apply

Don't just fill out the form. Ask these before you commit:

- Do you underwrite on current value or after-renovation value?

- Is this a fully disbursed line or staged draw?

- Is the rate fixed, variable, or a hybrid?

- When do principal-and-interest payments begin?

- Are detached ADUs eligible?

- Can I keep my first mortgage? (Confirm second-lien position.)

- What are the estimated total closing costs?

You've done the work. You know your equity lane, your project scope, and the questions to ask. Most homeowners who get this far say the same thing: “I wish I'd done this math months ago instead of going back and forth.”

The single best next step is finding out what's actually feasible at your specific address — zoning, setbacks, ADU type, and estimated value add — so you can move from “considering it” to “doing it.”

See What You Can Build — Free ADU Report in 60 Seconds

Zoning, setbacks, ADU type, and estimated value add for your specific address.

Get My Free ADU ReportFrequently Asked Questions

Is RenoFi better than a HELOC for an ADU?

It depends on your equity position. If your current home equity already covers your ADU budget, a standard HELOC is simpler and faster. If it doesn't, RenoFi is usually the stronger path because it lends against your home's projected post-ADU value. The right product matches your equity math, not the slickest marketing.

How much equity do I need to build an ADU with a standard HELOC?

Enough that (current home value x 0.85) minus mortgage balance produces a number equal to or greater than your ADU budget. For a $200K detached ADU on a $600K home, that means roughly $90K to $110K or more in borrowable equity. Less than that, and you're likely looking at RenoFi or alternative financing.

Can I use a HELOC to build a detached ADU?

Yes. Most standard HELOC lenders don't restrict how you use the funds. The real question is whether you can borrow enough. Detached ADUs are the most expensive type, and the budget frequently exceeds standard HELOC borrowing power for homeowners with moderate equity.

What if I just bought my house and have no equity?

A standard HELOC almost certainly won't work. RenoFi is designed for this situation -- it uses projected post-ADU value to calculate your borrowing power. If even RenoFi's math falls short, look at Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, or FHA 203(k) renovation loans.

Will RenoFi replace my first mortgage?

No. RenoFi products sit in second lien position, meaning your existing first mortgage stays in place with its current rate and terms.

Can I keep my low mortgage rate with either option?

Yes to both. Standard HELOCs and RenoFi products are both second liens. Your first mortgage rate remains untouched. This is a significant advantage over cash-out refinancing or construction-to-permanent loans.

Can projected ADU rent help me qualify for a HELOC?

Generally not for an unbuilt unit. Fannie Mae allows rental income from an existing ADU on a one-unit principal residence for purchase or limited cash-out refi transactions, capped at 30% of qualifying income. Freddie Mac's CHOICERenovation specifically restricts rental income from units included in the renovation project. Plan to qualify based on your current financial position.

Is HELOC interest tax-deductible for ADU construction?

Potentially. IRS Publication 936 indicates interest may be deductible when used to buy, build, or substantially improve the securing home. Consult your tax advisor for your specific situation.

What happens if the after-renovation appraisal comes in low?

Your RenoFi borrowing power shrinks. If the appraiser can't support the projected post-ADU value -- often because comparable sales data is thin -- you'll need to bridge the gap with savings, scale down the project, or explore alternative financing. Research local ADU comps before applying.

Are there ADU-specific HELOCs besides RenoFi?

Yes. Some credit unions, particularly in California, offer specialty ADU HELOC products with expanded LTV limits. These are regional products, not nationally available. Check with local credit unions in states with heavy ADU activity.

Is Figure the same as a traditional staged-draw HELOC?

Not exactly. Figure's published materials describe a fully disbursed structure where you receive the full loan amount upfront, with the option to redraw as principal is repaid. Figure offers both fixed and variable rate structures depending on product and state. A traditional staged-draw HELOC lets you draw incrementally. Both lend against current value, but the disbursement and interest mechanics differ.

What if I plan to sell the property soon?

Borrowing against your home to build an ADU only makes financial sense if you hold the property long enough to recoup the investment through rental income, value appreciation, or both. If you're planning to sell within a year, the construction timeline alone may not leave enough room. If you sell before paying down the HELOC, the balance comes out of your proceeds.

What if neither RenoFi nor a HELOC fits?

Look at construction-to-permanent loans, Fannie Mae HomeStyle, Freddie Mac CHOICERenovation, FHA 203(k), or home equity investment products. We cover all of them in our complete ADU financing options guide.

What if my lender doesn't allow detached ADU construction?

Some HELOC lenders restrict funds to renovations of the existing structure. Always confirm before you apply. If your lender has this restriction, find one that doesn't -- or explore construction loan alternatives.

Methodology, Sources, and Editorial Policy

How We Compared These Products

This page compares financing paths, not “best lenders.” We used neutral, publicly documented criteria: borrowing basis, typical LTV limits, speed to funding, disbursement structure, state availability, and documented risks. Products are not ranked by who pays us more.

Calculator Assumptions

- Standard HELOC base: 85% of current home value (national midpoint; individual lenders range from 80% to 95%)

- RenoFi base: 90% of after-renovation value (conservative; RenoFi's published materials reference 90–95% depending on product)

- All examples use $600K current value and $780K after-renovation value (30% increase)

- All borrowing-power figures are illustrative estimates, not personalized offers

Sources Cited in This Article

- RenoFi.com — product pages, ADU financing guide (reviewed April 4, 2026)

- Figure.com — HELOC product pages, fixed-rate HELOC guide (reviewed April 4, 2026)

- Urban Institute — "To Increase the Housing Supply, Focus on ADU Financing" (April 2024)

- Consumer Financial Protection Bureau — HELOC consumer guide; "Home Equity Contracts: Market Overview" (January 2025)

- Bankrate — RenoFi Home Equity Review (February 2026)

- IRS Publication 936 — Interest deductibility for home equity loans (reviewed April 4, 2026)

- Fannie Mae Selling Guide B3-3.8-01 — Rental income guidelines (reviewed April 4, 2026)

- Fannie Mae Single-Family — Accessory Dwelling Units guidelines

- Freddie Mac — CHOICERenovation guidelines; Bulletin 2026-2 (February 2026)

- HUD — FHA 203(k) program guidelines

- Patelco Credit Union — ADU Line of Credit product page (reviewed April 4, 2026)

What We Are and What We're Not

The Dwelling Index is an independent educational resource for homeowners planning ADUs. We are not a lender, broker, or financial advisor. We do not originate loans or make lending decisions. Nothing on this page constitutes a personalized loan offer, financial advice, or guarantee of approval or specific outcomes.

The Dwelling Index is reader-supported. When you use our links to explore financing options, request prefab pricing, or purchase floor plans, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full affiliate disclosure · Editorial methodology

Get the Full Picture Before You Start

Our free 2026 ADU Starter Kit includes financing path comparisons, cost ranges by ADU type, a step-by-step planning checklist, and the exact questions to ask every contractor and lender before you sign anything. Over 4,000 homeowners have downloaded it this year.

Download the Free 2026 ADU Starter KitNot sure where to start? See what's possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU ReportLast verified: April 4, 2026. If you notice anything on this page that needs updating, contact our editorial team.