New Silver ADU Loan: 2026 Fit Matrix, Real Requirements, and Better Alternatives

By The Dwelling Index Editorial Team · Last updated · Last verified

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder.

The Short Answer (Read This First)

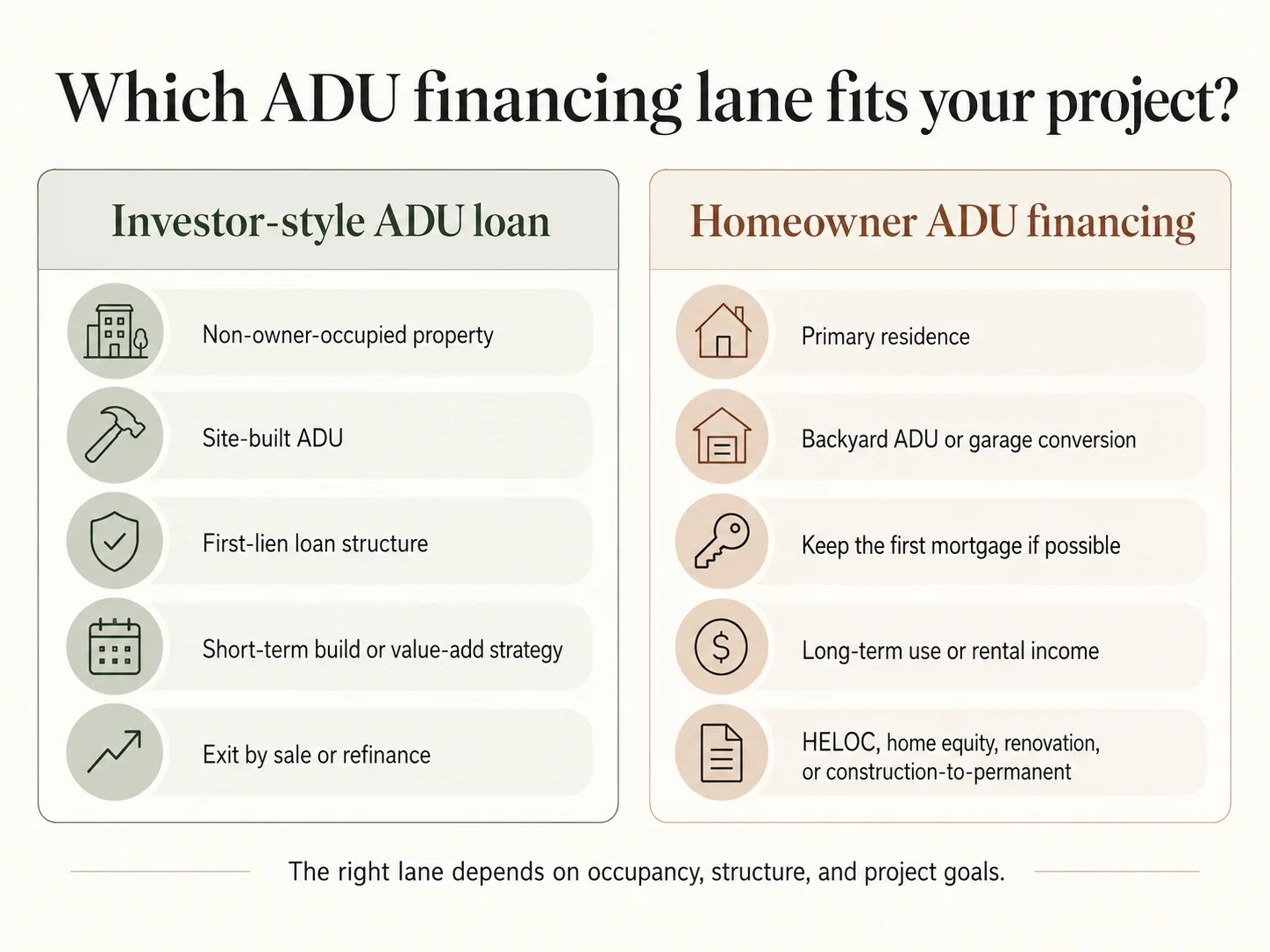

New Silver does not publish a product called an "ADU loan." New Silver Lending LLC is a business-purpose private lender for real estate investors. Its products are Fix & Flip, Rent (DSCR), and Ground Up Construction; its Commercial Real Estate program is currently paused. New Silver's Help Center is explicit that it "does not provide loans against properties that are or will be occupied by their owner."

If you're a homeowner planning to build an ADU on your own property, New Silver is the wrong path. Skip to the homeowner alternatives section below.

If you're a real estate investor building or rehabbing an ADU on a non-owner-occupied property, the Ground Up or Fix & Flip product can fit — but only if the property is site-built, not rural, in one of the 40 states where New Silver lends, you've completed at least one prior project, and you can bring real cash to closing. The full fit matrix is below.

| Your situation | New Silver fit | What to do next |

|---|---|---|

| You'll live in the home and add an ADU for yourself, family, or rental | Not eligible | Compare homeowner ADU financing paths |

| Investor adding a site-built ADU to a non-owner-occupied rental | Possible fit | Check the fit matrix below |

| Prefab, modular, manufactured, or mobile ADU | Not eligible | Prefab ADU financing paths |

| Rural property | Not eligible | Local bank, credit union, USDA route if eligible |

| You need a second lien behind your existing mortgage | Not eligible | HELOC or home equity loan |

| You need 100% total financing (no skin in the game) | Not available | No-equity ADU financing guide |

| You're in AK, ID, MN, NV, ND, OR, SD, UT, VT, Guam, or Puerto Rico | Not eligible | State-specific ADU financing alternatives |

| Louisiana Fix & Flip or Ground Up project | Not eligible (DSCR is okay) | Local investor lender for construction phase |

| Zero completed real estate projects | Not eligible | Partner with experienced co-borrower, or build a track record first |

Verified May 20, 2026 against New Silver Help Center primary sources.

See What You Can Build at Your Address

Get your free ADU feasibility report in 60 seconds. Works for homeowners and investors. Tells you what your specific lot will allow before you spend a dollar on financing.

Get Your Free ADU Report →

Is There Actually a New Silver ADU Loan?

No — not as a separately named product. New Silver publishes investor loan products including Fix & Flip, Rent (DSCR), and Ground Up Construction; its Commercial Real Estate program is currently paused. When investors talk about a "New Silver ADU loan," they almost always mean one of three things: a Ground Up construction loan to build the ADU, a Fix & Flip loan to acquire and add an ADU as part of a value-add play, or a Rent (DSCR) loan to refinance a stabilized property after the ADU is complete and leased.

The New Silver products mapped to ADU use cases

| Product | What it's for | Loan range | ADU relevance |

|---|---|---|---|

| Fix & Flip | Buy + renovate + resell or refinance. Property must be 1–4 units, non-owner-occupied. | $100K min / $5M max | Possible for investor "BRRRR" plays where adding an ADU is part of the rehab strategy. Term up to 18 months per the product page; strategy framed on a 12-month horizon in the Help Center. |

| Rent (DSCR) | Buy or refinance a stabilized rental. 30-year fixed. Rates "starting in the 6s." | $150K min / $3M max | The natural refi destination after the ADU is built, permitted, and rented. Not for construction. |

| Ground Up Construction | New residential construction on shovel-ready 1–4 unit properties. 12-month term, two 3-month extensions available. | $100K min — see note below on max | The most common New Silver fit for investor ADU projects. Eligibility is narrow. |

| Commercial Real Estate | Acquire/rehab/refi multifamily, mixed-use, manufactured housing parks, industrial. | — | Currently paused. New Silver has stated the CRE program is paused with no relaunch date confirmed. |

Source: New Silver Help Center, "What types of loan products do you offer?" and "What is the minimum and maximum loan amount?"; New Silver construction-loan product page.

Why the wording matters

"New Silver ADU loan" is a searcher-created phrase, not a lender-branded product. That's a clue. When you search a brand-plus-product phrase and the brand has no product by that name, you're usually being routed by an algorithm that pattern-matched the topic, not by a real fit. The page you want is the one that tells you which New Silver product (if any) applies — and we built this one for exactly that purpose.

Who New Silver Is a Fit For When the Project Involves an ADU

New Silver is most likely to fit an ADU-related project when all seven of the following are true: the borrower is an investor with at least one prior completed project, the property is and will remain non-owner-occupied, the ADU is site-built (not factory-built), the property is in a state where New Silver lends, New Silver will be in first-lien position, the borrower can bring real cash to closing, and the exit plan is either resale or a stabilized refinance. Miss any one of these and the application stops.

Best-fit scenario #1 — Investor adding a site-built ADU to a non-owner-occupied SFR

This is the cleanest fit. You own a single-family rental in a non-rural area, you're adding a detached or attached site-built ADU to increase rental income and asset value, and you'll either sell the property at a higher post-improvement value or refinance into a long-term DSCR loan once the ADU is built, permitted, and leased. New Silver's Ground Up product covers the construction phase; its Rent product is the natural refi exit. Doing both with the same lender simplifies the handoff.

Best-fit scenario #2 — Shovel-ready ground-up construction

Per New Silver's Help Center, the Ground Up product is "specifically designed for experienced real estate investors looking to finance the construction of brand new dwellings from the ground up" and is "ideal for projects that are ready to break ground." Translated: you have permits in hand, plans approved, contractor lined up, and you're days from breaking ground — not still in the design phase. Lenders fund builds, not concepts. Raw or vacant land without approved plans and permits is not eligible.

Best-fit scenario #3 — Stabilized rental with a completed ADU you want to refinance

If you've already built the ADU using cash, a HELOC, or a different construction lender, and you want to pull equity out and lock long-term financing, New Silver's Rent (DSCR) loan is one of several DSCR products in the market that can refinance the stabilized property. Documented rent from a completed, permitted ADU is part of the property's rental-income picture for DSCR underwriting — verify treatment directly with New Silver before relying on it.

The 12-Point New Silver ADU Fit Matrix

We assembled this matrix from New Silver's own Help Center articles, product pages, and partner FAQ. Every "poor fit" cell is backed by a New Silver-published statement. This is the table that doesn't exist anywhere else on the open web.

| ADU scenario | New Silver fit | Why | Better path if not a fit |

|---|---|---|---|

| Homeowner building ADU on primary residence for parent, adult child, or rental | Not eligible | New Silver Help: "We do not provide loans against properties that are or will be occupied by their owner." | HELOC, home equity loan, cash-out refi, renovation loan, construction-to-permanent |

| Garage conversion in owner-occupied house | Not eligible | Same owner-occupancy exclusion | FHA 203(k), Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, HELOC |

| Investor adding ADU to non-owner-occupied SFR | Possible fit | Aligns with Fix & Flip or Ground Up if site-built, not rural, in-state, and experience meets minimum | Compare with local bank investor construction loan or other DSCR lender |

| Ground-up site-built ADU on investment property | Possible fit | Ground Up product covers shovel-ready new construction on 1–4 unit properties | Construction-to-permanent or local investor construction loan |

| Stabilized rental with completed ADU | Possible fit | Rent (DSCR) loan refinances stabilized properties; 30-year fixed; minimum $150K | Compare DSCR lenders on rate and terms |

| Prefab, modular, manufactured, or mobile ADU | Not eligible | New Silver Help explicitly excludes manufactured, modular, prefabricated, and mobile homes | Prefab ADU financing routes; specialized prefab lenders |

| Rural ADU property | Not eligible | New Silver Help excludes "properties in rural areas" | Local community bank, credit union, USDA route if eligible |

| Borrower wants a second lien (keep first mortgage in place) | Not eligible | New Silver requires first-lien position; no secondary financing per partner FAQ | HELOC or home equity loan |

| Borrower needs 100% total project financing | Not available | New Silver Help: "We do not offer 100% financing." Borrower must bring skin in the game. | No-equity ADU financing guide |

| Zero completed real estate projects | Not eligible | New Silver: "we no longer provide fix and flip loans to borrowers with 0 completed projects." Ground Up requires 2+ projects in past 3 years. | Partner with experienced co-borrower or guarantor; or build a track record on a smaller project first |

| One completed project | Possible — Fix & Flip only | Fix & Flip allows one-project investors with 700+ FICO; Ground Up still requires 2+ | Partner with a 2+ project co-borrower for Ground Up |

| Project in AK, ID, MN, NV, ND, OR, SD, UT, VT, Guam, or Puerto Rico | Not available | New Silver does not lend in these locations | State-specific ADU financing alternatives |

All "Not eligible" and "Not available" rows are sourced to New Silver Help Center articles published or updated through April 2026. Last verified May 20, 2026.

See What You Can Build at Your Address

Get your free ADU feasibility report in 60 seconds. Whether you fit New Silver or not, the first decision is what your lot can actually support.

Get Your Free ADU Report →Who Should Probably Not Use New Silver for an ADU

If you're in any of the categories below, stop reading the New Silver pages and switch tracks. The homeowner ADU financing market is well-developed in 2026; you have options.

Owner-occupied homeowners

Rule: If the ADU is on the home you live in or plan to live in, New Silver is not a path. New Silver's Help Center is explicit: "We do not provide loans against properties that are or will be occupied by their owner." This rules out the most common ADU use case in America — homeowners building a detached or attached ADU in their backyard for an aging parent, adult child, rental income, or future downsizing.

This is by design. New Silver's own Terms describe its business as providing business-purpose loans for investment properties only and explicitly state it does not provide consumer mortgages. What to do instead: Skip down to "Homeowner ADU Financing Paths." Start with HELOC or home equity loan if you have existing equity; renovation loan or construction-to-permanent if you don't.

Prefab, modular, manufactured, or mobile ADUs

The factory-built ADU market is booming — companies like BOXABL, Nest Tiny Homes, Modular Home Direct, and dozens of regional builders deliver units faster and often cheaper than site-built. None of them work as collateral for New Silver. Per New Silver Help, ineligible property types include manufactured homes, modular homes, prefabricated homes, and mobile homes. This is one of the largest blind spots in the "best lenders for ADU" content that ranks today — most generic lender listicles never check whether the lender will actually lend on the type of ADU you're considering. What to do instead: Compare prefab-specific financing routes, or work directly with the prefab builder's recommended lender list.

Rural ADU properties

New Silver's Help Center lists "properties in rural areas" as an ineligible collateral type. Whether a specific property is treated as rural is an underwriting and appraisal judgment, not a sharp geographic line — verify directly before applying if your property is in a low-density area. What to do instead: Local community banks and credit unions are typically the strongest path for rural ADU construction.

Borrowers who want a second lien

New Silver requires first-lien position on the property. From the partner FAQ: New Silver's products require its loan in first lien, with no secondary financing layered on top. If you have a low-rate first mortgage from 2020 or 2021 you do not want to lose, New Silver is not the answer — taking a New Silver loan would mean refinancing the first mortgage and surrendering that rate. What to do instead: A HELOC or home equity loan sits in second lien, leaves your first mortgage untouched, and is the standard play for homeowners protecting a low first-mortgage rate.

Borrowers needing 100% total financing

New Silver's Help Center is direct: "While we will provide as much upfront financing as possible, we do not offer 100% financing." In practice, this means you'll bring cash to closing equal to the gap between (a) the lower of the LTC cap or ARV cap and (b) total project cost plus closing fees. A separate New Silver Help article says construction financing may fund "up to 100% of the construction budget" — that's the construction budget component, not the total project basis. It is not the same as no-money-down financing. What to do instead: True no-equity ADU paths are limited; we cover realistic options in our no-equity ADU financing guide.

Borrowers in states where New Silver does not lend

Per the New Silver Help Center article "What states do we not lend in?", updated April 14, 2026, New Silver is not currently licensed to lend in: Alaska, Idaho, Minnesota, Nevada, North Dakota, Oregon, South Dakota, Utah, Vermont, plus Guam and Puerto Rico. Louisiana has partial availability — DSCR/Rental loans are available, but Fix & Flip and Ground Up construction are not.

| State / Territory | Next path |

|---|---|

| Oregon, Utah | Strong local ADU lending markets thanks to permissive state laws — see our state ADU financing pages |

| Nevada | Local credit unions and community banks for investor construction |

| Idaho, Minnesota, North Dakota, South Dakota | Regional community bank construction lending |

| Alaska, Vermont | Local lender; small markets, fewer options |

| Louisiana | Local investor construction lender for the build; New Silver DSCR works for the post-stabilization refi |

| Guam, Puerto Rico | Local lender required; mainland DSCR market does not extend reliably |

Zero completed real estate projects

This is the single most common disqualifier we see for first-time ADU investors. New Silver's FICO and experience policy is explicit: the company no longer provides Fix & Flip loans to borrowers with zero completed projects. Ground Up requires two or more projects completed in the past three years. A one-project borrower needs 700+ FICO for Fix & Flip. What to do instead: Bring on a co-borrower guarantor with experience and a higher credit score, partner with a general contractor or experienced investor on the project, or start with a smaller cash-funded rehab to build a track record before pursuing investor construction financing.

What New Silver's Published ADU-Relevant Requirements Actually Are

If you've made it past the disqualification gauntlet and New Silver might fit your project, here's the full picture of what the underwriting looks like — sourced directly from New Silver's own published Help Center and product pages.

Ground Up Construction loan — the most ADU-relevant product

| Requirement | Published New Silver figure | Notes |

|---|---|---|

| Loan amount range | $100,000 minimum / $5,000,000 maximum | Source conflict noted above; one Ground Up Help article still lists $3M max. Verify before structuring an upper-end deal. |

| Property type | 1–4 unit residential, shovel-ready, non-owner-occupied | Raw/vacant land without approved plans and permits is not eligible. |

| Borrower citizenship/residency | U.S. citizen or legal resident | Per New Silver construction FAQ. |

| Loan-to-Cost (LTC) | Up to 90% | LTC is the loan as a percentage of total project cost. |

| After-Repair Value (ARV) | Up to 75% | ARV is the appraised value when construction is complete. |

| Interest rate range | 10.25%–11.25% | Published range only; borrower-specific terms require a current term sheet. |

| Origination fee | 1%–2% | Published range only; borrower-specific. |

| Minimum FICO | 650 | Below 650 → declined unless co-borrower guarantor brings higher score. |

| Investor experience | 2+ completed projects in past 3 years | This is the single most common disqualifier for first-time ADU investors. |

| Loan term | 12 months, with 2 × 3-month extensions | Maximum total term is 18 months. ADU permit delays can chew through this. |

| Approval & closing | Instant term sheet; ~7-day closing target with expedited appraisal | Speed advantage versus traditional banks. |

| Payment structure | Interest-only during the loan term | No principal amortization during construction. |

| Credit pull | Soft inquiry to apply | Hard pull occurs later in the process. |

Source: New Silver Help Center, "How does a Ground Up loan work?", "What is the minimum and maximum loan amount?", "What is the minimum FICO score required?", and the current New Silver construction-loan product page. Last verified May 20, 2026.

Fix & Flip loan — second-most-likely ADU fit

| Requirement | Published New Silver figure |

|---|---|

| Loan amount | $100,000 minimum / $5,000,000 maximum; minimum as-is property value $100,000 |

| Term | Help Center frames strategy as buy-renovate-resell/refi within 12 months; current Fix & Flip product page lists terms up to 18 months |

| Property type | 1–4 unit residential, non-owner-occupied |

| Minimum FICO + experience | 650 FICO with 2+ completed projects, OR 700+ FICO with 1 completed project. Zero-project borrowers are not eligible. |

| Use case | Buy + renovate + resell or refi |

The Fix & Flip product makes sense if you're acquiring a property where adding an ADU is part of the rehab — the existing structure needs work, and you'll add an ADU during the same project to maximize rent or sale value. Less rigid experience requirements than Ground Up for one-project borrowers with strong credit, but the 12-month strategic horizon is tight if permits drag.

Source: New Silver Help Center, "What types of loan products do you offer?" and "What is the minimum FICO score required?"; New Silver Fix & Flip product page.

Rent (DSCR) loan — for the refi exit

| Requirement | Published New Silver figure |

|---|---|

| Term | 30-year fixed |

| Rates | "Starting in the 6s" (per New Silver Help, May 2026) |

| Loan range | $150,000 minimum / $3,000,000 maximum |

| Minimum FICO | 660 |

| Property type | Stabilized (no rehab pending), 1–4 unit residential, non-owner-occupied |

Rent (DSCR) is the natural exit if you completed the ADU and have it leased. The 30-year fixed structure is more borrower-friendly than the short-term Ground Up product. Rate sensitivity is high — DSCR rates moved a full 250+ basis points between 2021 and 2024 and remain volatile. Published "starting from" rates are starting rates for the strongest borrower profiles and should not be treated as guaranteed.

Source: New Silver Help Center, "What types of loan products do you offer?" and "What is the minimum and maximum loan amount?"

State availability — the complete map

| State category | States/territories |

|---|---|

| All New Silver products available (40 states + DC) | AL, AZ, AR, CA, CO, CT, DE, FL, GA, HI, IL, IN, IA, KS, KY, ME, MD, MA, MI, MS, MO, MT, NE, NH, NJ, NM, NY, NC, OH, OK, PA, RI, SC, TN, TX, VA, WA, DC, WV, WI, WY |

| Partial — DSCR/Rental only | Louisiana |

| No lending | AK, ID, MN, NV, ND, OR, SD, UT, VT, Guam, Puerto Rico |

Source: New Silver Help Center, "What states do we not lend in?" Updated April 14, 2026.

Documentation New Silver typically requires

- Purchase and sale contract (if acquiring) or current payoff (if refinancing)

- Construction budget with line items

- Liquidity statement (bank statements showing ability to cover down payment and reserves)

- Proof of experience (HUD-1s or closing statements from past projects)

- Entity documents (LLC operating agreement, EIN, certificate of formation)

- Property insurance binder (builder's risk during construction)

- For Rent product: signed leases or market rent appraisal (Form 1007 equivalent)

ADU-specific documents we recommend preparing

New Silver may not request all of these directly, but underwriters and appraisers will ask:

- Approved permit set or permit application status

- Architectural plans for the ADU

- Site plan showing setbacks, FAR (floor area ratio) compliance, parking

- Contractor bid and license verification

- Utility connection plan (water, sewer, electric — utility lateral work is often the most variable single line item)

- Existing structure condition report if attaching or converting

- Exit plan documentation: rent comps for stabilization, or comps for resale

The faster you produce these, the faster you close. New Silver's published target is approximately 7 days for Ground Up closes with expedited appraisal — that target is achievable only when documentation is ready before application.

Download the Free ADU Starter Kit

18-page worksheet covering feasibility, financing checklist, and capital stack template. Built so you walk into your lender call with the questions answered, not asked.

Get the Free Starter Kit →Questions to Ask New Silver Before You Apply

If you're past the fit matrix and ready to talk to a loan officer, save yourself a week by asking these specific questions upfront. They surface the most common deal-killers.

- Will my ADU project be underwritten as Ground Up, Fix & Flip, or Rent? The product determines everything else — rate, term, draw schedule, experience requirement. Don't let the lender pick later.

- Will the appraisal treat my property as rural? Get a preliminary read from the lender before ordering the appraisal. If they think it might come back rural, you save $600+ and a week of waiting.

- Will the ADU be classified as prefab, modular, or manufactured? Some "site-built ADUs" use panelized factory components. Confirm classification up front.

- Which maximum loan amount applies — the $3M Help article number or the $5M min/max number? Get the current binding figure in writing on the term sheet.

- Does my completed-project history satisfy the experience requirement for the product I'm applying for? Be specific — number of projects, dates, addresses, role (principal vs. co-investor).

- Can the completed ADU's projected rent be used in the Rent/DSCR refinance? Confirm how they'll document it (signed lease, market rent appraisal, vacancy factor treatment).

- What's the LTC and ARV cap on this specific deal, and which one is binding? This determines your cash gap.

- What's the realistic close timeline given my documentation readiness and appraisal complexity? The 7-day target is for clean, simple files.

What We Verified

Verified on May 20, 2026

- ✓ New Silver currently publishes Fix & Flip, Rent (DSCR), and Ground Up Construction loan products. The Commercial Real Estate program is currently paused.

- ✓ New Silver does not provide loans against properties that are or will be occupied by their owner.

- ✓ New Silver does not lend on manufactured, modular, prefabricated, mobile, or rural-area properties.

- ✓ Ground Up construction loan: $100K minimum; 90% LTC; 75% ARV; 650 FICO minimum; 2+ completed projects required; 12-month term with two 3-month extensions; 10.25%–11.25% published interest rate range; 1%–2% published origination range. Source conflict: $3M max per the Ground Up Help article; $5M max per the min/max loan Help article and current construction-loan page. Verify with lender before structuring an upper-end deal.

- ✓ Fix & Flip: $100K minimum / $5M maximum; 650 FICO with 2+ projects OR 700 FICO with 1 project; zero-project borrowers not eligible; term up to 18 months per the product page.

- ✓ Rent (DSCR) loan: 30-year fixed; rates "starting in the 6s"; $150K minimum / $3M maximum; 660 FICO minimum.

- ✓ New Silver does not offer 100% financing.

- ✓ Non-lending states: AK, ID, MN, NV, ND, OR, SD, UT, VT, plus Guam and Puerto Rico. Louisiana is DSCR-only.

- ✓ Borrowers must be U.S. citizens or legal residents. Raw/vacant land without approved plans and permits is not financed.

- ✓ New Silver has a public affiliate program; Dwelling Index does not have an active affiliate relationship with New Silver as of this writing.

- What we did not verify directly: specific borrower-level pricing (varies by file), exact ADU rental-income treatment in DSCR calculation (verify with lender), and grant-program details (verify directly with state agencies before relying on them).

How Does New Silver Compare With Homeowner ADU Financing Options?

This is the section most "New Silver ADU loan" searchers actually need. If you're owner-occupied, here's how the realistic homeowner paths compare side by side, organized by which specific constraint each path resolves.

Affiliate disclosure: The Dwelling Index is reader-supported. Some links on this page are affiliate links. If you click one and take a qualifying action, we may earn a commission at no extra cost to you. Affiliate relationships do not influence our editorial rankings or conclusions. Read our full disclosure.

| Financing path | Best for | Resolves which New Silver disqualifier? | Main advantage | Main drawback |

|---|---|---|---|---|

| HELOC (Home Equity Line of Credit) | Homeowner with 20%+ equity who wants to keep first mortgage | Owner-occupied + second-lien needs | Keeps low first-mortgage rate; pay interest only on what you draw | Variable rate; limited to existing equity; second-lien |

| Home equity loan | Homeowner wanting fixed second-lien debt | Owner-occupied + wants fixed payment | Fixed rate, predictable payment, lump sum | Pricing depends on lender and market; still capped by existing equity |

| Cash-out refinance | Homeowner willing to replace first mortgage | Owner-occupied + has no rate-protected first mortgage | Single mortgage; long amortization | Replaces existing first-mortgage rate (often the deal-killer in 2026) |

| Renovation loan (Fannie HomeStyle, Freddie CHOICERenovation) | Homeowner whose current equity won't cover the project | No current equity + owner-occupied | Lends against as-completed value, not current value | More documentation, draw process, contractor approval |

| Construction-to-permanent loan | Larger new-build ADU scope | Owner-occupied + larger scope than renovation loan limits | One closing; converts to permanent mortgage at completion | Complex underwriting; lender list is narrower |

| FHA 203(k) | FHA-eligible homeowner adding/renovating with limited equity | No current equity + lower down payment | Lower down payment threshold; ADU-eligible per recent HUD policy | FHA overlays; mortgage insurance; lender list limited |

| RenoFi-style ARV loan | Homeowner without enough equity for HELOC | No current equity + wants second-lien | Up to 90% after-renovation value through third-party lender network; preserves first mortgage | Availability varies by state and lender; check current options |

| New Silver investor loan | Non-owner-occupied investor project | Resolves nothing for owner-occupants | Speed (~7-day target close) and LLC-friendly | Not available to owner-occupants; experience required |

Explore Mortgage-Backed ADU Financing Options

Compare HELOC, cash-out refi, and construction loan options through our mortgage research partner. Best for owner-occupied homeowners; investors should use the fit matrix above.

Compare Homeowner ADU Financing →

The honest order of operations for homeowner ADU projects in 2026

- First, calculate your existing equity. If you have enough to cover the project with a HELOC at ~80% combined loan-to-value (CLTV), this is usually the first lane to test — it protects your first mortgage. Most homeowners who bought before 2022 with appreciation can use this lane.

- If you don't have enough equity but have strong income, a renovation loan (Fannie HomeStyle or Freddie CHOICERenovation) lends against the post-ADU value — the most powerful structural tool homeowners have.

- Cash-out refi only if your existing first mortgage rate is at or above current market rates. If your rate is below 4.5%, replacing the first mortgage is often the deal-killer; run the full debt-stack math before choosing cash-out refi.

- Construction-to-permanent loans make sense for larger or more complex builds where renovation loan limits won't cover the scope.

How Much Cash Do You Actually Need Before a New Silver ADU Project Closes?

This is where the "90% LTC" headline gets reality-checked. A worked example.

Scenario: Investor acquiring a non-owner-occupied SFR in Sacramento, CA, planning a 750 sq ft detached ADU as part of the project.

| Line item | Amount (illustrative) |

|---|---|

| Property acquisition price | $475,000 |

| ADU hard construction costs (750 sq ft) | $262,500 |

| Site work (utilities, foundation, grading) | $35,000 |

| Soft costs (permits, design, surveys, impact fees) | $22,500 |

| Total project basis | $795,000 |

| Estimated ARV (appraised value when ADU is complete and leased) | $950,000 |

| 90% LTC cap | $715,500 |

| 75% ARV cap | $712,500 |

| Maximum New Silver loan (lower of the two caps) | $712,500 |

| Origination fee (2% midpoint of published 1%–2% range) | $14,250 |

| Borrower cash required at closing (before reserves and closing costs) | ~$96,750 |

That's the gap between the maximum loan and the project basis, plus the origination fee. Add typical closing costs (title, escrow, appraisal, legal) and lender-required liquid reserves of 3–6 months of debt service, and the realistic cash need before closing is comfortably into six figures.

For an investor with that level of liquidity who can move fast on a deal, New Silver's value is real — the alternative is a traditional bank construction loan that typically takes substantially longer to underwrite. For an investor without that liquidity, New Silver's "skin in the game" requirement is the wall.

Note on rates: New Silver's current construction-loan product page publishes an interest rate range of 10.25%–11.25% and an origination fee range of 1%–2%. These are published ranges for the strongest borrower profiles and current market conditions — borrower-specific pricing requires a current term sheet from New Silver. Rate ranges shift with the broader market.

See What You Can Build at Your Address

Run your project's real numbers. Our free ADU feasibility report shows what your specific lot will allow, expected ADU size, and budget range — the inputs every lender will ask for.

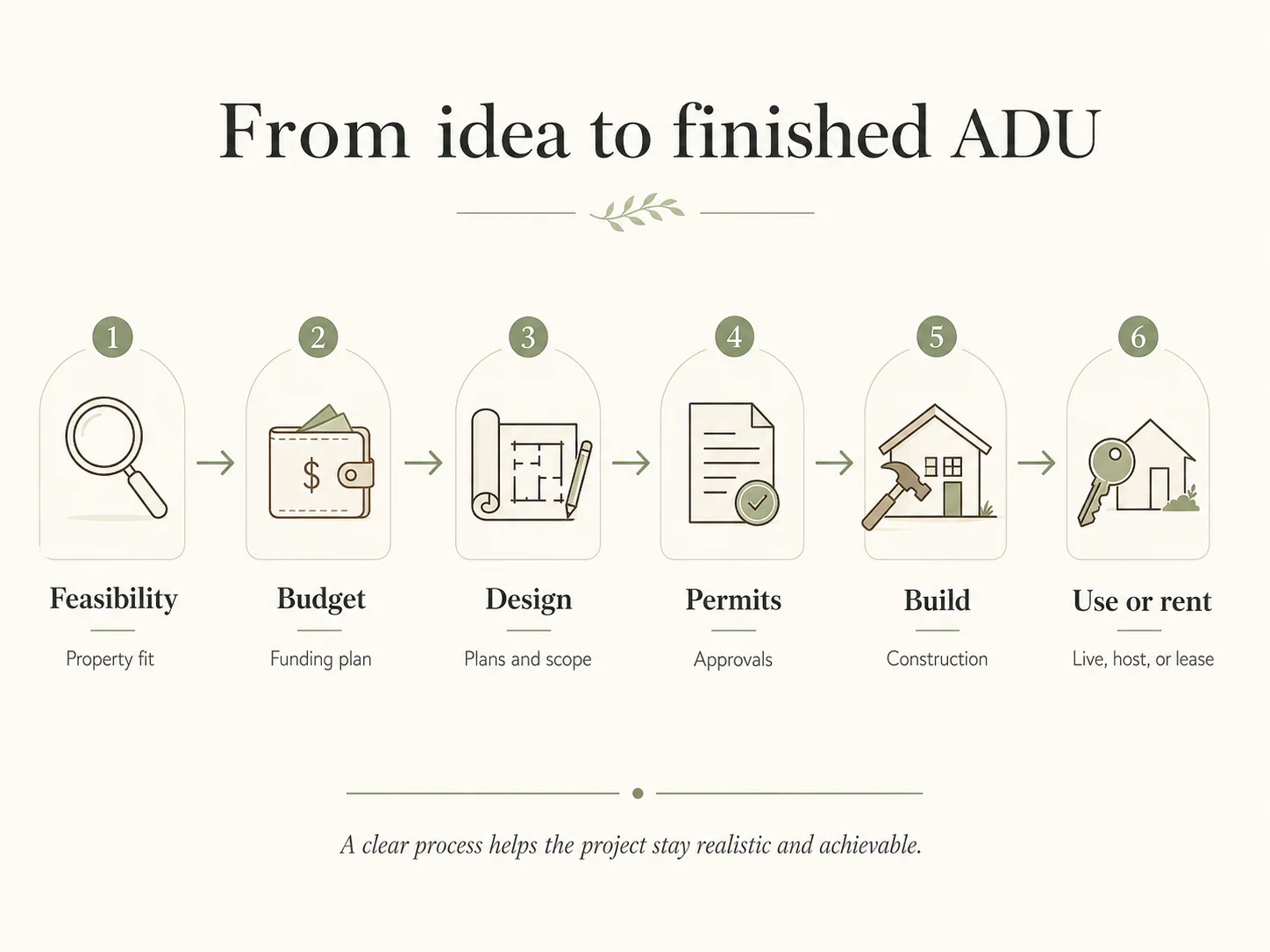

Get Your Free ADU Report →How Does an Investor ADU Capital Stack Work With New Silver?

For investors who fit New Silver's box, the ADU project is rarely a single loan. It's a capital stack across multiple phases. The full investor ADU project typically runs five phases over 18–24 months from acquisition to long-term financing — not the 12-month base term of the construction loan alone. Understanding this prevents the most common project failure: running out of construction-loan term before stabilizing rent and refinancing.

Phase 1: Acquisition (if not already owned)

Either cash, a separate acquisition loan, or — most common with New Silver — bundling acquisition + rehab + ADU construction into a single Ground Up or Fix & Flip loan.

Phase 2: Construction

Ground Up (or Fix & Flip with construction component). 12-month term, with 2 × 3-month extensions available. Interest-only payments. Funds released via draw schedule against documented progress milestones — typically foundation, framing, dry-in, mechanical rough-in, drywall, and final.

Phase 3: Certificate of Occupancy and lease-up

After construction completes and the city issues the certificate of occupancy (CO), you can begin marketing the ADU. Lease-up typically takes weeks to months depending on the rental market. The clock on your construction loan is still running.

Phase 4: Stabilization and seasoning

Most DSCR lenders require documented rental history (or a signed lease with verifiable terms) before they'll refinance into a long-term DSCR loan. This "seasoning period" is the most-missed risk in investor ADU planning. Verify your refi lender's seasoning requirement before closing the construction loan.

Phase 5: DSCR refinance

Refinance into a 30-year fixed DSCR loan (New Silver's Rent product, or another DSCR lender). Pull equity out at the new appraised value. Lock long-term rates. Pay off the Ground Up loan.

Phase 6 (optional): Portfolio loan rollup

Once you have 3+ stabilized rentals with ADUs, some lenders offer portfolio loans that consolidate multiple individual DSCR loans into a single facility with better terms.

Run Your Project's Numbers

Use our free ADU feasibility report to see what your specific lot can support, including realistic project budget and timeline inputs you can hand to your lender.

Get Your Free ADU Report →How Fast Can New Silver Close on an ADU-Related Loan?

New Silver's published closing target is approximately 7 days for a Ground Up loan with expedited appraisal, per the Help Center. Their Help Center also states Fix & Flip and Ground Up loans can close in as little as 5 days with expedited appraisal in optimal cases. New Silver's homepage describes an average 10-day close.

That speed advantage is real and is the single strongest reason investors choose New Silver over a traditional bank construction loan. In a competitive market where you need to close on a purchase quickly to win a deal, New Silver's published timing can be the difference.

What slows down even a New Silver close:

- Permit status uncertainty — if the ADU permit is not yet issued, expect underwriting questions

- Incomplete construction budget — line items are non-negotiable

- Appraisal disputes on ARV — if your number and the appraiser's number diverge, you re-negotiate the loan amount

- Rural property classification — if the appraisal calls the property rural, underwriting can decline

- Entity formation in progress — you can apply without an LLC, but funds will close in an entity name per New Silver Help

- Title or lien issues — existing liens, easements, encroachments

- State availability gap — if the property is in a non-lending state, the application can't progress

- Prefab/modular collateral — same answer; can't progress

- Zero project history — the application stops at the experience screen

The pattern in all of these: speed of close depends entirely on whether the deal fits the box. Deals inside the box close fast. Deals outside the box don't close at all.

What Are the Biggest Risks of Using New Silver for an ADU?

The biggest risks are using a short-term business-purpose loan for a project that actually needs long-term homeowner financing, missing one of New Silver's hard exclusion criteria, underestimating the cash gap, and assuming an ADU refinance or rental exit will work before permits, appraisal, rent, and local rules are verified.

Risk #1 — Wrong borrower type

The biggest mistake is owner-occupied homeowners treating New Silver as a normal ADU mortgage path. The application will close at the disqualification gate. Time wasted. Read the property eligibility before applying.

Risk #2 — Project type mismatch

Prefab, modular, manufactured, mobile, or rural — none of these collateral types work. If you're shopping for a prefab ADU and you saw New Silver in a "best lenders" listicle, the listicle didn't check.

Risk #3 — Construction loan timeline risk

The 12-month base term with two 3-month extensions (18-month maximum) is tight. If permitting in your city takes months and construction takes more months, you may be at or past the maximum before stabilization. Build a realistic timeline first, then size the loan term and exit plan accordingly.

Risk #4 — Refi exit risk

Your construction loan exit depends on the DSCR refi appraising at or above ARV, the ADU being permitted with a CO in hand, and stabilized rent supporting DSCR underwriting. Any one of these failing — appraisal comes in low, CO is delayed, rent doesn't hit comps — and you're either extending the Ground Up loan or selling.

Risk #5 — Borrower cash gap

New Silver does not offer 100% financing. The cash gap between 90% LTC / 75% ARV and total project basis is real. If you're entering a deal hoping the loan will cover everything, you'll discover at term-sheet time that it won't.

Risk #6 — State and product gap risk

The nine no-lending states, plus Guam, Puerto Rico, and Louisiana's partial availability, shape investor strategy. If you're building a portfolio in Oregon or Utah, New Silver doesn't help; you need a state-licensed investor construction lender.

Risk #7 — Experience gate

Zero-project borrowers are not eligible for Fix & Flip or Ground Up. One-project borrowers need 700+ FICO for Fix & Flip and still don't qualify for Ground Up. Bring on an experienced co-borrower or partner — don't apply hoping the underwriter will make an exception.

Still investor-fit? Check current New Silver terms directly.

We don't have an affiliate relationship with New Silver, so this is a direct, non-monetized referral.

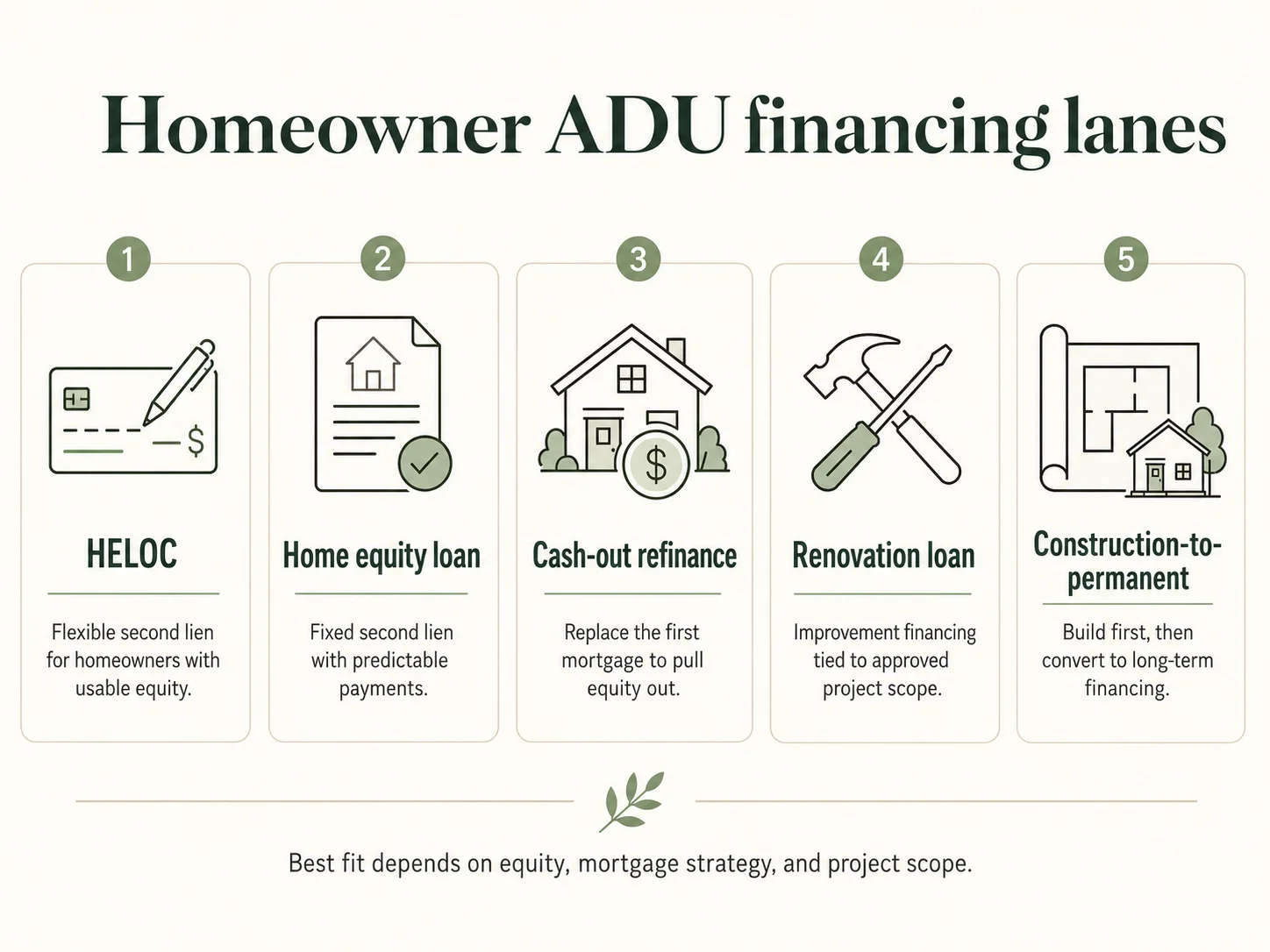

What Should a Homeowner Use Instead If New Silver Is the Wrong Fit?

This is the section we'd want to read if we landed here as an owner-occupied homeowner. The decision tree is roughly this.

Step 1 — Do you have enough existing equity?

Calculate your current home's market value. Subtract your current mortgage balance. The difference is your equity. Most HELOCs and home equity loans cap at 80% combined loan-to-value (CLTV), so usable equity is roughly:

If usable equity covers your ADU project budget, HELOC or home equity loan is usually your shortest path — it protects your first mortgage. HELOC if you want flexibility and variable rate; home equity loan if you want fixed rate and lump sum.

Step 2 — Not enough equity? Look at as-completed value loans.

Renovation loans (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation) and specialty products like RenoFi lend against the post-ADU appraised value, not the current value. These products are the single most powerful structural tool for homeowners whose current equity won't cover a project.

A homeowner with $80,000 in usable equity facing a $200,000 ADU project is stuck on a HELOC. The same homeowner with the same project, using a HomeStyle Renovation loan that values the home at $700,000 post-ADU, can often access materially more capital.

Note on Fannie Mae ADU rules: Fannie's ADU guidelines allow rental income from a single ADU to be considered for qualification on certain transactions through HomeStyle Renovation, construction-to-permanent, and HomeReady (for existing ADUs). Important limits: Fannie does not permit ADUs with 2–4 unit primary dwellings, with manufactured-home primary residences, or with multiple ADUs on the same property. Verify your specific transaction structure with a lender. Source: Fannie Mae Single Family ADU guidance.

Step 3 — Construction-to-permanent loans for larger scope

For larger ADU projects (1,000+ sq ft, high-end finishes, complex utility work), construction-to-permanent loans handle the construction draw structure and convert to permanent financing at completion — single closing, single set of fees. Local credit unions and regional banks often have the strongest products for ADU work.

Step 4 — FHA 203(k) for FHA-eligible borrowers

The FHA 203(k) program supports ADU-related improvements. HUD's 2023 policy update expanded ADU rental-income treatment in qualifying scenarios and clarified ADUs as eligible improvements under Standard 203(k). FHA 203(k) requires FHA mortgage insurance and uses an approved 203(k) consultant for the rehab plan, but the down payment threshold is friendlier than conventional construction loans. Detached new-construction ADUs need careful fit analysis — check the dedicated FHA 203(k) ADU guide for current eligibility rules. Source: HUD FHA Info Messages 2022–2023.

Step 5 — Cash-out refinance — only if your existing rate is at or above market

Cash-out refinance replaces your first mortgage. In 2026, most homeowners with a sub-5% existing rate should think hard before refinancing. Cash-out refinance makes sense if your current rate is at or above the current market rate, you want long amortization, and you want to consolidate financing into a single mortgage.

Step 6 — Grant programs (state-specific, often limited, never count on them)

State and local ADU grant programs have been popular news but unreliable in funding. A snapshot, verified May 20, 2026:

- California's CalHFA ADU grant (the $40K reimbursement program) was fully allocated in December 2023 and remains closed to new reservations. Beware of scammers claiming to help access funds. (Source: CalHFA program update.)

- MassHousing Accessory Dwelling Unit Loan Program (ADULP) is active for income-eligible Massachusetts homeowners who own and occupy a single-family home as their primary residence and have plans and permits in hand. Up to $250,000 for detached ADUs and up to $150,000 for attached ADUs. (Source: MassHousing ADULP program page.)

- Colorado / CHFA has ADU finance programs (loans, credit enhancements, rate buydowns) rolling out through 2026. Eligibility, lender participation, and income restrictions vary; verify current program details directly with CHFA before relying on them. (Source: CHFA and Colorado OEDIT.)

If you're in one of those states, check current status — but don't structure your project around a grant.

Get Your Free ADU Feasibility Report

Answer 8 questions, see what's possible at your address — zoning, financing paths, and budget range tailored to your lot. Works whether you're a homeowner or investor.

Get Your Free ADU Report →

Frequently Asked Questions

Does New Silver have an ADU loan?

No, not as a separately named product. New Silver publishes Fix & Flip, Rent (DSCR), and Ground Up Construction; its Commercial Real Estate program is currently paused. For an investor ADU project, the Ground Up product is the most likely fit; Fix & Flip if the ADU is part of a broader rehab; Rent if you're refinancing a property where the ADU is already built and leased.

Can I use New Silver to build an ADU on my primary residence?

No. New Silver's Help Center states the lender "does not provide loans against properties that are or will be occupied by their owner." Owner-occupied projects need homeowner financing paths — HELOC, home equity loan, renovation loan, construction-to-permanent, or FHA 203(k).

Can New Silver finance a prefab, modular, or manufactured ADU?

No. New Silver explicitly excludes manufactured, modular, prefabricated, and mobile homes from eligible collateral. For prefab ADU financing, work with the prefab builder's recommended lender list or specialty prefab financing routes.

Does New Silver do 100% ADU financing?

No. New Silver Help Center: "We do not offer 100% financing." A separate Help article notes that construction budget may be funded up to 100%, but that's a different concept than total project financing. Borrower equity is required.

What credit score does New Silver require?

Per the New Silver FICO article: Ground Up requires 650 FICO; Fix & Flip requires 650 FICO with 2+ projects or 700 FICO with 1 project; Rent requires 660 FICO. Below these thresholds, you may bring on a co-borrower guarantor with a higher score.

What's the minimum number of completed projects to qualify with New Silver?

Ground Up requires 2+ completed projects in the past 3 years. Fix & Flip requires 2+ projects at 650 FICO or 1 project at 700+ FICO. New Silver no longer provides Fix & Flip loans to borrowers with 0 completed projects.

Does New Silver require an LLC?

You can apply without an LLC, per the New Silver Help Center. But Fix & Flip, Ground Up, and Rent loans must close in an entity name — so you'll need to form an LLC before funding.

What states does New Silver lend in?

New Silver lends in 40 states plus DC, with all products available. Louisiana is DSCR-only. Non-lending states: Alaska, Idaho, Minnesota, Nevada, North Dakota, Oregon, South Dakota, Utah, Vermont — plus Guam and Puerto Rico.

Is New Silver better than a HELOC for an ADU?

They serve different audiences and aren't directly comparable. New Silver is investor / business-purpose financing for non-owner-occupied projects. A HELOC is a homeowner second-lien product for owner-occupied properties.

Can New Silver close faster than a bank construction loan?

New Silver publishes a target close of approximately 7 days for Ground Up loans with expedited appraisal — among the fastest in the market. Traditional bank construction lending typically takes substantially longer for investor projects, though timing varies by lender.

Does ADU rental income count toward DSCR calculation?

For DSCR underwriting, documented rent from a completed, permitted ADU is part of the property's rental-income picture. The exact treatment varies by lender — verify New Silver's specific Rent/DSCR treatment of ADU rental income directly before relying on it.

What's the difference between LTC and ARV in a New Silver Ground Up loan?

LTC (Loan-to-Cost) is the loan as a percentage of total project cost (acquisition + construction + soft costs). ARV (After-Repair Value) is the appraised value when the project is complete. New Silver caps Ground Up at 90% LTC and 75% ARV. They calculate both and lend the lower of the two.

What happens after the ADU is built?

Investor borrowers refinance into a long-term loan (often a DSCR product like New Silver's Rent, or a competitor DSCR lender), sell the improved property, or hold and continue to rent. Homeowners typically retain the property and either house family or generate rental income — the long-term mortgage was already locked in via the construction-to-permanent or renovation loan structure.

A Note on Sourcing and Methodology

We built this guide from New Silver's own published Help Center articles, product pages, and partner FAQ as primary sources for any claim about New Silver. Where we cite a specific figure (rate, LTC, FICO, loan size, state availability), the source is a New-Silver-published page, identified by URL in the source notes below. We re-verified each source on May 20, 2026, and surfaced source conflicts (Ground Up max loan amount, Fix & Flip term) transparently rather than picking one number.

We used Fannie Mae, Freddie Mac, FHA/HUD, and primary state agency sources (CalHFA, MassHousing, CHFA Colorado) for any claim about homeowner mortgage alternatives, agency renovation products, or state programs. We used third-party lender review sites only as cross-checks, not as primary sources for New Silver facts.

Editorial judgments labeled as such ("best fit for," "most common disqualifier") are conclusions drawn from the verified facts above. They are not promises of approval, terms, or returns. Run your own underwriting math, talk to the lender directly, and verify rates and terms at application — they change.

Source notes

- New Silver Help Center: "What types of loan products do you offer?" — https://help.newsilver.com/en/articles/3230272

- New Silver Help Center: "What types of property can you lend against?" — https://help.newsilver.com/en/articles/3614102

- New Silver Help Center: "How does a Ground Up loan work?" — https://help.newsilver.com/en/articles/3683500

- New Silver Help Center: "What is the minimum and maximum loan amount?" — https://help.newsilver.com/en/articles/3230275

- New Silver Help Center: "What is the minimum FICO score required?" — https://help.newsilver.com/en/articles/3230261

- New Silver Help Center: "What states do we not lend in?" — https://help.newsilver.com/en/articles/14616683

- New Silver Help Center: "Do you do 100% financing?" — https://help.newsilver.com/en/articles/4530441

- New Silver Help Center: "Do you provide construction financing?" — https://help.newsilver.com/en/articles/3653911

- New Silver Help Center: "Do I need an LLC or an entity to apply?" — https://help.newsilver.com/en/articles/5557898

- New Silver Help Center: "What type of documentation is required?" — https://help.newsilver.com/en/articles/3653917

- New Silver Help Center: "How do I calculate the maximum loan amount?" — https://help.newsilver.com/en/articles/5445111

- New Silver Help Center: "How fast can you close?" — https://help.newsilver.com/en/articles/9630560

- New Silver Construction Loan product page — https://newsilver.com/construction-loan/

- New Silver Affiliate Program — https://newsilver.com/affiliate-program/

- Fannie Mae ADU guidance — singlefamily.fanniemae.com

- HUD FHA Info Messages 2022–2023 (ADU policy update) — hud.gov

- CalHFA ADU program status — calhfa.ca.gov

- MassHousing ADULP program page — masshousing.com

- Colorado CHFA / OEDIT ADU finance programs — oedit.colorado.gov

- RenoFi — renofi.com

Not sure where to start?

See what's possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Report →