HELOC for ADU: When It Works, When It Doesn’t, and What to Do Next

Independent ADU resource · Not a lender or broker

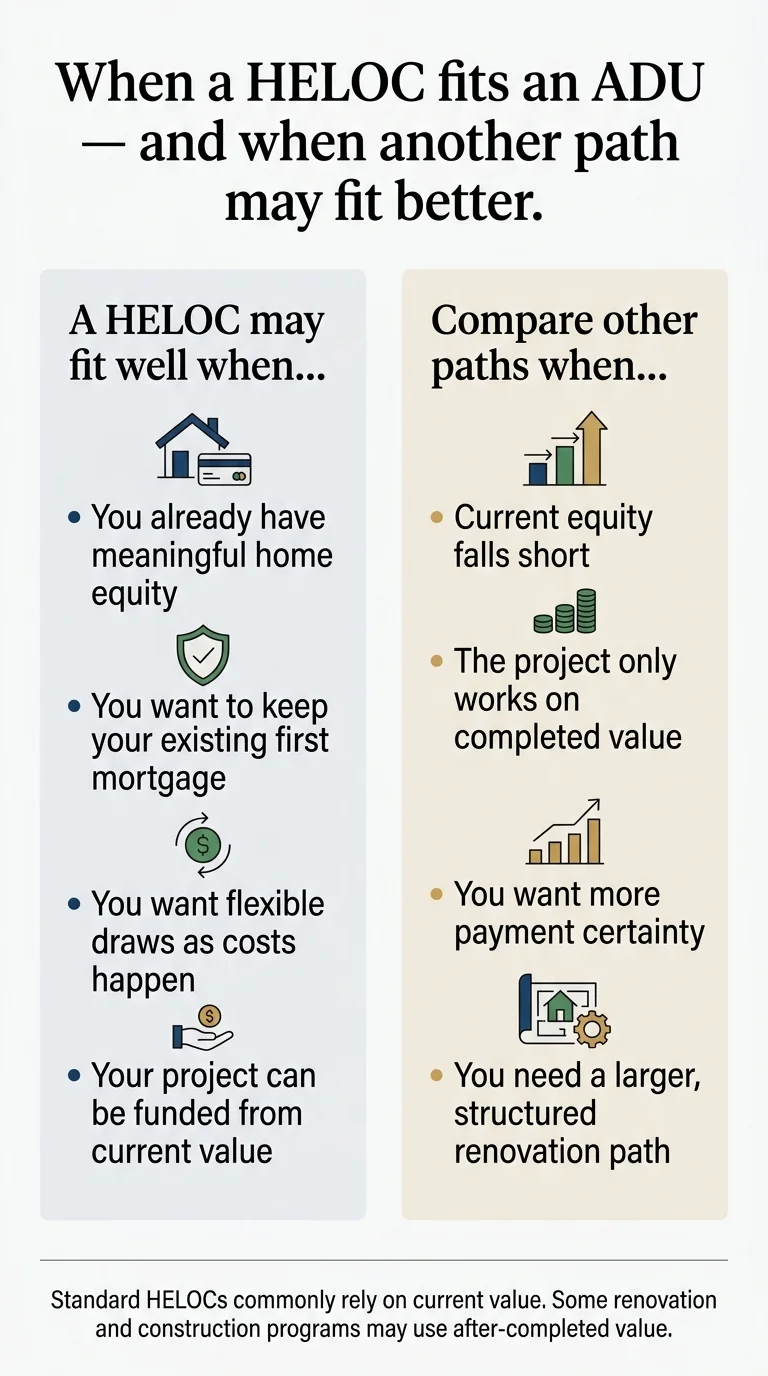

A HELOC for ADU construction can be a strong fit when you already have meaningful home equity, want to draw funds in stages as permits and building unfold, and don’t want to replace your existing first mortgage. Among homeowners who use mortgage products for ADU financing, 56% choose a HELOC or home equity loan — making home-equity-based financing the dominant strategy by a wide margin.

But here’s what most guides won’t tell you upfront: a standard HELOC only works if your current equity is large enough to cover the project. If the finished ADU’s future value is the only reason the numbers pencil out, a standard HELOC is usually the wrong first move — and a renovation or construction loan that underwrites to completed value may get you further. That distinction — current value vs. after-completed value — is the single most important decision in ADU financing, and most pages bury it 3,000 words deep.

We won’t do that. Below is the full decision framework: who a HELOC fits, who it doesn’t, how much equity you actually need, what the real risks are, and exactly which alternative path to explore if a HELOC falls short.

(Source: Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing,” April 2024. Verified March 2026.)

Independent educational resource. The Dwelling Index is not a lender, broker, or builder. We research financing paths so you can make an informed decision. Read our editorial standards →

Quick Verdict: Which ADU Financing Path Fits You?

Before we go deeper, find yourself in this table. It takes 30 seconds and may save you weeks of applying for the wrong product.

| If this sounds like you | Usually the best first look | Why | Biggest watch-out |

|---|---|---|---|

| Strong current equity + low first mortgage you want to keep | HELOC | Flexible draws match phased construction costs. Your first mortgage stays untouched. | Variable rate. Your home is collateral. |

| Strong equity + want fixed, predictable payments | Home equity loan | Lump sum with a fixed rate. No payment surprises. | Less flexible if costs shift during construction. |

| Limited current equity — project only works on completed value | Renovation or construction loan | Underwrites to what your home will be worth with the ADU, not just today’s value. | More paperwork, longer approval, and may replace your first mortgage. |

| Want one loan and your existing mortgage rate isn’t sacred | Cash-out refinance | One payment, potentially large lump sum. | Replaces your first mortgage entirely — you lose your current rate. |

| Some cash on hand and only a moderate gap | Cash + smaller HELOC | Reduces borrowing, lowers risk, keeps reserves partly intact. | Depletes some liquid savings. |

Can You Use a HELOC to Build an ADU?

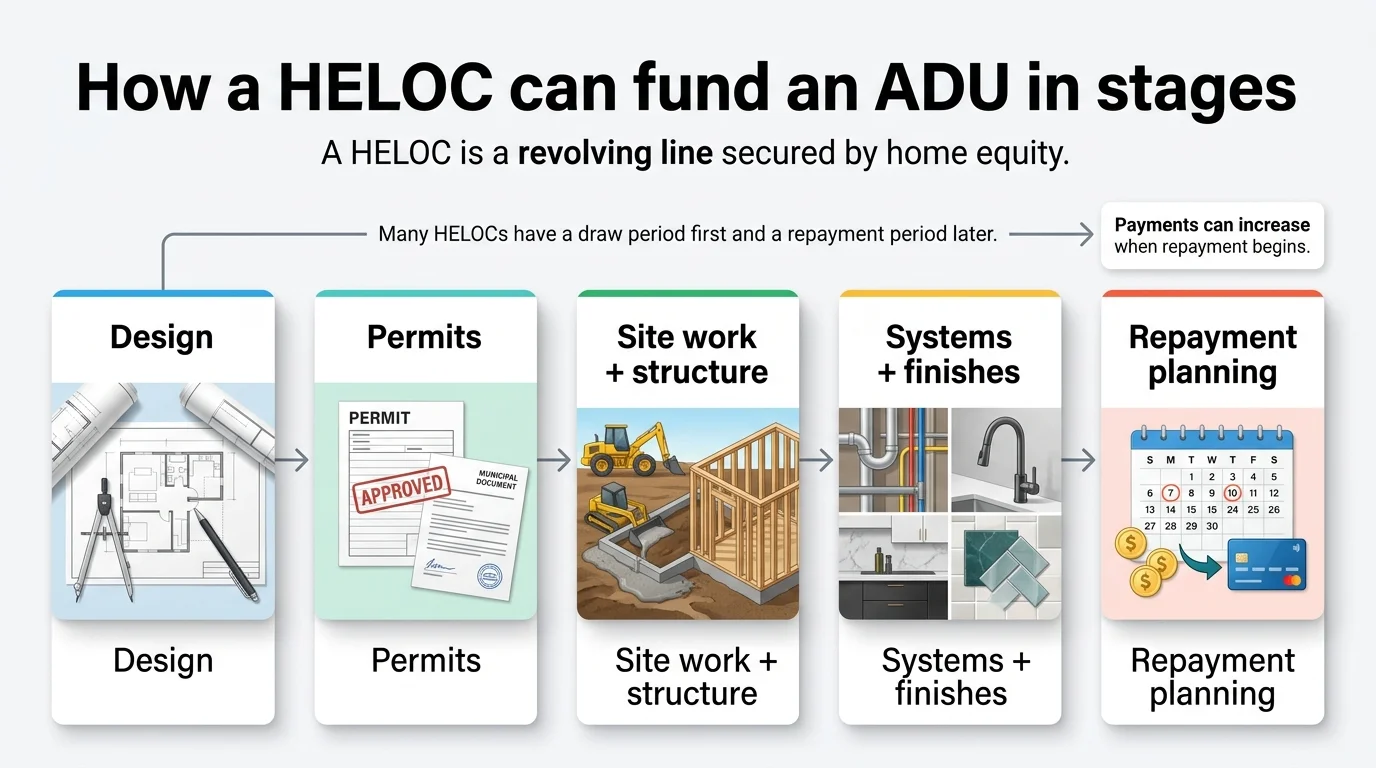

Yes. A HELOC is a revolving line of credit secured by your home’s equity. You get approved for a maximum amount, then draw against it as needed — similar to a credit card, but at a much lower variable interest rate because your home backs it.

This structure is why HELOCs have become the go-to for ADU construction. ADU costs don’t hit all at once. They arrive in phases: design, permitting, site prep, foundation, framing, mechanical systems, finishes. A HELOC lets you pull exactly what each phase requires and — with many HELOC products — pay interest only on what you’ve actually drawn rather than a full lump sum.

Why a HELOC Matches Phased ADU Costs

Here’s a simplified example of how draws might work on a $200,000 HELOC for a detached ADU project:

| Construction phase | Draw amount | Running total borrowed | You’re paying interest on |

|---|---|---|---|

| Design + permits | $15,000 | $15,000 | $15,000 |

| Site prep + foundation | $50,000 | $65,000 | $65,000 |

| Framing + rough systems | $60,000 | $125,000 | $125,000 |

| Finishes + final inspections | $45,000 | $170,000 | $170,000 |

Total project cost: $170,000. You were approved for $200,000 but only borrowed $170,000 — and you paid interest on that full amount only during the final phase. With a lump-sum loan, you’d have been paying interest on the entire $200,000 from day one.

Note: HELOC draw and repayment structures vary by lender. Some products allow interest-only payments during the draw period; others may require partial principal, minimum draws, or an initial draw at closing. Always confirm your specific lender’s terms.

When the Answer Becomes “Not Yet” or “Not This Way”

A standard HELOC may not be the right tool if:

- You don’t have enough current equity. Most lenders cap your combined loan-to-value (CLTV) around 80–85% of your home’s current appraised value. If your remaining equity isn’t enough to cover ADU costs, you’ll need a product that underwrites to completed value instead.

- You’re highly sensitive to rate changes. HELOC rates are typically variable and tied to the Prime Rate. If rates rise meaningfully, your payments rise with them.

- You’re planning to sell the property soon. A HELOC adds a lien. If you sell before the ADU pays for itself, the math may not work.

- Your reserves are thin. Construction almost always costs more than the initial estimate. If you have no cushion beyond the HELOC itself, one overrun could put you in a difficult position.

None of these are permanent dealbreakers. They just mean you need a different financing path — and we’ll cover every alternative below.

Is a HELOC the Right Fit for Your ADU — or Is Another Path Smarter?

The answer depends almost entirely on one thing: how much current equity you have relative to what your ADU will cost.

When a HELOC Is Usually the Best Fit

A standard HELOC tends to work well when you’ve owned your home for several years, have paid down a meaningful chunk of your mortgage, and your home has appreciated. If you can tap enough equity at a typical CLTV cap to cover your ADU budget — and still have reserves — a HELOC gives you the most flexibility with the least friction.

It also wins when you care about preserving your first mortgage rate. If you locked in at 2.5–3.5% during 2020–2021, replacing that with a higher-rate refinance just to pull cash is an expensive trade. A HELOC sits as a second lien alongside your existing mortgage. Your original loan stays untouched.

When a Home Equity Loan May Be the Better Fit

If you have strong equity but want payment predictability, a home equity loan (HEL) offers a fixed rate and a lump sum. You’ll know exactly what your payment is from month one. The trade-off is less flexibility — you borrow the full amount upfront even if construction hasn’t started yet, and you pay interest on all of it immediately. For homeowners who have a locked-in contractor bid and want zero surprises on the financing side, a HEL can feel safer than a variable-rate HELOC.

When a Cash-Out Refinance Makes Sense

If your existing mortgage rate isn’t particularly low — or if you have very high equity and a low or zero mortgage balance — a cash-out refinance consolidates everything into one loan. You replace your current mortgage with a larger one and pocket the difference as cash for the ADU. The clear downside: you’re replacing your existing mortgage terms entirely. For homeowners sitting on a sub-4% rate, this is usually a non-starter.

When Renovation or Construction Financing Wins

This is the option most HELOC guides skip — and it’s the one that matters most for homeowners who don’t have enough current equity.

A renovation loan (like Fannie Mae HomeStyle or Freddie Mac CHOICERenovation) or a construction-to-permanent loan underwrites based on your home’s after-completed value — what the property will be worth once the ADU is finished. That’s a fundamentally different calculation than a standard HELOC, which only looks at today’s value.

If your home is worth $400,000 today with a $300,000 mortgage, a standard HELOC at 80% CLTV gives you only $20,000 — nowhere near enough for most ADU projects. But a renovation loan that appraises the completed project at $520,000 could open up significantly more borrowing power.

Fannie Mae explicitly allows its products to be used for adding an ADU. Freddie Mac’s CHOICERenovation program specifically names converting a garage or outbuilding into an ADU as an eligible project. FHA’s updated policies clarify ADUs as eligible for Standard 203(k) rehabilitation loans and allow projected rental income in certain qualifying scenarios — though FHA does not allow ADU rental income to be counted for cash-out refinances.

Sources: Fannie Mae Single Family ADU page; Freddie Mac CHOICERenovation guidelines; HUD Mortgagee Letter 2023-17. Verified March 2026.

When Paying Partly in Cash Lowers Your Risk

If you have savings but not enough to cover the full project, consider splitting: pay a portion in cash and take a smaller HELOC for the gap. This reduces your monthly obligation, keeps more equity untouched, and creates a buffer if costs run over. The downside is obvious — you’re deploying savings that could earn returns elsewhere. But for homeowners who want to minimize debt exposure, this hybrid approach often hits the sweet spot between risk and cost.

How Much Equity Do You Actually Need?

This is where most homeowners get stuck — and where most guides get vague. Let’s do the actual math.

The Formula

(Home’s current appraised value × lender’s max CLTV) − existing mortgage balance = maximum HELOC

CLTV caps vary by lender. The 80–85% range is common for standard HELOCs, though some specialty products go higher.

Three Homeowner Scenarios

| Scenario A: Long-term homeowner | Scenario B: Mid-equity homeowner | Scenario C: Recent buyer | |

|---|---|---|---|

| Home value | $600,000 | $450,000 | $400,000 |

| Mortgage owed | $180,000 | $310,000 | $350,000 |

| Current equity | $420,000 (70%) | $140,000 (31%) | $50,000 (12.5%) |

| Max CLTV at 80% | $480,000 | $360,000 | $320,000 |

| Max HELOC | $300,000 | $50,000 | −$30,000 (does not qualify) |

| Enough for most ADUs? | Yes — covers virtually any ADU type | Likely too low for detached build; may cover garage conversion | Does not qualify for a standard HELOC |

| Best path | Standard HELOC | Cash + small HELOC, or renovation/construction loan | Renovation loan (HomeStyle, 203(k)) or construction loan |

These are illustrative examples, not guarantees of borrowing capacity. Actual amounts depend on your lender’s requirements, credit profile, income, and local property values.

Why So Many Homeowners Hit a Borrowing Gap

The Urban Institute identified this as one of the central barriers to ADU development nationwide: the gap between what a homeowner can borrow against current value and what ADU construction actually costs. Standard HELOCs work beautifully for homeowners with deep equity. But for younger homeowners, recent buyers, or anyone who purchased near peak prices with a small down payment, the math often doesn’t reach.

That doesn’t kill the project. It just means you need to start with a product designed for that exact situation — and those products exist.

(Source: Urban Institute, “To Increase the Housing Supply, Focus on ADU Financing,” April 2024. Verified March 2026.)

Free ADU Report

Not sure if your equity covers your ADU plan? Find out in 60 seconds.

See what you can build at your address — zoning, feasibility, and the financing paths that match your lot.

What Does It Take to Qualify for an ADU HELOC?

Beyond equity, lenders evaluate several factors. Requirements vary by lender and property type, so treat these as general guideposts — not universal rules. Ask each lender for their exact thresholds before you apply.

Credit score

Lender minimums vary, but credit scores of 680+ generally position you well for competitive terms. Higher scores (740+) open access to the most favorable structures. Some lenders work with lower scores, often with tighter CLTV caps.

Debt-to-income ratio (DTI)

Lenders evaluate whether your total monthly debt payments — including the projected HELOC payment — stay within their DTI limits. Caps typically fall in the 43–50% range of gross monthly income. Don’t assume projected ADU rental income will count toward qualifying on a standard HELOC.

Income and employment stability

Lenders want to see consistent income. W-2 employees typically provide pay stubs and tax returns. Self-employed borrowers usually need two years of tax returns.

Appraisal

Your lender will order an appraisal to confirm your home’s current value. For ADU-specific HELOCs involving construction management, the appraisal process may be more involved.

| Qualification factor | General guideposts | What strengthens your position |

|---|---|---|

| Credit score | Lender-specific; 680+ positions you well | Pay down revolving debt, correct report errors |

| DTI ratio | Typically under 43–50% (varies by lender) | Reduce existing monthly obligations |

| Equity (CLTV) | Commonly 80–85% max; some go higher | Longer ownership, mortgage paydown, home appreciation |

| Income documentation | W-2s, pay stubs, or 2 years of tax returns | Stable employment history, consistent earnings |

Sources: Alliant Credit Union HELOC guidelines; Patelco ADU HELOC program; CFPB HELOC guide. Verified March 2026.

Will a HELOC Actually Cover Your ADU Budget?

Your HELOC amount means nothing in isolation. It matters relative to what your ADU will cost — and ADU costs vary enormously depending on what you’re building, where, and whether you’re working with existing structure or starting from scratch.

| ADU type | Typical cost range | Standard HELOC likely covers it? | If there’s a gap |

|---|---|---|---|

| JADU (interior conversion, under 500 sq ft) | $40,000–$80,000 | Usually yes, even with moderate equity | — |

| Garage conversion | $80,000–$180,000 | Yes, if you have 40%+ equity | Cash supplement or renovation loan |

| Attached ADU | $150,000–$300,000 | Often yes with strong equity; tight with moderate equity | Renovation or construction loan |

| Detached ADU (new build) | $200,000–$400,000+ | Only with very strong equity | Renovation loan, construction loan, or partial cash + HELOC |

Cost ranges reflect 2024–2026 national averages; your local market may be higher or lower. For detailed cost breakdowns, see our ADU cost guide → and cost per square foot analysis →. Always get project-specific bids before committing to a financing amount.

The Hidden Costs That Blow Budgets

When estimating whether your HELOC covers the project, make sure your budget includes items that contractors sometimes present as add-ons or exclusions:

- Permit fees and plan review costs (varies widely by municipality)

- Utility connections — sewer, water, electrical, gas (can be significant for a detached ADU)

- Site work — grading, drainage, hardscaping, landscaping restoration

- Design and architectural fees

- Surveying costs

- Impact fees (required in some jurisdictions)

These “soft costs” can add meaningfully on top of the construction bid. Account for them before you finalize your borrowing amount.

Why Do Homeowners Use a HELOC for ADU Construction?

If a HELOC fits your equity position, the advantages are real and practical:

You keep your current first mortgage.

This is the big one. If you locked in at a historically low rate, a HELOC lets you access equity without sacrificing those terms. Your first mortgage stays exactly as-is. The HELOC sits alongside it as a separate second lien.

You draw only what you need, when you need it.

ADU construction is unpredictable. With a HELOC, you pull funds as each phase demands — and you’re not paying interest on money sitting idle in your account.

Many HELOCs allow interest-only payments during the draw period.

A common HELOC structure includes a 5–10 year draw period where you may only be required to pay interest on the outstanding balance — though not all products work this way. Confirm your lender’s specific draw-period terms before relying on this structure.

The application is often simpler than a construction loan.

Construction loans typically require approved contractor documentation, detailed plans, and staged inspections by the lender. A standard HELOC is generally faster to close and less paperwork-intensive.

Sources: CFPB guide on HELOCs; Patelco ADU HELOC program documentation. Verified March 2026.

That said, convenience is not the same thing as best fit. The flexibility of a HELOC is an advantage only if you have the equity and discipline to use it well.

What Are the Real Risks of Using a HELOC for an ADU?

Every competitor page breezes through this section. We won’t. If we’re going to help you evaluate a financial product that uses your home as collateral, you deserve the full picture — plus a clear plan for managing each risk.

Payment Shock After the Draw Period

How to manage it: Know exactly when your draw period ends and what your repayment terms will be before you sign. Calculate what the principal + interest payment will look like. Ideally, have the ADU generating rental income or refinance into a fixed-rate loan before repayment kicks in.

(Source: Consumer Financial Protection Bureau, “What is a home equity line of credit?” Verified March 2026.)

Variable-Rate Exposure

How to manage it: Some lenders offer fixed-rate HELOC options or fixed-rate conversion features. Ask about these before you close. At minimum, stress-test your budget at 1–2 percentage points above your starting rate.

Your Home Is the Collateral

How to manage it: Never borrow the maximum just because you qualify for it. Keep an emergency fund separate from your HELOC. Build your ADU budget with a 15–20% contingency buffer. If the rental income plan falls through, you need to be able to service the debt from your regular income.

The Lender Can Freeze or Reduce Your Credit Line

How to manage it: Don’t plan construction phases that depend on draws you haven’t secured yet. Build in a cash cushion. Consider drawing slightly ahead of need during critical construction phases, keeping the excess in a dedicated project account.

(Source: Consumer Financial Protection Bureau. Verified March 2026.)

Construction Cost Overruns

How to manage it: Get detailed, itemized bids from at least two contractors. Add a 15–20% contingency. A HELOC’s flexible draw structure actually helps here — you can access additional funds up to your credit limit if needed, which is harder with a fixed lump-sum loan.

Appraisal Complications

How to manage it: Work with lenders experienced in ADU properties. Proactively provide comparable sales data showing ADU properties in your area. Fannie Mae’s appraisal guidelines (Selling Guide, Section B4-1.3-05) instruct appraisers to identify and describe the ADU and adjust for it — but execution varies by appraiser.

Now — all of those risks are real. And none of them mean “don’t build an ADU.” They mean go in with your eyes open, your numbers tested, and your exit planned. Homeowners who do that consistently come out ahead.

Free ADU Report

See what you can build at your address — get your free ADU report in 60 seconds.

See what you can build at your address — zoning, feasibility, and the financing paths that match your lot.

How Does the Rental Income Math Actually Work?

This is the question that turns caution into action. The cash-flow picture varies by market and project — but the mechanics are consistent.

The General Pattern

During the draw period, your HELOC payment may be interest-only (depending on your terms). In many rental markets, a well-located ADU generates monthly rent that can cover a substantial portion — or all — of that interest-only payment. This is especially true in markets with strong rental demand.

Once the repayment period begins and you’re paying principal and interest, the monthly obligation increases. Over time, rents typically trend upward while a fixed repayment schedule stays level — especially if you refinance to a fixed rate after construction.

The Timeline to Think About

Year 1 (construction)

No rental income yet. HELOC interest payments come from personal funds.

Years 2–5 (draw period, ADU rented)

Rental income begins. The offset depends on your local market and HELOC balance — but many homeowners in competitive markets find the ADU covers a meaningful share of the payment.

Years 5–10 (if repayment begins)

Payments increase. Consider refinancing to a fixed-rate loan. Rental income continues to help, and the ADU has been building property value the entire time.

Long term

Between rental income, property appreciation, and potential tax benefits, a HELOC-funded ADU can be a strong wealth-building move. The key is surviving the construction period and having a clear exit strategy for when the draw period ends.

These are illustrative scenarios, not guarantees of returns. Actual results depend on local rental market conditions, construction costs, your specific loan terms, and regulatory factors. Research comparable ADU rents in your area before building a financial plan around rental income.

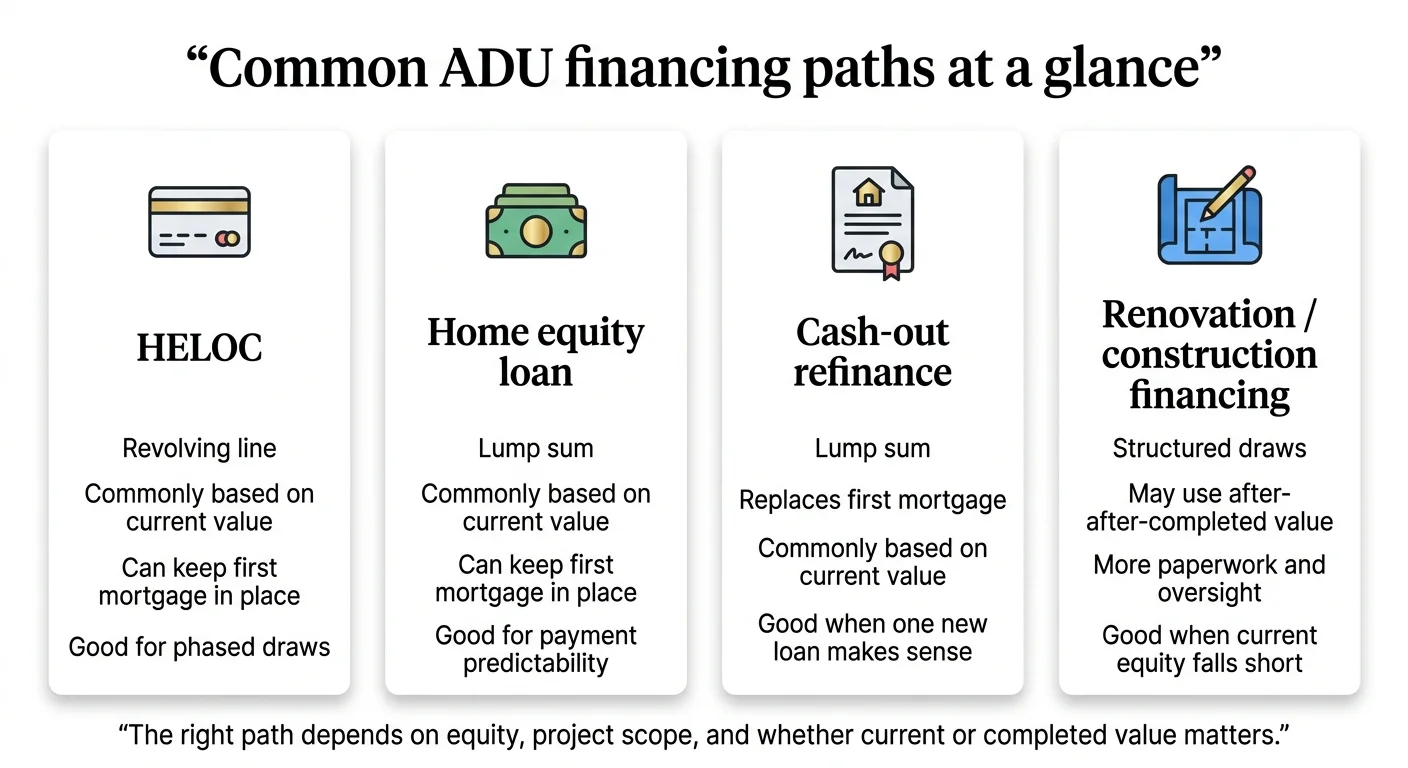

HELOC vs. Home Equity Loan vs. Cash-Out Refinance vs. Construction Loan: Which Fits Best?

| HELOC | Home equity loan | Cash-out refinance | Renovation / construction loan | |

|---|---|---|---|---|

| Appraises based on | Current home value | Current home value | Current home value | After-completed value |

| Keeps your first mortgage? | Yes | Yes | No — replaces it | Depends on product |

| How funds arrive | Flexible draws as needed | Lump sum upfront | Lump sum upfront | Staged draws with lender oversight |

| Rate structure | Typically variable | Typically fixed | Typically fixed | Varies by product |

| Initial payment | Often interest-only during draw (varies) | Principal + interest from day one | Principal + interest from day one | Often interest-only during construction |

| Best for | Homeowners with strong current equity who want flexibility | Homeowners with strong equity who want payment certainty | Homeowners with high equity and a mortgage rate they don’t mind replacing | Homeowners with limited current equity who need completed-value underwriting |

| Biggest downside | Variable rate; payment increase at repayment | Less flexible; pay interest on full amount from day one | Lose your current mortgage rate | More paperwork; longer timeline; lender controls draw schedule |

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. This comparison is sorted by loan structure — not by compensation. Full affiliate disclosure →

Compare Lenders

Know your path — now find the lender who fits it

Compare current options from lenders who specialize in ADU construction financing, sorted by loan type.

The Dwelling Index is reader-supported. When you use our links to apply for financing or request pricing, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation. Full disclosure →

What If You Don’t Have Enough Equity for a HELOC?

A large number of homeowners searching “HELOC for ADU” are going to discover that a standard HELOC doesn’t get them far enough. If that’s you, the project isn’t dead. The financing path just looks different.

Future-Value Financing in Plain English

Standard HELOC says:

“Here’s what your home is worth today. You can borrow against that.”

Renovation loan says:

“Here’s what your home will be worth once the ADU is complete. You can borrow against that.”

Fannie Mae HomeStyle Renovation

Fannie Mae explicitly allows its lending products to be used for adding an ADU. The HomeStyle Renovation loan uses the home’s projected as-completed appraised value for underwriting, which can dramatically expand borrowing capacity compared to a current-value HELOC.

How the math changes: If your home is worth $400,000 today but the appraiser estimates it’ll be worth $540,000 with a completed ADU, HomeStyle can underwrite to that higher figure — potentially opening up over $130,000 more in borrowing power versus a standard HELOC.

(Source: Fannie Mae Single Family — Accessory Dwelling Units page; Fannie Mae HomeStyle Renovation Fact Sheet. Verified March 2026.)

Freddie Mac CHOICERenovation

Freddie Mac’s CHOICERenovation program specifically includes both converting existing structures (garages, outbuildings) into ADUs and adding new ADUs as eligible projects. Like HomeStyle, it underwrites based on the completed value.

(Source: Freddie Mac CHOICERenovation program guidelines. Verified March 2026.)

FHA 203(k)

FHA has clarified that ADUs are eligible for the Standard 203(k) rehabilitation loan program. Updated FHA policies also allow projected ADU rental income to be considered in certain qualifying scenarios for FHA-insured mortgages — a meaningful change for homeowners whose income alone might not meet DTI requirements. One important caveat: FHA does not allow ADU rental income to be used as qualifying income for cash-out refinances.

The Standard 203(k) requires a minimum of $5,000 in repairs/improvements and is designed for major renovation projects. FHA insurance means more flexible credit requirements than conventional products.

(Source: HUD Mortgagee Letter 2023-17 on ADU eligibility and rental income. Verified March 2026.)

The Hybrid: Cash + Smaller HELOC

If the gap between your HELOC capacity and the ADU cost is moderate — say $30,000–$60,000 — you may not need a full renovation loan. Paying a portion in cash and taking a smaller HELOC can close the gap while keeping your first mortgage intact and minimizing borrowing costs.

“Not enough equity” doesn’t mean “can’t build an ADU.” It means the right product is waiting — you just need to match the financing to your situation.

Can Rental Income from the ADU Help You Qualify?

This is one of the most common questions we hear, and the answer is more nuanced than most guides let on.

For a Standard HELOC: Don’t Count on It

When you apply for a standard HELOC to fund an ADU that doesn’t exist yet, most products underwrite based on your current income and current home value. Projected rental income from a not-yet-built ADU generally won’t help you qualify. However, some ADU-specific products (like Patelco’s California ADU HELOC) may consider projected income under their specific guidelines — so it’s worth asking.

For a Post-Construction Refinance: Potentially Yes

Once the ADU is built and occupied, rental income may help you qualify for a refinance. Fannie Mae’s current published guidelines allow ADU rental income to be used in certain purchase or limited cash-out refinance scenarios on a one-unit principal residence with one ADU — subject to a qualifying-income cap of 30% and specific documentation requirements.

For FHA-Insured Products: Recent Policy Changes

FHA’s updated policies allow projected ADU rental income in qualifying scenarios for FHA-insured mortgages — but this does not apply to cash-out refinances. This is relevant for homeowners exploring the 203(k) path.

| Scenario | Can rental income help you qualify? |

|---|---|

| Applying for a standard HELOC before the ADU exists | Generally no (some ADU-specific products may differ) |

| Applying for a construction/renovation loan | Depends on the product and lender |

| Refinancing after the ADU is built and rented | Potentially yes, under Fannie Mae guidelines with documentation and a 30% income cap |

| FHA-insured mortgage with an ADU | Potentially yes, except for cash-out refinances |

Sources: Fannie Mae Selling Guide, Section B3-3.8-01 (Rental Income); HUD Mortgagee Letter 2023-17. Verified March 2026.

The bottom line: don’t build your qualification plan around rental income that doesn’t exist yet — but absolutely build your exit strategy around it.

Is HELOC Interest Tax-Deductible for ADU Construction?

HELOC interest may be deductible if the borrowed funds are used to buy, build, or substantially improve the home securing the loan — and you itemize deductions. Building an ADU on your property generally qualifies as a substantial improvement under IRS rules.

The funds must go toward qualifying home improvement.

Interest on HELOC funds used for personal expenses, debt consolidation, or anything unrelated to improving the securing property is not deductible.

There’s a combined debt limit.

Under the Tax Cuts and Jobs Act (now made permanent), you can deduct interest on up to $750,000 of total home-acquisition debt (including your first mortgage and the HELOC) for married filing jointly, or $375,000 for married filing separately. Your existing mortgage balance counts toward this cap.

You must itemize deductions.

If you take the standard deduction, HELOC interest deductibility doesn’t help you. Your total itemized deductions must exceed the standard deduction thresholds for itemizing to make sense.

Documentation is essential.

Keep all contractor invoices, permit receipts, material receipts, and bank statements showing HELOC draws went directly to ADU construction. Don’t mix qualifying and non-qualifying expenses in the same HELOC.

(Source: IRS Publication 936 (Home Mortgage Interest Deduction). Verified March 2026.)

This section is educational, not tax advice. Tax situations vary by individual circumstances. Consult a qualified tax professional for guidance specific to your situation.

Will the ADU Appraise Well Enough to Refinance Later?

If your plan involves taking a HELOC now and refinancing into a fixed-rate loan after the ADU is complete, appraisal is a key variable.

How Appraisers Are Supposed to Treat an ADU

Fannie Mae’s Selling Guide (Section B4-1.3-05) instructs appraisers to identify the ADU, describe it in the property analysis, analyze its effect on value and marketability, and adjust for it in the sales comparison approach. The ADU should be treated as a value-adding feature — not ignored or dismissed.

Why Comps Still Matter

The challenge is practical: in many markets, there aren’t enough recent sales of comparable properties with ADUs. When comps are thin, appraisers often default to conservative valuations. This is improving as ADU construction accelerates — more ADU sales means better comp data — but it remains a factor in markets where ADUs are still relatively new.

Three Exit Strategies After the ADU Is Complete

Keep the HELOC and repay.

When the draw period ends, you shift to principal + interest payments and pay it down over the remaining term. Simple, predictable, but monthly payments increase.

Refinance into a fixed-rate loan.

Consolidate the HELOC and your first mortgage into a single fixed-rate loan. This eliminates variable-rate risk and simplifies your payment — but you need a solid appraisal and you’ll reset your mortgage terms.

Pay off with other liquidity.

If you’ve accumulated savings or other assets during the draw period, you can pay down or eliminate the HELOC without refinancing. Cleanest exit, but requires available capital.

Plan your exit strategy before you take the HELOC, not after construction is done.

What Should You Ask a Lender Before Using a HELOC for an ADU?

This checklist separates homeowners who make informed decisions from those who learn the hard way. Bring it to every lender conversation.

About structure and terms

- What is your maximum CLTV for a HELOC?

- How long is the draw period, and what happens when it ends?

- Is a fixed-rate option or fixed-rate conversion available?

- Is there a required minimum or initial draw at closing?

- Is there an early termination fee if I pay off or refinance early?

About underwriting

- Do you underwrite based on current value or after-completed value?

- What type of appraisal is required — drive-by or full interior?

- Can the credit line be frozen or reduced after approval?

About ADU-specific considerations

- Do you have experience with HELOC-funded ADU projects?

- Are there restrictions on how funds can be used (construction only, or any use)?

- Does the property need to be owner-occupied?

- What documentation will you need — contractor bids, permits, construction plans?

If a lender can’t clearly answer questions 6 and 9, they probably don’t have meaningful ADU experience. Keep looking.

How to Use a HELOC for an ADU Without Getting Trapped

The order matters. Most guides tell you to “just get pre-approved.” That’s step 4, not step 1. Follow this sequence and you’ll avoid the most common — and most expensive — mistakes.

Step 1

Confirm Your ADU Is Legal and Get Realistic Cost Estimates

Before you borrow a dollar, verify that your property can legally support an ADU. Check zoning, setbacks, lot coverage requirements, height limits, and any owner-occupancy rules in your municipality. Simultaneously, get detailed estimates from at least two experienced ADU contractors. Not ballpark numbers — itemized bids with line items for design, permitting, site prep, foundation, framing, mechanical systems, finishes, and contingency.

Step 2

Estimate Your Tappable Equity — and Leave a Buffer

Use the formula: (home value × 80%) − mortgage balance = approximate max HELOC. Then subtract 15–20% as a contingency buffer. This is your realistic borrowing target. If the formula says you can access $240,000, your working budget should be $195,000–$205,000.

Step 3

Choose the Right Financing Path

Based on your equity math and the decision framework earlier in this guide, determine whether a standard HELOC, home equity loan, renovation loan, construction loan, or hybrid approach fits best. Don’t default to a HELOC just because it’s the most popular option.

Step 4

Get Pre-Approved and Compare Terms

Apply with 2–3 lenders. Compare CLTV limits, draw period length, repayment terms, fixed-rate options, closing costs, and any early termination fees. Critical: do not start construction until your financing is fully approved and closed.

Step 5

Match Draws to Your Contractor’s Payment Schedule

Once construction begins, draw HELOC funds as each phase requires payment — not before. This minimizes the time you’re paying interest on drawn funds. Keep a dedicated project account if possible for a clean paper trail.

Step 6

Protect Your Contingency Until the End

Resist the urge to draw your full contingency buffer early. Cost overruns tend to cluster in the later phases — finishes, inspections, utility hookups, and landscaping. Having available HELOC capacity during the final stretch can mean the difference between finishing on budget and scrambling for emergency funds.

Step 7

Plan Your Exit Before Construction Ends

Decide now — not after the ADU is done — how you’ll handle the HELOC when the draw period ends. If refinancing is the plan, start talking to lenders 3–6 months before the ADU is complete. You’ll need a strong appraisal, and as we covered earlier, appraisal outcomes for ADU properties aren’t always predictable.

Free ADU Report

Every step you take now makes the decision clearer. See what’s possible at your address.

See what you can build at your address — zoning, feasibility, and the financing paths that match your lot.

Edge Cases: What Changes Whether a HELOC Works for Your ADU

Is a HELOC a good idea for a garage conversion?

Often yes — and it may be the single best HELOC-ADU match. Garage conversions typically sit in a cost range that falls within standard HELOC borrowing power for most homeowners with moderate equity. The existing structure reduces costs and timelines compared to a ground-up build.

What if my home is paid off?

You’re in a strong position. With no existing mortgage, your entire home value is available equity. A HELOC gives you maximum borrowing power with minimal complexity. You also have more options — a cash-out refinance at a fixed rate gives predictable payments with no variable-rate exposure.

What if I’m planning to sell soon?

Proceed with caution. The ADU may not appraise at construction cost, especially in markets with limited ADU comp data. Run the numbers conservatively: will the expected increase in sale price — net of all costs — actually leave you ahead?

What if the property is a second home or rental?

Occupancy rules vary sharply by lender and product. Some HELOCs are primary-residence-only. Others may allow second homes or investment properties with separate eligibility requirements — typically higher equity thresholds and stricter qualification standards. Always confirm occupancy and property-type eligibility with each lender before applying.

What if the ADU is for aging parents instead of rent?

The financing mechanics are the same, but the financial picture is different. You won’t have rental income to offset HELOC payments, so your ability to service the debt must come entirely from other income. Many homeowners in this situation opt for a smaller, simpler ADU (a JADU or garage conversion) to keep costs manageable.

What about HOA rules and local restrictions?

If your property is in an HOA, check the CC&Rs before planning anything. Some HOAs restrict ADU construction regardless of what state or municipal law allows. In some states, recent legislation limits HOA authority to block ADUs — but enforcement varies.

Will building an ADU raise my property taxes?

Yes, in most jurisdictions. The ADU’s value will typically be added to your property’s tax assessment, increasing your annual tax bill. In California, new construction (including an ADU) is assessable at current fair market value upon completion, while the existing home retains its Prop 13 base. Other states handle reassessment differently. Check with your county assessor’s office for specifics.

FAQ: HELOC for ADU

Can you use a HELOC to build an ADU?

Yes. Home-equity-based financing (HELOCs and home equity loans) is the most popular way homeowners fund ADU construction, used in 56% of mortgage-based ADU financing cases according to the Urban Institute.

How much equity do I need for an ADU HELOC?

CLTV caps vary by lender, but many standard HELOCs require that your combined mortgage and HELOC balances stay within 80–85% of your home’s current value. Use the formula: (home value × 80%) − mortgage balance = approximate max HELOC.

Can I get a HELOC if I still have a mortgage?

Absolutely. A HELOC is a second lien that sits alongside your existing first mortgage. Your original loan terms stay untouched.

Is a HELOC better than a home equity loan for an ADU?

It depends on your priorities. A HELOC offers flexible draws and potentially lower initial payments during construction — ideal for phased costs. A home equity loan offers a fixed rate and predictable payments — ideal if you want payment certainty. Both require strong current equity.

What happens when the HELOC draw period ends?

You typically shift from lower or interest-only payments to full principal + interest payments over the remaining loan term. The CFPB warns that this transition can mean a significant payment increase. Plan for it before you borrow.

Can the lender freeze my HELOC?

Yes. The CFPB notes that lenders can freeze or reduce a HELOC if your home value drops, your financial situation changes, or you fail to meet loan terms. This can happen mid-construction.

Is HELOC interest tax-deductible for ADU construction?

HELOC interest may be deductible if the funds are used to buy, build, or substantially improve the home securing the loan, and you itemize deductions. A combined debt limit of $750,000 applies for married filing jointly. Keep documentation of all ADU-related expenses. Consult a tax professional for your specific situation. (Source: IRS Publication 936.)

Can rental income from the ADU help me qualify for the HELOC?

For most standard HELOCs, no — projected rental income from a not-yet-built ADU typically isn’t counted. Some ADU-specific products and government-backed programs have narrower rules that may allow it. Documented rental income may help you qualify for a post-construction refinance under Fannie Mae or FHA guidelines.

Will a HELOC cover a detached ADU?

Only if your equity is deep enough. Detached ADUs are typically the most expensive ADU type, and often exceed standard HELOC capacity for mid-equity homeowners. If there’s a gap, a renovation or construction loan may be the better starting point.

What if I don’t have enough equity for a HELOC?

Explore renovation loans (Fannie Mae HomeStyle, Freddie Mac CHOICERenovation) or FHA 203(k). These products underwrite based on your home’s projected after-completed value, which often unlocks enough borrowing power even with limited current equity.

Will an ADU appraise high enough to refinance later?

It depends on your local market. In areas with strong ADU comp data, appraisals tend to reflect the value added. In markets where ADUs are still new, appraisals can be conservative. Working with ADU-experienced lenders and proactively providing comp data helps.

Should I use a HELOC if I plan to sell soon?

Proceed with caution. The ADU may not appraise at construction cost in a sale scenario, and you’ll carry the HELOC debt until closing. Run conservative numbers before committing.

Can I use a HELOC for a prefab ADU?

Potentially — but ask whether the unit will be permanently affixed, titled as real property, and considered acceptable collateral under that specific lender’s guidelines. Treatment varies by lender and property type, so confirm before assuming.

Not Sure Where to Start?

You’ve read through the decision framework, the equity math, the comparison, and the risks. You know more about HELOC-funded ADU construction than the vast majority of homeowners.

The next step is property-specific. What you can actually build — the ADU type, the size, the placement, and the realistic budget — depends on your lot, your local regulations, and your equity position.

Free ADU Report

See what’s possible at your address — get your free ADU report in 60 seconds.

See what you can build at your address — zoning, feasibility, and the financing paths that match your lot.

Free Download

2026 ADU Starter Kit

Includes a borrowing-gap worksheet, lender question checklist, ADU cost estimator, and a one-page “HELOC vs. Other Paths” decision summary. No commitment, no spam.

Download the Free 2026 ADU Starter KitFind Your State ADU Financing Rules

Keep Reading

Last updated: March 31, 2026 · Sources verified against official Fannie Mae, Freddie Mac, HUD, CFPB, and IRS documentation

Sources cited: Urban Institute (“To Increase the Housing Supply, Focus on ADU Financing,” April 2024); Consumer Financial Protection Bureau (HELOC guide); IRS Publication 936; Fannie Mae Selling Guide (Sections B3-3.8-01 and B4-1.3-05); Fannie Mae Single Family ADU page; Freddie Mac CHOICERenovation guidelines; HUD Mortgagee Letter 2023-17; Alliant Credit Union HELOC guidelines; Patelco ADU HELOC program documentation; California State Board of Equalization (New Construction guidelines). All sources verified as of March 2026.

The Dwelling Index is an independent national ADU resource. We do not originate loans, act as a broker, or rank financing options by compensation. Editorial methodology → · Affiliate disclosure →