RenoFi Review 2026: Is It Worth Using for ADU Financing?

The Bottom Line

RenoFi is a legitimate renovation financing platform (NMLS #1802847) that lets you borrow against your home’s after-renovation value — not just what it’s worth today. For homeowners building an ADU with limited equity, this can be the difference between a $0 borrowing ceiling and six figures in available funds. But RenoFi is not a lender — it’s a broker that connects you with credit union lending partners. The process is slower and more document-heavy than a traditional HELOC. And you pay for a non-refundable appraisal before you know if you’re approved. Go in prepared.

Sources: RenoFi official FAQ & disclosures, Bankrate, Trustpilot, BBB, Reddit, BiggerPockets, Glassdoor. The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full disclosure

| Question | Short Answer |

|---|---|

| Is RenoFi legit? | Yes. Licensed mortgage broker, NMLS #1802847, backed by First Round Capital and Canaan Partners. |

| Is it a lender? | No. RenoFi is a broker that matches you with credit union lending partners. |

| Good for low-equity homeowners? | Yes — this is precisely who it's built for. |

| Can I keep my current mortgage rate? | Yes. RenoFi loans sit in second position. Your first mortgage stays untouched. |

| Can I use my own contractor? | Yes, but your contractor must pass RenoFi's due diligence review. |

| How long does it take? | Typically 30–60 days once your documents are complete. Some borrowers report longer for complex projects. |

| Available in my state? | Availability varies. Texas is excluded for ARV products. Confirm directly with RenoFi before ordering an appraisal. |

| Biggest risk? | You pay for an appraisal upfront and it's non-refundable if you're not approved. |

| Better alternative if I have equity? | A standard HELOC or a home equity investment if you can't take on monthly payments. |

A detached backyard ADU — one of RenoFi’s strongest use cases for after-renovation-value financing.

RenoFi Review Verdict: Is RenoFi Legit for ADU Financing?

Yes — and this is the short version for everyone who just needs to know.

RenoFi (Renovation Finance LLC) is a real, licensed company. It’s registered with the Nationwide Multistate Licensing System as a mortgage broker (NMLS #1802847), headquartered in Berwyn, Pennsylvania, and backed by institutional investors including First Round Capital, Canaan Partners, and Comcast Ventures. It holds an A- rating from the Better Business Bureau and a 4.6-star TrustScore on Trustpilot across 124+ published reviews.

It is not a fly-by-night operation. It is also not a bank. RenoFi is the middleman between you and a credit union lending partner, and understanding that distinction is the key to understanding both its strengths and its friction points.

For ADU homeowners specifically, RenoFi solves a problem that most financing products can’t: it lets you borrow based on what your home will be worth after the ADU is built. If you bought recently and have thin equity, this can be transformative. If you already have plenty of equity, you don’t need it.

The rest of this page helps you figure out which camp you’re in.

What We’d Want to Know Before Applying (The Honest Downside)

We’re leading with the part most review sites bury at the bottom, because you deserve it upfront.

RenoFi’s process is slower and more document-heavy than a traditional HELOC.

That’s not a bug — it’s structural. Because RenoFi underwrites against what your home will be worth, the lender needs to verify your renovation plans, your contractor’s qualifications, and an “as-completed” appraisal. RenoFi’s official guidance says the process typically takes about 30–60 days once your documents are complete. But BBB complaints and Glassdoor employee reviews reference timelines stretching well beyond that for complex projects.

The documentation burden is real.

You'll need contractor estimates broken down by labor and materials, preliminary plans, a renovation contract with payment schedule, and standard financial documents. Several BBB reviewers specifically cite this as the sticking point — getting contractors to produce the level of detail RenoFi requires.

The appraisal is non-refundable.

You pay the appraiser directly before you know if you're approved. If the appraisal comes in low or you're denied, that money is gone.

Here’s the context that matters:

This friction exists because the product solves a problem nothing else does. If you bought your home recently and have minimal equity, a standard HELOC gives you near-zero borrowing power. RenoFi can unlock substantial funds by looking at what the ADU will add to your property value. For many ADU builders, the choice isn’t “RenoFi vs. something faster.” It’s “RenoFi vs. not building the ADU at all.”

The majority of published Trustpilot reviews report that the concierge-style guidance made the complexity manageable. When the project is straightforward and the assigned advisor is responsive, it works well. When the project is complex or communication drops, it gets frustrating fast.

How RenoFi Actually Works (Step by Step)

RenoFi confuses people because it doesn’t fit neatly into a category they already know. It’s not a bank. It’s not a traditional HELOC provider. It’s not a construction lender. Here’s what it actually is.

RenoFi is a broker with proprietary technology

RenoFi (Renovation Finance LLC) partners with credit unions nationwide. It uses its own “Renovation Underwriting” technology to evaluate your project and financial profile, then connects you with a lending partner that can fund the loan. Think of it as a concierge that prepares your application and finds you the right credit union — then the credit union makes the final credit decision and funds the loan.

Source: RenoFi disclosure page, NMLS #1802847

This means RenoFi controls the customer experience but not the lender’s timeline or approval criteria. That distinction matters when things go wrong — and it explains why some negative reviews describe feeling caught between two entities.

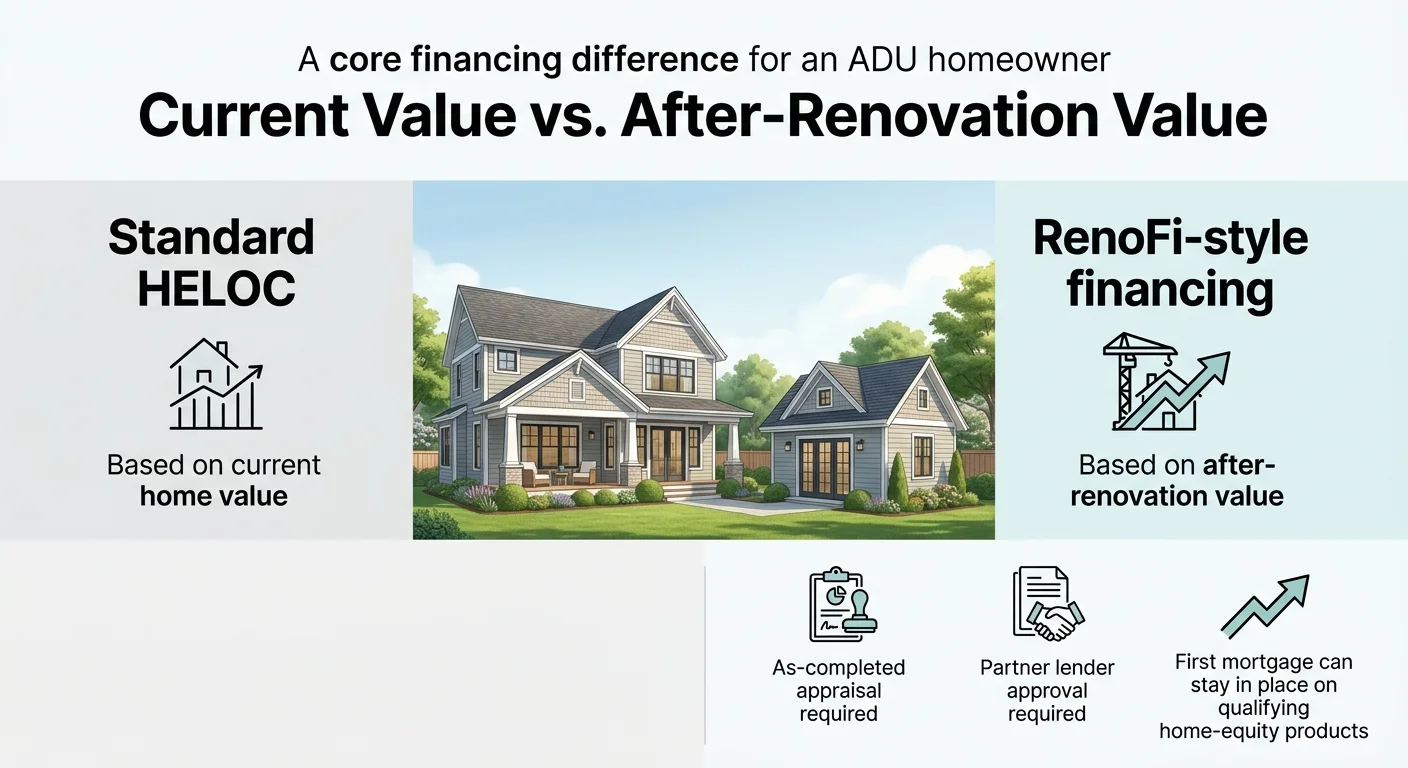

The after-renovation value concept — and why it changes the math for ADU builders

This is the core of what makes RenoFi different from every standard HELOC on the market.

Standard HELOC

Lends against your home’s current value. If your home is worth $500,000 and you owe $400,000, most lenders cap at 80% LTV — giving you functionally $0 in borrowing power. You can’t borrow a dime for that ADU.

RenoFi Renovation HELOC

Lends against what your home will be worth after the ADU is built. If the ADU pushes value to $650,000, RenoFi’s partners can go up to 90% of that after-renovation value — giving you up to $185,000from the same starting position.

The core financing difference: standard HELOC vs. RenoFi’s after-renovation-value model.

Here’s how that plays out across three common ADU scenarios:

| Your Situation | Home Value | Mortgage Balance | Standard HELOC (80% LTV) | RenoFi (90% of ARV) |

|---|---|---|---|---|

| Recent buyer, detached ADU | $500,000 | $400,000 | $0 — already at 80% LTV | Up to ~$185,000 (if ARV = $650K) |

| 5-year owner, garage conversion | $600,000 | $350,000 | Up to ~$130,000 | Up to ~$325,000 (if ARV = $750K) |

| Long-time owner, large ADU | $800,000 | $200,000 | Up to ~$440,000 | Up to ~$655,000 (if ARV = $950K) |

These are illustrative examples, not loan offers or guarantees. Actual borrowing power depends on lender criteria, credit profile, DTI ratio, appraisal results, and the specific RenoFi product. RenoFi’s own disclosure states: “There is no guarantee your home will increase in value and, in rare cases, you may owe more than your home is worth.”

Notice the pattern: RenoFi’s advantage is massive for the recent buyer with thin equity and shrinks as you accumulate more equity. If the standard HELOC already covers your ADU budget, the extra complexity of RenoFi isn’t worth it.

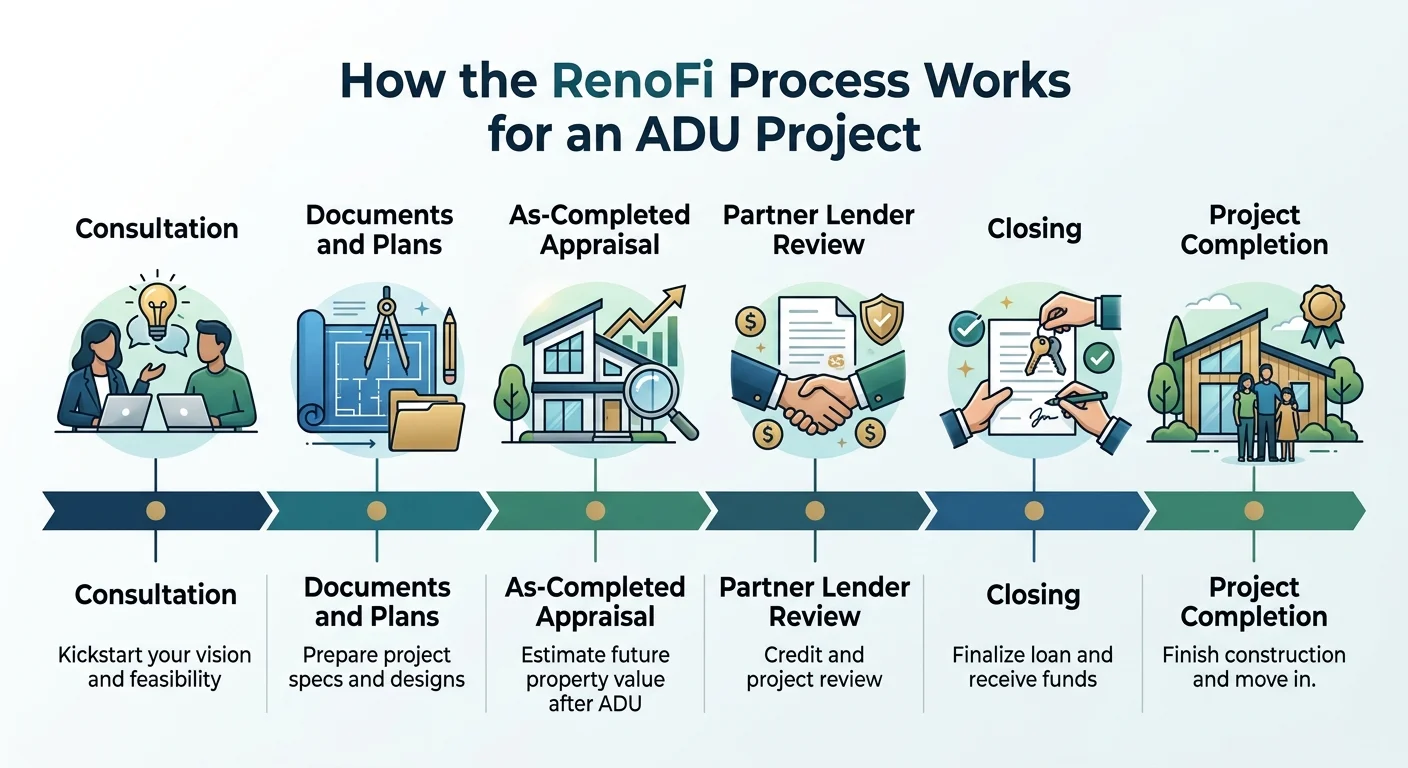

The six-step process

The RenoFi process for an ADU project — six steps from consultation to project completion.

Free consultation

You speak with a RenoFi Advisor about your project. No hard credit pull at this stage (RenoFi may do a soft pull during pre-qualification). No commitment. They'll tell you quickly whether you're a fit.

Document gathering

This is where the work begins. Upload financial documents (bank statements, pay stubs, tax returns) plus renovation documents (contractor estimates with labor/material breakdowns, preliminary plans, renovation contract with payment schedule). RenoFi's portal handles the uploads.

Source: RenoFi application checklist

RenoFi underwriting review

RenoFi's team evaluates your project feasibility, contractor qualifications, and financial profile before involving a lender. This is the extra step that doesn't exist with a standard HELOC — and it's the main reason the timeline is longer.

As-completed appraisal

An appraiser evaluates both your home's current value AND its projected post-ADU value. You pay the appraiser directly. This cost is non-refundable even if you're ultimately not approved — so make sure your documentation is solid before reaching this step.

Source: RenoFi FAQ

Lender application and approval

RenoFi connects you with a credit union partner. The lender runs their own underwriting and makes the final credit decision.

Closing and funding

For HELOCs, you get access to a revolving credit line during a 10-year draw period. For fixed-rate home equity loans, you receive a lump sum. Unlike typical construction loans, RenoFi loans don't require draw schedules or inspections during construction — funds are available upfront.

Source: RenoFi FAQ

After the project

Once your ADU is complete, a final inspection verifies the work matches the approved plans. RenoFi issues a certificate of completion and any temporary renovation fees from the lender are removed.

Realistic timeline: Typically about 30–60 days from document submission to closing for a straightforward ADU project with complete documentation. If you’re self-employed, have an unusual property, or your contractor needs time to produce detailed estimates, add weeks.

Source: RenoFi FAQ — verified April 4, 2026

What RenoFi Actually Costs — and Why the “Free Service” Claim Confuses People

RenoFi says working with them is free. Multiple borrowers describe the process as expensive. Both are technically true, and the confusion is worth resolving.

How RenoFi gets paid

RenoFi is generally compensated by its lending partners. However, RenoFi’s account terms disclose that on select mortgage loan products, RenoFi may receive borrower-paid broker compensation at closing. This is an important distinction — the blanket “no fees” messaging doesn’t tell the full story.

Sources: RenoFi FAQ, RenoFi Account Terms of Use — verified April 4, 2026

What you should expect to pay

| Cost Category | Who Charges It | When You Pay | What to Verify |

|---|---|---|---|

| Lender origination/closing costs | Credit union lender | At closing | Ask for the full closing cost estimate in writing before ordering the appraisal |

| As-completed appraisal | Appraiser (you pay directly) | Before approval — non-refundable | Get the exact cost from your RenoFi Advisor before authorizing |

| Temporary renovation-period charge | Credit union lender | Monthly during construction only | Confirm whether your lender charges this and at what amount |

| Possible broker compensation | RenoFi (on select mortgage products) | At closing | Ask directly whether your specific product includes borrower-paid RenoFi compensation |

| Credit union membership | Credit union | Before closing | Usually nominal — ask about requirements |

The bottom line on fees

Before you order the appraisal (the first non-refundable cost), get every charge confirmed in writing from both your RenoFi Advisor and the lending partner. The borrowers who report surprise costs in reviews are almost always the ones who didn’t ask these questions upfront.

Why some reviews describe it as expensive

When you add lender fees, appraisal costs, closing costs, and months of renovation-period charges, the total out-of-pocket can add up. That’s not unusual for a secured home equity product of this size — but it’s a long way from “free.” The lesson: RenoFi’s advisory service may be free. The loan is not. Understand total cost before signing.

How Hard Is RenoFi to Qualify For?

RenoFi is not easy-mode financing. The after-renovation-value model creates additional qualification layers beyond what a standard HELOC requires.

The basics

Most RenoFi lending partners look for:

Sources: RenoFi FAQ; Bankrate — verified April 4, 2026

What can disqualify you

Beyond the basics, these situations can block or complicate a RenoFi application:

Can You Use Your Own Contractor? (And Can You Owner-Build?)

This question comes up constantly on Reddit and BiggerPockets, and most review sites barely touch it.

You can use your own contractor — with a catch

RenoFi does not require you to use a contractor from their network. You’re free to choose your own. But your contractor must pass RenoFi’s due diligence review for the lender’s benefit. That means your contractor needs to provide:

- Detailed cost estimates broken down by labor and materials

- A preliminary renovation contract with payment schedule and change order procedures

- Proof of insurance and any state-required licensing

- A project timeline

Important: contractor licensing requirements vary by state.

RenoFi evaluates your contractor to protect the lender, but does not endorse or guarantee any contractor’s work. You should do your own due diligence independently.

If your contractor can’t or won’t produce this documentation, your application stalls. This is the #1 process friction cited in BBB complaints — not RenoFi itself, but getting contractors to deliver the paperwork at the level of detail the underwriting requires.

Pro tip from review patterns

Get your contractor to produce a line-item estimate before you start the RenoFi process. If they resist breaking costs into labor and materials, that’s a signal — either they’re not organized enough for this process, or they’re hiding margins.

Sources: RenoFi FAQ, RenoFi Terms of Use — verified April 4, 2026

Owner-building has limits

If you plan to self-manage the project as your own general contractor (and you’re not a GC by trade), RenoFi’s lending partners may cap you at three subcontractors. Owner-builders also face additional scrutiny on project feasibility. This isn’t a dealbreaker, but it adds friction.

If you’re planning a full owner-build with minimal subcontractor involvement, a standard HELOC or personal loan — where no one reviews your construction plans — may be a better fit. You’ll sacrifice RenoFi’s borrowing power but gain total flexibility.

Source: RenoFi FAQ

Free ADU Feasibility Report

Before you apply for financing, find out what you can build.

Zoning, setbacks, and size limits vary wildly — and there’s no point applying for financing on a project your municipality won’t permit.

See What You Can Build at Your AddressWhat Real Customers Say: Aggregated Review Analysis

We pulled review data from every major platform so you don’t have to cross-reference five sites yourself.

Review scores across platforms

| Platform | Rating | Volume | Key pattern |

|---|---|---|---|

| Trustpilot | 4.6 / 5 | 124+ published reviews | Advisors praised by name, process works but takes longer than expected |

| BBB | A- (not accredited) | 6 complaints filed | Documentation friction, communication gaps on complex cases |

| Bankrate | 3.8 / 5 | Limited sample | Good service, limited negotiation room on terms |

| BiggerPockets | Mixed (forum) | Several threads | Useful for ADU financing, broker model is unusual, worth investigating |

| Glassdoor (employees) | 3.6 / 5 | ~24 reviews | Internal: long sales cycles, lean operations |

Data aggregated April 4, 2026. Check each platform for the most current reviews.

The positive pattern

- Individual advisors praised by name — the quality of your assigned advisor appears to be the single biggest predictor of experience

- 'Seamless' and 'easy' are common descriptors in positive reviews once documentation is in order

- The concierge model genuinely helps first-timers navigating renovation financing

- The online document portal works well — even reviewers who found the process long generally praised its usability

The negative pattern

- Timeline reality vs. expectation — the most common complaint across BBB and Trustpilot

- Communication drops — advisors becoming unresponsive during complex underwriting phases

- Unexpected costs — charges or fee structures not fully understood until closing

- Documentation requests that feel endless — 'they kept asking for more documents' appears across platforms

- The appraisal is a gamble — you pay before approval and it's non-refundable

The insider perspective most reviews miss

We also reviewed RenoFi’s Glassdoor employee reviews — not because employee satisfaction directly affects your loan, but because operational realities trickle down to customer experience. Multiple employees mention lean operations and internal challenges with lender partner communication, which aligns with the communication gaps some borrowers report. This isn’t a reason to avoid RenoFi. It is a reason to go in with realistic expectations.

How to protect yourself if you apply

Based on the full pattern analysis across platforms, here are the highest-leverage things you can do:

Ask for your advisor's direct contact (cell number, not just a general support line) at the first meeting.

Set timeline expectations in writing. Get a realistic timeline specific to your project type and state in email — not just a verbal estimate.

Have your contractor documentation complete before you start. This is the single biggest variable in how fast your application moves.

Get every fee confirmed in writing before ordering the appraisal. This is your last off-ramp before committing non-refundable money.

Get a second financing option pre-approved as backup. If RenoFi stalls, you don't want to be months in with no alternative.

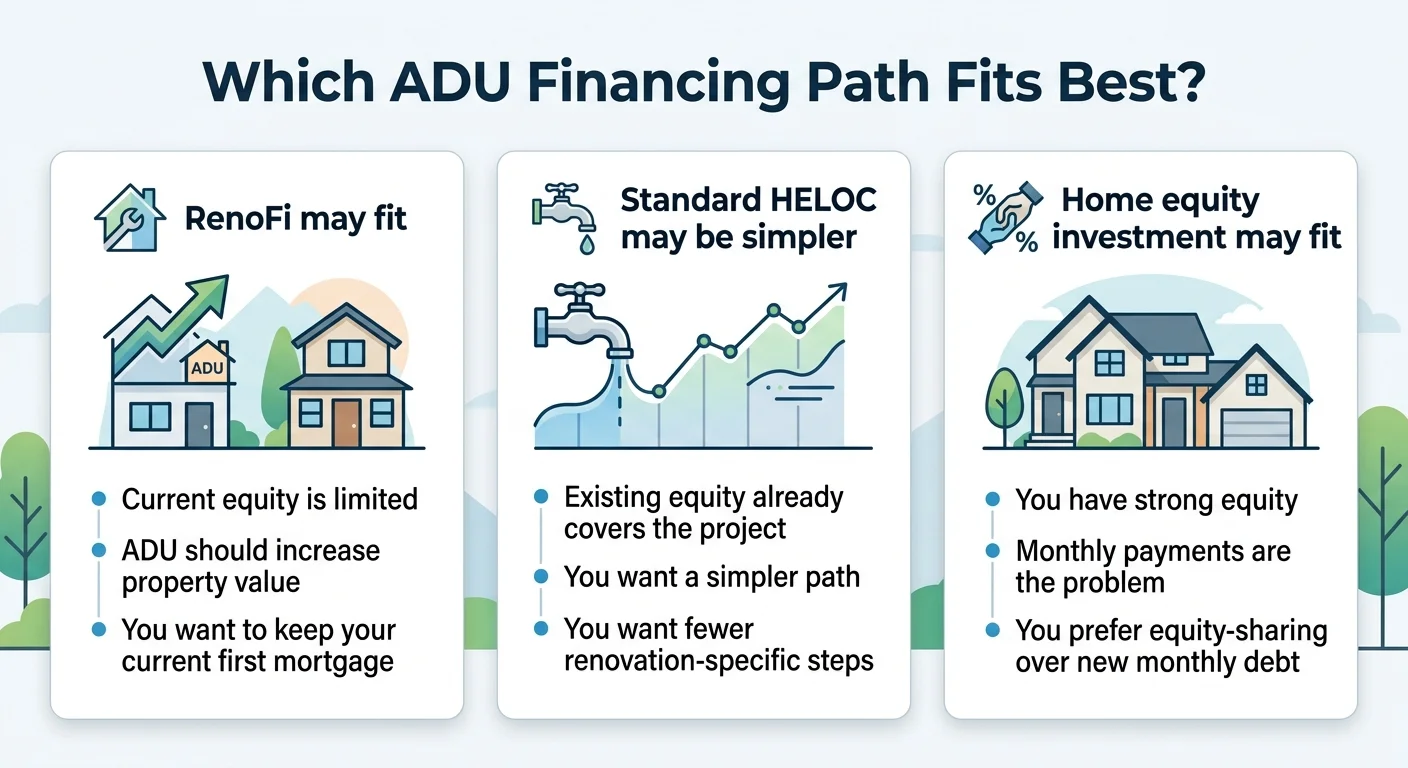

Is RenoFi Right for You? The ADU Decision Framework

Not every ADU homeowner should use RenoFi. Not every one should skip it. Here’s how to know.

Which ADU financing path fits best. Source: The Dwelling Index analysis, April 2026.

Use RenoFi if all of these are true:

- You have limited equity in your home and a standard HELOC doesn't cover your ADU budget

- You want to keep your current first mortgage (especially if you locked in a favorable rate)

- Your ADU project will meaningfully increase your property value — and comparable homes with ADUs in your area have sold at a premium

- You have a contractor who can produce detailed cost breakdowns, plans, and a preliminary contract

- You can tolerate a 30–60+ day process and don't need funds within the next two weeks

- RenoFi products are available in your state for your property type — confirm directly before starting

Skip RenoFi if any of these are true:

- You already have enough equity for a standard HELOC — if a regular HELOC covers your ADU budget, take the simpler, faster path

- You need money fast — if your contractor is ready to break ground within two weeks, RenoFi's timeline won't work

- You're in Texas — RenoFi's ARV products are not available in Texas

- You're equity-rich but cash-flow-poor — if you can't add a monthly payment, a home equity investment is a better structure

- Your project is under $50K — the documentation overhead isn't worth it for smaller projects

- You plan to owner-build without licensed subcontractors — RenoFi's contractor due diligence will create friction

RenoFi vs. Every Other ADU Financing Path: Full Comparison

This is the section most review sites skip or do poorly. They review RenoFi in isolation. You need to see it next to every realistic alternative so you can choose the right financing lane for your equity position, timeline, and ADU project.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation. Full disclosure

| RenoFi Renovation HELOC | Standard HELOC | Home Equity Investment | FHA 203(k) | Construction Loan | |

|---|---|---|---|---|---|

| Best for | Low equity + planned ADU | Strong equity + speed | Equity-rich, no monthly payments | Low equity + okay with refi | Large projects, experienced borrowers |

| Lending basis | After-renovation value | Current value | Current value | After-renovation value | After-renovation value |

| Keeps first mortgage? | Yes | Yes | Yes | No — requires refi | Usually requires refi |

| Monthly payments | Yes | Yes | None | Yes | Interest-only during build |

| Typical timeline | 30–60 days | As fast as 5 days | 2–4 weeks | 45–60+ days | 30–90 days |

| Documentation | Heavy | Light | Moderate | Very heavy | Very heavy |

| Available in TX? | No (ARV products) | Yes | Check availability | Yes | Yes |

| Main watchout | Longer process, appraisal risk | Low borrowing power if thin equity | You share future appreciation | Kills your low first mortgage rate | Draw schedules, inspections |

Comparison reflects general product structures as of April 2026. Terms and availability change — verify directly with each provider.

RenoFi vs. Standard HELOC: Speed vs. borrowing power

If you have strong existing equity — say your home is worth $600K with a $300K mortgage — a standard HELOC can close in days, requires minimal paperwork, and gives you substantial borrowing power. No renovation plans needed, no as-completed appraisal, no contractor due diligence.

But if you bought recently and owe close to what your home is currently worth, a standard HELOC gives you next to nothing. RenoFi is built specifically for this gap.

The rule is simple: if a standard HELOC already covers your ADU budget, use it. If it doesn’t, RenoFi is likely your best path.

RenoFi vs. Home Equity Investment: Monthly payments vs. equity share

Home equity investments (HEIs) from companies like Hometap give you a lump sum of cash with no monthly payments. Instead, you give the investor a share of your home’s future appreciation, settled when you sell (or at the end of a 10–30 year term).

This structure is purpose-built for equity-rich homeowners who can’t take on more monthly debt — retirees building an ADU for aging-in-place, fixed-income homeowners who want rental income from an ADU but can’t float another loan payment. The tradeoff: if your ADU significantly increases your property value, the HEI company’s share of that appreciation could cost more over time than a HELOC’s interest would have.

RenoFi vs. FHA 203(k): Two ARV-based options, very different structures

Both RenoFi and FHA 203(k) lend against after-renovation value. The critical difference: FHA 203(k) requires you to refinance your first mortgage. If you locked in a favorable rate during 2019–2022, an FHA 203(k) forces you to give that up for today’s rates. For many homeowners sitting on pandemic-era mortgage rates, that’s a dealbreaker. RenoFi sits in second position — your first mortgage stays untouched.

FHA 203(k) also adds inspection and draw-schedule requirements during construction that RenoFi doesn’t impose. However, FHA’s lower credit score threshold may make it the better option for borrowers who don’t meet RenoFi’s lending partners’ minimums.

RenoFi vs. Construction Loan: Complexity vs. access

Construction loans are purpose-built for building projects but come with significant overhead: draw schedules (the lender releases funds in stages as work progresses), periodic inspections, and typically require refinancing your first mortgage. For a standard ADU project, RenoFi is simpler — no draw schedules, no inspections during construction, and your first mortgage stays in place.

The Dwelling Index is reader-supported. When you use our links, we may earn a commission at no extra cost to you. Full disclosure

Know your lane? Go directly to the right path.

Using RenoFi Specifically for an ADU: What’s Different

RenoFi finances all kinds of renovations, but ADU projects create a uniquely strong case for their model. Here’s why — and what to watch for.

Why ADUs are RenoFi’s sweet spot

ADUs produce some of the largest after-renovation value increases of any home improvement project. The delta between current value and after-renovation value is exactly where RenoFi’s lending model creates the most borrowing power. The actual value an ADU adds depends on local comparable sales, the ADU’s legality and permitting, its size and quality, and buyer demand in your market. RenoFi has a dedicated ADU landing page, ADU-specific loan advisors, and published case studies for ADU projects.

ADU types RenoFi can finance

Ground-up new construction on a vacant lot — RenoFi does not finance this. The ADU must be on the same lot as your existing primary or second home.

The appraisal question every ADU builder should understand

The as-completed appraisal is the hinge point of every RenoFi loan. An appraiser evaluates what your property will be worth after the ADU is finished. If that number comes in lower than you expected, your borrowing power drops.

Comparable sales matter enormously.

If homes with ADUs in your neighborhood have sold recently at a premium, your appraiser has data to support a higher after-renovation value. If no one nearby has an ADU, the appraiser is working with less, and they tend to be conservative.

How to reduce appraisal risk

Before paying for the as-completed appraisal, do your own comparable property research. Look at recent sales of homes with ADUs in your area. If comps support a strong value increase, you’re in good shape. If you can’t find any ADU comp sales nearby, proceed with caution.

What happens if the appraisal comes in low

Your maximum loan amount decreases. In the worst case, the gap between your project cost and available borrowing power becomes too large, and the loan doesn’t work. The appraisal fee is non-refundable. This is a real financial risk you should factor in before starting.

Real-world ADU scenario walkthroughs

A modern ADU used as a home office — the type of project where RenoFi’s after-renovation-value model can unlock substantial borrowing power.

Scenario 1: The recent buyer building a detached ADU

Sarah bought her home in 2023 for $480,000 in a Portland suburb. She owes $440,000. She wants to build a 600 SF detached backyard ADU for $185,000, which she expects will push property value to $650,000+ based on comparable sales in her neighborhood.

Scenario 2: The long-time owner considering a garage conversion

Mike has owned his home in suburban Denver for 12 years. Home value: $650,000. Mortgage: $280,000. He wants to convert his detached garage into a 1-bed ADU for $95,000.

Scenario 3: The retiree who can't add a monthly payment

Joan owns her home outright in Raleigh — worth $420,000, no mortgage. She wants to build a small ADU ($120,000) for her aging mother. But she's on a fixed retirement income and cannot take on a monthly HELOC payment.

Does one of those scenarios sound like your situation?

If you’re not sure, start by finding out what you can build — everything else follows from there.

See What You Can Build — Free ADU Report in 60 SecondsWhat to Have Ready Before You Apply

A well-prepared application is the single biggest factor separating smooth RenoFi experiences from frustrating ones. Based on RenoFi’s published checklist and patterns from review analysis, here’s what to gather before your first conversation.

Financial documents

- Two most recent months of bank statements (all personal accounts)

- Two most recent months of investment and retirement account statements

- Recent pay stubs (or two years of tax returns if self-employed)

- Current mortgage statement

- Proof of homeowner's insurance

Renovation/ADU documents(the hard part)

- Contractor estimate with labor and material breakdowns — this is the document most applicants struggle to produce. Get it before you start.

- Preliminary renovation contract with estimated timeline, payment schedule, and change order procedures

- ADU plans or design drawings (preliminary is fine)

- Contractor insurance documentation and any state-required licensing

Questions to ask your RenoFi Advisor in the first call

What are all the fees I should expect — from RenoFi, the lender, and third parties? Get this in writing.

What happens if the as-completed appraisal comes in lower than expected?

How long is the current average timeline for ADU projects in my state?

Do I need to join a credit union? Which one, and what does membership require?

What can cause my application to be denied after I've already paid for the appraisal?

Are there any restrictions on my contractor or on owner-building?

What does the certificate of completion process look like after my ADU is built?

Questions to ask your contractor before you start the RenoFi process

Can you provide a line-item estimate that breaks costs into labor and materials? If they resist, this process will be painful.

Can you provide a preliminary contract with a payment schedule and change order procedures? RenoFi requires this.

Are you licensed (where required) and insured? RenoFi's due diligence will verify this.

Have you worked on ADU projects before? Contractors who know the ADU permitting process produce better documentation.

What's your realistic timeline from permit to certificate of occupancy? This affects how long you'll pay any renovation-period charges.

What happens after your ADU is built

Once your ADU is complete, RenoFi coordinates a final inspection to verify the work matches the approved plans. If everything checks out, they issue a certificate of completion, and any temporary renovation-period charges from the lender are removed.

If the inspection reveals issues — work that doesn’t match plans, code violations, or safety concerns — you’ll need to resolve them first. The lesson: build to plan, build to code, and document everything during construction.

Final Verdict: Should You Use RenoFi for Your ADU?

After analyzing 124+ published reviews, BBB complaints, Glassdoor employee perspectives, and comparing the product against every major alternative, here’s where we land.

Green light — RenoFi is probably your best path if:

You bought your home in the last few years, have limited equity, want to build an ADU that will meaningfully increase property value, have a contractor who can produce detailed documentation, can tolerate a 30–60+ day process, and want to keep your current mortgage rate. In this scenario, RenoFi solves a financing gap that nothing else on the market addresses as well. Thousands of homeowners have used it successfully — the key is going in prepared.

Yellow light — proceed carefully if:

Your project is complex (large scope, unusual property, self-employed), you’re particular about timeline, or your contractor isn’t accustomed to producing detailed breakdowns. RenoFi can still work, but prepare for a longer process and get everything in writing.

Red light — use an alternative if:

You have enough equity for a standard HELOC (take the faster path), RenoFi products aren’t available in your state, you need funds within two weeks, you can’t take on monthly payments (explore a home equity investment), or your project is under $50K.

The one-sentence takeaway

RenoFi is not the fastest or simplest way to finance an ADU — but for homeowners who lack the equity for a standard HELOC and want to keep their current mortgage, it can create borrowing power that nothing else on the market matches.

Frequently Asked Questions

Is RenoFi a legitimate company?

Yes. RenoFi (Renovation Finance LLC) is a licensed mortgage broker, NMLS #1802847, headquartered in Berwyn, Pennsylvania. The company is backed by institutional investors including First Round Capital, Canaan Partners, and Comcast Ventures. It holds an A- rating from the BBB and a 4.6-star TrustScore on Trustpilot across 124+ published reviews. It is not a direct lender — it brokers loans through credit union partners.

How long does RenoFi take to close?

Typically about 30-60 days from document submission to closing for standard projects. Complex projects, incomplete documentation, or delays from the lending partner can extend this. The best way to stay on the faster end: have all your documents — especially contractor estimates with labor and material breakdowns — complete before you start.

What credit score do you need for RenoFi?

Most lending partners require a minimum of around 640, though this varies by lender. Higher scores qualify for better terms.

How much can you borrow with RenoFi?

Borrowing limits depend on your lender, property, and project. Most lending partners allow up to 125% of current value and up to 90% of after-renovation value, with some going higher.

Can you use RenoFi for an ADU?

Yes. RenoFi actively markets ADU financing and has dedicated ADU advisors. ADUs are a strong fit for the ARV model because they can produce meaningful property value increases.

Does RenoFi work for new homeowners?

Yes — this is exactly who RenoFi is designed for. Most lending partners have no seasoning requirement, meaning you can apply shortly after closing on your home purchase.

Do you have to use RenoFi's contractor?

No. You can use your own contractor. They must pass RenoFi's due diligence review, which includes insurance verification, any state-required licensing, and detailed project documentation. RenoFi does not endorse or guarantee any contractor's work.

Can you owner-build with RenoFi?

With limitations. If you're not a GC by trade, lending partners may cap you at three subcontractors and will scrutinize your project more closely.

What are RenoFi's fees and costs?

Borrower-paid costs may include: lender origination and closing costs, a borrower-paid as-completed appraisal (non-refundable), possible temporary renovation-period charges from the lender during construction, and on select mortgage products, possible borrower-paid broker compensation. Get every charge confirmed in writing before ordering the appraisal.

What if the appraisal comes in low?

Your borrowing power decreases. If the gap between project cost and available funds is too large, the loan may not work. The appraisal fee is non-refundable regardless of outcome.

What states is RenoFi available in?

Product and state availability varies by lender and loan type. RenoFi's ARV-based products are not available in Texas, and some products may have restrictions in other states. Confirm your specific product availability directly with RenoFi before paying for an appraisal.

What if I'm in Texas?

RenoFi's ARV products are not available in Texas due to the state's home equity lending regulations (Texas Constitution Article XVI, Section 50). Texas homeowners building ADUs have several alternatives: standard HELOCs (available in Texas with state-specific rules), FHA 203(k) renovation loans, construction loans, or personal loans for smaller projects.

What are the best RenoFi alternatives for ADU financing?

It depends on your equity position. Strong equity: standard HELOC (fastest path). Low equity: RenoFi or FHA 203(k). Equity-rich but cash-flow-poor: home equity investment. Large complex project: construction loan. Want to compare: lending marketplace.

How We Researched This Review

This review is based on direct analysis of:

- RenoFi's official website, FAQ, disclosure page, account terms of use, wholesale page, qualification requirements, and application checklist

- Trustpilot — 124+ published reviews, 4.6 TrustScore (as of April 4, 2026)

- Better Business Bureau — A- rating, 6 complaints filed with company responses

- Bankrate — editorial review with 3.8/5 customer rating

- BiggerPockets — forum discussions from ADU builders and real estate investors evaluating RenoFi

- Glassdoor — ~24 employee reviews providing operational context (3.6/5 rating)

- Reddit — threads from r/AccessoryDwellings, r/Homebuilding, r/Mortgages, and r/RealEstate

We compared RenoFi’s product structure against five alternative financing paths using documented terms from each provider. Our financial comparison examples are illustrative and use conservative assumptions — they are not personalized loan offers, rate quotes, or guarantees of any kind.

Editorial independence: The Dwelling Index earns revenue through affiliate partnerships with some financing providers mentioned in this review. Our editorial recommendations and verdict are based on independent research. Affiliate relationships never influence our ratings, rankings, or advice.

Last verified: April 4, 2026. Financing products, terms, and availability change frequently. Confirm current details directly with any provider before applying.

Not sure where to start?

Whether RenoFi is the right fit or not, the first step is the same.

Find out what your city allows and what your property can support — before you talk to any lender.