Freddie Mac ADU Rules in 2026: Eligibility, Rental Income, and Your Best Next Step

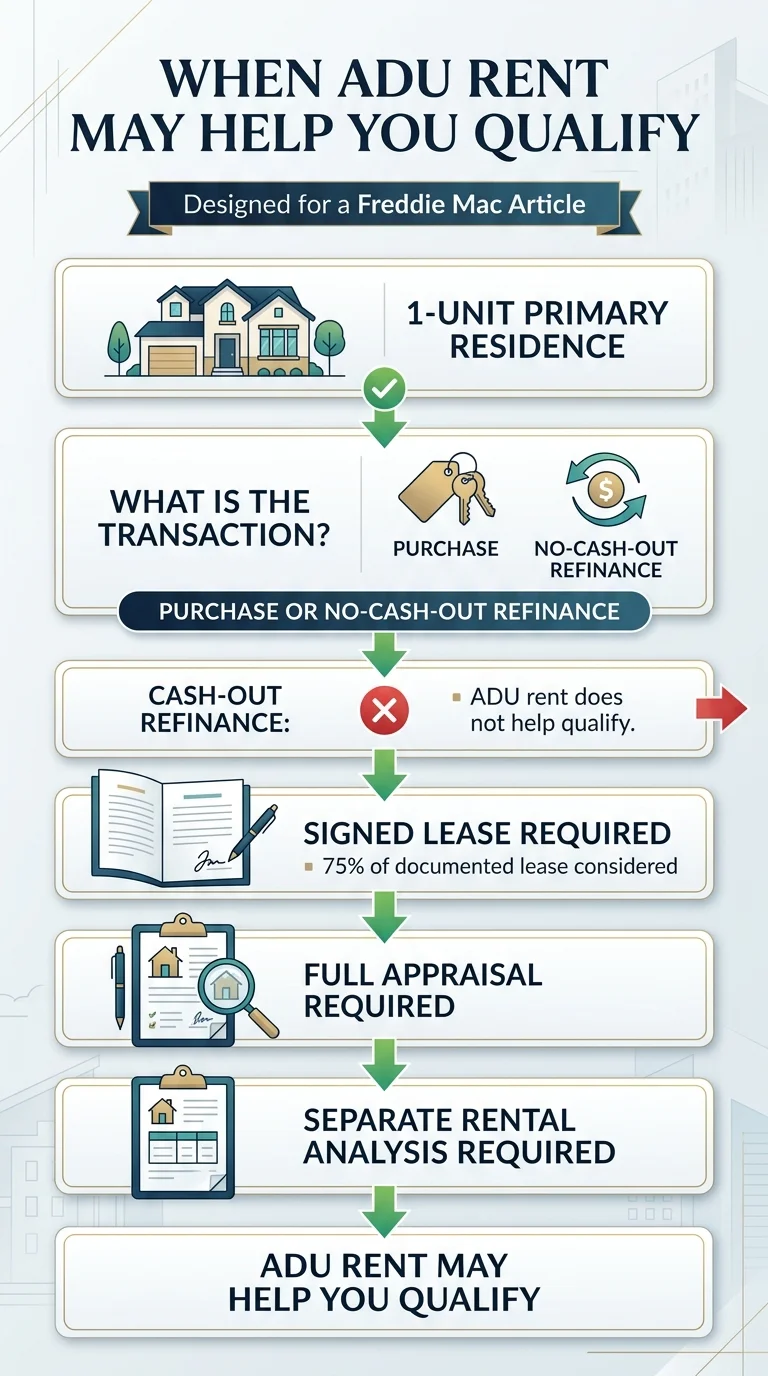

Freddie Mac ADU rules allow one accessory dwelling unit on eligible 1-, 2-, and 3-unit properties — and on a 1-unit primary residence, documented ADU rent may help qualify you for a purchase or no-cash-out refinance. That’s the headline. But most articles stop there and skip the details that actually decide whether your loan closes: the 75% lease haircut, the 30% income cap, a mandatory full appraisal with ADU-specific comps, landlord education requirements, and the fact that cash-out refinances and projected rent from a unit under construction are both excluded.

This guide translates every current Freddie Mac ADU rule into plain English, walks through the rental income math with real examples, compares Freddie to Fannie Mae, FHA, and HELOC paths, and gives you the exact questions to ask a lender before you spend a dollar on plans or permits.

Sources: Freddie Mac Guide Section 5601.2, Chapter 5306, Bulletins 2022-11, 2025-15, 2026-1, ADU Fact Sheet (February 2026)

| Your situation | Freddie Mac answer | Why |

|---|---|---|

| 1 ADU on a 1-, 2-, or 3-unit property | Usually eligible | Core rule — Guide Section 5601.2 |

| Need ADU rent to help qualify — 1-unit primary, purchase or no-cash-out refi | Possible with conditions | 75% lease rule, 30% income cap, full appraisal required |

| Cash-out refinance using ADU rent to qualify | Not allowed | Freddie Mac excludes cash-out refis from the rent-to-qualify provision |

| Building a new ADU and want projected rent to qualify | Not allowed | Projected rent from an ADU under construction cannot be used to qualify |

| 4-unit property with an ADU | Not eligible | Section 5601.2 only allows ADUs on 1-, 2-, and 3-unit properties |

| Freddie Mac as your direct lender | Not how it works | Freddie Mac buys loans — you work with a bank, credit union, or mortgage company |

Source: Freddie Mac Guide Section 5601.2; Freddie Mac ADU Fact Sheet (February 2026); Guide FAQ FA1520.

A detached ADU on a 1-unit primary residence — Freddie Mac’s core eligibility scenario.

What Does Freddie Mac Actually Allow for ADUs?

Freddie Mac allows eligible mortgages on properties with one accessory dwelling unit on 1-, 2-, and 3-unit properties. This applies to every Freddie Mac mortgage product — not just affordable or specialty programs. You can purchase, refinance, or build an ADU through a Freddie Mac-backed loan, and in certain situations, the ADU’s rental income can even help you qualify.

That’s the framework. Now here’s the stuff that actually decides whether your loan closes.

One ADU on 1-, 2-, and 3-unit properties

This is the foundational rule. Your property can have one primary dwelling (single-family home) plus one ADU. Or a duplex plus one ADU. Or a triplex plus one ADU. The combined total can’t exceed four units.

This expansion happened in June 2022 through Bulletin 2022-11. Before that, Freddie Mac only backed ADU properties that were single-family homes.

One ADU means one. If your property has two ADUs (increasingly common in states that allow multiple ADUs), the property doesn’t qualify under these provisions regardless of how many total units you have.

A note on Fannie Mae: Effective March 31, 2026, Fannie Mae expanded its own ADU rules significantly for loans using the new UAD 3.6 appraisal format. Fannie Mae now allows ADUs on 2- and 3-unit properties (matching Freddie Mac) and goes further by allowing up to three ADUs on 1-unit properties. We cover the full comparison below. See our Fannie Mae ADU guide for details.

Source: Freddie Mac Guide Section 5601.2; Freddie Mac Bulletin 2022-11; Fannie Mae Selling Guide Supplement: UAD 3.6 Policy (December 2025).

Your ADU’s legal status matters — a lot

The ADU must comply with local zoning in one of three ways:

There’s one exception worth knowing: on a 1-unit property, an ADU with illegal zoning may still be eligible under conditions outlined in Guide Section 5601.2(c). This exception doesn’t exist for 2- or 3-unit properties, and rental income from an illegally zoned ADU can never be used to qualify, period.

If your ADU was built without permits but your city has since adopted ADU-friendly ordinances, getting retroactive permitting may be possible and is often worth the effort. It opens both Freddie Mac eligibility and the rental income qualification pathway.

Source: Freddie Mac Guide Section 5601.2; Freddie Mac ADU Fact Sheet (February 2026).

Freddie Mac is not a lender — and that changes everything

This is the single most misunderstood thing about Freddie Mac ADU financing. You will never call Freddie Mac, fill out a Freddie Mac application, or get a check from Freddie Mac.

Freddie Mac (the Federal Home Loan Mortgage Corporation) is a government-sponsored enterprise that buys mortgages from lenders on the secondary market. When Freddie Mac says “we will purchase mortgages on properties with ADUs,” what they’re really saying is: lenders, you can make these loans and sell them to us, which means you won’t be stuck holding them on your books.

That’s the green light that makes ADU-friendly conventional loans available at your local bank, credit union, or mortgage company. But each lender decides whether to offer these programs and often adds their own restrictions called “overlays.” Pennymac, for instance, adopted Freddie Mac’s ADU expansion but specifically excluded CHOICERenovation for ADUs due to an internal overlay.

The practical takeaway: don’t assume your lender offers every Freddie Mac ADU program just because Freddie Mac allows it. You may need to shop multiple lenders.

Source: Freddie Mac corporate overview; Pennymac Announcement 22-44.

Freddie Mac ADU core rules at a glance. Source: Freddie Mac Guide Section 5601.2 and ADU Fact Sheet (February 2026).

Can ADU Rental Income Help You Qualify?

Yes — but in a narrower lane than most articles make it sound. We’re going to walk through the exact rules, then do the math with real numbers.

When ADU rent counts toward qualification

All of these must be true simultaneously:

That’s a real checklist, and every item matters. Miss one and the rental income gets zeroed out of your qualification.

Source: Freddie Mac Guide Chapter 5306; Freddie Mac ADU Fact Sheet (February 2026); Guide FAQ FA1520.

When Freddie Mac ADU rental income may help you qualify. Source: Freddie Mac Guide Chapter 5306.

The 75% lease rule and 30% income cap — with actual math

Scenario: You’re buying a $475,000 home with a detached 1-bedroom ADU. The ADU has a signed lease at $1,800/month. Your W-2 employment income is $7,000/month.

| Step | What happens | The math |

|---|---|---|

| 1. Start with gross lease | Your ADU lease amount | $1,800/mo |

| 2. Apply 75% lease haircut | Freddie Mac counts 75% of documented lease | $1,800 × 0.75 = $1,350/mo |

| 3. Calculate total qualifying income | Your employment income + counted ADU rent | $7,000 + $1,350 = $8,350/mo |

| 4. Check the 30% cap | ADU rent as % of total income | $1,350 ÷ $8,350 = 16.2% — Under 30% |

| 5. Final qualifying income | What your lender uses | $8,350/mo |

That extra $1,350/month matters. Depending on current rates and your debt-to-income ratio, it can meaningfully expand the loan amount you qualify for — often the difference between getting approved and falling short.

When the 30% cap actually bites

If your employment income were $3,200/month and your ADU rented for $2,200/month, the 75% rule gives you $1,650 in countable rent. But $1,650 ÷ ($3,200 + $1,650) = 34% — over the 30% cap. Your lender would need to reduce the counted rental income to stay under the cap, shrinking the benefit.

The pattern: ADU rental income is most powerful for borrowers who already have solid income and use the ADU rent as a qualification boost, not a primary income source.

These are illustrative examples only — not guarantees of qualification or loan approval. Actual results depend on current interest rates, your complete financial profile, property specifics, and your lender’s underwriting requirements.

Source: Freddie Mac Guide Chapter 5306; Freddie Mac ADU Fact Sheet (February 2026).

Why cash-out refinance is different

If you’re doing a cash-out refinance — pulling equity from your home — you cannot use ADU rental income to qualify under the Chapter 5306 provisions. This trips up homeowners who built an ADU, saw their property value increase, and want to tap that equity. You can still do a cash-out refi on a property with an ADU through Freddie Mac, but the ADU rent doesn’t help your qualification math.

The no-cash-out refinance path does work for rental income qualification, and this is specifically how the post-construction refinance helps: you can refinance short-term ADU financing (a construction loan, HELOC draw, or personal loan you used to build the ADU) into a conventional mortgage and use the ADU rent to qualify — provided the ADU is complete and generating documented rental income at that point.

Does Your Property Actually Qualify as an ADU Under Freddie Mac?

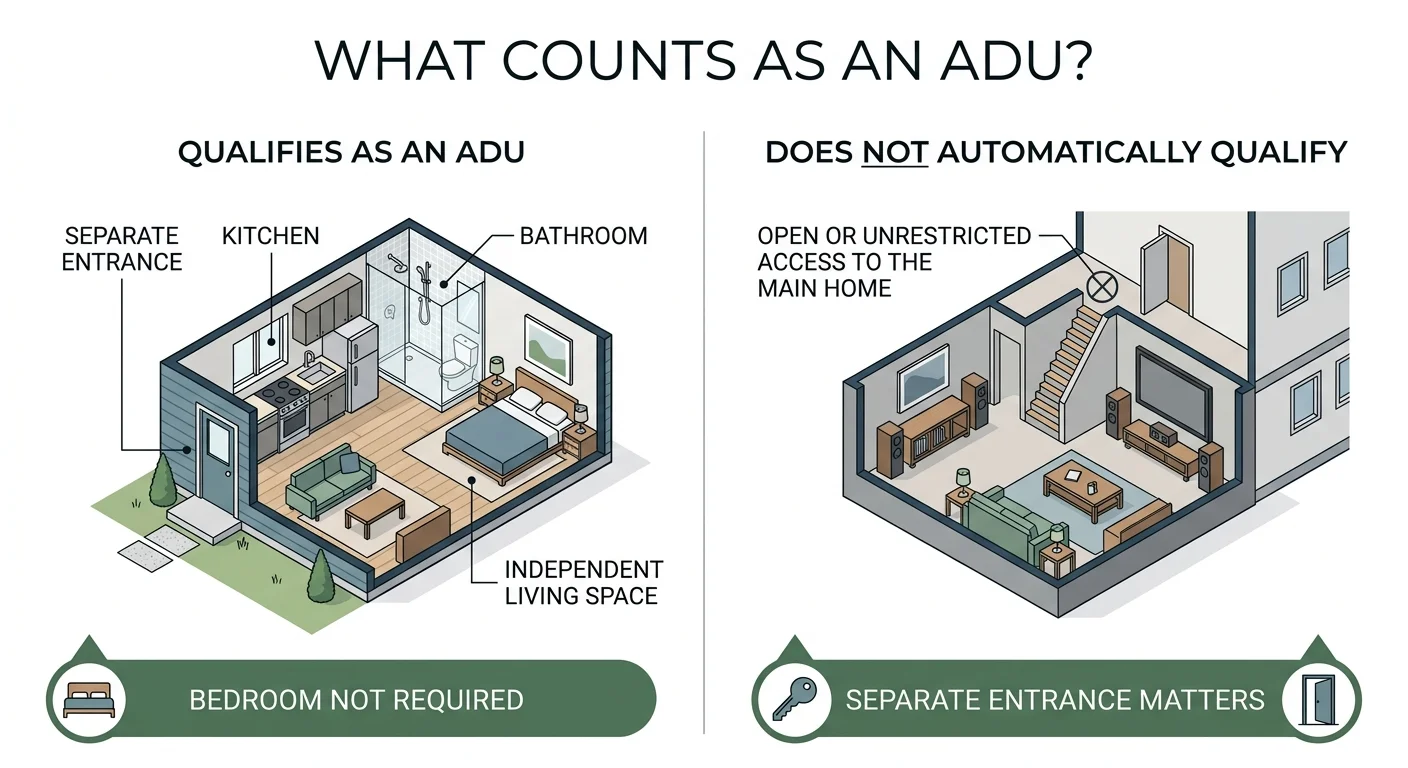

Not every extra living space is an ADU in Freddie Mac’s eyes. This matters because if the appraiser doesn’t classify the space as an ADU, the whole framework changes — suddenly you might have a 2-unit property instead of a 1-unit with an ADU, and that affects your loan terms, down payment, and qualification math.

Freddie Mac’s ADU definition (in plain English)

An ADU must be:

An ADU does not need:

A bedroom (efficiency/studio layouts qualify)

A specific minimum or maximum square footage (though manufactured home ADUs need 400+ sq ft)

The ADU can be attached (basement conversion, above-garage apartment, home addition), detached (backyard cottage, freestanding guest house), or within the main structure — as long as it meets the independence and separate-entrance tests.

Source: Freddie Mac Guide Section 5601.2; Freddie Mac ADU Appraisal Report Checklist (November 2025); Guide FAQ FA1505, FA1507, FA1508.

What counts as an ADU under Freddie Mac rules. Source: Freddie Mac Guide FAQ FA1505, FA1507, FA1508.

Three edge cases that change the classification

A finished basement with unrestricted access to the main house is not an ADU.

If someone can walk from the main home into the basement without going outside or through a separate locked entrance, Freddie Mac doesn’t consider it independent. The space may add value, but it’s not an ADU under these rules.

A missing cooking appliance doesn’t automatically disqualify the ADU.

Freddie Mac’s FAQ clarifies that the absence of a single cooking appliance does not by itself change the classification. The appraiser evaluates the overall configuration, independence, and utility of the space.

Manufactured home ADUs are allowed — with conditions.

As of February 2026 (Bulletin 2025-15), the primary dwelling can be a multiwide manufactured home (including CHOICEHome properties) and still have a manufactured home ADU on the lot. This was a major expansion. Fannie Mae has since also expanded manufactured home ADU eligibility under its UAD 3.6 policy.

Source: Freddie Mac Guide FAQ FA1505, FA1507; Freddie Mac Bulletin 2025-15; Fannie Mae Selling Guide Supplement: UAD 3.6 Policy.

Free ADU Feasibility Report

Does your property qualify?

Before you shop lenders or chase appraisals, confirm your property and ADU concept are actually feasible at your address.

Get Your Free ADU Feasibility Report in 60 SecondsThe Honest Challenge With Freddie Mac ADU Loans

We’re going to be straight with you — because everything we say after this is 10x more credible when we don’t sugarcoat the hard part.

The appraisal is where most Freddie Mac ADU loans face real friction.

Freddie Mac requires the appraiser to find comparable sales and comparable rentals involving ADUs, and in many markets those comps simply don’t exist in enough volume yet. If the appraiser can’t adequately support the value with ADU-comparable properties, the loan may stall.

This doesn’t mean it’s impossible. Appraisers can expand their geographic search area, use older comparable sales, and work with properties that have similar ADU configurations even if they’re not perfect matches. And the comp situation is improving year over year as ADU construction accelerates. Freddie Mac’s own research found ADU growth concentrated in Sun Belt states, with double-digit growth in several major metro areas since 2015 — which means more comps in more markets every quarter.

The practical move: before you commit to a Freddie Mac ADU loan path, talk to a local appraiser who has experience with ADU properties in your area. A 15-minute conversation can save you months of frustration.

Source: Freddie Mac ADU Appraisal Report Checklist (November 2025); Freddie Mac Research, “ADUs Can Increase Housing Stock” (January 2023).

Which Freddie Mac Loan Product Fits Your ADU Situation?

There are six common ADU scenarios, and each one points to a different Freddie Mac product path. Find yours.

You're buying a home that already has an ADU

Your path: Standard Freddie Mac purchase mortgage (any eligible product).

This is the simplest scenario. The home has an existing, legal ADU. You get a conventional loan, the appraiser values the property including the ADU, and if you want to use the ADU rental income to qualify (and the property is a 1-unit primary residence), you follow the Chapter 5306 requirements above. Down payment depends on the product and property type. For eligible 1-unit primary-residence scenarios, low-down-payment options such as Home Possible or HomeOne can go as low as 3%. Multi-unit properties have different maximum LTV limits — your lender will confirm the specific requirement for your situation.

Source: Freddie Mac Home Possible; Freddie Mac HomeOne; Freddie Mac ADU Fact Sheet.

You want to build a new ADU or convert an existing structure

Your path: CHOICERenovation® mortgage.

This is Freddie Mac's renovation loan, and it's the flagship product for ADU construction. You can roll the cost of building a new ADU or converting a garage, basement, barn, or shed into an ADU directly into your mortgage — no separate construction loan needed.

- Available for purchase (buy a home + build an ADU in one loan) or no-cash-out refinance

- For eligible 1-unit primary-residence scenarios, down payment can go as low as 3% for first-time buyers and 5% for repeat buyers. Multi-unit scenarios have different LTV limits.

- Down payment calculated on the lesser of (purchase price + construction cost) or the completed appraised value

- ADU construction must be completed before final loan closing for the refinance path

- Freddie Mac specifically states it can be used to add a factory-built/prefab ADU for low-to-moderate income borrowers

Critical rule most articles miss: If the ADU is part of the renovation project being funded by the CHOICERenovation mortgage, projected rent from that ADU cannot be used to qualify for the loan. Only rent from units not included in the renovation project may be used for qualification. This changed with Bulletin 2026-1, effective for applications received on or after May 4, 2026.

Source: Freddie Mac CHOICERenovation Fact Sheet; Freddie Mac Bulletin 2026-1; Guide FAQ FA1520.

You already built an ADU and need to refinance the short-term debt

Your path: No-cash-out refinance (CHOICERenovation or standard conventional).

You used a construction loan, HELOC, or personal loan to build your ADU. Now it's complete and you want to refinance that short-term debt into a conventional mortgage at better terms. CHOICERenovation specifically allows a no-cash-out refinance to pay off short-term financing used for ADU construction, provided the work is completed before the note date. Since the ADU is already built and (ideally) rented, you can potentially use the documented ADU rental income to help qualify for this refinance — following all the Chapter 5306 rules. This is the scenario where the rent-to-qualify benefit shines brightest.

You want to cash out equity from your ADU-enhanced property

Your path: Standard cash-out refinance (any Freddie Mac product).

You can do a cash-out refi on a property with an ADU to access the equity the ADU has created. Just know that ADU rental income cannot be used to qualify for a cash-out refinance under Chapter 5306. Your other income must support the loan on its own.

You want to add energy-efficient upgrades to an existing ADU

Your path: GreenCHOICE Mortgage®.

Solar panels, energy-efficient windows, high-efficiency HVAC, insulation upgrades — GreenCHOICE lets you finance these improvements at conventional rates. A niche product, but relevant for homeowners with older ADUs that need modernizing.

Low-to-moderate income, building an ADU for housing stability

Your path: Home Possible® with an ADU, or CHOICERenovation for a factory-built ADU.

Home Possible allows up to 97% LTV on eligible 1-unit properties and was designed for borrowers at or below area median income. Combined with CHOICERenovation's ability to finance factory-built (prefab) ADU additions, this is Freddie Mac's most accessible ADU path for homeowners who couldn't otherwise afford the project.

Source: Freddie Mac Home Possible; Freddie Mac ADU Fact Sheet (February 2026).

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation. Full Disclosure

Found your scenario? The next step is talking to the right lender.

Freddie Mac doesn’t lend directly — you need a bank, credit union, or mortgage company that offers the specific program you need.

Freddie Mac vs. Fannie Mae vs. FHA vs. HELOC: Picking the Right Path

Freddie Mac is one of several legitimate ADU financing paths, and it’s not always the best one. The right path depends on your property type, existing mortgage, equity position, and whether you need rental income to qualify. Here’s the current landscape as of April 2026.

The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research. Full Disclosure

| Feature | Freddie Mac | Fannie Mae (incl. UAD 3.6) | FHA | HELOC / Home Equity |

|---|---|---|---|---|

| ADU on multi-unit property | 1-, 2-, 3-unit | 2- and 3-unit (UAD 3.6 loans, eff. Mar 31, 2026) | 1-unit only | N/A (separate product) |

| Max ADUs allowed | 1 per property | Up to 3 on 1-unit (UAD 3.6 only); 1 on 2-3 unit | 1 | N/A |

| Manufactured home with ADU | Yes — multiwide (Feb 2026) | Yes — incl. MH Advantage (UAD 3.6 only) | Limited | N/A |

| ADU rent to qualify | Yes — purchase & no-cash-out refi on 1-unit primary | Yes — purchase & limited cash-out refi on 1-unit principal | Yes — up to 75% of est. rent | No |

| Rental income cap | 30% of total qualifying income | Subject to documentation rules | 75% of est. rent (50% for new ADU via 203k) | N/A |

| Projected rent from ADU under construction? | No | No | Yes — 50% via 203(k) for new ADU | N/A |

| Renovation product for ADU | CHOICERenovation® | HomeStyle® Renovation | 203(k) | N/A |

| Keeps existing first mortgage? | No (replaces it) | No (replaces it) | No (replaces it) | Yes |

| Best for | Multi-unit w/ ADU, CHOICERenovation, post-build refi | Multiple ADUs (UAD 3.6), rental income qualification | Lower credit, projected rent on new construction | Preserving a low first-mortgage rate |

Sources: Freddie Mac Guide 5601.2 & Chapter 5306; Fannie Mae Selling Guide Supplement: UAD 3.6 Policy (Dec 2025); Fannie Mae Selling Guide B3-3.8-01 (Oct 2025); HUD Mortgagee Letter 2023-17. Verified April 4, 2026.

When Freddie Mac is your strongest path

- You have a duplex or triplex with an ADU and your lender isn't yet set up for Fannie Mae's UAD 3.6 expansion (many aren't as of early 2026)

- You want to use CHOICERenovation to roll ADU construction into a single mortgage

- You built your ADU and want a no-cash-out refinance using documented rental income to qualify

- You qualify for Home Possible or HomeOne and want the lowest possible down payment on a 1-unit ADU property

When Fannie Mae might fit better

Full guide- You have (or want) multiple ADUs on a 1-unit property — Fannie Mae now allows up to three under UAD 3.6

- Your lender has adopted UAD 3.6 and offers better pricing on Fannie Mae products

- You're using ADU rental income to qualify on a purchase or limited cash-out refinance

When FHA might fit better

- Your credit score is below conventional minimums

- You want to build a new ADU and use projected rental income to qualify — FHA's 203(k) program allows 50% of projected rent for new ADU construction

- You're comfortable with mortgage insurance premiums for the life of the loan

When a HELOC or home equity loan is the real answer

Full guide- You locked in a 3% or 3.5% mortgage in 2020-2021 and refuse to refinance into today's rates

- A HELOC or home equity loan keeps your low first-mortgage rate while funding ADU construction

- ADU rental income doesn't help qualification via HELOC, but you avoid giving up your existing rate

Preserving your existing low-rate first mortgage

Here’s a scenario we see constantly: a homeowner locked in a 3% or 3.5% mortgage in 2020–2021, wants to build an ADU, but refuses to refinance into today’s rates. Completely rational. A cash-out refi through Freddie Mac would mean giving up that rate on your entire mortgage balance.

The alternative: a HELOC or home equity loan that sits behind your first mortgage. You keep your low rate, borrow against existing equity, and fund the ADU construction without disturbing your primary loan.

A detached ADU behind a craftsman home — the kind of property that can qualify for multiple Freddie Mac loan paths.

CHOICERenovation: The Deep Dive

If you’re building a new ADU or converting an existing structure, CHOICERenovation is likely the Freddie Mac product that brought you to this page. Here’s what the program actually delivers — and where it has limits.

What CHOICERenovation can do for your ADU project

CHOICERenovation wraps the cost of renovations — including ADU construction — into a single conventional mortgage. One loan, one closing, one monthly payment. You don’t need a separate construction loan that you then refinance later.

Freddie Mac explicitly states that CHOICERenovation can be used to:

- Renovate an existing residence to add an ADU

- Make an ADU renovation part of a home purchase transaction

- Finance a no-cash-out refinance to pay off short-term ADU construction debt

- Add a factory-built (prefab) ADU for low-to-moderate income borrowers

What CHOICERenovation requires

The property must have an existing dwelling — CHOICERenovation is a renovation product, not a ground-up construction-on-vacant-land product. You need renovation plans, cost estimates from a contractor, and an appraisal that includes the projected completed value. For the refinance path, ADU construction must be completed before the note date.

The projected-rent restriction (don’t skip this)

If the ADU is part of the renovation project being funded by your CHOICERenovation mortgage, projected rent from that ADU cannot be used to qualify.

This is clearly stated in Freddie Mac’s FAQ and reinforced by Bulletin 2026-1 (effective May 4, 2026 for CHOICERenovation rental income qualification specifics). This means you can’t use CHOICERenovation to build an ADU and count the future ADU rent in your qualification — at least not in the same transaction.

A workaround: Build the ADU using CHOICERenovation (qualifying on your other income alone), then later do a no-cash-out refinance once the ADU is complete and generating documented rental income.

Source: Freddie Mac CHOICERenovation Fact Sheet; Freddie Mac Bulletin 2026-1; Guide FAQ FA1520.

When a construction loan is cleaner

Construction financing can be structured as one-time-close or two-time-close depending on the product and lender. Some paths convert to permanent financing within one transaction; others require a second closing. If your project involves extensive ground-up work, an unusual property, or if your lender doesn’t offer CHOICERenovation for ADUs, a construction path may be more straightforward.

The Appraisal: Where Freddie Mac ADU Loans Get Real

The appraisal is not a formality. For ADU properties — especially when rental income is involved — it’s often the most complex and consequential step in the loan process.

What the appraiser must deliver

For any Freddie Mac loan on a property with an ADU, the appraiser must:

- Confirm the ADU meets Freddie Mac's definition (separate entrance, kitchen, bathroom, independent from primary dwelling)

- Describe the ADU: general condition, finished square footage, total number of rooms including bedrooms and bathrooms

- Determine whether the property is properly classified as a 1-unit with ADU versus a 2-unit property

- Support the property's value with comparable sales

Additional appraisal requirements when ADU rent is used to qualify

When you’re using ADU rental income under Chapter 5306, the bar goes up:

- ACE (appraisal waiver) is never acceptable, even if LPA offers one

- Sales Comparison Approach must include at least one comparable sale with an ADU

- Rental analysis must include at least three comparable rentals supporting market rent, and at least one must include a rented ADU

- The rental analysis can be documented on Form 1000

The practical challenge — and what’s changing

In markets with strong ADU adoption, finding comps is increasingly manageable. In markets where ADUs are newer, the appraiser may need to expand geographically or temporally. Freddie Mac allows older comparable sales and sales without ADUs when the subject ADU conforms to local zoning — but the appraiser must still support the value.

Our recommendation: talk to an experienced local appraiser before you commit to the loan. A brief consultation to ask “can you find ADU comps in this area?” can save you significant time and money.

2026 update

Fannie Mae and Freddie Mac rolled out UAD 3.6, a redesigned Uniform Appraisal Dataset that expands ADU and manufactured housing reporting capabilities. Lenders using the new format (mandatory by November 2, 2026) will have a more structured way to document ADU characteristics and valuation.

Source: Freddie Mac ADU Appraisal Report Checklist (November 2025); Freddie Mac Guide Section 5601.2; Fannie Mae/Freddie Mac UAD 3.6 announcements.

What to Ask Your Lender Before You Spend Money on Plans or Permits

Most homeowners walk into a lender conversation and ask “can I get a loan for my ADU?” That’s too vague. These specific questions surface whether this lender can actually close your file:

1. Do you originate Freddie Mac-backed loans on properties with ADUs?

Some lenders have never closed one.

2. Do you offer CHOICERenovation, and can you use it for ADU construction or conversion?

Some lenders carry CHOICERenovation but exclude ADU projects through an internal overlay.

3. If I need ADU rental income to qualify under Guide Chapter 5306, can you process that?

This requires specific documentation and appraisal handling.

4. What overlays do you apply beyond Freddie Mac's published guide requirements?

Higher credit score minimums, larger down payments, geographic restrictions — ask directly.

5. Do you have an appraiser relationship in my market who has experience valuing ADU properties?

The appraiser's familiarity with ADU comps in your area is critical.

6. If Freddie Mac turns out not to be the cleanest path for my situation, what alternative do you recommend?

A good loan officer will tell you if a HELOC, Fannie Mae path, or construction loan is a better fit.

If you’re getting vague answers or your loan officer seems unfamiliar with Guide Section 5601.2, that’s a signal to keep shopping.

Ready to compare your options?

Freddie Mac ADU Policy Timeline: What Changed and When

Freddie Mac’s ADU rules have expanded significantly since 2022. This timeline helps you confirm which rules are current.

| Date | Update | What changed |

|---|---|---|

| June 2022 | Bulletin 2022-11 | ADU eligibility expanded from 1-unit to 1-, 2-, and 3-unit properties. ADU rental income qualification added for 1-unit primary residences. CHOICERenovation approved for ADU construction/renovation. "ADU" added to Freddie Mac glossary. |

| Nov 2025 | Bulletin 2025-15 | Manufactured home ADU eligibility expanded: primary dwelling can now be a multiwide manufactured home, including CHOICEHome. Effective Feb 9, 2026. |

| Nov 2025 | Appraisal Checklist update | Updated ADU Appraisal Report Checklist with enhanced guidance for ADU valuation, definition confirmation, and rental analysis. |

| Feb 2026 | Fact Sheet update | Refreshed ADU Fact Sheet reflecting all current requirements. |

| Feb 2026 | Bulletin 2026-1 | Enhanced specificity for ADU eligibility. CHOICERenovation rental income qualifying updates effective May 4, 2026 — clarifies that rent from units included in the renovation project cannot be used to qualify. |

| March 2026 | UAD 3.6 rollout | Expanded ADU and manufactured housing reporting within the new Uniform Appraisal Dataset. Mandatory for all GSE appraisals by Nov 2, 2026. Also enables Fannie Mae's expanded ADU eligibility (2-3 unit properties, multiple ADUs on 1-unit). |

Source: Freddie Mac Guide Bulletins 2022-11, 2025-15, 2026-1; Fannie Mae Selling Guide Supplement: UAD 3.6 Policy. Verified April 4, 2026.

Edge Cases That Keep Sending People Back to Search

These are the questions we see over and over in forums, Reddit threads, and lender conversations. If you’re still here, one of these is probably yours.

"Do I really need 20% down for a home with an ADU?"

No. This is one of the most persistent myths in ADU financing. For eligible 1-unit primary-residence scenarios, Freddie Mac offers low-down-payment options: Home Possible and HomeOne can go as low as 3%. CHOICERenovation starts at 3% for first-time buyers on 1-unit primary residences. Multi-unit properties and renovation scenarios have different maximum LTV limits that your lender will specify. The actual down payment depends on the specific product, property type, and your lender's overlays — but 20% is not the default.

Source: Freddie Mac Home Possible; Freddie Mac HomeOne; CHOICERenovation Fact Sheet.

"Can Freddie Mac finance a 2-unit or 3-unit property with an ADU?"

Yes. One ADU on a 2-unit or 3-unit property is eligible, as long as the total unit count doesn't exceed 4. This has been allowed since June 2022.

"What about a 4-unit property with an ADU?"

Not eligible. Freddie Mac's ADU rule in Section 5601.2 allows one ADU on 1-, 2-, and 3-unit properties only. A 4-unit property does not qualify for an ADU under this provision.

"What if my ADU was built without permits?"

On a 1-unit property, an ADU with illegal zoning may still be eligible under specific conditions in Guide Section 5601.2(c). On 2- or 3-unit properties, the ADU must be legal, legal non-conforming, or in an area without zoning — no illegal exception. Either way, rental income from an illegally zoned ADU can never be used to qualify.

"Can projected rent from a new ADU under construction be used to qualify?"

No. Freddie Mac's FAQ (FA1520) states that projected rental income from an ADU undergoing construction or renovation cannot be used for qualifying purposes. You need an existing, completed ADU with documented rental income. FHA's 203(k) program does allow projected rent for new ADU construction — that's a key differentiator if this is your situation.

Source: Freddie Mac Guide FAQ FA1520; HUD Mortgagee Letter 2023-17.

"Can I use ADU rent on a cash-out refinance?"

No. ADU rental income qualification under Chapter 5306 is only available for purchase and no-cash-out refinance transactions.

"I live in the ADU and rent out the main house. Is that allowed?"

The property can still be treated as a primary residence if a borrower occupies the ADU. But rent from the main dwelling cannot be used to qualify the mortgage in that scenario.

Source: Freddie Mac Guide FAQ FA1519; Guide Section 5306.1.

"What if I already have a 3% mortgage and refuse to refinance?"

Completely rational. A HELOC or home equity loan that sits behind your first mortgage is probably your better path. You keep your low rate, borrow against equity, and fund the ADU construction separately.

See ADU HELOC and home equity options"Is a finished basement an ADU?"

Not automatically. A finished basement with unrestricted access to the main living area — no separate entrance, no lockable separation — does not meet Freddie Mac's ADU definition. A basement can qualify as an ADU if it has been converted with a separate entrance, kitchen, and bathroom that functions independently. A nicely finished rec room with an open staircase to the main floor doesn't count.

"Does Freddie Mac consider ADU rental income outside the 1-unit primary-residence lane?"

Yes. Guide Chapter 5306 also addresses rental income from ADUs on a subject 1- to 4-unit investment property and from ADUs on a non-subject investment property. The rules differ from the primary-residence provisions — work with your lender to understand the requirements for your specific scenario.

Source: Freddie Mac Guide Section 5306.1.

Your Next Step Based on Your Exact Scenario

You’ve made it through the rules. Now pick the path that matches where you are.

Buying a home with an existing legal ADU

Get pre-approved with a lender who offers Freddie Mac (or Fannie Mae) conventional loans. Ask the six questions above. If you want to use ADU rental income, confirm the lender can process Chapter 5306 requirements.

Building a new ADU and willing to refinance

Ask your lender about CHOICERenovation. Remember: projected rent from the ADU being built can't be used to qualify for this loan — you'll need to qualify on your other income.

Need to keep your current low-rate first mortgage

A HELOC or home equity loan is probably your path.

See ADU HELOC and home equity optionsAlready built an ADU with short-term financing

A no-cash-out refinance can convert that debt into a conventional mortgage, and documented ADU rental income may help you qualify.

ADU situation is unusual — multiple ADUs, unpermitted, or 4-unit property

Freddie Mac may not be your first stop. Fannie Mae's UAD 3.6 expansion allows multiple ADUs on 1-unit properties.

Explore all ADU financing pathsFree ADU Feasibility Report

Not sure which path is right for your property?

Our free ADU feasibility report checks your address, local ADU rules, and property potential — so you know what’s possible before you talk to a single lender.

See What You Can Build at Your AddressFreddie Mac ADU: Frequently Asked Questions

Is Freddie Mac a lender?

No. Freddie Mac buys mortgages from lenders on the secondary market. You'll work with a bank, credit union, or mortgage company that originates Freddie Mac-backed loans.

Does Freddie Mac allow an ADU on a primary residence?

Yes. One ADU on 1-, 2-, and 3-unit properties, using any Freddie Mac mortgage product. The ADU must be legal, legal non-conforming, or in an area without zoning (with a narrow exception for some 1-unit illegal-zoning situations). (Guide Section 5601.2)

Can I use ADU rental income to qualify for a Freddie Mac mortgage?

Yes, with conditions. The property must be a 1-unit primary residence, the loan must be a purchase or no-cash-out refinance, the ADU must already exist and be legally zoned, and the rental income is subject to a 75% lease haircut and a 30% income cap. A full appraisal with ADU-specific comps is required. (Guide Chapter 5306)

Can projected rent from a new ADU under construction be used to qualify?

No. Freddie Mac states that projected rental income from an ADU undergoing construction or renovation cannot be used for qualifying purposes. (Guide FAQ FA1520)

Can I use ADU rent on a cash-out refinance?

No. ADU rental income qualification is available only for purchase and no-cash-out refinance transactions.

Does the ADU need a bedroom?

No. Freddie Mac explicitly states efficiency/studio ADUs qualify without a dedicated bedroom. (Guide FAQ FA1508)

Does the ADU need a separate entrance?

Yes. A separate entrance independent from the primary dwelling is non-negotiable in Freddie Mac's ADU definition. (Guide FAQ FA1505)

If I live in the ADU and rent the main house, can I use that rent to qualify?

The property can still be treated as a primary residence. However, rent from the main dwelling cannot be used to qualify the mortgage in that scenario. (Guide FAQ FA1519; Section 5306.1)

What if the ADU is in the basement?

A basement qualifies as an ADU only if it has a separate entrance, kitchen, and bathroom and functions independently from the main living area. A finished basement with unrestricted access to the main home does not meet the definition.

What if the ADU is illegal or unpermitted?

On 1-unit properties, an illegal-zoning ADU may still be eligible under specific conditions (Guide Section 5601.2(c)). On 2- or 3-unit properties, the ADU must be legally zoned. Rental income from an illegal ADU can never be used for qualification.

Can Freddie Mac finance a 4-unit property with an ADU?

No. Section 5601.2 allows one ADU on 1-, 2-, and 3-unit properties only.

What is CHOICERenovation and does it work for ADUs?

CHOICERenovation is Freddie Mac's renovation loan. It can finance ADU construction, conversion, or post-build refinancing. But remember: projected rent from the ADU being built cannot be used to qualify for the CHOICERenovation loan itself.

Can a manufactured home be an ADU under Freddie Mac?

Yes. As of February 2026 (Bulletin 2025-15), manufactured home ADUs are allowed when the primary dwelling is a multiwide manufactured home. The manufactured ADU must meet minimum 400 sq ft and standard HUD requirements.

Does Freddie Mac require landlord education?

Yes, for purchase transactions using ADU rental income to qualify. At least one qualifying borrower must complete a course unless they have 1+ year of property management experience. The course cannot be provided by an interested party, the originating lender, or the seller. MI providers like MGIC and Arch offer acceptable courses. (Guide Chapter 5306)

Editorial Methodology and Source Log

Last verified: April 4, 2026

Primary sources

- Freddie Mac Single-Family Seller/Servicer Guide, Section 5601.2

- Freddie Mac Single-Family Seller/Servicer Guide, Chapter 5306 (Rental Income)

- Freddie Mac ADU Fact Sheet, February 2026

- Freddie Mac ADU Appraisal Report Checklist, November 2025

- Freddie Mac Guide Bulletins 2022-11, 2025-15, 2026-1

- Freddie Mac Guide FAQs: FA1505, FA1507, FA1508, FA1519, FA1520

Comparison sources

- Fannie Mae Selling Guide Supplement: UAD 3.6 Policy (December 2025, effective March 31, 2026)

- Fannie Mae Selling Guide B3-3.8-01, Rental Income (October 2025)

- HUD Mortgagee Letter 2023-17 (FHA ADU rental income and property eligibility policies)

The Dwelling Index is an independent educational resource. We are not a lender, broker, or real estate agent. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our editorial recommendations are based on independent research and are never influenced by compensation.

All financial scenarios presented on this page are illustrative examples only and are not guarantees of qualification, approval, or specific loan outcomes. Actual results depend on current interest rates, your complete financial profile, the specific property, and your lender’s underwriting requirements. Consult a licensed loan officer for your specific situation.

Corrections: If you spot an error or an outdated rule on this page, email us at corrections@dwellingindex.com.

Free 2026 ADU Starter Kit

New to ADUs? Start with the free guide.

Our 2026 ADU Starter Kit covers financing paths, cost ranges, and a checklist for your first lender conversation — all in one place.

Get the Free 2026 ADU Starter Kit