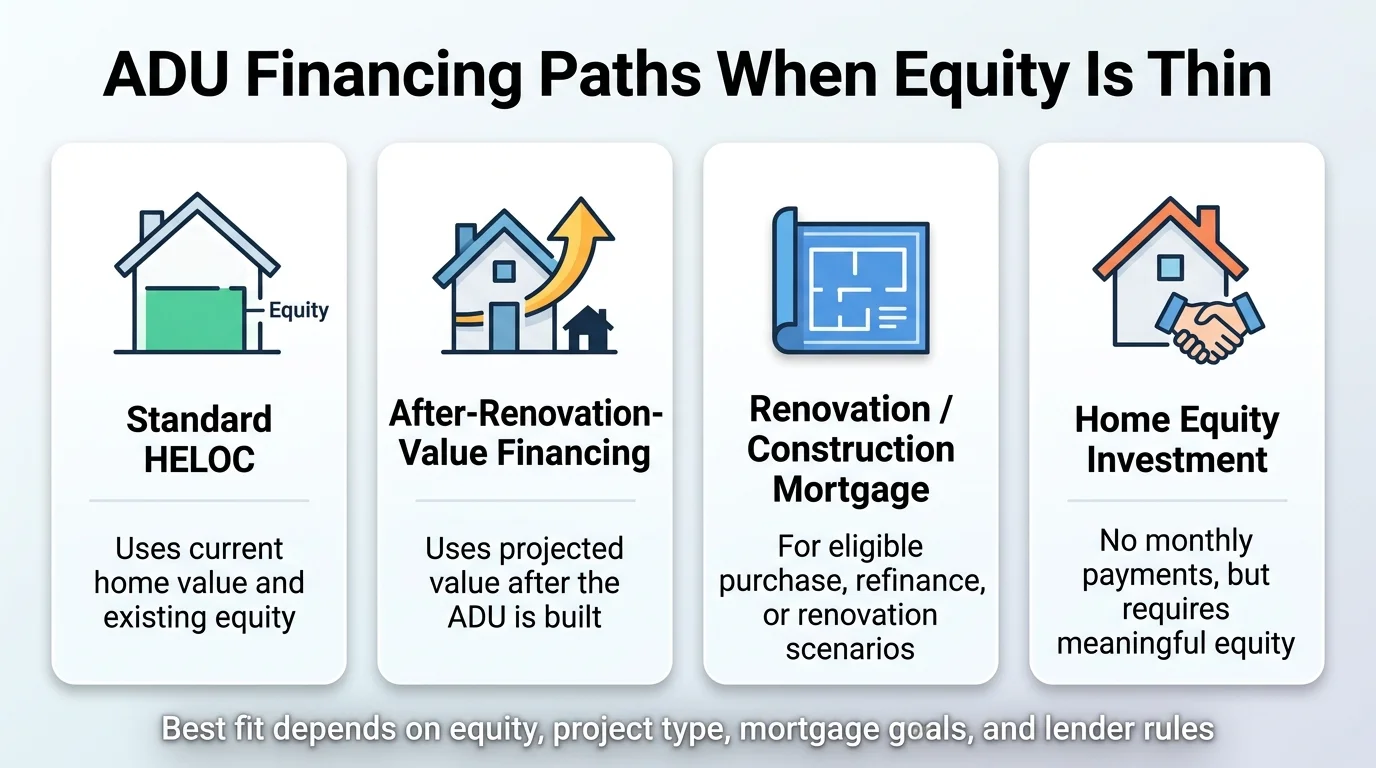

At a Glance: ADU Financing Paths When Equity Is Thin

Before we go deep, here's the landscape. Find your row, then read the section that matches.

| Financing Path | Best For | Low-Equity OK? | Monthly Payments? |

|---|---|---|---|

| Renovation HELOC (ARV-based) | Recent buyers, low equity, keep first mortgage | Yes | Yes (interest-only during draw) |

| Fannie Mae HomeStyle Renovation | Low equity, willing to refinance | Yes | Yes (mortgage) |

| Freddie Mac CHOICERenovation | Low equity, willing to refinance | Yes | Yes (mortgage) |

| FHA 203(k) | Lower credit, attached conversions or existing ADU rehab | Yes | Yes (mortgage) |

| Construction-to-Permanent | Ground-up builds with defined scope | Sometimes | Yes (mortgage) |

| Home Equity Investment (HEI) | Equity-rich but cash-poor, fixed income | No | No monthly payments |

| Standard HELOC / Home Equity Loan | High existing equity | No | Yes |

Table sorted by equity requirement (lowest first), not by any commercial relationship. FHA 203(k) note: for adding a brand-new ADU, HUD requires the unit be attached to the existing structure. However, FHA's 2023 ADU guidance (FHA INFO 2023-81) also allows rehabilitation of an existing ADU that is attached or unattached. Confirm eligibility with your lender. Affiliate disclosure applies.

That's the map. Now let's walk through each path in detail.

Starting with why the most common option fails when equity is thin — then covering each alternative in the order most homeowners should evaluate them.

Can You Finance an ADU With No Equity?

Yes — but not with the product most people try first.

If “no equity” means you don't have enough tappable equity for a standard HELOC, multiple financing paths still exist. The strongest options for low-equity homeowners use future-value underwriting: they lend based on what your property will be worth after the ADU is built, not just what it's worth today.

If you have substantial equity but don't want monthly payments, that's a different lane — and we cover that separately below.

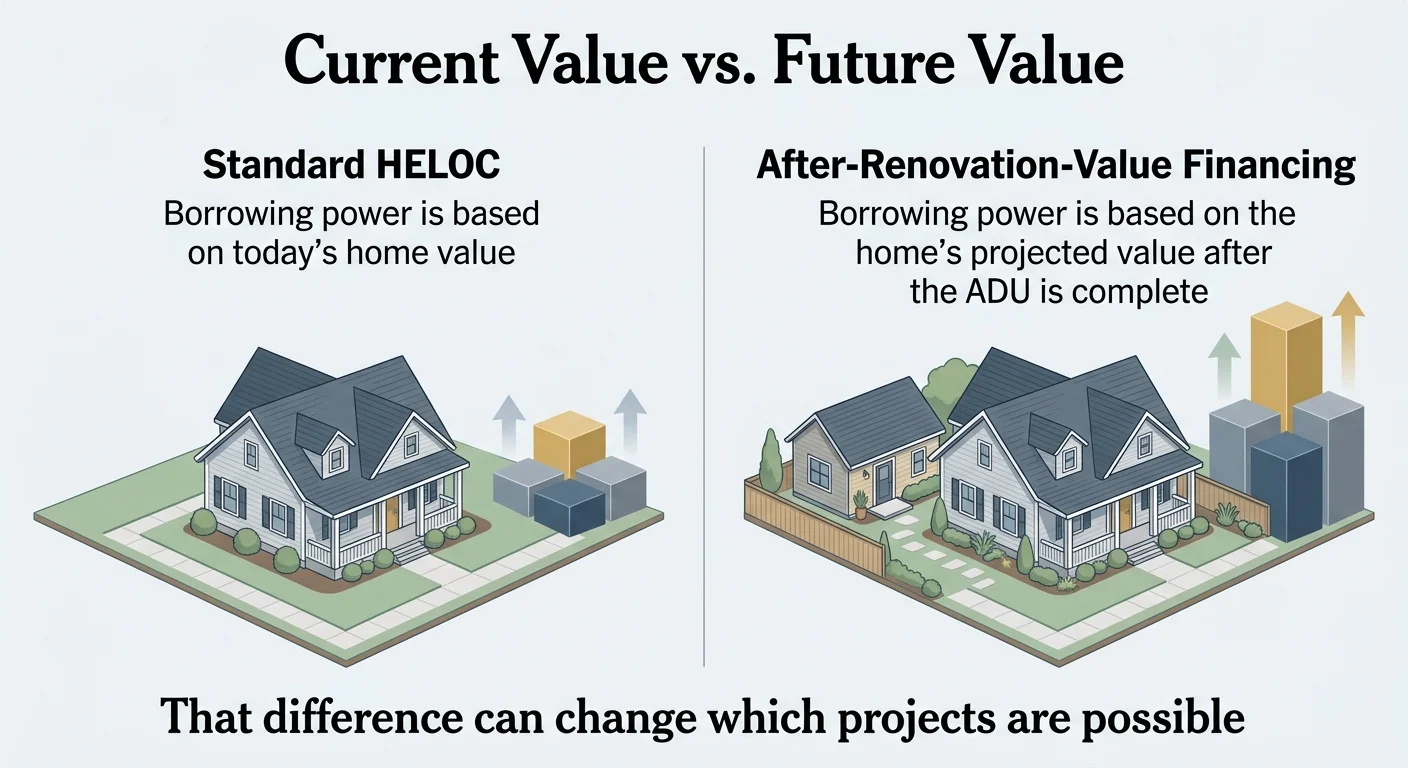

Why a Standard HELOC Usually Fails When You Have Little Equity

Most ADU financing advice starts with “get a HELOC.” And for homeowners sitting on 20+ years of equity, that's fine. But if you bought your home in the last five years — or anytime prices were near peak — a standard HELOC is almost certainly not going to fund a six-figure ADU project.

Standard HELOCs and home equity loans are capped by your home's current value, typically at 80–85% combined loan-to-value (CLTV). The bank adds your existing mortgage balance plus any new borrowing, and the total can't exceed that ceiling. For a recent buyer, the math kills you fast.

The same home, the same day — but a completely different borrowing limit depending on which value the lender uses.

The Borrowing Power Gap: A Real Example

Say you bought your home in 2022 for $450,000 and currently owe $400,000. Your home is now worth about $475,000. You want to build a detached 600 SF ADU.

Standard HELOC (80% of current value)

80% × $475,000 = $380,000 max total debt

You already owe $400,000

$380,000 − $400,000 =

$0 available

The bank literally cannot lend you anything

Renovation HELOC (after-renovation value)

Post-ADU value (as-completed): $625,000

90% × $625,000 = $562,500

Minus existing mortgage: $562,500 − $400,000 =

$162,500 available

Same homeowner. Same house. Same day.

Illustrative examples, not guarantees of approval. Actual borrowing power depends on your credit profile, income, property location, lender requirements, and appraised after-renovation value. Maximum LTV varies by lender.

Same homeowner. Same house. Same day.

The difference is which number the lender uses: today's value or tomorrow's. That gap — and the fact that most homeowners don't know a product exists to close it — is why this page exists.

When a HELOC Still Works

If your equity math puts you at $100K+ available, a standard HELOC is the simplest and fastest path. No contractor documentation required upfront, no as-completed appraisal. If you have the equity, don't overcomplicate this.

For more on standard HELOC options for ADUs, see our HELOC for ADU guide or the full ADU Financing Options Guide.

The Best Low-Equity Path for Most Homeowners: After-Renovation-Value Financing

An after-renovation-value (ARV) product — sometimes called a renovation HELOC — does something standard equity products don't: it underwrites your loan based on what your home will be worth after the ADU is built, not what it's worth today. The result? Dramatically more borrowing room, even if you closed on your home last year.

How It Works in Practice

Submit your ADU project details

Plans, contractor information, a budget estimate, and your property information.

Lender orders an as-completed appraisal

An appraiser reviews your ADU plans and estimates what the property will be worth once construction is done.

Borrowing power calculated against future value

Limits vary by lender and product, but can be significantly higher than standard equity products.

Structured as a second lien

Your current first mortgage stays in place. You keep your existing rate — which matters enormously if you locked in between 2020 and early 2023.

Who this fits best

- Homeowners who bought in the last one to five years and haven't built up significant equity

- Homeowners with a low-rate first mortgage they don't want to touch

- Anyone whose standard HELOC borrowing math comes up short for their ADU budget

- Homeowners building either attached or detached ADUs (both eligible)

Who it does not fit

- Homeowners who can't provide contractor bids and basic project documentation

- Properties where the ADU won't meaningfully increase appraised value

- Homeowners in states where renovation HELOC products aren't currently available

The honest tradeoff

Renovation HELOCs are more complex than walking into your bank and asking for a credit line. You'll need contractor documentation, a project budget, and an as-completed appraisal — which adds time and cost beyond a standard HELOC.

The reality: For homeowners who bought recently and haven't built up equity, this additional process is often the only path to borrowing what they actually need. The extra paperwork is a one-time hurdle for a financing advantage that can unlock six figures in borrowing power that simply doesn't exist through any other product.

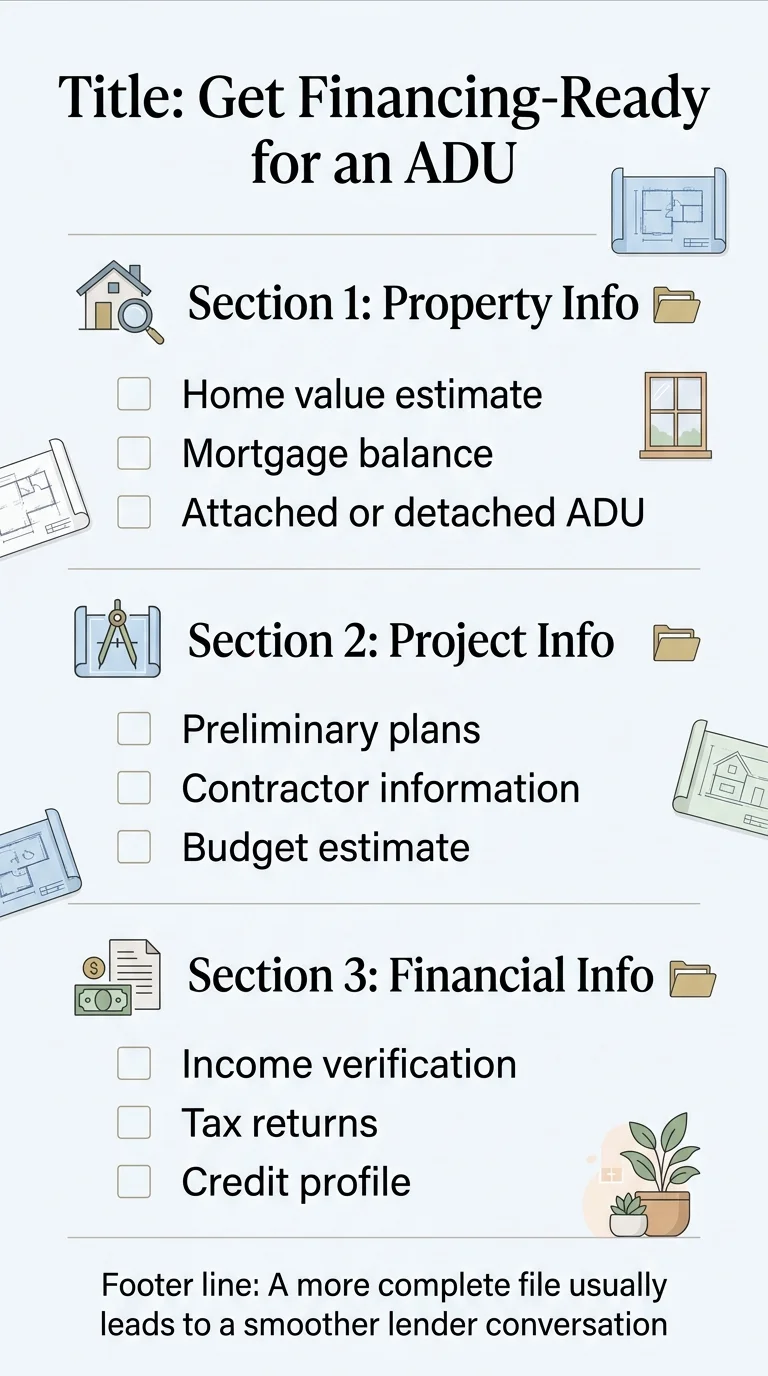

What You'll Need Ready Before Applying

Contractor name, license number, and contact information

Preliminary project budget or cost estimate

ADU plans or architectural drawings (even preliminary ones)

Basic property information (lot size, existing structures, zoning confirmation)

Income verification and tax returns

Credit authorization

About RenoFi

RenoFi, the most prominent renovation HELOC broker, partners with credit unions to offer ARV-based products. They are not themselves a lender — they match homeowners with participating lenders in their area. It's free to work with RenoFi, and there's no obligation to move forward. renofi.com Confirm current state availability directly with RenoFi before applying.

Does this sound like your situation?

If you bought recently and want to keep your current mortgage rate, this lane was built for you.

See whether an after-renovation-value path fits your project.

Explore Renovation HELOC OptionsNo Monthly Payments Sounds Perfect — But These Are Not True No-Equity Options

Home equity investments (HEIs) from companies like Hometap, Unlock, and Point have gotten a lot of attention — and for good reason. The pitch is compelling: receive a lump sum of cash in exchange for a share of your home's future appreciation. No interest. No monthly payments. Settle when you sell, refinance, or reach the end of your term.

But here's what most articles won't tell you:

HEIs require meaningful existing equity. They are equity-access products, not zero-equity products. If you just bought your house and owe 80–95% of its value, an HEI won't work for you.

Requires at least 25% equity. Available in 16 states. Terms up to 10 years.

Source: hometap.com. Verified April 2026. Confirm current state availability before applying.

Requires approximately 30% equity with minimum property value of $175,000. Available in select states. No income requirements.

Source: unlock.com — How It Works. Verified April 2026. Confirm current state availability before applying.

Requires sufficient equity. Accepts credit scores from 500+. Terms up to 30 years in select regions.

Source: Point Help Center — State Availability. Verified April 2026. Confirm current state availability before applying.

Who HEIs Actually Fit

Retirees or fixed-income homeowners

Substantial equity but can't absorb another monthly payment. An aging-parent ADU funded by an HEI lets them house family without straining fixed cash flow.

Homeowners with high equity but a high debt-to-income ratio

Maybe they qualify on paper but adding a HELOC payment would be financially uncomfortable.

Anyone who has the equity and genuinely prefers sharing future appreciation over paying interest

Some people simply don't want more debt, even if they could qualify. For the right situation, the premium is worth it.

The Tradeoff You Need to Understand

When your home appreciates — and ADUs are specifically designed to increase value — you share that upside with the HEI company. If your home gains significantly in value over the term, you're giving up a meaningful chunk of that gain.

At the end of the term, you must settle. That typically means selling the home, refinancing to buy out the investor's share, or paying from savings or another source. Hometap does share in downside risk — if your home loses value, you may owe less than the original investment amount. But the upside-sharing cost over a decade of appreciation can exceed what you'd pay in interest on a traditional loan. Run the numbers both ways before committing.

Hometap vs. Unlock vs. Point: Quick Comparison

| Feature | Hometap | Unlock | Point |

|---|---|---|---|

| Min. Equity | ~25% | ~30% | Sufficient equity required |

| Max. Investment | Up to $600K | Up to $500K | Up to $500K–$600K |

| Term | 10 years | 10 years | Up to 30 years |

| Min. Credit Score | 500–600+ | 500+ | 500+ |

| Monthly Payments | None | None | None |

| State Availability | 16 states (check list) | Select states (check list) | Select regions (check list) |

HEI companies have limited state availability. Verify directly with each company before applying. HEIs are investments, not loans — you share future appreciation in exchange for no monthly payments or interest. Affiliate disclosure applies.

The bottom line on HEIs

If you have meaningful equity and genuinely cannot or do not want to take on monthly debt, HEIs deserve a serious look — especially for aging-parent ADUs or fixed-income situations. If you're a recent buyer with minimal equity, skip this lane entirely and look at the renovation HELOC or agency renovation loan sections.

If you're equity-rich but cash-flow-sensitive

This lane was designed for homeowners in your exact position.

Check HEI availability in your state before investing time in an application.

Agency Renovation and Construction Loans That Work With Little Current Equity

Beyond renovation HELOCs and HEIs, government-backed programs are specifically designed to finance home improvements — including ADUs — based on future value. These carry more complexity than a second-lien product, but they can be powerful for the right borrower.

Fannie Mae HomeStyle Renovation

Fannie Mae's HomeStyle Renovation loan allows homeowners to finance adding an ADU to an existing property, using the as-completed value for underwriting. It can also be used with Fannie Mae's Construction-to-Permanent product for new builds that include an ADU. HomeStyle has been explicitly updated to support standalone detached ADU construction.

- Lends based on the property's future value after the ADU is built

- Can finance attached or detached ADUs

- Available nationally through participating lenders

- Requires contractor bids, architectural plans, and a draw schedule

- Funds are disbursed in phases as construction progresses

Freddie Mac CHOICERenovation

Freddie Mac's CHOICERenovation loan is the parallel product. It can finance adding a new ADU or renovating an existing structure into one, with future-value underwriting.

- Also lends against as-completed value

- Supports both attached and detached ADUs

- Available nationally through participating lenders

- Similar documentation and draw-schedule requirements as HomeStyle

Source: Freddie Mac Single-Family Seller/Servicer Guide — ADU provisions

FHA 203(k) — Mainly Attached, With One Important Exception

HUD's current guidance draws a clear line: if you're adding a brand-new ADU under the Standard 203(k) program, the unit must be attached to the existing structure. That makes 203(k) a strong fit for garage conversions, basement conversions, attic conversions, and additions built onto the existing home.

The exception (FHA INFO 2023-81)

FHA's 2023 ADU policy update also allows rehabilitation of an existing ADU — whether attached or unattached. So if your property already has an unpermitted or deteriorated detached structure you want to convert into a legal ADU, 203(k) may be on the table.

Sources: HUD 203(k) program guidance and FHA INFO 2023-81 . Confirm current ADU eligibility and requirements with your lender.

When Agency Loans Beat a Renovation HELOC — and When They Don't

When they make sense

- You're willing to refinance your first mortgage (or your current rate is high enough that refinancing doesn't hurt)

- You want a single consolidated payment instead of first mortgage plus a second lien

- You need to borrow more than a renovation HELOC allows

- You're buying a property and building the ADU as part of the purchase

When they don't

- You have a mortgage rate locked in well below current market rates and replacing it would significantly increase your monthly payment

- You want a simpler process — agency renovation loans involve draw schedules, inspections, and contractor oversight

- Your project timeline is flexible and you'd prefer the speed of a second-lien product

Agency Renovation Loan Comparison

| Feature | HomeStyle | CHOICERenovation | FHA 203(k) |

|---|---|---|---|

| New Detached ADU? | Yes | Yes | No — must be attached |

| Rehab Existing Detached ADU? | Yes | Yes | Yes (per FHA INFO 2023-81) |

| Future-Value Underwriting? | Yes | Yes | Yes |

| Keep Current Mortgage? | No — replaces it | No — replaces it | No — replaces it |

| Draw Schedule? | Yes | Yes | Yes |

| Availability | National (participating lenders) | National (participating lenders) | National (FHA-approved lenders) |

Max LTV, minimum credit scores, and other requirements vary by transaction type, occupancy, and lender overlay. Confirm current program rules directly with your lender before applying.

Looking at a renovation or construction loan?

If a renovation HELOC doesn't fit your state or situation, these agency-backed paths are worth exploring. A lending comparison marketplace can show you what's currently available in your area.

Compare Renovation Loan OptionsWill ADU Rental Income Help You Qualify?

This comes up constantly: “If I'm going to rent the ADU for $2,000 a month, can that income help me qualify for the loan?”

The short answer: sometimes, but don't count on it to save an otherwise thin application.

Fannie Mae

Updated its selling guide to allow ADU rental income toward qualifying on one-unit principal residences in limited purchase and limited cash-out refinance scenarios. Requires market rent support (comparable rental data or appraisal rent schedule).

Source: Fannie Mae Selling Guide — ADU rental income provisionsFreddie Mac

Similarly allows ADU rental income to be considered if specific documentation requirements are met.

Source: Freddie Mac Seller/Servicer Guide

FHA

Allows ADU rental income in some cases but specifically CANNOT be used to qualify for a cash-out refinance on a one-unit property with an ADU.

Source: FHA INFO 2023-81What This Means in Practice

Don't build your financing plan around projected rental income saving your qualification. Treat it as a potential boost, not the foundation. If you need the rent to qualify, make sure you:

Have conservative market rent data for your area and ADU type

Provide it upfront to your lender with your application

Ask your loan officer specifically whether their underwriting will count it — not all lenders apply this uniformly even when the agency guidelines allow it

Why the As-Completed Appraisal Is the Most Important Step

Every future-value financing path — renovation HELOCs, HomeStyle, CHOICERenovation, 203(k) — depends on one number: the appraised value of your home after the ADU is built. That appraisal is the single biggest lever determining how much you can borrow.

What Drives a Strong Appraisal

Your local market matters most

ADU value-add varies widely by region. In markets with strong rental demand, a well-built ADU can significantly increase your property's appraised value. In softer markets, the boost may be more modest.

ADU type and quality matter

A fully finished 600+ SF detached ADU with its own kitchen, bath, and entrance typically adds more value than a basic garage conversion.

Comparable sales with ADUs help

If homes with ADUs in your area have sold at a premium, your appraiser has data to support a higher value. If comps are scarce, the appraisal may be more conservative.

Managing appraisal risk

If you're concerned about the appraisal coming in low, ask a local appraiser for a preliminary value opinion before committing to the full application. It's a small investment that can save significant frustration — and it gives you a realistic picture of your borrowing power before you're deep in the process.

For detailed ADU cost breakdowns by type and region, see our Complete ADU Cost Guide.

Which Path Is Right for You?

By now you've got the full landscape. Here's the decision in its simplest form:

If you bought recently and have less than 20% equity — AND want to keep your current mortgage rate

Best path: Renovation HELOC (ARV-based)

Lends on your home's future value, keeps your first mortgage intact, and is designed specifically for equity-light homeowners.

If you bought recently and have less than 20% equity — AND are willing to refinance

Best path: Fannie Mae HomeStyle or Freddie Mac CHOICERenovation

Future-value underwriting with high LTV limits. More complex, but maximum borrowing power.

If your ADU is an attached conversion (garage, basement, attic) or rehab of an existing structure

Best path: FHA 203(k) is an additional option

Often with more flexible credit requirements. HomeStyle and CHOICERenovation also work.

If you have significant equity but can't take on monthly debt payments

Best path: Home equity investment (Hometap, Unlock, or Point)

A lump sum with no monthly payments — in exchange for sharing future appreciation. Verify state availability first.

If you have 20%+ equity and want the simplest, fastest process

Best path: Standard HELOC or home equity loan

Don't overcomplicate it.

If you don't yet have contractor bids, plans, or a clear project scope

Best path: You're not financing-ready — and that's completely normal

The right next step is confirming your property qualifies for an ADU, scoping the project, and getting the documentation lenders will need.

See what's possible at your address — it takes 60 seconds and it's free.

We check your lot's zoning, setbacks, and local ADU rules, then show you what you can realistically build. Currently available in CA, UT, TX, CO, and NY.

Get Your Free ADU ReportThree Real Scenarios: Finding the Right Lane

Numbers help. But seeing yourself in a scenario helps more. Here are three composite profiles based on the patterns we see most often.

The right financing path depends on your equity position, your current mortgage rate, and whether you can absorb a monthly payment.

The Recent Buyer Who Wants to Keep a Low Rate

Profile

Sarah bought her home in 2021 for $520,000 at a 3.1% mortgage rate. She now owes $480,000. The home is worth approximately $550,000. She wants to build a detached 500 SF ADU in the backyard for rental income.

Standard HELOC math

80% × $550,000 = $440,000. She owes $480,000. Result: $0 available. She cannot borrow a cent through a standard HELOC.

Alternative

The as-completed appraisal estimates post-ADU value at $680,000. Using future-value underwriting, Sarah may qualify for a meaningful amount — potentially enough to fund most of her ADU project — while keeping her 3.1% first mortgage intact.

Best path

Renovation HELOC. She preserves her low rate, and the ADU's rental income can help offset her new payment over time.

Main risk

The as-completed appraisal comes in lower than expected, reducing borrowing power. Mitigation: get a preliminary value estimate before committing to the full application.

The Retiree Who Can't Take on More Monthly Debt

Profile

Robert and Linda, both 68, own their home outright — it's worth $650,000 with no mortgage. Linda's mother needs to move in due to declining health. They want to build an attached 400 SF ADU. They live on Social Security and a small pension. Adding a monthly loan payment is not realistic.

Situation

They have substantial equity — far more than the minimum required for an HEI. They cannot absorb monthly payments.

Best path

Home equity investment. The ADU houses Linda's mother, potentially saving thousands per month compared to assisted living, and the appreciation-sharing cost is a reasonable trade for that quality of life.

Main risk

They need to be able to settle the investment at term end. With no mortgage debt and a valuable property, refinancing to buy out the HEI company's share is a realistic exit strategy.

The Garage Conversion With a Tight Budget

Profile

Marcus bought a house with an attached two-car garage for $380,000 three years ago. He owes $340,000. The home is worth about $400,000. He wants to convert half the garage into a studio ADU.

Standard HELOC math

80% × $400,000 = $320,000. He owes $340,000. Result: $0 available.

Alternative

Because this is an attached conversion, both renovation HELOC products and FHA 203(k) are on the table. The FHA path is worth checking because Marcus's credit score is in the low 600s — within FHA range. His current mortgage rate is already near current market rates, so refinancing doesn't significantly change his monthly payment.

Best path

Worth exploring an FHA-backed renovation path for the attached conversion, subject to current HUD rules and lender requirements.

Main risk

The draw-schedule process is more involved than a lump-sum product. For an attached garage conversion at a lower budget, the trade-off may be worth it.

All scenarios are illustrative composites. Actual results depend on individual circumstances, market conditions, lender requirements, and appraised values. These are not guarantees of approval or outcomes.

What About ADU Grants? The Truth About Free Money

We get this question weekly, so let's be direct.

CalHFA ADU Grant (California)

Funding exhaustedOffered up to $40,000 toward predevelopment costs. CalHFA's official site says the latest round of ADU Grant funding was fully allocated on December 28, 2023. Whether and when additional rounds will open is uncertain.

Confirm current status directly with CalHFASan Diego Housing Commission ADU Finance Program

Limited fundsCan offer up to $250,000 for eligible City of San Diego homeowners. SDHC's application portal indicated that funds were not available for FY2025 and only limited prior-year funds were being made available on a first-come, first-approved basis.

Confirm current availability with SDHCMunicipal programs

Varies by citySome municipalities offer reduced impact fees, expedited permitting, or below-market-rate loans for ADU construction. Worth checking at your city's planning or housing department.

Check your city's planning or housing department

How homeowners are actually paying for ADUs right now

Grant programs are real and helpful when available — but they're not something to build your entire financing plan around. Funding runs out. Waitlists grow. Even when available, most grants cover predevelopment costs (plans, permits, surveys), not the full construction bill. Homeowners are building ADUs every day without waiting for grant funding — using the renovation HELOC, agency renovation, and HEI paths detailed above.

What Lenders Will Ask For Before They Take You Seriously

One of the biggest hidden blockers: people apply too early. They reach out to a lender before having the basic project information that every serious financing path requires. Get these ready before your first call and you'll move faster than 90% of applicants.

Property Information

- Current home value (recent appraisal, Zillow estimate, or comparable sales analysis)

- Mortgage balance and current interest rate

- Lot size and existing structures

- Zoning confirmation that your property allows an ADU

- Whether your planned ADU is attached or detached

Project Documentation

- ADU type (detached new build, garage conversion, basement conversion, attached addition)

- Preliminary plans or architectural drawings

- Contractor name, license, and contact information

- Preliminary cost estimate or contractor bid

- Rough construction timeline

Financial Documents

- Two years of tax returns

- Recent pay stubs or income verification

- Bank statements

- Credit score (check free through most banks or Credit Karma)

- Current debt obligations

Why attached vs. detached matters

This detail catches homeowners off guard. For new ADU construction, FHA 203(k) requires the unit be attached to the existing structure. Rehabilitation of an existing detached ADU may be eligible. HomeStyle, CHOICERenovation, and renovation HELOCs all work for both attached and detached. Know your ADU type before you apply.

Download the Free 2026 ADU Starter Kit

Financing checklists, state-by-state permit guides, cost calculators, and lender comparison worksheets — delivered instantly.

Get the Free Starter KitHonest Tradeoffs, Real Risks, and When to Wait

Every financing path has downsides. Here's what no one's affiliate page will tell you — and why you should know it before you apply.

Renovation HELOCs Are Powerful but Underused for a Reason

The Terner Center for Housing Innovation at UC Berkeley specifically flags this: renovation loans are well-suited for homeowners without significant equity, but they remain relatively underused. Why? Because the process is more complex than a standard HELOC. You need contractor documentation before you apply. The as-completed appraisal adds time and cost. None of that means you shouldn't use them. It means go in with eyes open and documents ready. The homeowners who have the smoothest experience treat the application like a construction project: organized, documented, and patient with a process that's more involved than a credit card application.

Source: Terner Center for Housing Innovation at UC Berkeley — ADU research.

HEIs Can Be Expensive When Your Home Appreciates

Home equity investments have no interest and no monthly payments — which feels free. It's not. You're sharing future appreciation, and if your property value rises significantly (which an ADU is specifically designed to cause), the settlement amount can exceed what you'd pay in cumulative interest on a traditional loan. Run the numbers before committing. For some homeowners, the HEI still wins because the no-payment flexibility is worth the premium. Compare both scenarios for your situation.

When You Should Wait Instead of Applying

Not every homeowner is financing-ready, and applying prematurely can hurt more than it helps. Here are the signals to pause:

You don't have a contractor or even preliminary bids

Every serious low-equity financing path requires project documentation. Without a defined scope and budget, you're asking a lender to underwrite a hypothetical.

You haven't confirmed your property even qualifies for an ADU

Zoning restrictions, setback requirements, lot size minimums, owner-occupancy rules, utility capacity, and HOA covenants can all prevent you from building. Discover these before you pay for an appraisal.

Your credit or income profile needs work

If your credit score or debt-to-income ratio is stretched, spending three to six months improving your position before applying can give you better terms and a higher approval probability.

You're planning to sell within two to three years

ADUs are a long-game investment. The construction timeline, permit process, and lease-up period mean you may not fully recoup your investment on a quick sale. If a move is on the horizon, run the exit math carefully.

If any of these apply, the right move isn't “find a different loan.” It's “build the foundation first”: confirm feasibility, scope the project, strengthen your financial position, then apply from a position of readiness.

Common Mistakes That Send Homeowners Back to Search

We've seen these patterns repeatedly. Each one wastes weeks and costs emotional energy. Avoid them.

Assuming 'no monthly payment' means 'no equity required'

HEIs solve the monthly-payment problem, not the equity problem. They require meaningful existing equity. If you have little equity, the renovation HELOC or agency renovation path is where you need to look.

Applying before getting contractor-ready numbers

Renovation HELOCs, HomeStyle loans, and construction loans all require contractor information and a project budget. Walking into a lender with 'I want to build an ADU, how much can I borrow?' gets you a conditional answer at best and a wasted credit pull at worst. Get a contractor bid first.

Assuming detached and attached ADUs finance the same way

They don't. New ADU construction under FHA 203(k) must be attached. Some lenders have additional restrictions on detached structures. Confirm your ADU type with your lender before applying.

Thinking rental income will save a weak application

Fannie Mae and Freddie Mac allow ADU rental income toward qualification in specific scenarios, but it's not a universal override. Treat it as a potential boost, not a lifeline.

Ignoring state coverage before clicking an HEI button

Hometap, Unlock, and Point are not available in all states. Check availability first — every company lists their service area on their website.

Using high-cost unsecured debt when renovation financing exists

Personal loans and credit cards carry significantly higher interest costs than secured renovation products. These should be last resorts — not Plan A — when dedicated renovation financing products exist specifically for this situation.

Financing before confirming your property even qualifies

Zoning rules, setback requirements, lot size minimums, owner-occupancy rules, and utility capacity can all determine whether you can build an ADU at your specific address. Confirm feasibility before you spend money on plans or applications.

Not sure if your property qualifies? That's the first thing to check.

We verify zoning, setbacks, lot coverage, and local ADU rules for your specific address — in about 60 seconds.

See What's Possible at Your AddressOnce You're Approved: What Happens Next

Financing is the wall. Once you clear it, the rest is a construction project — and it helps to know what's ahead.

With a renovation HELOC

Funding mechanics vary by provider. RenoFi's public FAQ says its renovation HELOC products do not use typical construction draws — the full approved amount is made available, with completion confirmation after the project is done. Other products may work differently. Confirm disbursement and repayment terms directly with your lender.

With an agency renovation loan

Funds are disbursed through a draw schedule. Your lender and an inspector verify construction progress at predetermined milestones before releasing the next tranche. This protects you and the lender, but your contractor needs to be comfortable with the process.

With an HEI

You receive a lump sum. No draw schedule, no inspections, no lender oversight on how you spend it. Simpler, but you're managing the budget and contractor accountability yourself.

Regardless of financing path, your next steps are:

Finalize your ADU plans with a designer or architect if you haven't already

Pull permits — timeline varies widely by city, from a few weeks to several months

Begin construction with your licensed contractor

Complete inspections as required by your municipality

Get your certificate of occupancy

If renting: list the unit, screen tenants, and start generating income

For homeowners considering prefab or modular ADUs, see our Prefab ADU Company Comparison. For rental planning, see our ADU Rental Income Guide.

How We Researched This Page

This page was built from official program materials (Fannie Mae, Freddie Mac, HUD/FHA), partner product documentation (RenoFi, Hometap, Unlock, Point), academic research (Terner Center for Housing Innovation at UC Berkeley), and real homeowner language from forums and search data.

Every product detail, program rule, and state-availability claim was verified against official public materials. Grant program statuses were verified against administering agency publications.

We do not quote specific interest rates, APRs, or monthly payments because these change constantly and vary by borrower profile. We do not guarantee approval, qualification, or specific financial outcomes. This page is educational — not financial advice. Consult with a qualified mortgage professional or financial advisor for guidance specific to your situation.

Frequently Asked Questions

Can I finance an ADU if I just bought my house?

Yes. Renovation HELOCs and agency renovation loans (HomeStyle, CHOICERenovation) lend against your home's future value, not just current equity. These products are designed for recent buyers who haven't built up significant equity. You will need a defined project scope, contractor information, and standard financial documentation.

Can you build an ADU with no equity at all?

In most cases, 'no equity' really means 'not enough tappable equity for a standard HELOC.' If that's you, future-value renovation products are worth checking — they underwrite against your home's post-ADU value. If you have zero equity and no income or credit profile that supports borrowing, the right step may be a smaller-scope project or building equity before applying.

What is an after-renovation-value (ARV) loan?

An ARV loan uses an as-completed appraisal to determine borrowing power based on what your home will be worth after your ADU is built. This can significantly increase the amount you can borrow compared to products that only consider current value.

Do home equity investments require equity?

Yes. HEIs from Hometap, Unlock, and Point require meaningful existing equity — typically 25–30% or more. They are equity-access products, not zero-equity solutions.

Is RenoFi a lender?

No. RenoFi is a mortgage broker that partners with credit unions to offer renovation-underwritten loan products. It is free to work with RenoFi and there is no obligation to proceed.

Can FHA 203(k) be used for a detached ADU?

For new ADU construction, HUD requires the unit be attached to the existing structure. However, FHA's 2023 ADU policy also allows rehabilitation of an existing ADU that is attached or unattached. Confirm eligibility with your FHA-approved lender.

Will lenders count future ADU rental income toward my qualification?

Sometimes. Fannie Mae and Freddie Mac have updated guidelines to allow ADU rental income in specific purchase and refinance scenarios. FHA allows it in some cases but not for cash-out refinances. Not all lenders apply this uniformly — ask your loan officer specifically.

Can I keep my current mortgage and still finance an ADU?

Yes, if you use a second-lien product like a renovation HELOC, standard HELOC, home equity loan, or home equity investment. Agency renovation loans (HomeStyle, CHOICERenovation, 203(k)) replace your first mortgage.

What if I have low equity and low income?

This is the hardest situation. If you can't support monthly payments on borrowed funds and don't have equity for an HEI, consider: a smaller-scope project (garage conversion vs. detached new build) to reduce the financing needed, building equity for one to two years through mortgage payments and market appreciation, or checking whether your municipality offers subsidized ADU financing programs.

Is a personal loan a good way to finance an ADU?

For most full-scope ADU projects, no. Personal loans are unsecured, carry higher interest costs, shorter terms, and lower maximums than secured renovation products. They can work as a bridge for soft costs (architectural drawings, permit fees), but they should not be the primary financing for a major construction project.

What if my state is not served by Hometap, Unlock, or Point?

Look at renovation HELOC products (available in most states), Fannie Mae HomeStyle (available nationally through participating lenders), or a lending comparison marketplace to see what is available in your area.

More from The Dwelling Index

ADU Financing Options Guide

Compare all financing paths — HELOC, construction loans, HEIs — by your equity and goals.

HELOC for ADU

When a standard HELOC works well and when it doesn't — with math.

How Much Does an ADU Cost?

Full cost breakdown by type, size, and region.

Best Prefab ADU Companies

Compared by price, quality, timeline, and delivery area.

ADU for Aging Parents

Best setups, real costs vs. assisted living, and financing for families.

ADU for Home Office

Full ADU or simpler backyard office? Costs, permits, and best small plans.

See what's possible at your address

Free ADU report covers zoning, lot fit, estimated costs, and next steps — personalized to your property. Takes 60 seconds.

Get Your Free ADU ReportGet the Free 2026 ADU Starter Kit

Financing checklists, state-by-state permit guides, cost calculators, and lender comparison worksheets — delivered instantly.

Download the Starter Kit© 2026 The Dwelling Index. All rights reserved. This content is for educational purposes only and does not constitute legal, tax, or financial advice. Consult qualified professionals for guidance specific to your situation. Product availability, rates, and program rules change frequently — verify all financing details directly with lenders before making decisions.