ADU Financing: How to Choose the Right Path in 2026

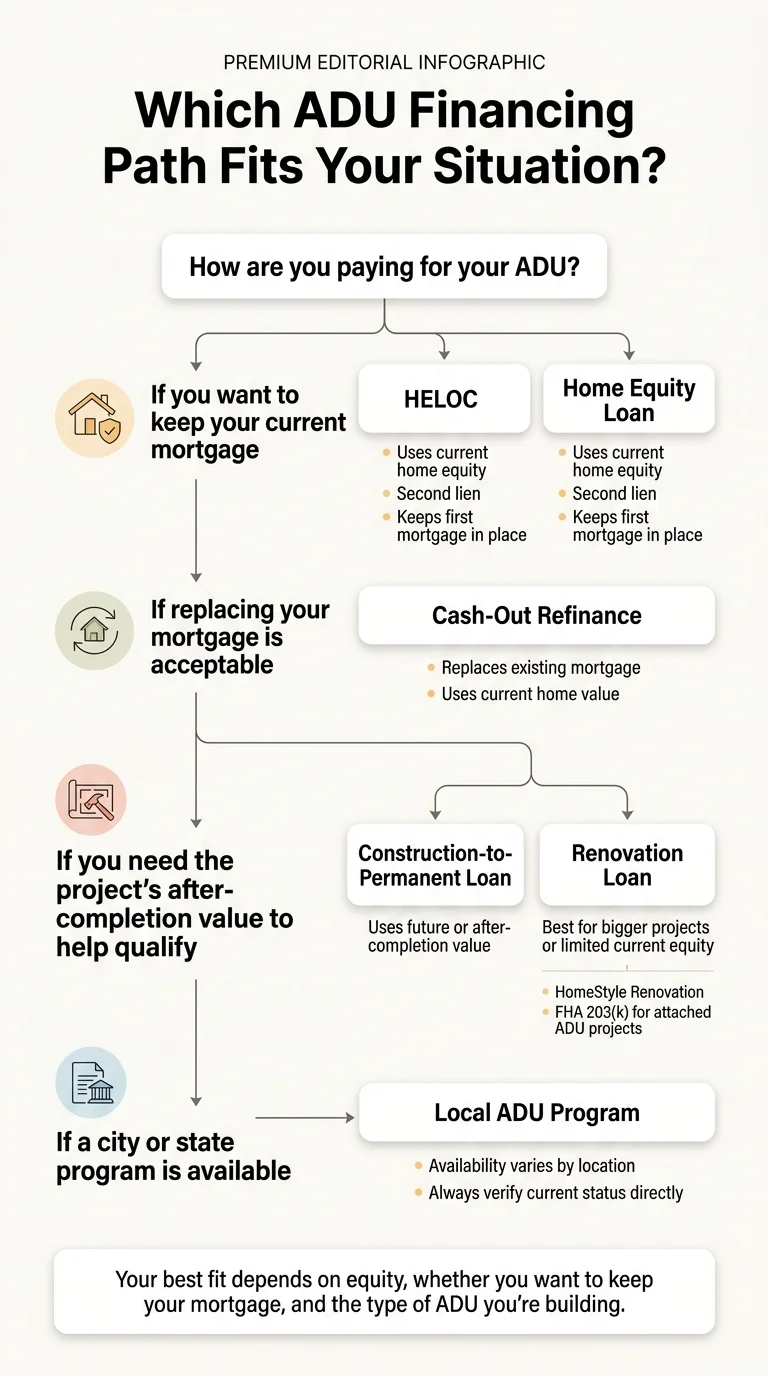

ADU financing usually comes down to one fork in the road: if you have enough equity and want to keep your current mortgage, start with a HELOC or home equity loan. If you don't have enough equity — or you need the lender to consider what your home will be worth after the ADU is built — look at construction or renovation financing instead.

That's the whole decision in two sentences. The rest of this page fills in the details: which path fits which situation, what the current Fannie Mae and Freddie Mac rules actually say, which government programs are live right now (and which ones aren't), and how to avoid the financing mistakes that cost homeowners the most.

There is no magic nationwide “ADU loan.” What exists are standard lending paths that work differently depending on your equity, your mortgage, and your ADU type. We built this guide to help you find the path that fits yours — not the one that earns a lender the highest commission.

Jump to what matters most

Fastest Way to Choose Your ADU Financing Path

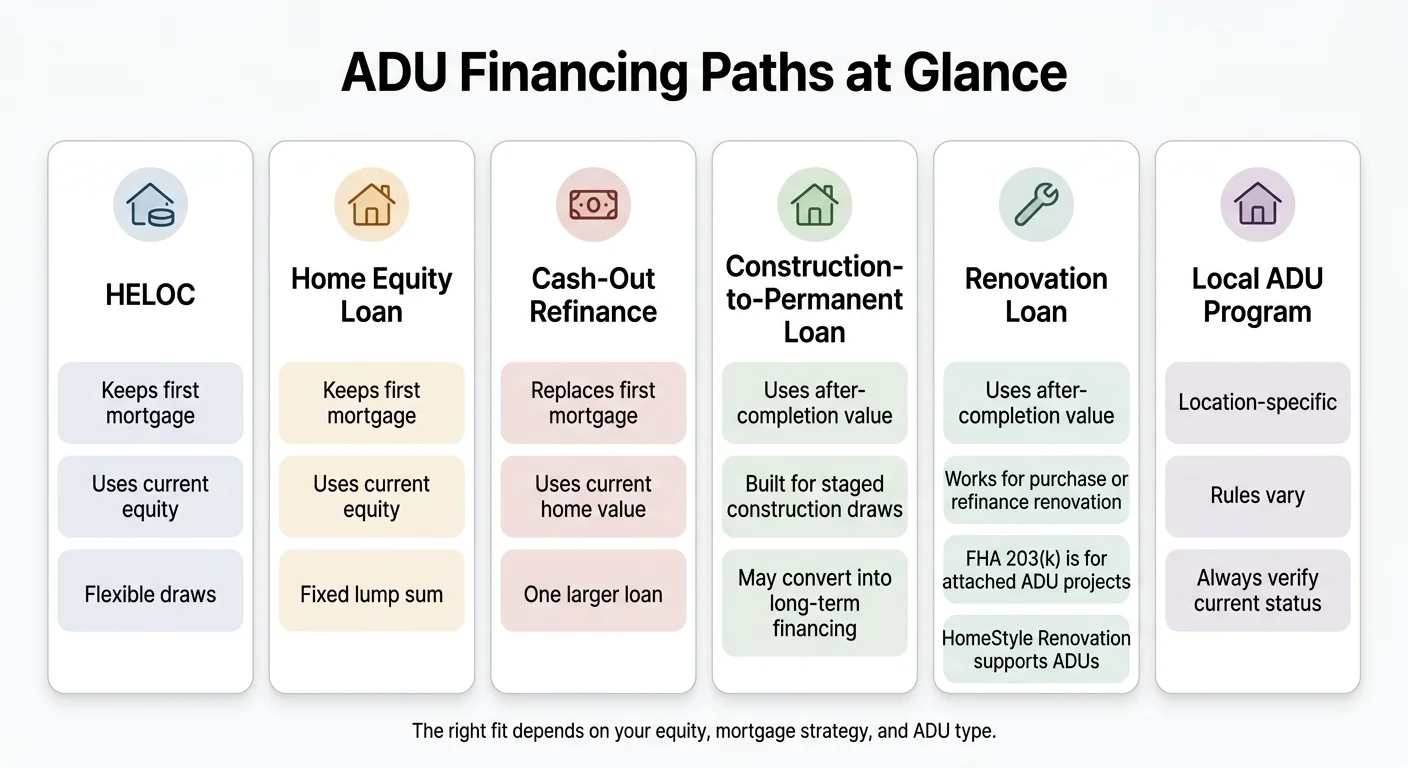

| Financing Path | Best When… | Keep Mortgage? | Based On | Main Watchout |

|---|---|---|---|---|

| HELOC | You have equity and want flexibility | ✅ Yes | Current home value | Variable rate can rise |

| Home Equity Loan | You want a fixed rate and predictable payments | ✅ Yes | Current home value | Lump sum — less flexible for phased builds |

| Cash-Out Refinance | Your current rate is already high | ❌ Replaces mortgage | Current home value | You lose your existing rate |

| Construction Loan | Low equity but strong income | Depends on type | Future (post-ADU) value | Complex draw process; may require later refinance or convert automatically |

| Renovation Loan (203(k) / HomeStyle) | You're buying a home or willing to refinance | ❌ Replaces mortgage | Future (post-ADU) value | Strict timelines and contractor requirements |

| Local Program / Grant | You're income-qualified in a participating area | Varies | Varies | Many are paused, waitlisted, or geographically limited |

Sources: Fannie Mae Selling Guide B2-3-04, Freddie Mac ADU Fact Sheet (Feb 2026), HUD 203(k) Program Comparison. Last verified March 31, 2026.

Looking for state-specific ADU financing rules?

Which ADU Financing Option Fits Your Situation?

Skip the textbook definitions for a minute. Here's how to think about this based on where you actually are financially.

If you have enough equity and want to keep your mortgage →

Start by comparing a HELOC and a home equity loan. Both sit on top of your existing mortgage as a second lien, which means you don’t touch your first mortgage rate. Terner Center research identifies second-lien loans — HELOCs and home equity loans — as the most common mortgage method among homeowners who have built ADUs. (Terner Center/Urban Institute, “ADU Construction Financing,” 2022)

If you don’t have enough equity →

You need a lender who will underwrite based on what your home will be worth after the ADU is built, not what it’s worth today. That’s a construction loan, a construction-to-permanent loan, or a renovation loan like FHA 203(k) or Fannie Mae HomeStyle. These products exist specifically for this gap.

If you’re converting a garage, basement, or existing space →

Conversions are typically the most affordable ADU type. Most equity-based products can handle the budget. Renovation loans also work well here.

If you’re building detached, prefab, modular, or manufactured →

Your ADU type matters for loan eligibility. A site-built detached ADU qualifies for nearly every financing path. A manufactured (HUD-code) ADU has specific requirements around permanent foundations and legal classification as real property.

If you need rental income to help you qualify →

Both Fannie Mae and Freddie Mac now allow ADU rental income to count toward your qualifying income under specific conditions. This is a meaningful policy shift — and most ADU financing guides haven’t caught up to it yet. Details in the rental income section →

If you’re counting on a grant or local program →

Some are real and currently funded. Many are paused, fully allocated, or more restrictive than they sound. See our verified program tracker →

If this sounds like your situation, start here:

| Your Situation | Start With | Why |

|---|---|---|

| Significant equity, want to keep your mortgage rate | HELOC or Home Equity Loan | Preserves your first mortgage; most common path when equity is available |

| Significant equity, current rate is already high | Cash-Out Refinance | Consolidates into one payment; may improve your overall rate |

| Low equity, strong income, ready to build | Construction or Construction-to-Perm Loan | Lender uses your home's future value to qualify you |

| Buying a new home and adding an ADU | FHA 203(k) or Fannie Mae HomeStyle | Finances purchase and ADU construction in one loan |

| Income-qualified in a participating city/state | Local ADU Financing Program | Can reduce costs; check current status first |

| Have cash or want no-debt options | Cash, Home Equity Investment (HEI), or documented family loan | Avoids interest cost, but carries opportunity cost or equity-sharing tradeoffs |

Free ADU Report

Not sure which path fits your property?

See what you can build at your address \u2014 zoning, feasibility, and the financing paths that match your lot.

What Are the Main ADU Financing Options?

Every path below uses the same format: who it fits, who it doesn't, how it works, biggest upside, biggest downside. No filler.

HELOC for an ADU

Best Fit

Homeowners with equity who want to keep their current mortgage and draw funds as construction progresses.

Bad Fit

Homeowners who bought recently and have minimal equity, or anyone uncomfortable with a variable interest rate.

How It Works

A HELOC is a revolving line of credit secured by your home equity. You're approved for a maximum amount but only draw — and pay interest on — what you need. Most HELOCs have a draw period followed by a repayment period. Lenders typically allow you to borrow up to 80–85% of your home's current appraised value minus your existing mortgage balance (exact limits vary by lender and credit profile).

Biggest Upside

Flexibility. You draw as construction progresses, and you don't pay interest on money sitting unused. Your first mortgage stays untouched.

Biggest Downside

Variable rate means your payment can increase. Borrowing power is limited to current value — if you don't have much equity, you may not be able to borrow enough.

Home Equity Loan for an ADU

Best Fit

Homeowners with significant equity who want a fixed rate and predictable monthly payments from day one.

Bad Fit

Anyone with limited equity, or who needs staged draws during construction.

How It Works

A fixed lump sum at a fixed rate, repaid over a set term. Like a HELOC, it sits on top of your first mortgage as a second lien.

Biggest Upside

Rate certainty. Your payment never changes. Your first mortgage stays intact.

Biggest Downside

You borrow the full amount upfront, even if construction hasn't started. Less flexible than a HELOC for phased builds.

Cash-Out Refinance for an ADU

Best Fit

Homeowners whose current mortgage rate is close to or higher than today's rates, or who owe very little and want to consolidate into one payment.

Bad Fit

Anyone sitting on a rate well below current market levels. Replacing that rate could cost more over the loan's life than the ADU itself.

How It Works

You refinance your entire first mortgage for a larger amount and take the difference as cash. Most cash-out refis allow borrowing up to 80% of current home value.

Biggest Upside

One loan, one payment. If your existing rate is already high, you might even improve it.

Biggest Downside

You're replacing your first mortgage. For homeowners who locked historically low rates, the math rarely works in their favor.

Construction Loan for an ADU

Best Fit

Homeowners who don't have enough equity for standard products but have strong income and creditworthiness. Also works for ground-up new builds that need staged draws.

Bad Fit

Anyone who wants simplicity. Construction loans require contractor bids, approved plans, a draw schedule, periodic inspections, and — depending on the product — conversion to permanent financing after construction.

How It Works

The lender appraises your home based on its projected value after the ADU is completed. You borrow against that future value. Funds are released in stages ('draws') as construction milestones are verified by an inspector. Construction-to-permanent loans convert automatically to a standard mortgage once the ADU is complete. Construction-only loans require a separate refinance. Fannie Mae explicitly surfaces construction-to-permanent as an ADU financing path.

Biggest Upside

Lets you borrow against what your home will be worth. A critical unlock if you don't have enough current equity.

Biggest Downside

More complex than other paths. Higher closing costs, more paperwork, and you typically need approved plans and a permitted project before the lender will close.

Renovation Loans for ADUs (FHA 203(k), Fannie Mae HomeStyle, Freddie Mac CHOICERenovation)

Best Fit

Homebuyers who want to purchase a property and add or renovate an ADU simultaneously. Also works for existing homeowners willing to refinance.

Bad Fit

Homeowners who want to keep a low existing rate. These products replace your first mortgage.

How Each Works

FHA Standard 203(k)

Finances purchase or refinance plus renovation costs in one loan. Down payment as low as 3.5%. Requires a HUD-approved consultant and contractor. Can cover conversion of an existing structure to include an ADU, adding an attached ADU, and renovating an existing attached or detached ADU. Should not be treated as the default path for a brand-new detached ground-up ADU — the program's ADU provisions are oriented toward conversions and renovations rather than new standalone construction. FHA allows a portion of projected ADU rental income in qualifying under specific conditions. Sources: HUD 203(k) Consumer Fact Sheet; HUD ML 2023-17

Fannie Mae HomeStyle Renovation

Finances purchase or refinance plus renovation based on projected after-completion value. Renovation must be completed within 15 months. ADUs of all types — including detached, modular, and HUD-code manufactured — are eligible if they meet Fannie Mae's property requirements. Source: Fannie Mae Selling Guide B2-3-04

Freddie Mac CHOICERenovation

Similar structure to HomeStyle — finances the purchase or refinance of a home along with renovation, including ADU construction.

Biggest Upside

Lets you borrow based on what the home will be worth post-renovation. Excellent for buyers or homeowners with limited equity who want one loan to cover everything.

Biggest Downside

More paperwork than standard loans. Strict timelines. Contractor requirements. You're refinancing your first mortgage.

Local ADU Financing Programs and Incentives

Best fit: Income-qualified homeowners in cities or states with active programs.

Bad fit: Anyone banking on program availability without verifying current status. Many programs are paused, fully allocated, or pilot-phase only.

We maintain a full verified program tracker below. Here's the honest framing: real programs exist, but they cover a fraction of total ADU demand. Most homeowners will use one of the five paths above — sometimes with a local incentive stacked on top to reduce the total cost.

Cash and Non-Debt Options

If you have savings or other liquid assets, paying cash avoids all interest costs. The tradeoff is opportunity cost.

Home Equity Investments (HEIs) offer a lump sum in exchange for a share of your home's future appreciation. No monthly payments, but you give up a portion of future value gains. Review the terms carefully — the cost of sharing appreciation over a long hold period can exceed the cost of interest on a traditional loan.

Family loans work for some homeowners, but document them properly with a written promissory note. Undocumented loans create tax exposure and can complicate your primary mortgage underwriting.

How Do ADU Financing Paths Compare Side by Side?

| Feature | HELOC | Home Equity Loan | Cash-Out Refi | Construction Loan | Renovation Loan | Local Program |

|---|---|---|---|---|---|---|

| Preserves first mortgage? | ✅ Yes | ✅ Yes | ❌ No | Depends | ❌ No | Varies |

| Current equity required? | Yes | Yes | Yes | Low or none | Low | Varies |

| Uses future value? | ❌ No | ❌ No | ❌ No | ✅ Yes | ✅ Yes | Varies |

| Detached ADU? | ✅ | ✅ | ✅ | ✅ | ✅ HomeStyle, CHOICERenovation | Varies |

| Garage/basement conversion? | ✅ | ✅ | ✅ | ✅ | ✅ | Varies |

| Prefab/modular ADU? | ✅ | ✅ | ✅ | ✅ | ✅ (with requirements) | Varies |

| Manufactured ADU? | Case-by-case | Case-by-case | Case-by-case | Case-by-case | ✅ (permanent foundation + real property required) | Varies |

| Draw structure? | Revolving draws | Lump sum | Lump sum | Staged draws | Staged draws | Varies |

| Rate type | Variable | Fixed | Fixed | Variable → Fixed (C-to-P) | Fixed | Varies |

| ADU rent helps qualify? | Generally no | Generally no | Generally no | Varies by lender | Varies by program | Varies |

Sources: Fannie Mae Selling Guide B2-3-04, Freddie Mac ADU Fact Sheet (Feb 2026), HUD 203(k) Comparison. Last verified March 31, 2026. Actual terms vary by lender — always compare multiple quotes.

The Dwelling Index is reader-supported. When you use our links to apply for financing or request pricing, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation. Full disclosure →

Should You Keep Your Current Mortgage or Replace It?

This is the single most expensive question in ADU financing, and most guides bury it. If you locked in a mortgage during the low-rate environment of 2020–2022, replacing that rate to build an ADU could cost you far more in total interest over the loan's life than the ADU costs to construct. Worth getting right.

When a HELOC or Home Equity Loan Usually Wins

If your first mortgage rate is meaningfully lower than today's rates, a second lien (HELOC or home equity loan) preserves that rate. You pay a higher rate on the ADU money only — not on your entire mortgage balance. For most homeowners who locked favorable rates in recent years, this is the starting point.

When a Cash-Out Refinance Can Still Make Sense

If your current rate is already at or near today's rates — or if you owe very little on your mortgage — the math can favor consolidating everything into one new loan. Run the numbers across both scenarios. Compare total interest paid over the full life of the loan, not just the monthly payment.

When Future-Value Financing Is Your Only Option

If you don't have enough equity for a HELOC or home equity loan, current-value products simply won't provide enough funds. This is where construction loans and renovation loans earn their complexity — they let you borrow based on the projected value of your home after the ADU exists. The Terner Center/Urban Institute identified this “equity gap” as one of the primary reasons lower-equity homeowners struggle to build ADUs, and it's exactly the gap these products are designed to close. (Terner Center, “ADU Construction Financing,” 2022)

How Much Equity Do You Need to Finance an ADU?

The answer depends entirely on which path you choose — and there's a crucial distinction most guides gloss over.

Current-Value Lending vs. After-Completion Lending

Current-value products (HELOC, home equity loan, cash-out refi) calculate borrowing power based on what your home is worth right now. The formula is typically:

If your home is worth $500,000 and you owe $350,000, that's ($500,000 × 0.80) − $350,000 = $50,000. Not enough for most ADU builds.

After-completion products (construction loans, renovation loans) calculate borrowing power based on what your home will be worth with the ADU. If that same $500,000 home would appraise at $650,000 with a detached ADU, your borrowing ceiling increases substantially:

That's the difference between “can't afford it” and “fully funded.” This is why construction and renovation loans exist — and why they're worth the extra paperwork for homeowners without deep existing equity.

Note: Exact LTV limits vary by lender and loan product. These examples use 80% LTV for illustration. Your lender will determine your specific limits based on your credit profile, income, and property.

What Lenders and Appraisers Want to See

Before you apply for any ADU financing, have these ready:

- Approved plans or permitted designs — Many lenders won't underwrite without them, especially for construction and renovation loans

- Contractor bids — At least two detailed bids from licensed, insured contractors

- Current home appraisal — Your lender will order this, but know that ADU appraisals can be challenging in markets with few comparable ADU sales

- Proof of permits or permit eligibility — Lenders want to know your ADU is legal and buildable

- Clear project scope and budget — The more defined your project, the smoother the underwriting

Can Rental Income from the ADU Help You Qualify?

Yes — and this is one of the most important policy changes in ADU financing over the last two years. But the rules differ by agency, and they're more specific than most guides suggest.

What Fannie Mae Currently Allows

Rental income from an ADU on a one-unit principal residence can be used as qualifying income for purchase and limited cash-out refinance transactions. Key conditions:

- Rental income from only one ADU can be counted

- Income is capped at 30% of total qualifying income

- A signed lease or a Single-Family Comparable Rent Schedule (Form 1007) is required

- Borrowers with fewer than 12 months of property management experience face additional limits — qualifying rental income cannot exceed the borrower's housing payment (PITIA)

- Under the HomeReady program, ADU rental income can help qualifying borrowers with lower incomes access better terms

Source: Fannie Mae Selling Guide B3-3.1-08 and B3-3.8-01

What Freddie Mac Currently Allows

Freddie Mac's February 2026 ADU fact sheet outlines similar but distinct parameters for one-unit primary residence mortgages:

- ADU rental income is permitted on purchase and no-cash-out refinance transactions

- Lease-supported income is capped at 75% of the lease amount

- Total qualifying rental income is capped at 30% of total income used to qualify

- A comparable-rent analysis is required

- For purchase transactions, borrowers may need to complete landlord education

Source: Freddie Mac ADU Fact Sheet, February 2026; Freddie Mac Guide Section 5601.2

What FHA Allows

Under HUD Mortgagee Letter 2023-17, for a one-unit property with an ADU and no rental history, FHA uses 50% of the lesser of fair market rent or the lease amount. FHA rental income from an ADU cannot be used on a cash-out refinance transaction.

Source: HUD Mortgagee Letter 2023-17

The bottom line: ADU rental income can meaningfully improve your qualification odds, especially for homeowners who are close to qualifying but need a boost. It's a real tool — just not a blank check.

Compare Lenders

Know your path \u2014 now find the lender who fits it

Compare current options from lenders who specialize in ADU construction financing, sorted by loan type.

The Dwelling Index is reader-supported. When you use our links to apply for financing or request pricing, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation. Full disclosure →

Which Financing Path Works for Each ADU Type?

Your ADU type changes which financing products work smoothly — and which ones create friction.

Detached New-Build ADU

The most flexible for financing. Every path listed on this page works for a detached site-built ADU. Construction loans and renovation loans (particularly HomeStyle and CHOICERenovation) are especially useful here because a detached ADU adds the most appraised value, which strengthens future-value underwriting.

Garage Conversion ADU

Typically the most affordable ADU type, which means equity-based products (HELOC, home equity loan) can often cover the full budget. Renovation loans also work well. FHA 203(k) is a natural fit because the conversion is within or attached to the existing structure.

Basement or Internal Conversion / JADU

Similar to garage conversions in financing flexibility. Because you're working within the existing footprint, costs are usually lower and most lender underwriting is straightforward. FHA 203(k) is well-suited here. See our guide on what is a JADU for more detail.

Attached ADU Addition

All financing paths work. FHA 203(k) is explicitly eligible for attached additions. If you're extending the structure, construction loans handle the staged draw process naturally.

Prefab or Modular ADU

Prefab and modular ADUs built to local or state building code (not HUD code) are generally treated like site-built structures by lenders. Fannie Mae explicitly includes modular ADUs as eligible. Some prefab companies also offer their own financing or have lender partnerships — ask when comparing quotes.

Manufactured (HUD-Code) ADU

This is where financing gets more restrictive. A manufactured-home ADU must meet specific requirements to qualify for conventional financing:

- Must be on a permanent foundation in compliance with manufacturer requirements

- Must be legally classified as real property (not personal property)

- Must comply with HUD Federal Manufactured Home Construction and Safety Standards

- Must include HUD Data Plate or HUD Certification Label documentation

Fannie Mae's HomeStyle Renovation loan can finance a HUD-code manufactured-home ADU when these requirements are met. Freddie Mac specifies that manufactured-home ADUs must be legally classified as real property and meet minimum size thresholds. If your manufactured ADU doesn't meet these requirements, conventional financing may not be available — explore construction loans through local credit unions or specialized lenders.

Owner-Builder Projects

Financing an ADU when you're acting as your own general contractor is harder. Most construction loans and renovation loans require a licensed, insured general contractor. Some lenders will work with owner-builders, but expect stricter terms and more documentation. Start the lender conversation early — before you invest in plans and permits.

Best Financing Path by ADU Type

| ADU Type | Most Common Best Fit | Second-Best Path | Key Watchout |

|---|---|---|---|

| Detached new-build | Construction loan or HELOC (if equity exists) | HomeStyle / CHOICERenovation | Appraisal comps may be limited in your market |

| Garage conversion | HELOC or home equity loan | FHA 203(k) | Scope creep — get a detailed bid before borrowing |

| Basement / internal conversion | HELOC or home equity loan | FHA 203(k) | Building code requirements for egress, ceiling height |

| Attached addition | HELOC or construction loan | 203(k) or HomeStyle | Structural engineering costs often underestimated |

| Prefab / modular | HELOC or construction loan | HomeStyle / CHOICERenovation | Confirm lender treats modular same as site-built |

| Manufactured (HUD-code) | HomeStyle (with permanent foundation) | Specialized lender | Must be real property with HUD compliance documentation |

| Owner-builder | Limited lender options | HELOC (if adequate equity) | Many lenders won't finance owner-builder projects |

Are There ADU Grants or Local Financing Programs in 2026?

Let's start with honesty: there is no reliable nationwide ADU grant you can count on funding your project. Programs exist, but they are local, income-restricted, pilot-phase, or — in the most-searched case — fully allocated.

That said, real programs do exist elsewhere — and some are genuinely meaningful. Here's what we've verified:

Verified ADU Financing Programs (March 2026)

| Program | Location | Type | Amount | Status | Key Requirement |

|---|---|---|---|---|---|

| MassHousing ADU Loan | Massachusetts (statewide) | Fixed-rate 2nd mortgage | Up to $250K (detached) / $150K (attached) | ✅ Active — launched March 2026 | Designs and permits in hand |

| MHP ADU Incentive Program | Massachusetts (statewide) | Feasibility study funding | Varies | 🟡 Phase 1 launching Spring 2026 | MA homeowner |

| SDHC ADU Finance Program | San Diego, CA | Construction loan + tech assistance | Up to $250K | ✅ Active | Income-qualified; rent at affordable rate |

| Colorado CHFA ADU Finance | Colorado (ADU Supportive Jurisdictions) | Loans + credit enhancements | Varies | ✅ Active | Resident of certified ADU Supportive Jurisdiction |

| NYC Plus One ADU Program | New York City | Low/no-interest loans + grants | Varies | ✅ Accepting interest surveys | 1–2 family NYC homeowners |

| Salt Lake City Backyard Keys | Salt Lake City Westside | ADU loan (pilot) | Varies | 🟡 Pilot — rolling basis as funding available | Owner-occupant on qualifying Westside properties |

| Orlando ADU Incentive Program | Orlando, FL | Rebates + fee relief | Varies | ✅ Active | Tied to affordability requirements |

| Queen City ADU Program | Charlotte, NC | Up to $80K forgivable financing | Up to $80K | ⛔ Initial round closed Oct 31, 2025; confirm future rounds | Income-restricted tenants; 8-year affordability period |

| Portland ADU SDC Waiver | Portland, OR | System Development Charge waiver | Varies | ✅ Active (requires 10-year covenant) | Portland property owners building ADU |

| CalHFA ADU Grant | California (statewide) | Grant (non-repayable) | Up to $40K | ⛔ Fully allocated since Dec 2023 — NOT accepting applications | N/A |

This is not an exhaustive list. New programs launch regularly. Always confirm status directly with the administering agency before making financial decisions based on program availability. If your area isn't listed, check with your city or county planning department.

The Smart Move: Don't Wait for a Grant

If you've been waiting for a grant to make your ADU affordable, here's the reality most homeowners who build ADUs face: they fund the project with mainstream financing, not grants. The programs above help at the margins, but the core funding for most projects comes from the equity and lending paths described in this guide.

The smartest approach is to pursue local incentives where they exist and have a mainstream financing plan as your primary path. Waiting for grant funding that may never reopen — or may take months to process — can cost you more in construction-cost escalation than the grant would have saved.

Free ADU Report

While grant availability is limited, homeowners are building ADUs across the country every day. See which financing paths fit your situation.

See what you can build at your address \u2014 zoning, feasibility, and the financing paths that match your lot.

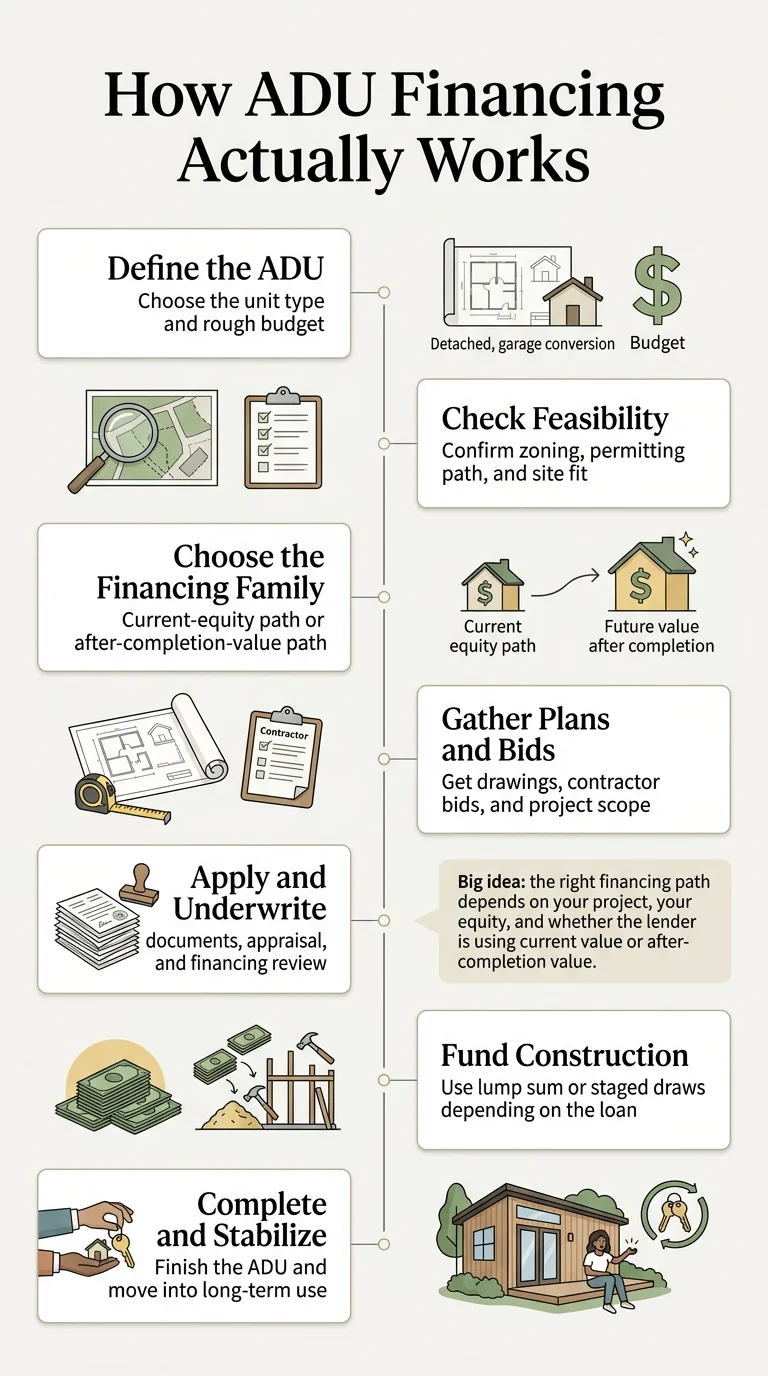

What Does the ADU Financing Process Actually Look Like?

Most guides make this sound linear and smooth. It's not always. Here's the real sequence, including the parts that trip people up.

Define Your ADU Type and Rough Budget

Before talking to any lender, know what you're building. A garage conversion and a detached 1,000 sq ft new build are different financing projects. Get at least two contractor bids or use an ADU cost estimator to establish a range.

→ How much does an ADU cost?Check Feasibility and Permit Path

Lenders won't fund an ADU that can't legally be built. Confirm your lot qualifies under local zoning: setbacks, lot coverage, height restrictions, and owner-occupancy rules. Pull your city or county's ADU ordinance or use a feasibility tool before you invest in plans.

Choose Your Financing Family

Based on your equity, mortgage rate, ADU type, and timeline — use the frameworks in this guide to narrow to 1–2 paths. Don't let a lender choose for you based on what they sell.

Gather Documents and Project Details

Personal Finance Documents

- Recent pay stubs or W-2s (or profit-and-loss for self-employed)

- Tax returns

- Bank statements

- Current mortgage statement

Property and Project Documents

- Approved ADU plans or permitted designs

- Detailed contractor bids with scope and timeline

- Proof of permits or permit eligibility

- Construction draw schedule (for construction loans)

Rental Income Documents (if applicable)

- Signed lease from existing tenant

- Or a Single-Family Comparable Rent Schedule (Fannie Mae Form 1007) with market rent analysis

Apply to Multiple ADU-Experienced Lenders

Apply to 2–3 lenders who have ADU financing experience. Not all loan officers understand ADU products — ask specifically about their ADU volume. The appraisal is often the longest step, especially for future-value products where the appraiser needs your plans and contractor bids.

Manage Draws and Inspections (Construction / Renovation Loans)

If you're using a construction or renovation loan, funds are released in stages as your contractor hits milestones. A lender-ordered inspector verifies progress before each draw. This protects both you and the lender, but it adds time. Build it into your construction timeline.

Convert to Permanent Financing (If Applicable)

Construction-to-permanent loans convert automatically. Construction-only loans require a separate refinance. Know which type you have before you close.

What Does the Right Financing Choice Look Like in Three Real Scenarios?

These are illustrative scenarios designed to show how the same financing landscape produces different right answers for different people. Not real individuals — realistic composites.

Case 1

Significant Equity, Low Mortgage Rate, Detached ADU

The Situation

A homeowner in a Denver suburb purchased 15 years ago. The home has appreciated substantially, and the remaining mortgage balance is well below half the current value — locked at a rate well below today's market. Excellent credit. Wants to build a detached ADU for rental income.

Best Path

HELOC. Ample equity means the full ADU budget is within reach. A HELOC preserves her favorable first mortgage rate. She draws funds as construction progresses and pays interest only during the build phase. Once the ADU is rented, rental income helps cover the HELOC payments.

Key Tradeoff

Why not a cash-out refi? Replacing a favorable rate on a low-balance mortgage with a higher rate on a much larger balance would cost significantly more over the loan's life — even though the monthly payment looks tidy on paper.

Bonus Opportunity

She checks whether her Colorado county is a CHFA-certified ADU Supportive Jurisdiction, which could unlock additional financing incentives through the Colorado ADU Finance Program.

Case 2

Low Equity, Strong Income, Need for Family Housing

The Situation

A homeowner in the Portland metro area bought in 2022 with a modest down payment. Current equity is minimal because the purchase was recent — a standard HELOC simply can't access enough funds. Strong income, good credit. Aging mother needs a place to live.

Best Path

Construction-to-permanent loan based on after-completion value. With the ADU factored in, the home's projected value creates meaningful borrowing power that doesn't exist today. He may still need to bring some personal savings to bridge the gap. Alternatively, a Fannie Mae HomeStyle renovation loan could cover the full amount — but he'd lose his current rate.

Key Tradeoff

This is exactly the 'equity gap' the Terner Center identified. The path exists, but it requires more creativity and likely combines multiple funding sources.

Bonus Opportunity

Portland's ADU System Development Charge waiver saves real money on permit-stage costs — and it's currently active.

Case 3

Garage Conversion with a Local Incentive

The Situation

A homeowner in San Diego with enough equity to cover the project through a HELOC. She wants to convert her detached garage into a studio ADU for rental income. She's income-eligible for the SDHC ADU Finance Program.

Best Path

Combine a HELOC with the San Diego Housing Commission's ADU Finance Program, which provides construction-to-permanent financing plus free technical assistance. The SDHC program could reduce her borrowing costs — but requires renting the ADU at affordable rates for up to seven years.

Key Tradeoff

The real decision: is the discounted financing worth the rental-rate restriction? For a homeowner who planned to rent at roughly market rates to a moderate-income tenant, the program math works. For someone targeting top-of-market rents, the restriction may not pencil.

These are illustrative examples, not guarantees of rates, costs, or returns. Actual costs vary by location, design, materials, and market conditions. Rental income projections should be validated with local market research. Consult a financial advisor before making borrowing decisions.

Free ADU Report

These homeowners figured out their path. Now it's your turn.

See what you can build at your address \u2014 zoning, feasibility, and the financing paths that match your lot.

How Does The Dwelling Index Evaluate ADU Financing Paths?

We sort and compare financing options by:

- Financing path and property fit — not lender compensation

- State and geographic availability

- Current-equity vs. after-completion fit — the most important variable most guides ignore

- Ability to preserve an existing first mortgage

- Rental-income treatment — per current Fannie Mae, Freddie Mac, and FHA guidelines

- Draw structure and construction compatibility

- Contractor and owner-builder constraints

- Official eligibility and local-program status — verified with dates

We do not rank lenders by compensation. We do not quote specific rates, APRs, or monthly payments. We position ourselves as an independent educational resource. When we link to lender partners, we disclose that relationship clearly.

ADU Financing FAQ

What is the best way to finance an ADU?

There’s no single best way — the right path depends on your equity, your current mortgage rate, and your ADU type. Homeowners with significant equity and a favorable mortgage rate typically start with a HELOC. Those with limited equity look toward construction loans or renovation loans that underwrite based on future value. The comparison table at the top of this page maps each path to the situation it fits best.

Is a HELOC or cash-out refinance better for an ADU?

If your mortgage rate is below current market rates, a HELOC almost always wins because it preserves your existing rate. A cash-out refinance replaces your entire mortgage, which only makes sense if your current rate is already at or above today’s levels.

Can I get a construction loan for an ADU?

Yes. Construction loans and construction-to-permanent loans are specifically designed for building projects and can underwrite based on the projected after-completion value of your home. They’re more complex than equity products but essential for homeowners without enough current equity. Fannie Mae explicitly lists construction-to-permanent as an ADU financing path.

Can I use FHA 203(k) for an ADU?

Yes, with important scope considerations. The Standard 203(k) can cover converting an existing structure to include an ADU, adding an attached ADU, and renovating an existing ADU. It should not be treated as the default path for building a brand-new detached ADU from the ground up. For detached new-build ADUs, Fannie Mae HomeStyle or a construction loan are typically better fits.

Can rental income from the ADU help me qualify?

Yes. Fannie Mae, Freddie Mac, and FHA all allow ADU rental income to count toward qualifying income under specific conditions, though the rules differ by agency. All three cap qualifying rental income at 30% of total income (Fannie Mae and Freddie Mac) or use a percentage of fair market rent/lease amount (FHA). A signed lease or comparable rent schedule is typically required.

Can I finance a prefab or modular ADU?

Yes. Modular ADUs built to state or local building code are treated like site-built structures by most lenders. Manufactured (HUD-code) ADUs require a permanent foundation and legal classification as real property. Fannie Mae’s HomeStyle loan explicitly allows HUD-code manufactured ADUs when these requirements are met.

What if I don’t have enough equity?

Explore future-value financing: construction loans, construction-to-permanent loans, FHA 203(k), or Fannie Mae HomeStyle. These products underwrite based on what your home will be worth after the ADU is built. Some local credit unions also offer ARV (after-renovation-value) HELOCs.

Are there ADU grants in California right now?

California’s statewide CalHFA ADU Grant has been fully allocated since December 2023 and is not accepting new applications. Some city-level programs remain active — San Diego’s SDHC program being the most notable. Always verify program status directly.

Do ADU financing programs require affordable rents?

Many do. Programs that provide reduced-cost financing often require the ADU to be rented at below-market rates to income-qualified tenants for a set period (typically 5–15 years). Read the program terms carefully before applying.

What documents do I need for ADU financing?

At minimum: income documentation, bank statements, current mortgage statement, approved ADU plans, contractor bids, and proof of permit eligibility. For construction and renovation loans, you’ll also need a detailed construction draw schedule. If claiming rental income, you’ll need a signed lease or comparable rent analysis.

What happens if the appraisal comes in low?

Your borrowing power drops. You may need to bring more cash to close, reduce project scope, or provide the appraiser with additional comparable data. Build a contingency buffer into your financing plan from the start.

Does an owner-builder approach make financing harder?

Yes, significantly. Most construction and renovation loans require a licensed, insured general contractor. Some lenders will work with owner-builders under stricter terms — discuss this early in the process.

Does an ADU usually add value to the property?

FHFA data shows that California properties with ADUs experienced stronger median appraised-value growth than properties without ADUs over 2013–2023. Results vary by market, unit type, and quality. This is historical California data, not a nationwide guarantee.

Will building an ADU increase my property taxes?

In most cases, yes. Assessment methods vary by state and locality — confirm the impact with your county assessor before finalizing your financial plan.

What to Do Next

There's no magic ADU loan. There are real financing paths, and the right one depends on your mortgage, your equity, your ADU type, and whether rental income can help you qualify. The wrong choice — especially replacing a favorable mortgage you don't need to — can be the most expensive mistake in the entire project.

The best next step isn't more browsing. It's getting a property-specific answer.

Free ADU Report

Not sure where to start? See what's possible at your address.

See what you can build at your address \u2014 zoning, feasibility, and the financing paths that match your lot.

Free Download

2026 ADU Financing Starter Kit

Financing checklists, state program directory, cost estimation templates, and lender interview questions. No commitment, no spam.

Download the Free 2026 ADU Starter KitFind Your State or City ADU Financing Rules

Keep Reading

Last updated: March 31, 2026 · Sources verified against official Fannie Mae, Freddie Mac, HUD, and local program documentation

The Dwelling Index is an independent national ADU resource. We do not originate loans, act as a broker, or rank financing options by compensation. Editorial methodology → · Affiliate disclosure →