RenoFi vs Cash-Out Refinance for an ADU: Which Funding Path Actually Fits in 2026?

By the Dwelling Index Editorial Team — Dwelling Index is an independent research resource covering ADU financing, costs, and regulations.

•

Not a lender. Not financial, legal, or tax advice. Educational comparison only.

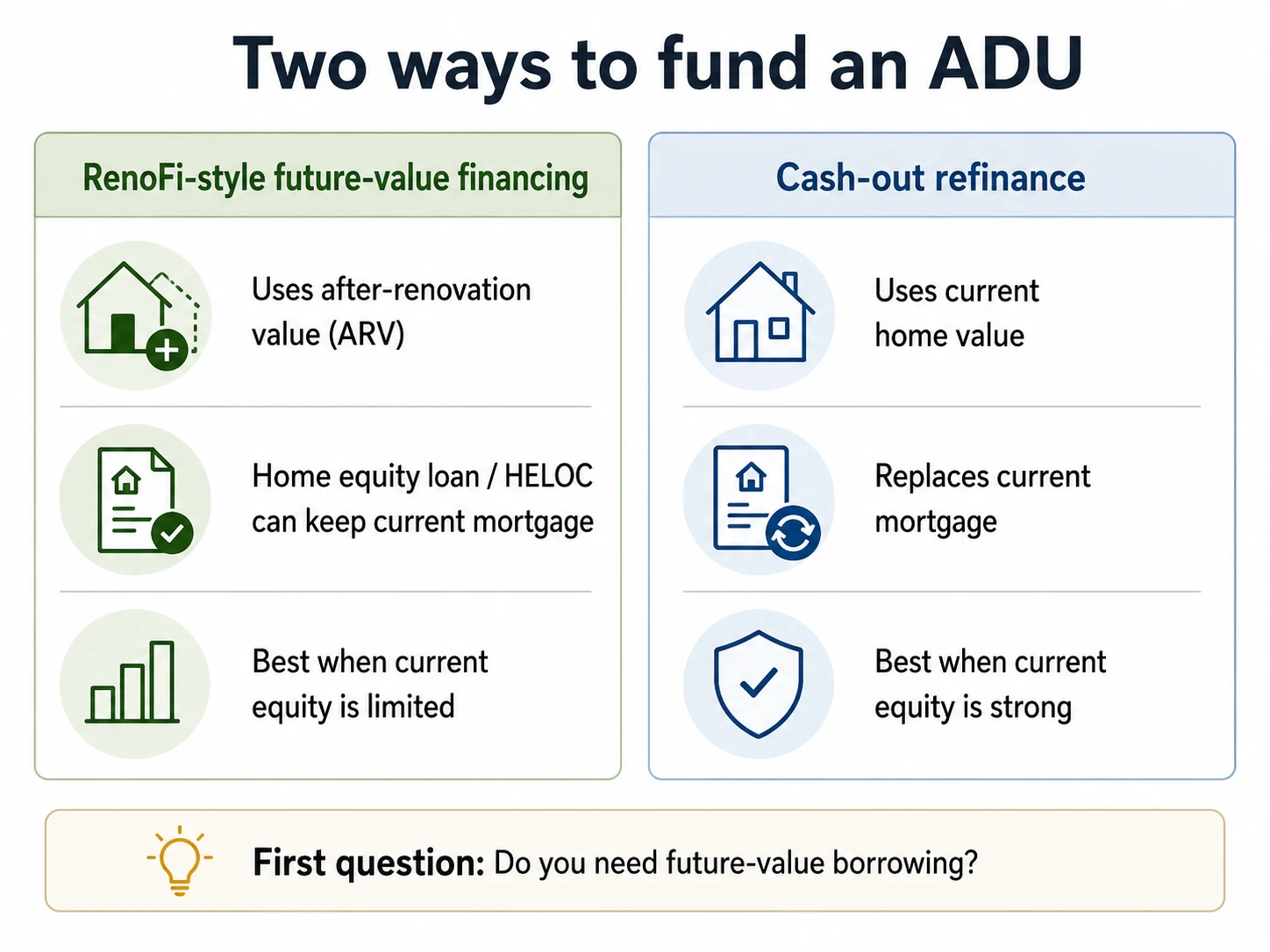

The bottom line, in one screen

RenoFi vs cash-out refinance comes down to two questions: do you need to borrow against your home’s future value to fund the ADU, and do you want to keep your existing mortgage? A RenoFi loan lets you borrow against your home’s after-renovation value (ARV) — up to 90% of that future value, up to $750,000 per RenoFi.com, through a third-party lender partner — and the home-equity-loan and HELOC versions sit behind your first mortgage so you keep your current rate. A traditional cash-out refinance replaces your entire first mortgage with a bigger one at today’s market rate. The 30-year fixed mortgage benchmark averaged 6.36% as of May 14, 2026 per Freddie Mac’s Primary Mortgage Market Survey, and cash-out refinance rates generally run higher than rate-and-term refinance rates because lenders consider them higher-risk.

Quick verdict:

- First-mortgage rate below 5% + not enough current equity for the ADU → start with a RenoFi-style after-renovation-value path (HELOC or Home Equity Loan version). Don’t touch the first mortgage.

- First-mortgage rate at or above today’s market + meaningful current equity → a cash-out refinance can fund the ADU and consolidate everything into one payment.

- RenoFi availability: RenoFi confirms its lenders do not currently offer loans in Nevada, and its site is not authorized by the New York State Department of Financial Services. Bankrate’s February 2026 review also lists Hawaii and Massachusetts as RenoFi exclusions. Texas requires direct product-level verification. [Verified May 21, 2026.]

Next step: Confirm your lot will support the ADU you’re financing before choosing a loan product. A financing approval doesn’t solve zoning, setbacks, or permit feasibility.

See What You Can Build at Your Address: Get Your Free ADU ReportAddress-level feasibility, in minutes. No hard credit pull.

RenoFi vs cash-out refinance at a glance

The two products do completely different things to your balance sheet. Here’s the head-to-head built from official RenoFi disclosures, Bankrate’s February 2026 review, Freddie Mac PMMS, and Fannie Mae’s Selling Guide. Sources and verification dates are listed in the “What We Verified” box at the end.

| Factor | RenoFi loan (HE Loan, HELOC, or RenoFi Refi) | Traditional cash-out refinance |

|---|---|---|

| Lender type | RenoFi is not the lender. Loans are made by third-party lender partners (some are credit unions) using RenoFi’s underwriting technology. RenoFi entity NMLS #1802847; California entity NMLS #2412747. | Direct mortgage lenders (banks, credit unions, online lenders) |

| Value the loan is written against | After-renovation value (ARV) — what an appraiser estimates the home will be worth once the ADU is built | Current appraised value |

| Max loan-to-value | Up to 90% of ARV per RenoFi.com; some wholesale lender programs may reach 95% ARV case-by-case | Conventional cash-out typically caps at 80% LTV for a one-unit primary residence per agency guidelines |

| Max loan amount | $25,000 to $750,000 per RenoFi.com | Conforming loan limit applies; jumbo above that |

| Typical 2026 rate context | Variable HELOC priced on prime + lender margin; fixed Home Equity Loan terms of 10, 15, or 20 years through lender partners. RenoFi does not publish rates publicly; rates vary by lender. | Freddie Mac PMMS 30-year fixed benchmark 6.36% as of May 14, 2026. Cash-out rates are generally higher than rate-and-term refi rates per Bankrate. |

| Keeps your first mortgage? | Yes — for the Home Equity Loan and HELOC versions. No — the RenoFi Refi replaces it. | No — replaces your existing mortgage entirely |

| Closing-cost range | Origination + title + recording + ARV appraisal — varies by lender partner | Typically 2%–5% of the new loan amount |

| Typical time to close | Bankrate flags the ARV appraisal process as RenoFi’s main tradeoff — longer than a standard HELOC; RenoFi’s own wholesale material references possible 30-day closings depending on lender and documentation | Varies by lender, appraisal, underwriting, and documentation |

| Minimum credit score | Some lenders accept 620; higher tiers for larger loans per Bankrate (Feb 2026) | Typically 620+ for conventional cash-out; FHA cash-out goes lower |

| State availability | Nevada: not offered (RenoFi.com). New York: site not authorized by NYDFS (RenoFi.com). Hawaii, Massachusetts: not available per Bankrate (Feb 2026). Texas: verify directly under TX Constitution Art. XVI §50(a)(6). | All 50 states |

| Appraisal type | Special ARV appraisal based on submitted renovation plans (RenoFi.com) | Standard appraisal of current value |

| Best fit | Recent buyer with low current equity but high-impact ADU project; homeowner protecting a sub-5% first mortgage | Homeowner with substantial current equity and a first mortgage at or above today’s market |

| Worst fit | Property in NV, NY, HI, or MA; project under ~$25K | Homeowner with a sub-5% first mortgage of any size — the blended-rate cost typically dwarfs the cash extracted |

The single most important row is the second one — value basis. That’s what makes one product lend you several times more than the other on the same property.

Sources: RenoFi.com (How It Works, FAQ, homepage NYDFS disclosure, Realtor page Nevada disclosure); Bankrate RenoFi Review (Feb 27, 2026); Freddie Mac PMMS (May 14, 2026); LendEDU RenoFi Review (May 1, 2026); Fannie Mae Selling Guide B2-1.3-03.

The four-input decision matrix: which path fits your situation?

Picking between these two products is determined by four inputs: your existing first-mortgage rate, your equity position today, your project size, and your state. Below is the decision matrix.

| If your first-mortgage rate is… | And your equity is… | And your project is… | And your state is… | Start here |

|---|---|---|---|---|

| Below 5% | Below 30% of current value | $50K–$500K | Available state | RenoFi HELOC or RenoFi Home Equity Loan — keep your low first mortgage, borrow against ARV |

| Below 5% | Above 30% of current value | Under $150K | Anywhere | Traditional HELOC — your current equity covers it; no need for the ARV process |

| Below 5% | Above 30% of current value | Above $150K | Available state | RenoFi HELOC — gets you to ARV-level borrowing without losing your rate |

| 5%–6% | Above 40% of current value | Any | Anywhere | Either path is defensible — choose based on whether you want one payment (cash-out) or two (RenoFi second lien) |

| Above 6% | Above 30% of current value | Any | Anywhere | Cash-out refinance — you’re not giving up a great rate; consolidate the ADU into one mortgage |

| Above 6% | Below 30% of current value | $100K+ | Available state | RenoFi Refi — replaces your mortgage anyway, but uses ARV instead of current value (lends more) |

| Any rate | Any | Investment property | Anywhere | Cash-out refi or DSCR financing — RenoFi ARV loans are generally restricted to primary residences and select second homes |

| Any rate | Any | Any | NV, NY, HI, MA | Cash-out refi, traditional HELOC, or Fannie Mae HomeStyle Renovation — RenoFi not available |

If your scenario falls between two rows, run the side-by-side math (we walk through it in the next section). The matrix is a starting point — your specific rate, DTI, credit profile, and contractor budget will move the answer.

Tells you what you can build, the cost range for your zip code, and which financing lane to test first.

What “RenoFi” actually is — and what RenoFi isn’t

RenoFi is a licensed mortgage broker (entity NMLS #1802847; California entity NMLS #2412747) that connects homeowners to third-party lender partners who underwrite renovation loans against after-renovation value rather than current value. RenoFi itself does not make the loan; the lender partner does. Some lender partners are credit unions, but not all are — verify the actual lender with your assigned RenoFi advisor. There are three distinct RenoFi products people frequently confuse with each other, and the difference between them is the entire point of picking one.

The three RenoFi products

| Product | Structure | Touches first mortgage? | Best for |

|---|---|---|---|

| RenoFi Renovation HELOC | Second-lien revolving line of credit, variable rate (prime + margin), 10-year draw period, then 10/15/20-year repayment | No | Homeowners who want a low first mortgage preserved and need flexibility on when to draw funds |

| RenoFi Renovation Home Equity Loan | Second-lien fixed-rate lump sum, 10/15/20-year amortization | No | Homeowners who want a low first mortgage preserved and want fixed, predictable monthly payments |

| RenoFi Refi (cash-out refi) | First-mortgage refinance written against ARV. Cap of 80% of ARV minus the existing mortgage balance; new total mortgage capped at $2M (amounts over $600K may require additional lender review). | Yes — replaces it | Homeowners whose existing first-mortgage rate is at or above today’s market and who want one consolidated mortgage payment |

The HELOC and Home Equity Loan versions sit behind your first mortgage. The RenoFi Refi replaces your first mortgage — which means it carries the same rate risk as any traditional cash-out refi. If you have a 3% first mortgage, the RenoFi Refi is almost always the wrong RenoFi product for you, and one of the second-lien versions is the right one.

How “after-renovation value” actually works

RenoFi orders a special ARV appraisal up front, based on the renovation plans you submit. The appraiser estimates what the home will be worth once the ADU is built. The lender partner then writes the loan against that future number rather than the home’s current appraised value. This is why a borrower with little current equity can still qualify for a six-figure renovation loan — the value created by the ADU is being credited toward borrowing power before the ADU exists.

Where RenoFi works — and where it doesn’t

Per RenoFi’s own materials and Bankrate’s February 27, 2026 RenoFi review, RenoFi’s availability footprint as of May 2026:

- ✗Nevada: RenoFi states directly on its site that its lenders do not currently offer loans for Nevada properties.

- ✗New York: RenoFi’s homepage carries a disclosure that the site is not authorized by the New York State Department of Financial Services and that no mortgage solicitation can be facilitated through the site for properties located in New York.

- ✗Hawaii and Massachusetts: Listed as exclusions in Bankrate’s February 2026 RenoFi review.

- !Texas: Texas’s home-equity lending rules under the Texas Constitution Article XVI §50(a)(6) impose strict consumer-protection requirements and product limitations. Verify with RenoFi directly before relying on availability or paying for an appraisal.

If you’re in any of these states, the strongest national alternative for ARV-based ADU borrowing is Fannie Mae’s HomeStyle Renovation loan (covered below).

How a cash-out refinance works in 2026 (and the trap most homeowners walk into)

A cash-out refinance replaces your existing mortgage with a new, larger one and pays you the difference in cash. In May 2026 that means trading your existing rate for a new mortgage priced off today’s market. The 30-year fixed-rate mortgage benchmark averaged 6.36% per Freddie Mac PMMS for the week of May 14, 2026 — note this is a national purchase-loan benchmark, not a cash-out refinance quote. Cash-out refi rates are generally higher than rate-and-term refinance rates because lenders treat cash-out loans as higher-risk.

The “blended-rate trap” worked out in real dollars

Here’s the math nobody on the front of the search results is showing you, on a typical recent-buyer scenario.

Setup

- Current home value: $500,000

- Existing first mortgage: $300,000 at 3.5% (locked in 2021)

- Existing monthly P&I: ~$1,347

- ADU project budget: $200,000

- Estimated after-ADU home value (ARV): $700,000

Path A — Traditional cash-out refinance at 6.36%

| Line | Amount |

|---|---|

| Current value × 80% max LTV | $400,000 |

| Minus existing mortgage | −$300,000 |

| Cash available for ADU | $100,000 ❌ Shortfall |

| New loan balance (max cash) | $400,000 |

| New monthly P&I at 6.36%, 30-yr | ~$2,492 |

| Monthly payment increase | +$1,145 |

| First-mortgage portion repriced 3.5% → 6.36% | $300,000 |

You wanted to extract $100,000 for an ADU. To get it, you also gave up your $300,000 at 3.5%. Under this example’s assumptions, repricing the existing $300,000 balance from 3.5% to 6.36% adds roughly $84,000 of additional interest over the first 10 years alone, before closing costs and other loan-cost differences. And you only got $100,000 — not enough to fund the $200,000 ADU.

Path B — RenoFi Home Equity Loan (second lien, illustrative rate)

| Line | Amount |

|---|---|

| ARV × 90% max LTV | $630,000 |

| Minus existing mortgage | −$300,000 |

| Borrowing room against ARV | $330,000 |

| Loan taken | $200,000 (full ADU funded) |

| Existing mortgage: untouched at 3.5% | $300,000 ✅ |

| Illustrative second-lien P&I at 9.0%, 20-yr | ~$1,799 |

| Existing first-mortgage P&I (unchanged) | ~$1,347 |

| Total monthly P&I | ~$3,147 |

The 9.0% used in Path B is an illustrative second-lien rate, not a RenoFi quote, APR, or advertised rate. RenoFi does not publish rates publicly; rates vary by lender partner.

In Path B you pay more total monthly — but you fully fund the ADU, your $300,000 first mortgage stays at 3.5%, and you only pay the higher rate on the new $200,000 of debt rather than on a $400,000 combined balance. In this specific example, the rate gap makes the cash-out path fail both the borrowing-power test and the first-mortgage-repricing test. Whether the same conclusion applies to your scenario depends on your loan balance, existing rate, ADU budget, projected ARV, closing costs, holding period, and tax treatment — run your own numbers before deciding.

Best for homeowners whose current equity already covers the ADU and whose existing mortgage isn’t worth preserving. If you have a sub-5% first mortgage, skip this and read the RenoFi sections above.

Same home, same ADU: which one actually lends you more?

On the math alone, RenoFi almost always wins on borrowing power for an ADU — because RenoFi is one of the few products designed to lend against future value. Here is the same balance sheet, run through three products. These numbers are illustrative and rounded for clarity.

Scenario: $500,000 home today, $350,000 existing mortgage at 4%, $200,000 ADU project, estimated $700,000 ARV.

| Same scenario, three products | Traditional cash-out refi | RenoFi Refi (cash-out, ARV-based) | RenoFi Home Equity Loan (second lien, ARV-based) |

|---|---|---|---|

| Value the loan is written against | Current $500K | ARV $700K | ARV $700K |

| Max LTV | 80% | 80% | 90% |

| Max borrowing basis | $400,000 | $560,000 | $630,000 |

| Minus existing mortgage | −$350,000 | −$350,000 | −$350,000 (sits behind it) |

| Cash available for ADU | $50,000 ❌ Shortfall | $210,000 ✅ | $280,000 ✅ |

| ADU funded? | ❌ Shortfall | ✅ Yes, with contingency | ✅ Yes, with contingency |

| Existing first mortgage at 4% | Replaced at today’s rate | Replaced at today’s rate | Preserved ✅ |

When RenoFi is the wrong choice

RenoFi is the wrong product when the state, property type, project size, or timeline doesn’t fit — or when you can’t tolerate the rate uncertainty of being matched to a single lender partner.

State exclusions

Per RenoFi’s own materials and Bankrate’s February 2026 review: Nevada (not offered), New York (NYDFS not authorized), Hawaii and Massachusetts (listed as exclusions in Bankrate’s review), Texas (verify directly before any application or appraisal payment).

Property type

RenoFi ARV loans are generally positioned for primary residences and select second homes (lender-dependent). If you’re building an ADU on an investment property, RenoFi isn’t typically an option and a cash-out refi or DSCR loan is your path.

Small projects

If your ADU project is under approximately $25,000–$50,000 — say, a basic conversion of an existing finished space into a JADU (junior accessory dwelling unit; defined in California Government Code §66313(d) as a unit no larger than 500 square feet of interior livable space contained entirely within a single-family residence) — a traditional HELOC at your existing bank or credit union will close faster and cheaper.

Timeline pressure

The ARV appraisal adds time to the underwriting process compared with a standard HELOC, where a current-value appraisal is faster and simpler. RenoFi’s own wholesale material references possible 30-day closings depending on lender and documentation, but Bankrate’s 2026 review flags the longer process as RenoFi’s primary tradeoff. Confirm the expected timeline with your assigned lender partner once matched.

Rate-shopping limits

This is RenoFi’s most honest weakness, and we’ll name it plainly: you cannot effectively shop RenoFi’s rate against the open market until after you’ve paid for the ARV appraisal. RenoFi matches you to one lender partner; you don’t get to compare three competing quotes the way you would with a refi marketplace. For an ADU borrower whose equity-to-project-cost gap is wide, the ARV math usually still wins — but the lack of shopping leverage is a real cost.

When a cash-out refinance is the wrong choice

A cash-out refinance is the wrong choice when your current first-mortgage rate is meaningfully below today’s market rate, because every dollar of your existing mortgage gets repriced — not just the cash you wanted to pull out. With Freddie Mac PMMS at 6.36% on May 14, 2026, and tens of millions of homeowners holding sub-5% pandemic-era rates, this is the single most expensive financing mistake on the market in 2026.

The blended-rate problem, restated as a verdict

If your existing first mortgage is well below today’s market, a cash-out refi is almost certainly the wrong product. The cash you extract is real, but the additional interest you pay on the repriced portion of your existing balance — over the remaining life of the loan — typically exceeds the cash extracted by a wide margin, as the worked example above demonstrates.

The 30-year amortization reset

A cash-out refi typically resets your amortization clock to 30 years. If you’ve already paid down 7 or 10 years of your existing mortgage, you’re starting over on a larger principal — meaning more of your monthly payment goes to interest for years before it starts touching principal again. The monthly looks affordable; the long-term cost is significant.

LTV and DTI thresholds

For conventional cash-out refinance on a one-unit primary residence, agency guidelines typically cap LTV at 80%; other property types and occupancy categories have lower caps. FHA cash-out refinance uses FHA mortgage insurance, not conventional PMI, and has its own LTV rules. Your debt-to-income ratio will also increase with the larger loan; if you’re already near lender thresholds (typically 43%–50% depending on the program), the cash-out may not qualify.

When the cash-out still wins

A cash-out refinance is genuinely the right call when:

- Your existing first mortgage is at or above today’s market rate (you’re not giving up anything by refinancing).

- Your existing balance is small enough that the repricing math doesn’t matter.

- You want a single mortgage payment and accept the tradeoff.

- You’re consolidating high-interest debt at the same time (a $40,000 credit card balance at 22% rolled into a mortgage rate in the 6%s is genuine savings).

What about the RenoFi Refi? Is it just a better cash-out?

The RenoFi Refi is a cash-out refinance written against after-renovation value, which means it carries the same first-mortgage-replacement risk as any cash-out refi but gives you significantly more borrowing power for an ADU. It’s the right product for one specific borrower: someone whose existing mortgage rate is already at or above today’s refi rate and whose project will materially boost ARV.

Per RenoFi.com, the RenoFi Refi caps the cash-out proceeds at 80% of ARV minus the existing mortgage balance, with the new total mortgage capped at $2 million; amounts over $600,000 may require additional lender review.

When the RenoFi Refi beats a traditional cash-out refi: when ARV is materially higher than current value and the borrower is already comfortable replacing the first mortgage. The ARV math is structurally superior to current-value math on any project that creates meaningful future value. It can still lose on rate, fees, lender availability, appraisal outcome, or process friction — verify all of these for your specific situation.

When the RenoFi Refi loses to the RenoFi Home Equity Loan or HELOC: when your existing first-mortgage rate is below today’s market rate. In that case, you don’t want to replace the first mortgage at all — you want to leave it alone and add a second lien against ARV. That’s exactly what the Home Equity Loan and HELOC versions are designed for.

The decision tree for picking among the three RenoFi products:

- Is your existing first-mortgage rate above today’s market? → RenoFi Refi.

- Is your existing first-mortgage rate below today’s market, and do you want a fixed monthly payment? → RenoFi Renovation Home Equity Loan.

- Is your existing first-mortgage rate below today’s market, and do you want flexibility on when you draw funds? → RenoFi Renovation HELOC.

What can go wrong with either product

Both paths can fail for reasons unrelated to the product itself: low appraisal value, DTI issues, credit-profile gaps, LTV ceilings, state-availability questions, first-mortgage seasoning rules, contractor documentation, or whether the ADU is actually permitted and buildable.

| Risk | Hits RenoFi HE Loan / HELOC? | Hits RenoFi Refi? | Hits traditional cash-out? | What to verify before applying |

|---|---|---|---|---|

| ARV appraisal comes in low | Yes — borrowing room shrinks | Yes — borrowing room shrinks | No (uses current value) | Contractor’s bid, scope of work, comparable ADU values in your zip code |

| Current equity too thin | Less likely (uses ARV) | Less likely (uses ARV) | Yes — can disqualify entirely | Your current LTV; check a current valuation estimate vs your balance |

| Existing first-mortgage rate is low | No (second-lien preserves it) | Yes — gives it up | Yes — gives it up | Your current rate vs PMMS benchmark this week |

| State or property type not eligible | Yes — NV/NY/HI/MA + TX caveat | Yes — same exclusions | Rarely (50-state available) | RenoFi.com directly, plus your state’s home-equity lending rules |

| DTI ratio too high | Yes | Yes | Yes | Whether projected ADU rent can count for your specific loan program |

| Cash-out seasoning rules | No (second lien) | Yes — agency rules apply | Yes — agency rules apply | Fannie Mae Selling Guide B2-1.3-03; lender’s specific rules |

| ADU not permitted under local zoning | Yes — kills the project | Yes — kills the project | Yes — kills the project | Your municipality’s ADU ordinance; consult the Feasibility Engine |

| Contractor not licensed/insured | Yes — most renovation lenders require documentation | Yes | Less strictly required | Your contractor’s license number and insurance certificates |

| Already started construction | Yes — most renovation lenders require pre-construction approval | Yes | No — funds are unrestricted | Whether any work has begun before underwriting |

A loan approval does not confirm zoning, setback, utility-lateral, or permit feasibility, and does not confirm HOA/CC&R compliance — state laws differ on how private restrictions interact with ADU rights. Confirm feasibility before you spend money on an appraisal or a loan application.

Free address-level feasibility check. Identifies state ADU statute, municipal setback and lot-size requirements, and approximate cost range. No hard credit pull.

Can projected ADU rental income help me qualify? The program-by-program matrix

The answer is “sometimes, and the rules vary significantly by program.” Most pages collapse this into a single sentence; we built the matrix instead, because the wrong assumption here kills more financing applications than any other.

| Loan program | ADU rental income — purchase or rate-and-term refi | ADU rental income — cash-out refi | Cap on income inclusion | Documentation typically required |

|---|---|---|---|---|

| FHA (HUD Mortgagee Letter 2023-17, Oct 2023) | Yes — actual or projected ADU rental income from the subject property may count; up to 75% of the lesser of fair-market rent or lease-agreement rent for prospective rent without prior history | No. Per ML 2023-17, ADU rental income on a one-unit-with-ADU property is ineligible for FHA cash-out refinance. | ADU rental income cannot exceed 30% of total monthly effective income | Single-Family Comparable Rent Schedule (Form 1007/1000) plus 2 months PITIA reserves |

| FHA Standard 203(k) — new ADU construction | Yes — up to 50% of proposed rental income may be used per the same ML 2023-17 rules | Not applicable (203(k) is construction financing, not standalone cash-out) | Same 30% effective-income cap | Same Form 1007 + reserves; contractor documentation per 203(k) rules |

| Fannie Mae HomeStyle Renovation | Yes for purchase or limited cash-out refinance only; ADU rental income rules apply per Fannie’s ADU policy in Selling Guide | Not eligible — HomeStyle Renovation is purchase or limited cash-out refinance only; no standard cash-out option | Per agency rental-income inclusion rules | Form 1007 and applicable Fannie documentation |

| Fannie Mae standard cash-out refinance | Not applicable (this is a cash-out product) | Subject to Fannie’s specific ADU policy — generally limited to defined scenarios and capped per Selling Guide rules | Per agency rental-income rules | Standard documentation |

| Freddie Mac CHOICERenovation | ADU rental income treatment applies in defined purchase and no-cash-out scenarios with documentation and caps | Verify with lender — Freddie’s ADU policy differs in technical detail from Fannie’s | Per agency rental-income rules | Per Freddie Mac Single-Family Seller/Servicer Guide |

Five questions to ask your specific lender in writing:

- For my exact loan type and occupancy, can projected ADU rent count toward DTI?

- If yes, at what percentage of fair market rent, and is there a cap as a percentage of effective income?

- What appraisal form is required (typically Form 1007)?

- Does the answer change if I switch from purchase/limited-cash-out to standard cash-out?

- What reserves are required at closing if I use rental income to qualify?

Get the answer in writing before relying on rental income for qualification. These projections are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

What if neither RenoFi nor cash-out refinance works?

If neither path fits, you still have viable options: a standard HELOC, a home equity loan, Fannie Mae HomeStyle Renovation, Freddie Mac CHOICERenovation, FHA 203(k), a construction-to-permanent loan, phased ADU construction, or delaying until rates or your equity position improve.

| Alternative product | Value basis | Loan purpose available | First-mortgage impact | ADU fit | Key disqualifier |

|---|---|---|---|---|---|

| Standard HELOC | Current value | Any | None (sits behind it) | Best when current equity covers project | Insufficient current equity |

| Standard home equity loan | Current value | Any | None | Fixed-rate version of standard HELOC | Insufficient current equity |

| Fannie Mae HomeStyle Renovation | As-completed appraised value | Purchase or limited cash-out refinance only — no standard cash-out; borrower may not receive cash back at closing | Replaces first mortgage | LTV up to 97% on one-unit primary; covers ADU per Selling Guide B2-3-04 | No cash back permitted; renovation cost cap of 75% per Fannie’s product matrix |

| Freddie Mac CHOICERenovation | As-completed value | Purchase or no-cash-out refinance | Replaces first mortgage | Eligible for ADU under Freddie ADU policy | Same as HomeStyle — no standard cash-out, terms and contractor requirements differ |

| FHA 203(k) Standard or Limited | As-completed value | Purchase or refinance | Replaces first mortgage | Lower credit-score thresholds; 203(k) Standard can fund larger projects | Stricter contractor and improvement-type rules; specific ADU eligibility per program |

| Construction-to-permanent loan | As-completed value | New construction financing | Replaces first mortgage at conversion | Strong for larger detached ADU builds | Builder approval process; less practical for small conversions |

| Phased construction or smaller scope | n/a | n/a | n/a | Reduce ADU size/scope to fit a smaller loan | Project timeline extends |

The strongest substitute for RenoFi when ARV-based borrowing is what you need but RenoFi isn’t available in your state is Fannie Mae HomeStyle Renovation, with one critical caveat the marketing language often glosses over: HomeStyle is purchase or limited cash-out refinance only. The borrower may not receive any cash back at closing in any amount. Funds are used for the renovation itself; excess funds are applied as a principal curtailment or reimbursed for documented additional renovation costs. If you wanted a true cash-out refi against future value, HomeStyle is not a substitute.

ADU costs in 2026: what you’re actually financing

Understanding what an ADU actually costs is essential to picking the right loan size. National averages run $150–$300 per square foot in 2026 per Angi, with total project costs averaging around $180,000 and a common range of $40,000–$360,000.

| Region | Cost per sq ft (2026) | Typical total project | Source |

|---|---|---|---|

| California — Bay Area, LA, San Diego | $300–$500+ | $150,000–$400,000+ | BFPM (April 2026) |

| California — Los Angeles detached ADU | Reflected in range below | $219,000–$459,000 | CALI ADU (April 2026) |

| California — Los Angeles garage conversion | Reflected in range below | $140,000–$245,000+ | CALI ADU (April 2026) |

| California — JADU through detached/prefab range | Varies by type | $80,000–$400,000+ | Andalusia Drafting (Feb 2026) |

| National average | $150–$300 | ~$180,000 (range $40K–$360K) | Angi (May 2026) |

Soft costs to budget on top of construction: design and architectural fees (typically around 10–15% of project cost per Angi), permit fees (California permit examples around $10–$12 per sq ft per Angi), utility connections if detached, site work, and a contingency (10–15% is a common construction-industry rule of thumb). Get itemized estimates from contractors before sizing your loan.

Questions to ask before applying to RenoFi or a cash-out refinance lender

Before submitting any application, get answers in writing to the following 15 questions. The goal is to confirm the product actually solves your problem.

- Are you the lender, the broker, a marketplace, or a technology platform?

- Does this product replace my first mortgage or sit behind it?

- Is the borrowing limit calculated against current appraised value, or after-renovation value?

- What’s the LTV or combined LTV (CLTV) cap for my state and occupancy type?

- Is this exact product available in my state?

- What appraisal is required — standard, comparable rent schedule (Form 1007), or as-completed?

- What happens to my borrowing limit if the as-completed appraisal comes in below the projected ARV?

- Can projected ADU rental income count toward my DTI, and if so at what percentage and cap?

- Are plans, permits, or a signed contractor contract required before closing?

- Are there construction draw inspections or milestone disbursements I need to plan around?

- What fees apply before approval (appraisal, application, processing)?

- What total closing costs apply at funding?

- Can the loan fund design fees, permit fees, utility connections, and site work — or only construction?

- What happens if my project cost exceeds the loan amount?

- Is there a prepayment penalty? An early payoff fee on a HELOC?

Bring this list to every lender conversation. The answers will tell you immediately whether the product is a fit.

Includes the 15-question lender checklist, ADU budget worksheet, and project-scope notes — built to bring to your first contractor and lender meetings. Email-gated; unsubscribe anytime.

Methodology: how we built this comparison

Dwelling Index compared RenoFi-style after-renovation-value financing and traditional cash-out refinancing using primary product disclosures, agency lending guidance, current rate-context sources, ADU cost references, and homeowner voice-of-customer research. Editorial conclusions are based on the financing problem each path solves, not on compensation.

Source hierarchy

- Official RenoFi product pages (renofi.com/how-it-works, /, /loans, /home-loans/home-equity-loan, /mortgage-refinancing/renofi-refi-cashout-refinance-for-renovation, /faq, /realtor, /notices/licenses) for product descriptions, max loan amounts, LTV ratios, state-disclosure language, and stated eligibility.

- Bankrate’s RenoFi review dated February 27, 2026 for state availability and lender comparison context.

- LendEDU RenoFi Review updated May 1, 2026 for product structure detail.

- Fannie Mae Single-Family Selling Guide (selling-guide.fanniemae.com) for HomeStyle Renovation rules (B5-3.2-01, B5-3.2-02), cash-out refinance eligibility (B2-1.3-03), limited cash-out (B2-1.3-02), and ADU policy (B2-3-04).

- Freddie Mac Primary Mortgage Market Survey (freddiemac.com/pmms) for the 30-year fixed-rate benchmark of 6.36% as of May 14, 2026.

- HUD Mortgagee Letter 2023-17 (Oct 16, 2023) for FHA ADU rental income and cash-out treatment rules.

- California Government Code Chapter 13 (sections 66310–66342) for ADU and JADU statutory definitions, accessed via Justia/FindLaw and the California HCD ADU Handbook (March 2025 update).

- IRS Publication 936 for home mortgage interest deductibility limits.

- Texas Constitution Article XVI §50(a)(6) for Texas home-equity lending rules.

- Industry voice-of-customer research from BiggerPockets and Reddit/r/RealEstate community discussions, used only for searcher phrasing — not for financing claims.

- California-specific ADU cost data from CALI ADU (April 2026), BFPM (April 2026), and Andalusia Drafting (Feb 2026).

- National ADU cost data from Angi (May 2026).

What we did not assume

- We did not assume RenoFi is available in every state.

- We did not assume RenoFi is automatically better than a cash-out refinance.

- We did not assume a cash-out refinance is automatically cheaper than RenoFi.

- We did not assume projected ADU rent will count toward qualifying income.

- We did not rank any lender by payout or commission.

- We did not use product reviews as evidence for loan-term promises.

- We did not quote any specific rate, APR, monthly payment, or closing cost as a guarantee. All figures cited are national benchmarks or illustrative examples from publicly available sources as of the verification date.

What we verified

| Fact | Source | Verified date |

|---|---|---|

| 30-year fixed-rate mortgage benchmark averaged 6.36% (national, not cash-out-specific) | Freddie Mac PMMS | May 14, 2026 |

| Cash-out refinance rates generally higher than rate-and-term refinance rates | Bankrate | 2026 |

| RenoFi entity NMLS #1802847; California entity NMLS #2412747 | RenoFi.com Licenses page | May 21, 2026 |

| RenoFi is not a lender; loans are made by third-party lender partners | RenoFi.com (How It Works, footer) | May 21, 2026 |

| RenoFi lenders do not currently offer loans in Nevada | RenoFi.com (Realtor page) | May 21, 2026 |

| RenoFi site not authorized by NYDFS; no NY mortgage solicitation | RenoFi.com (homepage footer) | May 21, 2026 |

| RenoFi not available in Hawaii or Massachusetts | Bankrate RenoFi review | February 27, 2026 |

| RenoFi Texas treatment — requires direct verification | Texas Constitution Art. XVI §50(a)(6); RenoFi product pages | May 21, 2026 |

| RenoFi loan range $25,000 to $750,000 | RenoFi.com | May 21, 2026 |

| RenoFi consumer-facing ARV LTV up to 90%; wholesale programs may reach 95% case-by-case | RenoFi.com consumer + wholesale pages | May 21, 2026 |

| RenoFi Refi caps at 80% of ARV minus existing mortgage; new total mortgage capped at $2M; amounts >$600K may require additional lender review | RenoFi.com Refi page | May 21, 2026 |

| Fannie Mae HomeStyle Renovation is purchase or limited cash-out refinance only; no cash back to borrower; LTV up to 97% on one-unit primary | Fannie Mae HomeStyle product matrix | 2025–2026 |

| Fannie Mae HomeStyle Renovation December 2025 update: 50% upfront disbursement; expanded ADU eligibility | Fannie Mae Selling Guide announcement | December 2025 |

| FHA ADU rental income ineligible for cash-out refinance; allowed for purchase/rate-and-term with 75% inclusion of lesser of fair-market or lease rent; capped at 30% of total monthly effective income | HUD Mortgagee Letter 2023-17 | October 16, 2023 (verified current May 2026) |

| California ADU law codified in Government Code Chapter 13, sections 66310–66342 | California HCD ADU Handbook; FindLaw | March 2025 (codification); May 21, 2026 (verified) |

| California JADU definition: 500 sq ft of interior livable space per §66313(d) | California Government Code §66313(d) via FindLaw; California HCD | May 21, 2026 |

| California state-exempt detached ADU path under §66323 — 800 sq ft floor area | California Government Code §66323 via Justia | May 21, 2026 |

| Mortgage interest deductibility limited to buy/build/substantially-improve use per IRS Pub 936 | IRS Publication 936 | 2024 (current) |

| ADU cost in California $150,000–$400,000+; $300–$500+ per sq ft | BFPM | April 2026 |

| Los Angeles detached ADU $219,000–$459,000; garage conversion $140,000–$245,000+ | CALI ADU | April 2026 |

| National ADU average around $180,000; range $40,000–$360,000; $150–$300 per sq ft | Angi | May 2026 |

| LendEDU RenoFi Review | LendEDU | May 1, 2026 |

This page is re-verified quarterly. The next scheduled refresh is August 2026. Rate context (Freddie Mac PMMS) is checked at every refresh; if the benchmark has moved more than 50 basis points since the last verification date, the page is updated immediately. RenoFi state availability is monitored continuously via the company’s own disclosures.

Frequently asked questions

Is RenoFi a real lender?

RenoFi is not the lender. RenoFi Loans are made by third-party lender partners — some are credit unions — that use RenoFi's underwriting technology. RenoFi operates as Renovation Finance LLC DBA RenoFi (NMLS #1802847), with a California entity as Renovation Technologies Holdings Inc. (NMLS #2412747).

Does RenoFi replace my mortgage?

It depends on which RenoFi product you choose. The RenoFi Renovation HELOC and the RenoFi Renovation Home Equity Loan both sit behind your existing first mortgage as second liens — your first mortgage stays untouched. The RenoFi Refi is a first-mortgage refinance and does replace your existing mortgage.

How much can you borrow with RenoFi?

RenoFi's consumer page describes a loan range of $25,000 to $750,000 and up to 90% of after-renovation value. Some wholesale lender programs may reach 95% ARV case-by-case. Final approval depends on credit profile, DTI, LTV/CLTV after the loan, the lender partner's guidelines, and the ARV appraisal result.

What credit score do I need for a RenoFi loan?

Per Bankrate's February 2026 review, some RenoFi partner lenders accept credit scores as low as 620, though the floor is typically higher for larger loan amounts. Different lender partners set different minimums.

Is RenoFi available in Nevada, New York, or Texas?

RenoFi's own materials state that RenoFi lenders do not currently offer loans for properties in Nevada, and that the RenoFi site is not authorized by the New York State Department of Financial Services for New York mortgage solicitation. Texas treatment depends on the specific RenoFi product and lender partner under Texas Constitution Article XVI §50(a)(6) home-equity rules — verify with RenoFi directly before paying for an appraisal.

Is RenoFi available in California?

Yes — RenoFi operates in California through its California entity, NMLS #2412747. California permits ADUs up to specific size limits under Government Code Chapter 13 (sections 66310–66342), with §66323 providing a state-exempt detached ADU path up to 800 square feet and local ordinances commonly allowing detached ADUs up to 1,200 square feet.

What's the difference between the RenoFi Refi and a traditional cash-out refinance?

Both replace your existing first mortgage with a new, larger one. The difference is what the loan is written against. A traditional cash-out refi uses your home's current appraised value (typically 80% LTV minus your balance). The RenoFi Refi uses your home's projected after-renovation value (up to 80% of ARV minus your balance), which on an ADU project typically lends materially more.

Will I pay for an ARV appraisal even if I'm not approved?

Yes. RenoFi discloses on its How It Works page that you pay for the appraisal up front and that approval is not guaranteed. If you're declined for credit, DTI, or other reasons after the appraisal, the appraisal cost is generally not refundable.

Can I use a cash-out refinance to build an ADU?

Yes. Cash-out refinance proceeds can be used for any purpose, including ADU construction, under Fannie Mae's cash-out refinance guidelines in Selling Guide B2-1.3-03. The constraint is borrowing power — most cash-out refis cap at 80% of current value minus your existing balance, which often leaves a shortfall for ADU projects when the homeowner has limited current equity.

What's the current cash-out refinance rate in 2026?

Cash-out refinance rates vary by lender, credit profile, LTV, loan amount, occupancy, and current market conditions. The Freddie Mac PMMS 30-year fixed benchmark was 6.36% on May 14, 2026 — this is a national purchase-loan benchmark, not a cash-out quote, and cash-out rates are generally higher per Bankrate. Your specific quote depends on your individual scenario; request live quotes from multiple lenders.

How long does a RenoFi loan take to close?

Bankrate's February 2026 review flags the ARV appraisal process as RenoFi's primary tradeoff — longer than a standard HELOC where a current-value appraisal is faster. RenoFi's own wholesale material references possible 30-day closings depending on lender and documentation; confirm the expected timeline with your assigned lender partner once matched.

Can projected ADU rental income help me qualify?

It depends on the loan program, and the rules differ sharply between programs. FHA explicitly does not allow ADU rental income on cash-out refinances per HUD Mortgagee Letter 2023-17, but does allow it on purchase and rate-and-term refis up to 75% of the lesser of fair-market or lease rent, capped at 30% of total monthly effective income. Fannie Mae HomeStyle Renovation is purchase or limited cash-out only — no standard cash-out, no cash back to borrower. Standard cash-out refinance programs apply Fannie's specific ADU rental-income rules. Confirm in writing with your specific lender before relying on projected rent.

What happens if the after-renovation appraisal comes in below the projected ARV?

Your borrowing room shrinks proportionally. The lender will lend against the lower appraised ARV, not the figure you originally projected. You'll then either need to reduce the ADU scope to fit the smaller loan, bring more cash to closing, choose a different product, or appeal the appraisal. This is the single most common cause of RenoFi-style financing failing late in the process — manage it by working with an experienced contractor whose scope of work is documented and whose comparables are defensible.

Does RenoFi work for a garage conversion ADU?

Yes, in principle. RenoFi's own materials reference ADUs and garage conversions as eligible renovation projects. The practical question is whether the conversion creates enough after-renovation value to justify the ARV appraisal and underwriting process. For a smaller garage conversion in the $80,000–$120,000 range, a standard HELOC at your current bank may close faster and cheaper.

Is RenoFi legit?

RenoFi is a licensed mortgage broker operating since 2018, with publicly disclosed NMLS licenses. It has raised institutional venture capital, including a Series B round led by Fifth Wall in 2024. Its loans are funded by third-party lender partners that hold their own state and federal lending licenses. The product is legitimate; the question for any individual borrower is whether it's the right fit for their state, project, equity position, and first-mortgage situation.

A note on what we’re routing you to, and what we’re not

We get paid when readers explore cash-out refinance options through our research partner Mortgage Research Center, and we tell you this clearly above and below the CTA. We do not currently have an active affiliate relationship with RenoFi, which means we earn nothing when you go directly to RenoFi.com. That asymmetry matters for your trust, so here’s how we handle it:

When the math on this page says RenoFi is the right product for your situation — particularly the second-lien Home Equity Loan or HELOC versions for a homeowner protecting a sub-5% first mortgage — we tell you that even though we don’t get paid for that recommendation. When the math says a cash-out refi is the right product, we route you to our partner because that’s the financially correct path for that borrower, not because of the compensation. Honest answers first; lane choice second.

If RenoFi becomes a tracked partner in the future, we’ll update this page’s disclosure and recommendation language accordingly.

Not sure where to start? See what’s possible at your address — get your free ADU report in 60 seconds.

Get Your Free ADU Feasibility Report