ADU Grant Paused? Here Are the Financing Alternatives That Actually Work in 2026

By The Dwelling Index Editorial Team · · Last verified May 26, 2026 · 26-min read

Independent ADU resource · Not a lender or broker · Editorial standards →

Bottom line, up front

If your ADU grant is paused, don’t put your project on hold waiting for it, and don’t build your budget around it. For the grant most people mean — California’s CalHFA ADU Grant — the program has been fully allocated since December 28, 2023, with no confirmed relaunch date — and CalHFA’s own page warns that anyone offering to “help you get” the grant is running a scam.

A handful of state and city programs are still open or briefly accepting applications (Massachusetts, New York City, San Diego, Vermont, Boston), but most verified programs are geographically, income-, or covenant-restricted. Your fallback plan can’t rely on a grant alone.

Your fastest safe next step: confirm your lot can legally support an ADU, identify your one binding constraint — equity, a low first-mortgage rate, monthly-payment tolerance, or needing rental income to qualify — then test the single financing lane that matches it. (Source: CalHFA.ca.gov/adu, verified May 26, 2026.)

Grant closed? Start here.

You searched for a grant, found out it’s not available, and now you’re stuck between “wait and hope” and “take on debt I didn’t plan for.” This table is the whole decision in one screen. Find the row that sounds like you, and start with that path. Everything below explains why.

| Your situation | First path to test | Why it fits | What to watch |

|---|---|---|---|

| Your state or city still has a real program | Local program first | Subsidized money usually beats private debt | Income caps, rent covenants, owner-occupancy, waitlists |

| You have equity + a low first-mortgage rate (locked in 2020–2022) | HELOC or home equity loan | Keeps your cheap first mortgage untouched | Variable rate (HELOC); home secures the loan |

| Low current equity but strong income | Renovation or construction-to-permanent loan | Underwrites against your home’s future value | More paperwork, draws, inspections, contractor rules |

| Your existing rate is already at or above market | Cash-out refinance | One loan, large proceeds, possibly better overall rate | A bad trade if you’d lose a sub-5% rate |

| You can’t add a monthly payment | Deferred local program, HECM (age 62+), or HEI (with caution) | Avoids a required monthly payment | Future equity cost; settlement triggers; legal complexity |

| You only need soft-cost money (plans, permits) | Small HELOC draw, savings, or a documented family loan | Avoids over-borrowing for a five-figure gap | Don’t use high-cost debt casually |

| You’re not sure the ADU is even legal on your lot | Feasibility check first | Financing a non-buildable project is the expensive mistake | Zoning, setbacks, utilities, fire access |

Terms like HELOC, HEI, and construction-to-permanent are defined in plain English in the sections below.

Before you chase funding or call a single lender, check the lot. Your zoning, setbacks, utilities, and allowed ADU type decide which financing paths are even worth comparing. It’s free, takes about 60 seconds, and there’s no phone call.

Is the ADU grant actually paused right now?

For the grant most homeowners mean — California’s CalHFA ADU Grant — yes, it is closed. CalHFA’s official ADU page states that the latest round of funding was fully allocated as of December 28, 2023, that it is not accepting new applications, and that there is no confirmed relaunch date. That same page warns that anyone claiming they can help you access the grant is running a financial scam. This affects homeowners nationwide who searched for the “$40,000 ADU grant,” because the CalHFA program is the one driving almost all of that search traffic.

Here’s the timeline that matters. The CalHFA grant added a final $25 million tranche through Senate Bill 104 in 2023, the last application window opened December 11, 2023, and it was exhausted by December 28, 2023. (Sources: CalHFA.ca.gov/adu; CalHFA ADU Program Evaluation, 2025; verified May 26, 2026.)

When a government agency’s own page and a contractor’s marketing page disagree about whether a grant is “still available,” the agency wins. If you’re budgeting around money a third-party blog promised you, confirm it on the administering agency’s .gov page first — you may be planning around money that no longer exists.

What “paused,” “closed,” “fully allocated,” and “waitlist” mean

These words are not interchangeable, and the difference decides whether waiting is rational or wishful.

- Paused — Not currently taking new applications. May reopen if the legislature appropriates more money. No guarantee, no date.

- Fully allocated — Every dollar currently authorized is already committed to other applicants. This is CalHFA’s status.

- Closed — Not accepting applications, period.

- Waitlist — A program may collect your name for a future round, but a spot on a list is not funding.

- Limited — Technically open, but constrained by income caps, geography, and a small funding pool that empties fast.

What CalHFA actually paid for — and the detail almost every page gets wrong

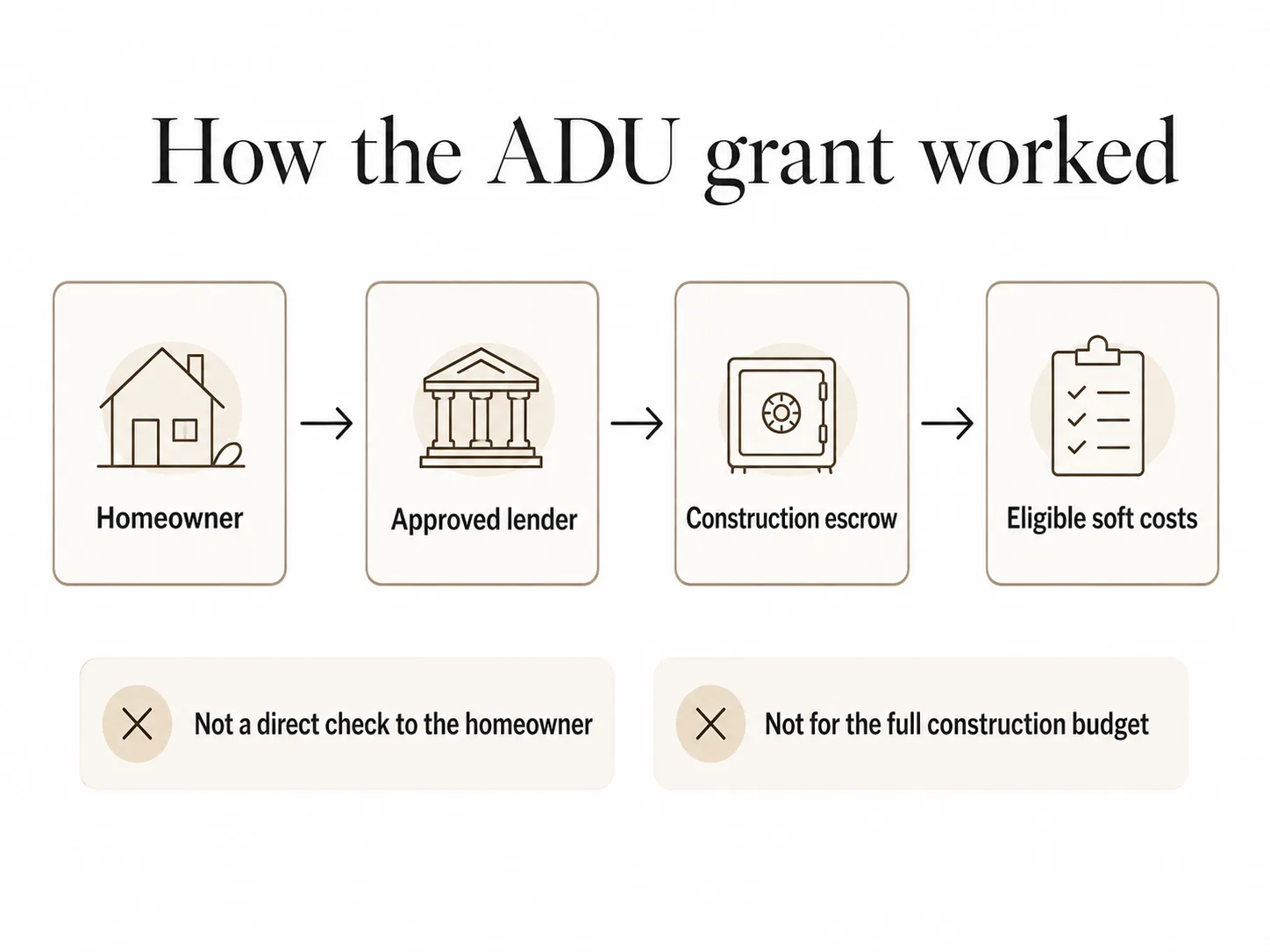

The CalHFA ADU Grant was never a check mailed to homeowners. It was up to $40,000 contributed directly into a construction escrow account through an approved lender, to reimburse eligible pre-development and non-recurring closing costs — not to fund the build itself. This is the single most misunderstood fact about the program, and it changes how you should think about any replacement.

CalHFA’s own term sheet confirms: CalHFA “will contribute up to $40,000 directly to construction escrow,” the funds flow through a participating lender rather than to you, anything you paid out of pocket up front “cannot be reimbursed as cash back” but only as a principal reduction on your construction loan, and CalHFA issues you a Form 1099-G for the year it contributes. (Source: CalHFA ADU Grant Program Term Sheet, calhfa.ca.gov; verified May 26, 2026.)

What the grant could cover (eligible soft costs):

- Architectural and design drawings

- Permit and plan-review fees

- Impact and development fees (often the biggest soft cost in high-fee cities)

- Soil tests and property surveys

- Energy reports and compliance documentation

- Utility hookups

- Construction-loan interest-rate buydowns

What still needed separate funding (the build itself):

- The actual construction labor and materials — the bulk of any ADU

- Major utility upgrades, meter separation, and sewer/septic work beyond the basic hookup

- Electrical panel upgrades

- Landscaping restoration after the build

- Your contingency reserve

So even at its peak, a $40,000 grant on a $200,000-plus detached ADU was a soft-cost subsidy, not a funding plan. That reframing matters more than the pause itself: if a paused grant is the only thing that made your ADU “affordable,” the project was never grant-deep underwater — it was construction-cost underwater.

What should you do first if the grant is closed?

Before applying for any loan, do three things in order: verify the program’s status on the official agency page (not a blog), confirm your property can legally support the ADU, and name your single binding constraint — equity, mortgage rate, monthly-payment tolerance, or needing rental income to qualify. The biggest, most expensive ADU mistake is borrowing money before confirming the lot is buildable. A loan does not fix zoning, setbacks, fire access, or a utility lateral that can’t carry the load.

We built this as a 72-hour plan because urgency without a sequence is exactly how anxious homeowners get scammed or over-borrow.

The 72-hour grant-pause action plan

| When | Do this | Why it matters |

|---|---|---|

| Hour 1 | Verify the official program status on the administering agency’s .gov page | Outdated blogs and scammers thrive on the gap between “the program existed” and “the program is funded right now” |

| Day 1 | Run a feasibility check on your address | Zoning, setbacks, lot coverage, height limits, and fire-zone rules decide which ADU type — and therefore which financing — is even possible |

| Day 1–2 | Decide whether you need soft-cost money (plans, permits) or construction money (the build) | Grants typically cover soft costs; loans typically cover the build. They are different problems with different solutions |

| Day 2 | Pull your current mortgage balance, your interest rate, and an estimate of your home’s value | These three numbers decide whether a second-lien path (HELOC) or a refinance even makes sense |

| Day 3 | Choose one financing lane to explore first | A single lane beats chasing five lender quotes with no framework — that’s how people stall |

Most homeowners skip straight to step three and start collecting loan quotes. Do step two first. Confirming what your lot actually allows — and which ADU type fits — is what tells you whether you need a $30,000 soft-cost gap filled or a $250,000 construction loan.

Check your property before you borrow

Confirm what’s buildable at your address before spending money on plans, permits, or lender applications.

Check What You Can Build at Your Address →Which ADU grants or subsidized loans are still open in 2026?

There is no easy nationwide ADU grant, but several state and city programs remain open or briefly accepting applications — most are subsidized loans, forgivable loans, rebates, or fee waivers rather than true cash grants, and nearly all carry income limits, geographic restrictions, and rental covenants. Treat any program you find as a bonus that lowers your total cost, not as the foundation of your budget.

We verified every row against the program’s official administering agency. Each program opens and closes on its own funding cycle — confirm intake status directly before relying on any of them.

2026 verified program-status snapshot

| Program (Geography) | Status | Type & max amount | The biggest catch | Source · verified |

|---|---|---|---|---|

| CalHFA ADU Grant (California, statewide) | ⛔ Closed | True grant, up to $40,000, paid into construction escrow for eligible soft costs | Fully allocated since Dec 28, 2023. No relaunch date. CalHFA warns of scammers offering “help” to access it. | calhfa.ca.gov/adu · May 26, 2026 |

| MassHousing ADU Loan (Massachusetts, statewide) | ✅ Open | State loan (not a grant), up to $250,000 detached / $150,000 attached | It’s a loan, not free money. Needs plans, permits, and pre-development materials in hand before applying. | masshousing.com · May 26, 2026 |

| Plus One ADU (New York City) | ⚠️ Open intake through June 12, 2026 — verify before applying | Up to $395,000 combined: a $175,000 HCR grant + $220,000 HPD loan (0–5%) | Owner-occupant of an eligible NYC home; income up to 165% AMI; property, flood, code, and compliance-period restrictions apply. | NYC HPD · May 26, 2026 |

| Plus One ADU (New York State, outside NYC) | ⚠️ Limited | Up to $125,000 total program funds — includes the local-administrator delivery fee, pre-development, and construction funds | Owner-occupied 1–4 unit primary residence; household income generally capped at 120% AMI; participating municipalities only; additional funds usually needed. | hcr.ny.gov/adu · May 26, 2026 |

| SDHC ADU Finance Program (City of San Diego) | ⚠️ Limited | Construction loan up to $250,000, 3% fixed, max 75% LTV, + no-cost technical assistance | City of San Diego only; income up to 80% AMI; owner-occupied; 680 min FICO; $2,500 fee due after approval at construction-loan closing; 7-year affordability restriction. | sdhc.org · May 26, 2026 |

| VHIP 2.0 (Vermont) | ⚠️ Regional / periodic intake — verify your county administrator & window | 0% forgivable loan, up to $50,000 per unit | Not a pure grant. Requires a 20% match (can be in-kind); rent at/below HUD Fair Market Rent or voucher amount for 5–10 years; reimbursement/milestone basis; windows vary by administrator. | Vermont ACCD · May 26, 2026 |

| Boston ADU Financial Assistance (Boston, MA) | ✅ Open | $7,500 soft-cost grant + up to $50,000 deferred 0% loan | Must attend Design and Budget workshops; must be working with a licensed architect with draft/permitted plans; income-eligible; current on all city payments. | boston.gov · May 26, 2026 |

This is not every program in the country — new ones launch and old ones close constantly. If you don’t see your area, check your city or county planning and housing department directly. For our full national tracker, see our verified ADU grants by state database.

What are the best ADU financing alternatives if a grant is paused?

The best alternative isn’t the one with the best marketing — it’s the one that solves your single binding constraint: how much usable equity you have, whether your current first-mortgage rate is worth protecting, whether you can carry a new monthly payment, and whether you need future ADU rent to qualify. There is no universal “ADU loan.” There are about nine realistic paths, and the right one is determined by your numbers, not by which lender advertises hardest.

Below, each path leads with its punchline, names who it fits, states the real downside plainly, and — because this is a grant-pause page — tells you exactly what it replaces from the grant you lost. We present these as lanes, not a ranked “best lender” list. We never sort financing by who pays us.

1. HELOC (home equity line of credit)

A HELOC is a revolving credit line secured by your home’s available equity — you draw funds as construction bills come due and pay interest only on what you’ve drawn. It’s a common ADU path for homeowners who have equity and want to keep a low first-mortgage rate, because it sits behind your existing mortgage instead of replacing it. A “HELOC” works like a credit card secured by your house: a draw period (usually 10 years) when you borrow and repay flexibly, then a repayment period (usually 20 years) of fixed principal-plus-interest payments.

- Replaces from the grant: Both the soft-cost money and the construction gap — a HELOC is flexible enough to cover plans, permits, and the build.

- Best fit: You have meaningful equity, you locked a cheap first mortgage, and your construction bills will arrive in stages.

- Bad fit: You bought recently with little equity, or you can’t tolerate a payment that rises if rates rise.

- Honest downside: Most HELOCs are variable-rate, indexed to the Wall Street Journal prime rate plus a lender margin. If prime rises during your draw period, your payment rises.

- The number that matters: As of May 24–25, 2026, Curinos reported a 7.21% national average HELOC rate, based on applicants with a minimum 780 credit score and maximum CLTV below 70%. WSJ / bank prime was 6.75%. These are benchmarks, not offers, APRs, guarantees, or your rate. (Source: Yahoo Finance / Curinos, May 24–25, 2026; Federal Reserve H.15.)

2. Home equity loan

A home equity loan gives you a fixed lump sum at a fixed rate, repaid on a set schedule, and it sits as a second lien behind your first mortgage. It fits a defined ADU budget better than a HELOC when you want one predictable payment and rate certainty. As of May 24–25, 2026, the Curinos national average fixed home equity loan rate was 7.36%, based on applicants with a minimum 780 credit score and CLTV below 70%. (Source: Yahoo Finance / Curinos, May 2026.)

- Replaces from the grant: The construction gap, as a fixed lump sum — best when you have one firm number to fund.

- Best fit: You have a firm budget and want your payment to never change.

- Damaging admission: You borrow the full amount up front, so interest accrues on the entire balance from day one — even before construction starts. For a phased build, that’s wasted interest a HELOC would avoid.

- The detail most guides miss: A HELOC and a home equity loan can be stacked — a small HELOC for early soft costs (plans, permits), a larger home equity loan for the construction draw. That mirrors how the CalHFA grant worked: soft costs first, build second.

3. Cash-out refinance

A cash-out refinance replaces your entire first mortgage with a larger one and hands you the difference in cash. It can work well when your current rate is already at or above today’s market — and it can be a costly trade if you’d give up a sub-5% pandemic-era rate. Most cash-out refis cap total borrowing around 80% of current home value.

- Replaces from the grant: The full project, as one consolidated loan — but only when the rate math works.

- Best fit: Your existing rate is similar to or higher than market, or you owe relatively little.

- The warning we won’t soften: If you locked 3.25% in 2021, replacing it to fund an ADU can cost more in extra interest over 30 years than the ADU itself. As a rule of thumb, if your existing first-mortgage rate is more than roughly 1.5 points below today’s market, use a second-lien product (HELOC or home equity loan) so only the new ADU money carries the higher rate.

Worked example (illustrative). Take a $700,000 home with a $400,000 first mortgage and a $200,000 ADU. A homeowner sitting on a 3.25% first mortgage who does a cash-out refinance of the whole $600,000 at today’s rates can pay on the order of $300,000+ more in total interest over 30 years than one who keeps the 3.25% mortgage and adds a separate second-lien product for just the $200,000. The two paths only converge when the existing rate is already near today’s market. These are illustrative figures, not an offer or a quote; actual costs depend on your exact rate, term, fees, and lender. For the full rate-by-rate model, see our ADU financing options guide.

4. Renovation loan or construction-to-permanent loan

If you don’t have enough current equity, a renovation loan or a construction-to-permanent loan can underwrite against your home’s projected after-completion value — letting you borrow against equity that doesn’t exist yet. This is the primary path for low-equity homeowners with strong income. A “construction-to-permanent” loan funds the build in staged draws tied to inspected milestones, then converts automatically into a regular mortgage when the ADU is finished.

- Replaces from the grant: The whole build, plus most soft costs — and solves the “no current equity” problem the grant never addressed.

- Best fit: Low current equity, strong income and credit, plans in hand, and a licensed, insured general contractor.

- Bad fit: You want simplicity. These require approved plans, a detailed draw schedule, lender-ordered inspections, and contractor oversight.

- The verified path facts: Fannie Mae’s ADU guidance confirms that borrowers adding an ADU can use HomeStyle Renovation financing, and those building a new one-unit property with an ADU can use construction-to-permanent financing; HomeStyle renovations must typically be completed within 15 months of closing. (Source: Fannie Mae Single-Family ADU page, verified May 2026.)

This is the lane most homeowners who thought they needed a grant actually need — because the grant never funded construction, and a future-value loan is the cleanest way to fund a build when your current equity is thin. If a renovation or construction-to-permanent loan is where you’re landing, the next move is to compare lenders who actually do ADU volume.

Affiliate disclosure: The Dwelling Index is reader-supported. When you use our links to explore financing options, we may earn a commission at no extra cost to you. Our recommendations are based on independent research and are never influenced by compensation.

Explore Mortgage-Backed ADU Financing Options → (via Mortgage Research Center)

Compare education-first paths — HELOCs, home equity loans, cash-out refinancing, and construction-to-permanent loans. Terms, approval, rates, and payments depend on lender underwriting; nothing here is a guaranteed offer.

5. FHA 203(k) and the agency rules on counting ADU rent

An FHA 203(k) renovation loan can fund ADU conversions and additions, and projected ADU rent can sometimes help you qualify — but only under specific, documented rules that differ by agency. Never assume future rent automatically boosts your qualifying income. HUD Mortgagee Letter 2023-17 (effective October 16, 2023) expanded the Standard 203(k) program to include eligible ADU conversions and additions.

The agency rules, in plain English:

- FHA: Under Standard 203(k), prospective ADU income with no rental history is calculated at 50% of the lesser of appraiser-supported fair-market rent or the lease/rental-agreement amount. FHA ADU rental income cannot be used to qualify for a cash-out refinance. (Source: HUD Mortgagee Letter 2023-17.)

- Fannie Mae: Since the Desktop Underwriter 12.1 release (March 2026), it automates ADU rental-income qualification on eligible purchase and limited cash-out refinance transactions for one-unit principal residences — using 75% of gross rent, capped at 30% of total qualifying income. (Source: Fannie Mae Selling Guide B3-3.8-01; Announcement SEL-2025-08.)

- Freddie Mac: Qualifying ADU rental income cannot exceed 30% of total qualifying income, rent from an illegal ADU may not be used, and a CHOICERenovation limitation effective May 4, 2026 bars using rent from a unit funded by renovation proceeds to qualify. (Source: Freddie Mac Single-Family ADU page.)

Illustrative example. A borrower with $6,000/month qualifying income and an ADU renting at $2,500/month: the lender takes 75% of $2,500 = $1,875, checks it against the 30% cap (≈$2,571), and uses the smaller figure — $1,875 — lifting qualifying income to $7,875. These are illustrative examples, not guarantees of returns. Actual results depend on local market conditions, construction costs, financing terms, and regulatory approvals.

6. Local subsidized loans and deferred programs

If a local program from the snapshot above fits your geography and income, compare it before private debt — subsidized rates and deferred or forgivable structures can beat a market-rate HELOC. But read the covenant first: rent caps, owner-occupancy rules, affordability periods, and repayment triggers are the real cost. Boston’s $7,500 grant plus $50,000 deferred 0% loan, San Diego’s $250,000 construction loan at 3% fixed, and Vermont’s $50,000 forgivable loan are all meaningfully cheaper than private debt — if you can live with the strings.

- Replaces from the grant: This is the closest replacement for the grant you lost — subsidized money with conditions, rather than market-rate debt.

7. Home equity investment (HEI)

A home equity investment (HEI) — sometimes called a home equity agreement — gives you cash now in exchange for a share of your home’s future value, with no required monthly payment. It can solve the “I can’t carry another payment” problem, but it replaces a monthly-payment problem with a future-settlement problem. You typically settle in 10–30 years, or earlier if you sell or refinance, by buying back the investor’s share including its slice of appreciation.

- Replaces from the grant: A cash infusion without a new monthly payment — useful when income, not equity, is the constraint.

- Best fit: You can’t take on a monthly payment, your credit keeps you from a HELOC, and you have a clear medium-term exit. HEIs are state-restricted — confirm your state is served.

- The caution we’re required to give: The Consumer Financial Protection Bureau describes home equity contracts as a complex, hard-to-compare category that can require a large, hard-to-predict future lump-sum repayment tied partly to your home’s value. (Source: CFPB, Home Equity Contracts Market Overview.) Consider a financial advisor or real estate attorney before signing.

- The detail most guides miss: Some HEI contracts use a discounted or adjusted starting home value, which changes both your payout and your settlement math. The CFPB gives an example of a 30% starting-value adjustment. Always ask for the net payout after all fees, the starting value used, the adjustment applied, and the exact settlement formula.

We do not place an affiliate link here. HEI providers require state-by-state availability verification before we route you to one.

8. HECM (reverse mortgage), for owners 62+

A Home Equity Conversion Mortgage (HECM) is an FHA-insured reverse mortgage for homeowners 62 and older that can fund an ADU without a required monthly payment. “No monthly payment” is not “no cost,” and it carries real foreclosure risk if obligations aren’t met. HECM borrowers must keep paying property taxes, homeowners insurance, and any HOA fees and maintain the home — the CFPB warns that failing to meet those obligations can trigger default and foreclosure even with no mortgage payment. (Source: CFPB, reverse mortgage rights and responsibilities.) Best fit: an equity-rich owner aging in place — including the multigenerational “house my parents on the property” use case. Model the total cost over your expected hold and compare it directly to a HELOC.

9. Personal loan, savings, documented family loan, or phased scope

For a small soft-cost gap — plans, permits, a survey — savings, a documented family loan, or a modest personal loan can be cleaner than over-borrowing against your house. They are not a way to fund a six-figure build. If family money is involved, put it in writing and check the gift/loan tax implications. Avoid funding an ADU on credit cards beyond tiny, immediately repayable expenses — credit-card interest will eat any rental upside.

- Replaces from the grant: The soft-cost piece specifically — which is exactly what the CalHFA grant covered. If your only gap is the $10,000–$30,000 of pre-development cost, this is your lane.

Which fallback path fits your situation?

Start with your binding constraint, not the product name. The same homeowner who should not start with a cash-out refinance (because they have a 3% mortgage) may be a perfect fit for a HELOC — and a low-equity homeowner who can’t use either may be ideal for a construction loan. Match the path to the constraint and most of the confusion disappears.

| Your binding constraint | Start here | Be careful with / usually skip |

|---|---|---|

| Low first-mortgage rate + equity | HELOC or home equity loan | Cash-out refinance |

| Low current equity + strong income | Renovation or construction-to-permanent loan | Standard home equity loan (not enough room) |

| You need ADU rent to qualify | Agency path with documented rent rules (Fannie DU 12.1 / FHA 203(k)) | A plan that assumes 100% of rent counts |

| You can’t carry a monthly payment | Deferred local program → HECM (62+) → HEI (with caution) | HELOC, home equity loan, cash-out refi |

| A city/state program fits you | The program first | Private debt before checking restrictions |

| Soft-cost gap only | Small HELOC draw, savings, documented family loan | A large refinance for a small need |

| ADU legality uncertain | Feasibility check first | Any loan application on an unverified project |

The single thread running through every row: your financing path changes the moment you learn what your lot actually allows. If it only supports a garage conversion, if utilities need upgrades, or if local rules block the ADU type you planned, the right lane shifts. Confirm that before you compare loans.

Should you wait for the ADU grant to reopen?

Wait only if your timeline is genuinely flexible, you haven’t yet paid for design work, and you are not depending on unconfirmed funding to make the project affordable. If a paused grant is the only thing that turns “unaffordable” into “affordable,” the honest answer is that your ADU isn’t finance-ready yet — and that’s far better to learn before you spend on plans, permits, or loan fees.

We’ll give you the real damaging admission here, because you deserve it: an ADU is not a fast or frictionless project. But here’s the hope, and it’s grounded: ADUs were built for years before any grant program existed, and the financing ecosystem is broader and more accessible now than it has ever been. A closed grant delays a subsidy. It does not cancel your project.

When waiting makes sense

- You’re in early research and haven’t paid for design.

- Your local program has a clear, published reopening date.

- Your build isn’t tied to an urgent family-housing need.

- You can keep your options open cheaply.

When waiting is the expensive choice

- You have aging-parent or adult-child timing pressure.

- You’re counting on rental income to start soon.

- Permit or design costs are already underway.

- Your program has no official reopening — only hope.

- Construction-cost inflation or worsening site conditions could grow your budget while you wait.

What scams and bad advice should you avoid?

Walk away from anyone who guarantees access to a closed ADU grant, asks for money to “hold your place,” tells you to hide the ADU from a lender or permit office, or pushes you into a loan before confirming your lot is buildable. CalHFA explicitly warns that anyone offering to help you get its ADU grant is attempting a scam. A grant pause is exactly the moment predators exploit, because anxious searchers are easy targets.

Do not pay an unaffiliated consultant, caller, or contractor to “hold your place” or guarantee grant access. Legitimate programs may have official, disclosed application, commitment, closing, or lender fees — San Diego’s SDHC program, for example, has a documented $2,500 application fee due at construction-loan closing — but those appear in the administering agency’s or lender’s own documents, never in a cold promise to secure closed grant funds.

The red flags, in the words they actually use:

- “We can still get you the CalHFA grant.” (The program is closed. This is the scam CalHFA named.)

- “Pay us a fee and we’ll get you on the list.”

- “You don’t need permits — just call it a remodel.”

- “Just refinance, it always works out.” (It doesn’t, if you have a low rate.)

- “Future rent will definitely qualify you.” (Agency caps say otherwise.)

- “No monthly payment means no cost.” (HEIs and HECMs have real back-end costs.)

- “Put it on credit cards until the rent starts.”

If anyone gives you names or numbers claiming grant access, CalHFA asks you to forward them to marketing@calhfa.ca.gov. (Source: CalHFA.ca.gov/adu, verified May 26, 2026.)

What documents will a lender or program ask for?

Expect to gather property, mortgage, income, project, contractor, and permit documents — and expect local programs to demand more upfront readiness than homeowners anticipate. Knowing the list in advance is how you avoid gathering 15 documents only to discover a single disqualifier.

| Path | Likely documents | The catch that surprises people |

|---|---|---|

| Local grant / subsidized program | Owner-occupancy proof, income verification, mortgage status, taxes, insurance, plans, permit readiness, program forms | MassHousing wants plans, permits, and pre-development materials in hand before you apply |

| HELOC / home equity loan | Mortgage statement, income docs, credit authorization, property valuation, title/lien review | Lenders want 680+ credit for the best pricing |

| Cash-out refinance | Full mortgage application, appraisal, income docs, payoff statement, title | You’re re-underwriting your entire mortgage, not just the new money |

| Renovation / construction-to-perm loan | Approved plans, permits, contractor bid, draw schedule, inspection access, appraiser support for as-completed value | The appraisal needs your plans + contractor bid before it can issue an as-completed value |

| Using ADU rent to qualify | Appraisal, rent schedule (Form 1007), lease or market-rent documentation, eligible transaction type | Caps apply (Fannie 30%; FHA 50% on prospective 203(k) rent) — and never on FHA cash-out |

| Local program (city-specific) | Same as above, plus program-specific prerequisites | Boston requires a licensed architect, two contractor quotes, and completed Design + Budget workshops; SDHC requires a 680 score and a $2,500 fee at closing; NY State Plus One’s $125,000 includes the administrator fee |

| Family loan | Written agreement, gift/loan documentation, tax/estate review if relevant | Undocumented family money can create tax and lender-seasoning headaches |

What we verified for this guide

What we verified — last checked May 26, 2026

- CalHFA ADU Grant status — fully allocated since Dec 28, 2023; no relaunch date — and the official scam warning (calhfa.ca.gov/adu)

- CalHFA grant mechanics — up to $40,000 paid into construction escrow through a lender, eligible soft costs (incl. utility hookups) only, Form 1099-G issued (CalHFA ADU Grant Term Sheet)

- MassHousing ADU Loan amounts and the readiness requirement (masshousing.com)

- NYC Plus One ADU — $175,000 HCR grant + $220,000 HPD loan = up to $395,000; 165% AMI cap; intake window through June 12, 2026

- NY State Plus One — $125,000 total including LPA fee; 120% AMI; 1–4 unit owner-occupied (hcr.ny.gov)

- San Diego SDHC — construction loan up to $250,000, 3% fixed, 75% LTV, 80% AMI, 680 FICO, $2,500 fee at closing, 7-year affordability (sdhc.org)

- Vermont VHIP 2.0 — $50,000 0% forgivable loan, 20% match, FMR covenant, regional/periodic intake (Vermont ACCD)

- Boston ADU Financial Assistance — $7,500 grant + $50,000 deferred 0% loan and prerequisites (boston.gov)

- Fannie Mae ADU HomeStyle and construction-to-permanent paths and DU 12.1 rental-income rule; Freddie Mac 30% cap and May 4, 2026 CHOICERenovation limit; FHA HUD ML 2023-17

- CFPB cautions on home equity contracts (HEIs) and HECM obligations

- Benchmark rates — Curinos HELOC 7.21% / home equity loan 7.36% (min 780 FICO, <70% CLTV); WSJ prime 6.75% (May 24–25, 2026)

What we did not verify and cannot: your individual approval odds, your specific rate or payment, lender availability in your area, or whether any paused grant will reopen. Confirm those directly with the administering agency or a licensed lender.

How we built the fallback matrix (methodology)

The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We do not originate loans, act as a broker, or sort financing options by compensation. This guide was built from official program pages, agency bulletins and term sheets, federal lending guidance, and current rate benchmarks.

Our rules:

- Official agency pages outrank builder blogs. When they conflict, the agency wins.

- Every program status carries a verification date.

- No “up to” dollar amount appears without its catch.

- Financing paths are sorted by homeowner constraint, never by affiliate compensation.

- No lender is ranked “best.” Rates are dated benchmarks, not offers.

- HEI and HECM products are presented with their CFPB-flagged risks.

- We include no testimonials on this page; for a money decision this consequential, official verification is stronger than an anecdote.

See our methodology, editorial standards, and affiliate disclosure.

Frequently asked questions

Is the $40,000 ADU grant still available in California?

No. CalHFA's official ADU page states the latest round of funding was fully allocated as of December 28, 2023, that the program is not accepting new applications, and that there is no confirmed relaunch date. CalHFA also warns that anyone claiming they can help you access the grant is running a scam. (Verified May 26, 2026.)

What are the alternatives if the ADU Grant Program is paused?

Start with any local program that fits your geography and income, then compare HELOCs, home equity loans, cash-out refinancing, renovation and construction-to-permanent loans, deferred local programs, and no-monthly-payment options (HEI or HECM). The right one depends on your equity, your current mortgage rate, your project stage, and whether you need ADU rent to qualify.

Should I wait for the CalHFA ADU Grant to come back?

Only if your timeline is flexible and you aren't making paid decisions based on unconfirmed funding. There is no confirmed relaunch date in CalHFA's official status. If the grant is the only thing that makes your ADU affordable, pause and re-scope before borrowing.

Was the CalHFA grant ever paid directly to homeowners?

No. CalHFA contributed up to $40,000 directly into a construction escrow account through an approved lender to reimburse eligible soft costs — it was never a cash check to the homeowner, and CalHFA issued a Form 1099-G for the amount contributed. (Source: CalHFA ADU Grant Term Sheet.)

Can I use a HELOC to build an ADU?

Often, yes, if you have enough equity and can handle variable-rate risk. A HELOC fits staged construction because you draw as bills arrive and pay interest only on what's drawn. It's secured by your home, and the rate can rise during the draw period. As of May 24–25, 2026 the Curinos national average HELOC rate was 7.21% for top-tier borrowers.

Can ADU rent help me qualify for financing?

Sometimes, under specific product and transaction rules. Fannie Mae (via DU 12.1, March 2026) allows it on eligible purchase and limited cash-out refis at 75% of gross rent capped at 30% of qualifying income; FHA allows it under HUD ML 2023-17 — including 50% of prospective rent under Standard 203(k) — but not on cash-out refis. Never assume all projected rent will count.

What if I don't have enough equity?

Look at renovation or construction-to-permanent loans, which underwrite against your home's projected after-completion value, plus any local subsidized program — or re-scope the project. Fannie Mae confirms HomeStyle Renovation and construction-to-permanent financing as ADU-capable paths.

Are ADU grants paid upfront?

Often no. Many programs are reimbursements, escrow/fund-control arrangements, deferred loans, forgivable loans, or construction draws. Always check the official term sheet for how and when money actually moves.

Are there ADU grants outside California?

Yes, but they're scattered and restricted. Verified examples include MassHousing's ADU Loan, NYC and New York State Plus One, Vermont's VHIP 2.0, Boston's ADU Financial Assistance, and San Diego's SDHC program. See the snapshot table above.

Can investors use ADU grants?

Usually not. Most programs require owner-occupancy and target income-eligible homeowners or affordable-rental creation. Check each program's owner-occupancy, income, and rental restrictions before applying.

What to do right now

If a program in your area is open and you qualify, move fast — funding is limited and competition is real. If your program is closed, waitlisted, or doesn’t exist where you live, you’re in the same position as most homeowners who successfully build ADUs every year: pick the financing lane that fits your equity and rate, confirm your lot is buildable, and proceed. And if you’re not yet sure what your property even allows, start there — it decides everything else.

Want the whole grant-pause playbook in one place? Our free 2026 ADU Starter Kit packages the grant-pause checklist, the financing-prep worksheet, and our “questions to ask before you borrow” script — the tools we didn’t have room for on this page.

See what’s possible at your address

Free ADU report in 60 seconds. No phone call.

Get Your Free ADU Report →Download the Free 2026 ADU Starter Kit

Grant-pause checklist + financing-prep worksheet. No spam.

Download the Free Starter Kit →The Dwelling Index is an independent research resource covering ADU financing, costs, and regulations. We are not a lender, broker, or builder. This page is educational and does not constitute financial, legal, tax, mortgage, or lending advice. Program availability, eligibility, rates, fees, and underwriting vary by lender, borrower, property, and location, and change without notice. Always confirm program status with the administering agency and verify ADU rules with your local planning and building department before making financial decisions.